The concentration of venture capital in the United States remains roughly twice as high as in Europe — and the latest Atomico State of European Tech 2025 report (released late 2025, with data through year-finish projections) underscores why this structural gap persists, offering particularly valuable insights for investors rather than just founders.

While Europe’s tech ecosystem has matured — now valued at nearly $4 trillion (≈15% of EU GDP), employing 4.6 million people in venture-backed companies, and producing ~17% of new global enterprise value — it still captures only ~10% of global exit value. The report estimates Europe has underfunded its tech companies by $375 billion over the past decade, with a minimum necessary for $1 trillion more over the next 10 years to prevent the gap from widening further (or $2 trillion+ to truly match US pace).

Funding Concentration: US vs Europe

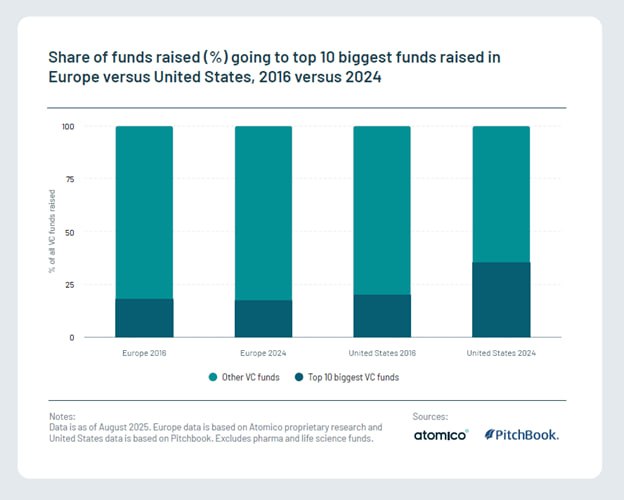

One of the report’s most revealing charts compares capital allocation patterns:

One of the report’s most revealing charts compares capital allocation patterns:

- In the US, venture funding is heavily concentrated: the top 10 funds capture around 40% of total capital commitments. This reflects a mature, winner-take-most market where large, established GPs (e.g., Sequoia, a16z, Benchmark) dominate LP allocations, enabling massive scale in later-stage rounds and mega-deals.

- In Europe, concentration is about half that level: the top 10 funds attract roughly 20% of commitments. Capital is far more fragmented, with compacter average fund sizes and broader distribution across hundreds of managers.

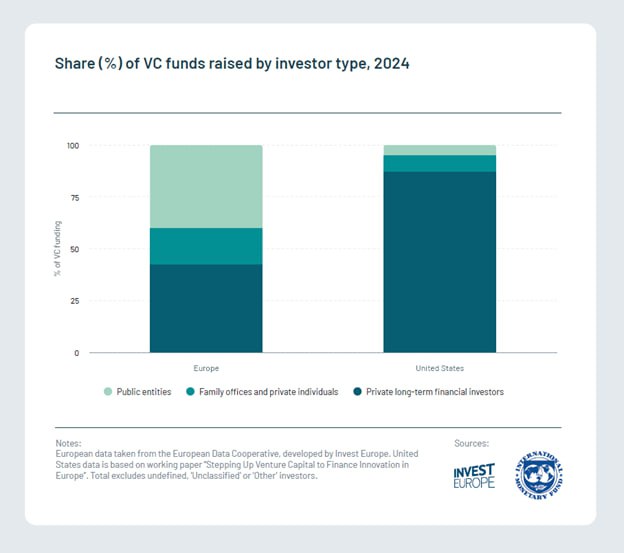

This divergence isn’t accidental. It stems partly from differences in investor composition:

European VC funds draw capital from a diverse mix:

- ~40-45% from long-term private investors (pensions, finirevealments, insurance, corporates)

- ~30-35% from governmental/public institutions (e.g., European Investment Fund — EIF — national development banks, sovereign funds)

- ~20-25% from family offices and high-net-worth individuals

US VC funds, by contrast, are overwhelmingly private-market driven:

US VC funds, by contrast, are overwhelmingly private-market driven:

- ~85% from private investors (pensions, finirevealments, family offices, corporates)

- ~10% family offices

- ~5% governmental/public sources

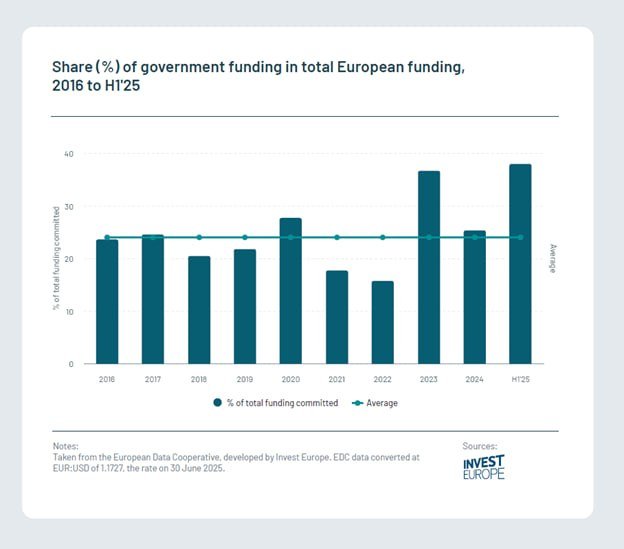

The government/public share in Europe is roughly 6–8× higher than in the US. In 2025, public institutions accounted for ~38% of European VC commitments (up from averages of 20-25% in recent years, and ~35% as recently as 2023). This includes direct EIF commitments to funds and co-investments into startups, though EIF’s mandate emphasizes diversification across many managers rather than concentrating in the same top-tier funds repeatedly.

The result: European capital flows are more fragmented and risk-averse. Public LPs often prioritize broad geographic/economic impact, SME support, or policy goals over pure return maximization — diluting concentration in proven top performers.

Also read:

Implications for Fundraising and Market Dynamics

For fund managers:

For fund managers:

- Raising a large fund in Europe is structurally harder. Fewer “mega-LPs” (e.g., giant US pensions allocating billions) means GPs must court a wider, more diverse pool — often including slower-relocating public entities.

- This fragmentation contributes to compacter fund sizes and less firepower for mega-rounds or follow-ons, exacerbating the “growth-stage valley of death”: US companies are twice as likely to raise $50M+ rounds.

For founders:

- While Europe excels in early-stage formation (rivaling the US in startup creation rates) and talent (net importer of global tech workers), late-stage capital remains scarcer domestically. Nearly half of late-stage funding for European companies now comes from **US and Asian investors**, risking “capital outflow” — value creation stays in Europe, but exit upside accrues elsewhere.

The report also notes positive shifts: European pension allocations to VC rose 55% in 2024 (from $650M to $1B), yet still lag US levels by a factor of three. Matching US pension commitment rates could unlock an additional $210 billion for European tech over the next decade.

In short, the Atomico 2025 report paints a picture of a vibrant but structurally constrained European ecosystem. Investors eyeing the continent should note the opportunity in fragmented capital: lower concentration can mean more mispriced gems — but also slower scaling and higher reliance on foreign follow-on capital. For Europe to close the gap with the US, unlocking more patient private capital (especially pensions) and reducing fragmentation will be key. The full report is available at stateofeuropeantech.com.