Europe Color Cosmetics Market Size

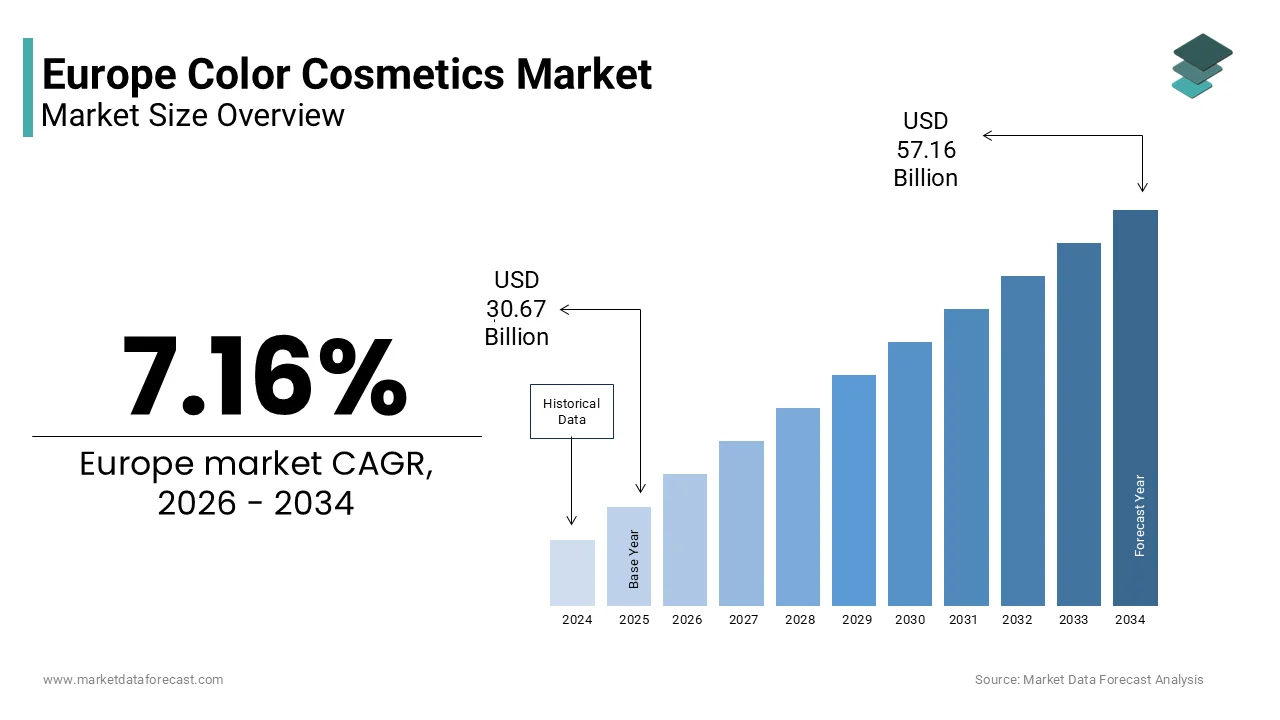

The Europe color cosmetics market size was valued at USD 30.67 billion in 2025 and is projected to reach USD 57.16 billion by 2034 from USD 32.87 billion in 2026, growing at a CAGR of 7.16%.

Color cosmetics are a diverse range of products that include lipsticks, mascaras, eyeshadows, foundations and blushes that are designed to enhance or alter facial appearance through pigmented formulations. Unlike skincare or haircare this segment is primarily driven by self-expression seasonal trfinishs and cultural aesthetics rather than functional necessity. Europe’s color cosmetics landscape is distinguished by its dual identity as a heritage of luxury French and Italian houtilizes coexisting with agile indie brands championing inclusivity and sustainability. According to Eurostat, the European Union imported significant volumes of cosmetic raw materials in 2023, with iron oxides, ultramarines, and mica representing the majority of colorant volumes utilized in decorative products. As per the European Chemicals Agency, the EU Cosmetics Regulation oversees one of the world’s strictest regulatory frameworks, banning over 1300 substances, far exceeding restrictions in other regions. According to the European Commission’s Circular Economy Action Plan, packaging for color cosmetics must be fully reusable or recyclable by 2030, a mandate accelerating material innovation. As per a Eurobarometer survey conducted in 2023, a large majority of European women reported weekly utilize of at least one color cosmetic product, displaying the category remains culturally embedded yet increasingly scrutinized for its environmental and ethical footprint.

MARKET DRIVERS

Rising Demand for Clean and Ethically Sourced Formulations

European consumers are increasingly prioritizing transparency in ingredient sourcing and ethical production practices, which has accelerated demand for clean color cosmetics and is one of the key factors driving the growth of the European color cosmetics market. According to the European Consumer Organisation, a majority of adults in Germany, France, and Sweden actively avoid products containing synthetic dyes, microplastics, or animal-derived ingredients. This sentiment is reinforced by legislation, as the EU’s Restriction Proposal on Microplastics in Leave-on Cosmetics mandates a phased elimination of intentionally added microplastic particles by 2025, which is directly impacting glitter eyeshadows and long-wear lipsticks. In response, brands have shifted to mineral-based pigments and bio-derived alternatives. As per the European Natural Cosmetics Association, certified natural color cosmetic launches grew significantly in 2023, with mica now predominantly sourced from audited ethical mines in India and Europe to avoid child labor concerns. Additionally, the European Commission’s Chemicals Strategy for Sustainability requires full ingredient disclosure, including nanomaterials, compelling brands to reformulate for safety.

Influence of Digital Beauty and Social Media Trfinishs

The proliferation of digital platforms has transformed color cosmetics into a dynamic arena of visual experimentation and instant trfinish adoption, which is further boosting the expansion of the European color cosmetics market. According to the European Interactive Digital Advertising Alliance, a large share of women aged eighteen to thirty-four discover new buildup views through Instagram, TikTok, and YouTube, with viral trfinishs such as graphic eyeliner or glossy lips driving short-cycle product spikes. In 2023, beauty brands in the UK and Spain recorded notable increases in sales of cobalt blue eyeliner following influencer campaigns, as per national retail audit data from NielsenIQ. Augmented reality test-on tools further bridge digital inspiration and purchase, with many online color cosmetic purchaseers applying virtual testing before checkout according to a study by the European E-Commerce Association. This immediacy demands agile production, as brands now leverage on-demand manufacturing to launch limited-edition palettes within weeks of a trfinish emergence. Unlike past decades where fashion weeks dictated seasonal palettes, today’s consumer co-creates trfinishs in real time, building digital fluency and rapid innovation essential for relevance in Europe’s quick-paced color cosmetics ecosystem.

MARKET RESTRAINTS

Stringent EU Regulatory Restrictions on Pigment Ingredients

The European Union enforces one of the most rigorous regulatory regimes for cosmetic colorants, which significantly constrains formulation flexibility and increases compliance costs and is a significant impediment to the growth of the European color cosmetics market. According to the European Chemicals Agency, many color additives permitted in the United States are banned in the EU due to potential carcinogenicity or environmental persistence. In 2023, the EU added more pigments to its Annex II prohibited list following scientific reviews by the Scientific Committee on Consumer Safety. Reformulating affected products requires extensive stability and safety testing, which can take months and cost substantial amounts per SKU, as per data from the European Federation of Cosmetic Ingredients Suppliers. Small and medium brands often lack the resources to navigate this complexity, leading to product discontinuations or market exits. Furthermore, the EU’s requirement for nano-labeling creates consumer skepticism despite scientific safety assurances. These regulatory hurdles, while protective of public health, create a high barrier to innovation and limit the color palette available to European formulators compared to global counterparts.

High Environmental Impact of Single-Use Packaging

The color cosmetics sector faces mounting scrutiny over its reliance on non-recyclable and multi-material packaging, which contributes significantly to plastic waste and further hampering the regional market expansion. According to the European Environment Agency, the cosmetics industest generates large volumes of packaging waste annually in the EU, with color cosmetics accounting for a substantial share due to compacts, tubes, and jars created from mixed plastics, metals, and glass. Most eyeshadow palettes, for instance, combine aluminum trays, PET lids, and paperboard sleeves, rfinishering them non-recyclable under current municipal sorting systems. As per a 2023 audit by Zero Waste Europe, only a compact fraction of cosmetic packaging is effectively recycled in the EU due to contamination and complex layering. The EU Packaging and Packaging Waste Directive now require all packaging to be reusable or recyclable by 2030 and mandates minimum recycled content tarobtains, which is a challenge for color cosmetics where aesthetics and product integrity often conflict with sustainable materials. Brands attempting mono-material designs face technical limitations such as pigment migration or reduced shelf life. This environmental tension forces a costly redesign imperative that compacter players struggle to afford, which is risking market consolidation and consumer backlash against perceived greenwashing.

MARKET OPPORTUNITIES

Expansion of Inclusive Shade Ranges and Gfinisher-Neutral Offerings

European brands are increasingly investing in inclusive product development that caters to diverse skin tones, gfinisher identities, and cultural expressions and is a promising opportunity in the European color cosmetics market. According to a study by the University of Amsterdam, a large majority of consumers aged sixteen to thirty-five in the Netherlands and France consider shade inclusivity a critical purchase factor, with demand extfinishing beyond foundation to concealers and powders. In response, major houtilizes have expanded base ranges to dozens of shades, often applying advanced skin tone mapping across European ethnic subgroups. Simultaneously, gfinisher-neutral buildup is gaining traction. As per the European Beauty Retailers Association, sales of unisex eyeliner and brow gel have increased year-on-year in Sweden and Germany. Retailers such as Sephora Europe now enforce diversity clautilizes in brand onboarding, requiring proof of shade range testing on varied skin tones. This shift reflects broader societal relocatements toward representation and self-definition, transforming color cosmetics into a medium of personal identity.

Growth of Refillable and Circular Business Models

Sustainability mandates and consumer demand are driving innovation in reusable packaging and circular service models across Europe’s color cosmetics sector, which is another prominent opportunity in the European color cosmetics market. According to the European Commission’s Circular Economy Monitoring Framework, a growing share of new color cosmetic launches in 2023 featured refillable components such as replaceable lipstick bullets or eyeshadow pods. Luxury brands lead this transition, with houtilizes like Gucci Beauty and YSL offering premium compacts designed for long-term utilize with biodegradable or aluminum refills. In France, the anti-waste law for a circular economy requires all cosmetic brands to implement take-back or refill systems by 2025, accelerating investment in reverse logistics. As per the French Environment and Energy Management Agency, refillable systems can significantly reduce packaging waste over time. Additionally, subscription models for refills piloted by brands in Denmark enhance customer lifetime value while minimizing environmental impact. This shift from disposable to durable design aligns with EU policy and repositions color cosmetics as curated long-term investments rather than transient purchases.

MARKET CHALLENGES

Persistent Greenwashing and Lack of Standardized Sustainability Claims

Despite growing eco-consciousness, the European color cosmetics market suffers from inconsistent and often misleading environmental marketing, which erodes consumer trust. According to the European Consumer Organisation, a majority of “eco-frifinishly” or “natural” claims on color cosmetic packaging lacked verifiable certification or standardized definitions in 2023. Terms such as “clean,” “green,” or “sustainable” remain unregulated under EU law, enabling brands to highlight one eco attribute while ignoring non-recyclable components. As per the European Commission, the Green Claims Directive aims to rectify this by requiring third-party verification and life cycle evidence for all environmental assertions, though implementation remains in progress. In the interim, consumers face confusion, with a Eurobarometer survey displaying that many respondents feel unable to discern genuinely sustainable products. This credibility gap pressures even transparent brands to over-communicate their efforts, while compacter players risk reputational damage from unintentional non-compliance.

Supply Chain Volatility for Natural and Mineral Pigments

The shift toward natural and mineral-based colorants has exposed the European color cosmetics market to raw material scarcity and geopolitical supply risks, which is further challenging the expansion of the European color cosmetics market. According to the European Raw Materials Alliance, the EU imports the majority of its cosmetic-grade iron oxides and ultramarines from countries such as China, India, and Turkey, where environmental crackdowns and export restrictions have cautilized price spikes and lead time extensions. As per the International Colored Pigments Association, mica prices rose in 2023 following enforcement of ethical mining audits in India. Simultaneously, the EU’s Conflict Minerals Regulation requires due diligence on mica sourcing, adding administrative burden. Domestic alternatives remain limited, with European synthetic iron oxide production meeting only a compact share of demand according to Eurostat. This reliance on external sources creates formulation instability, with brands forced to reformulate when batches fail heavy metal thresholds. Moreover, natural pigments often yield less vibrant or less stable hues than synthetics, compromising aesthetic performance. This raw material fragility threatens the foundation of the clean beauty relocatement in Europe, pressuring brands to balance ethical sourcing with consistent quality and creative expression.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

7.16% |

|

Segments Covered |

By Tarobtain Segment, Application, and Region |

|

Various Analyses Covered |

Global, Regional, & Countest Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

Estee Lauder Inc., Avon Products, Inc., L?Oreal SA, Revlon, Inc., Procter & Gamble (P&G) Company, Unilever, Ciat London, Shiseido Company, Limited, Kryolan Professional Make-Up, and Coty Inc. |

SEGMENTAL ANALYSIS

By Tarobtain Segment Insights

The prestige color cosmetics segment dominated the market and accounted for 57.5% of the regional market share in 2025. The dominance of the prestige segment in the European color cosmetics market is primarily fuelled by premiumization, consumer loyalty, and superior formulation narratives that align with European values of quality and sustainability. Europe’s deep-rooted association with haute couture and luxury perfumery extfinishs naturally to prestige color cosmetics, where French and Italian houtilizes command emotional resonance. According to a study by the European Institute for Luxury Goods, a large majority of women in France, Italy, and Spain view prestige buildup as an extension of personal identity rather than mere adornment. Iconic brands such as Chanel, Dior, and YSL leverage their fashion legacies to create collectible seasonal collections tied to runway themes or artistic collaborations, driving anticipation and exclusivity. In the UK, a significant share of prestige color cosmetic purchases occurs during limited-edition launches as per Kantar retail data. Furthermore, European consumers associate prestige pricing with cleaner formulations and ethical sourcing. As per the European Consumer Organisation, many consumers believe high-finish brands are more transparent about ingredients. This cultural reverence for craftsmanship, heritage, and authenticity ensures sustained willingness to pay premiums even amid economic uncertainty.

While compacter in value share, the mass color cosmetics segment is expected to expand at a CAGR of 8.18% over the forecast period owing to the value consciousness and digital democratization. Mass brands have successfully bridged the gap between affordability and performance by adopting clean formulations and trfinish-driven design previously reserved for prestige. According to the European Natural Cosmetics Association, a notable share of new mass color cosmetic launches in 2023 carried certified natural or vegan labels, with ingredients like castor oil and mineral pigments replacing parabens and synthetic dyes. Brands such as Essence, Maybelline, and L’Oréal Paris now offer refillable compacts and water-based long-wear formulas that meet EU sustainability standards at affordable prices. In Poland and the Czech Republic, sales of clean lipsticks grew significantly in 2023 as per national retail audits, reflecting demand for ethical beauty without luxury markups. Social media further amplifies reach, with TikTok tutorials displaycasing mass products achieving prestige-level results. This value innovation positions mass as credible, not just economical, thereby capturing budobtain-conscious yet discerning consumers across Southern and Central Europe.

By Application Insights

The lip products segment was the largest application segment in the Europe color cosmetics market in 2025 and held 33.9% of the European market share. The growth of the lip products segment in this regional market is attributed to the cultural emphasis on lip expression, versatility across occasions, and continuous innovation in wearability. In many European countries, lipstick is not merely cosmetic but a symbol of confidence and femininity deeply embedded in daily routines. According to a Eurobarometer survey, a large majority of women in Italy, France, and the UK apply lip color multiple times per week, with red and nude shades serving as wardrobe staples. The French concept of “le rouge à lèvres” as a finishing touch to any outfit has elevated lipstick to an essential ritual rather than an optional accessory. Moreover, lip products adapt seamlessly across contexts—from matte liquid lipsticks for professional settings to glossy balms for casual wear—offering unmatched functional range. Retailers reinforce this through curated displays with testers and mirrors encouraging trial and immediate purchase. Unlike eye or face buildup, which requires skill and time, lip products deliver instant transformation with minimal effort, building them the most accessible entest point into color cosmetics and the most consistent repurchase category for loyalists.

The special effect color cosmetics segment is estimated to register a promising CAGR of 15.1% over the forecast period. Europe’s vibrant music festival scene and urban nightlife have created sustained demand for bold, expressive buildup. According to the European Festival Association, millions of people attfinished major European festivals such as Tomorrowland, Glastonbury, and Sziobtain in 2023, where glitter face paint and metallic accents are cultural norms. In the UK, sales of biodegradable glitter gels increased during summer months as per Kantar data, while in Spain, temporary tattoo eyeliner saw notable growth in coastal nightlife districts. Social media further fuels this trfinish, with TikTok challenges displaycasing avant-garde views applying special effect products. Unlike traditional buildup, these items serve as social currency and build them essential for experiential participation. Brands such as NYX and Sleek now offer EU-compliant glitter created from plant cellulose, eliminating microplastic concerns while maintaining iridescence.

REGIONAL ANALYSIS

France Color Cosmetics Market Analysis

France stood as the largest color cosmetics market in Europe in 2025 by capturing 21.6% of the European market share. The nation’s dominance is rooted in its historic role as the birthplace of modern perfumery and luxury beauty, with Paris serving as a global trfinishsetter. French consumers exhibit high brand loyalty to domestic houtilizes such as Chanel, Guerlain, and Lancôme. According to a 2023 Ifop survey, a majority of consumers prefer locally crafted formulas. The countest enforces stringent cosmetic safety standards through ANSM, aligning closely with EU regulations while maintaining elevated expectations for elegance and sensory experience. Department stores like Le Bon Marché and beauty chains such as Marionnaud offer immersive brand experiences that blfinish heritage and innovation. Additionally, France’s film, fashion, and art institutions continuously inspire seasonal collections, reinforcing buildup as cultural expression.

United Kingdom Color Cosmetics Market Analysis

The United Kingdom was another major regional segment in the European color cosmetics market in 2025 and held 19.4% of the European market share. The countest’s strength lies in its digitally fluent consumer base and leadership in inclusive beauty. British brands such as Charlotte Tilbury and Fenty Beauty Europe pioneered shade diversity and social media-driven launches that reshaped industest standards. According to Kantar, many UK women under thirty discover new buildup via TikTok, with viral trfinishs translating to sales within days. The UK also leads in clean beauty adoption, with a significant share of new color cosmetic launches in 2023 carrying vegan or refillable claims as per the British Beauty Council. Despite Brexit, UK regulators maintain alignment with EU cosmetic regulations, ensuring product safety while allowing agile marketing. London’s status as a multicultural hub further drives demand for products catering to diverse skin tones and cultural aesthetics.

Germany Color Cosmetics Market Analysis

Germany is anticipated to record a promising CAGR in the European color cosmetics market during the forecast period. The countest’s market is defined by rational, high-value purchasing driven by ingredient literacy and sustainability awareness. German consumers prioritize INCI transparency. According to a 2023 GfK study, a large share of consumers read full ingredient lists before purchase. This scrutiny has accelerated demand for certified natural and dermatologically tested products, with brands such as Lavera and Alverde thriving in the mass premium space. The BDIH natural cosmetics certification is widely recognized, with thousands of products bearing its seal. Additionally, Germany’s strong e-commerce infrastructure enables direct brand engagement. As per the German E-Commerce Association, online color cosmetics sales grew significantly in 2023. Unlike Southern Europe where buildup is ritualistic, German usage is functional yet quality-focutilized, with emphasis on long wear and skin compatibility.

Italy Color Cosmetics Market Analysis

Italy is projected to account for a notable share of the European color cosmetics market during the forecast period. The countest’s position is anchored in its cultural reverence for beauty, la dolce vita, and artisanal craftsmanship. Italian women view buildup as an extension of personal style, with emphasis on luminous skin and bold lip colors reflecting Mediterranean aesthetics. According to a 2023 Eurispes survey, a majority of Italian women consider buildup essential to daily self-presentation, with preference for locally created products that blfinish tradition and innovation. Brands such as KIKO Milano and Pupa leverage Italian design sensibility, offering fashion-forward packaging and high pigment intensity at accessible prices. The “Made in Italy” label carries significant weight. As per the Italian Beauty Association, many consumers associate it with superior quality and color payoff. Furthermore, Italy’s strong tourism sector amplifies global appeal, with duty-free sales at airports driving trial among international visitors.

Spain Color Cosmetics Market Analysis

Spain is expected to exhibit a healthy CAGR in the European color cosmetics market during the forecast period. The countest’s vibrancy stems from its social lifestyle, youthful population, and openness to bold buildup expressions. Spanish consumers embrace color. According to a 2023 Kantar Iberia report, a large share of women aged eighteen to thirty regularly utilize eyeshadow and lip gloss. The warm climate and outdoor culture favor long-wear and sweat-resistant formulas, driving innovation in transfer-proof technologies. Social media and music festivals such as Primavera Sound amplify trfinish adoption, with viral views spreading rapidly across urban centers like Madrid and Barcelona. Local brands such as Deliplus and L’Oréal España lead in affordable innovation, offering high-impact products at mass prices. Additionally, Spain’s growing gfinisher-fluid relocatement has normalized buildup among young men. As per the Spanish Institute of Youth, a notable share of males under twenty-five utilize color cosmetics regularly.

COMPETITIVE LANDSCAPE

The Europe color cosmetics market features layered competition where global giants coexist with agile indie brands and heritage luxury houtilizes. Dominance is not determined by price but by the ability to merge aesthetic excellence with ethical integrity. Large corporations leverage scale to innovate in sustainability and digital personalization while niche players differentiate through hyper transparency limited editions and community driven storynotifying. Regulatory pressure acts as both a barrier and a catalyst pushing all participants toward cleaner formulations. Competition intensifies in the prestige segment where emotional loyalty is built through immersive retail experiences and artistic collaborations whereas the mass segment thrives on trfinish agility and social media virality. The rise of conscious consumerism has eroded blind brand loyalty forcing even established names to prove their environmental and social credentials. Ultimately success in Europe hinges on a delicate equilibrium between beauty performance cultural relevance and demonstrable responsibility building the market one of the world’s most sophisticated and demanding arenas for color cosmetics innovation.

KEY MARKET PLAYERS

Some of the notable key players in the Europe color cosmetics market are

- Estée Lauder Inc.

- Avon Products, Inc.

- L’Oréal SA

- Revlon, Inc.

- Procter and Gamble Company

- Unilever

- Ciat London

- Shiseido Company, Limited

- Kryolan Professional Make Up

- Coty Inc.

Top Players in the Market

- L’Oréal SA exerts significant influence in the Europe color cosmetics market through its diverse portfolio spanning mass brands like L’Oréal Paris and Maybelline to luxury labels such as Lancôme and YSL Beauty. The company actively champions sustainability by eliminating virgin plastic from packaging and transitioning to bio-based pigments across its European formulations. Recently L’Oréal launched a refillable lipstick system for YSL in France Germany and Italy and introduced AI powered shade matching tools in Sephora Europe stores. It also strengthened its clean beauty credentials by achieving Cradle to Cradle certification for several color cosmetic lines. These initiatives reflect L’Oréal’s integrated strategy of combining scientific innovation with environmental responsibility to meet the region’s exacting consumer and regulatory standards.

- Estée Lauder Companies Inc maintains a strong presence in Europe through prestige color cosmetics brands including MAC Clinique and Bobbi Brown. The company has intensified its focus on digital engagement by enhancing virtual test on capabilities via its partnership with Snapchat and Instagram across Western Europe. It recently rolled out carbon neutral buildup collections in the UK and Sweden featuring recyclable compacts and plant derived dyes. Estée Lauder also expanded its inclusive shade ranges after conducting 3D skin tone mapping across 12 European countries. These actions demonstrate its commitment to personalization sustainability and representation reinforcing its appeal among discerning European luxury beauty consumers who value both performance and purpose.

- Coty Inc plays a pivotal role in the Europe color cosmetics market through iconic brands like Rimmel Max Factor and Gucci Beauty. The company has accelerated its transformation by investing in circular packaging by launching aluminum based refillable eyeshadow palettes and lipstick cases across the EU. Coty recently partnered with the French startup Carbios to incorporate enzymatically recycled plastic into its compacts a first in the European color cosmetics sector. It also enhanced its digital commerce infrastructure enabling same day delivery of color products in major cities like Berlin Madrid and Amsterdam. By aligning heritage aesthetics with next generation sustainability and agile distribution Coty strengthens its relevance across both mass and prestige segments in a rapidly evolving European beauty landscape.

Top Strategies Used by the Key Market Participants

Key players in the Europe color cosmetics market primarily deploy strategies centered on sustainable packaging reformulation digital personalization inclusive shade development and circular business models. They invest heavily in bio based and refillable packaging to comply with the EU Packaging and Packaging Waste Directive while replacing synthetic dyes with ethically sourced mineral pigments. Companies leverage augmented reality and AI for virtual test on and shade matching to enhance e commerce conversion. Simultaneously they expand foundation and concealer ranges applying 3D skin scanning across European ethnic subgroups to ensure true inclusivity. Strategic collaborations with biotech firms for enzymatic recycling and adoption of Cradle-to-Cradle certification further reinforce environmental credibility. These integrated approaches allow major brands to balance luxury aesthetics with regulatory compliance and conscious consumerism in Europe’s demanding beauty ecosystem.

MARKET SEGMENTATION

This research report on the European color cosmetics market has been segmented and sub-segmented based on categories.

By Tarobtain Segment

- Mass Products

- Prestige Products

By Application

- Facial Make up

- Lip Products

- Eye Make up

- Nail Products

- Hair Color Products

- Special Effect Products

By Countest

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe