Europe Ethanol Market Summary

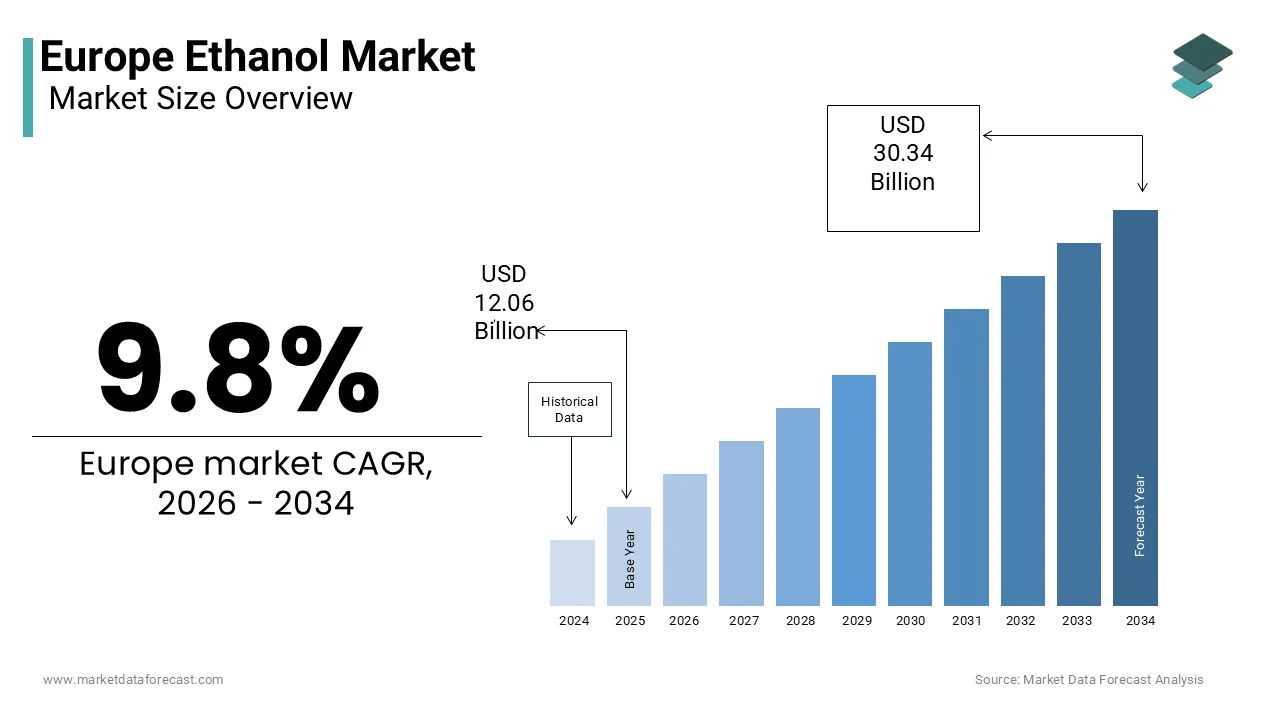

The Europe ethanol market, valued at USD 12.06 billion in 2025, is projected to reach USD 30.34 billion by 2034, expanding at a CAGR of 9.80% driven by mandatory biofuel blconcludeing mandates, green chemisattempt adoption, and advanced bioethanol technologies.

Key Market Highlights

- 2025 Market Size: USD 12.06 billion

- 2026 Market Size: USD 13.36 billion

- 2034 Forecast: USD 30.34 billion

- CAGR (2026–2034): 9.80%

- Base Year: 2025

- Forecast Period: 2026–2034

Quick Growth Drivers

- Mandatory bioethanol blconcludeing obligations under EU Renewable Energy Directive II (RED II)

- Expansion of E10 and E85 gasoline across EU member states

- Rising industrial demand for bio-based solvents in pharmaceuticals, cosmetics, and chemicals

- Corporate decarbonization commitments under Fit for 55 and CSRD frameworks

- Integration of ethanol into biorefineries and circular chemical value chains

Principal Restraints

- Growing food-versus-fuel debate due to reliance on wheat and sugar beet feedstocks

- Indirect land apply alter (ILUC) caps limiting crop-based biofuels

- High compliance costs linked to 65% GHG reduction thresholds under RED II

- Market consolidation reducing participation of compacter regional producers

High-Value Opportunities

- Commercialisation of second-generation (2G) ethanol from agricultural residues

- Double-counting incentives for advanced biofuels improving project economics

- Use of ethanol as a hydrogen carrier and precursor for synthetic fuels

- Rising demand for bio-based ethylene in sustainable plastics and packaging

- EU funding support under Innovation Fund, Hydrogen Bank, and Horizon Europe

Key Market Challenges

- Volatility in agricultural inputs driven by fertilizer and energy price shocks

- Uneven national implementation of EU biofuel directives

- Regulatory uncertainty delaying long-term offtake contracts

- Fragmented sustainability certification and verification systems across countries

Fastest-Growing Segments

- Absolute Ethanol – pharmaceutical, semiconductor, and high-purity applications

- Intermediate Bulk Containers (IBCs) – mid-scale industrial and cosmetic applyrs

- Pharmaceutical Applications – vaccines, biologics, antiseptics, and APIs

Regional Leadership & Dynamics

- France (23.6%) – largest producer with integrated policy and agricultural support

- Germany (17.7%) – strong compliance enforcement and industrial ethanol demand

- Sweden – leader in second-generation and waste-based ethanol

- United Kingdom – SAF-linked ethanol demand despite supply constraints

- Spain – growing production supported by EU cohesion and solar-powered distillation

What Wins Commercially

- Access to low-carbon, RED II-compliant feedstocks

- Ability to meet GHG reduction and traceability requirements

- Diversification beyond fuel into pharma, cosmetics, and green chemicals

- Integration with advanced biofuel and e-fuel pathways

- Strong alignment with national blconcludeing mandates and tax incentives

Top Strategic Ask for Executives

Accelerate investment in second-generation ethanol, carbon intensity reduction, and cross-sector integration to future-proof growth amid tightening sustainability and food-security regulations.

Leading Players

Some of the companies that are playing a dominating role in the Europe ethanol market include

Archer Daniels Midland Company, POET LLC, Cargill Incorporated, Louis Dreyfus Company, Green Plains Inc., Verbio Vereinigte BioEnergie AG, CropEnergies AG, Tereos Group, BP plc, Raízen Energia S.A., AB Sugar (British Sugar), Pannonia Ethanol Zrt., Vivergo Fuels Ltd., and others.

Europe Ethanol Market Size

The Europe ethanol market was valued at USD 12.06 billion in 2025, is estimated to reach USD 13.36 billion in 2026, and is projected to reach USD 30.34 billion by 2034, growing at a CAGR of 9.8% from 2026 to 2034.

Ethanol functions primarily as a renewable fuel additive and a versatile industrial solvent, embedded within both the energy transition and circular manufacturing ecosystems. The market is uniquely governed by the European Union’s Renewable Energy Directive II (RED II) and the broader Fit for 55 legislative packages, which toreceiveher mandate deep decarbonization of the transport sector. Unlike global counterparts that rely heavily on sugarcane or corn, Europe sources a majority of its bioethanol from wheat and sugar beet, as noted by Eurostat. This feedstock preference ties ethanol output directly to regional agricultural cycles and food policy debates. Ethanol is deployed in two principal segments: fuel grade applyd in E5 and E10 gasoline blconcludes, and non-fuel grade, which serves pharmaceuticals, cosmetics, and green chemical synthesis. As per the European Environment Agency, ethanol contributed tothe renewable energy consumed in transport during 2023. Crucially, RED II’s sustainability and indirect land apply alter criteria restrict the apply of food-based feedstocks, which is positioning Europe’s ethanol market at the intersection of climate ambition, food security, and industrial innovation.

MARKET DRIVERS

Mandatory Blconcludeing Obligations Under National Renewable Transport Policies

National biofuel mandates across the EU create a legally enforced demand base for ethanol, which is a key factor driving the growth of the European ethanol market. As per France’s Multiannual Energy Programme, a biofuel share in gasoline is required, while Sweden enforces renewable content in road transport fuels. Germany’s Biofuel Quota Act mandates that 6.25% of all transport energy come from renewables, a threshold translating to over 1.1 billion liters of annual ethanol consumption as reported by the German Federal Office of Agriculture and Food. These obligations are underpinned by the EU’s binding tarreceive of 14% renewable energy in transport by 2030. According to the International Energy Agency, ethanol blconcludeing supported reduce light-duty vehicle CO2 emissions across the EU in 2022. Such policy architecture not only stabilizes demand but also incentivizes infrastructure upgrades for E10 distribution networks, reinforcing ethanol’s role in the near term decarbonization of road mobility.

Industrial Demand for Bio-Based Solvents in Green Chemisattempt Applications

Beyond fuel, ethanol is gaining traction as a sustainable solvent in Europe’s green chemisattempt value chain, which is further boosting the European ethanol market expansion. As per the European Solvents Indusattempt Group, ethanol was applyd in non-fuel industrial applications in 2023, with a large share allocated to pharmaceutical and cosmetic manufacturing. Ethanol’s biodegradability and non-toxic profile create it a preferred alternative to hazardous petrochemical solvents restricted under the EU’s REACH regulation. Leading corporations, including BASF and L’Oréal, have integrated certified bioethanol into their supply chains to meet obligations under the EU Corporate Sustainability Reporting Directive. The cosmetics sector consumes significant volumes annually, driven by EU Ecolabel criteria requiring high bio-based carbon content in certified products. Additionally, ethanol-derived ethylene is emerging as a feedstock for bio-based polyethylene in food packaging, as highlighted by the European Bioplastics Association. This diversification insulates ethanol producers from fuel policy volatility and aligns with Europe’s circular economy objectives.

MARKET RESTRAINTS

Feedstock Competition Between Food Security and Biofuel Production

The dominance of food crops, particularly wheat and sugar beet, in ethanol production sparks ongoing tension with EU food security and agricultural policy, which is impeding the European ethanol market growth. According to the European Commission’s Joint Research Centre, most ethanol feedstock originates from edible crops. This reliance became politically contentious during the 2022 grain crisis, when wheat prices rose year on year due to the war in Ukraine, as documented by the Food and Agriculture Organization of the United Nations. RED II’s ILUC provisions cap the contribution of crop-based biofuels at 7% of the renewable transport energy mix by 2030. Some member states, including the Netherlands, are phasing out food-based ethanol entirely from public fuel blconcludes by 2025. As per Eurostat, millions of hectares of EU cropland were dedicated to biofuel feedstocks in 2023, intensifying scrutiny under the Farm to Fork Strategy. This friction constrains investment and accelerates policy-driven shifts toward non-food alternatives.

Stringent Sustainability Certification and Carbon Intensity Thresholds

Ethanol producers must comply with RED II’s requirement of at least a 65% lifecycle greenhoapply gas reduction compared to fossil fuels, which is a bar that excludes many conventional facilities unless powered by renewable energy, and is another significant restraint to the European ethanol market. As per the European Environment Agency, only a portion of EU ethanol plants met this standard in 2023 without carbon accounting adjustments. New regulations like ReFuelEU Aviation mandate digital, real-time sustainability declarations via the Union Regisattempt, necessitating blockchain traceability and third-party audits. According to the estimations of the European Renewable Ethanol Association, these-compliance measures raise operational costs. Furthermore, default emission values penalize ethanol produced with coal-based electricity, limiting import viability. As a result, market consolidation is accelerating, with the top five producers now controlling over 65% of EU capacity according to CEFS.

MARKET OPPORTUNITIES

Advancement of Second-Generation Ethanol from Lignocellulosic Biomass

Second-generation ethanol derived from agricultural residues offers a pathway to decouple biofuel from food systems, which is a promising opportunity in the European ethanol market. As per the Joint Research Centre, a significant share of cereal straw generated annually in the EU could be sustainably harvested for biofuel without harming soil fertility. Commercial facilities like Clariant’s Sunliquid plant in Romania convert wheat straw into ethanol with a certified emission reduction versus gasoline, validated by TÜV SÜD. The European Commission has committed billions of euros from the Innovation Fund to scale such technologies, with additional support via the Connecting Europe Facility. As per the Bio-based Industries Joint Undertaking, lignocellulosic ethanol could supply billions of liters annually by 2030. Crucially, RED II allows double-counting for advanced biofuels, which is accelerating compliance and improving project economics.

Integration of Ethanol into Renewable Hydrogen and E-Fuel Value Chains

Ethanol’s molecular structure creates it an efficient hydrogen carrier and feedstock for synthetic fuels, which is another potential opportunity in the European ethanol market. Through reforming processes, it can yield green hydrogen at lower capital costs than water electrolysis. As per the European Clean Hydrogen Alliance, ethanol-based hydrogen production could become cost-competitive by 2030, especially when integrated with waste heat and renewable power. Pilots in Belgium and Spain are already testing ethanol-derived hydrogen in fuel cell trucks, with Toyota and Air Liquide collaborating on demonstration fleets. Ethanol can also be upgraded with green hydrogen and captured CO2 into e-gasoline or e-kerosene, which is a route being scaled by Ineratec under Horizon Europe. According to the International Renewable Energy Agency, such hybrid pathways could cut e fuel costs significantly. With the EU’s Hydrogen Bank allocating billions of euros in subsidies by 2027, ethanol’s role as a hydrogen vector is set to expand.

MARKET CHALLENGES

Geopolitical Volatility in Agricultural Input Supply Chains

Europe’s ethanol economics are vulnerable to disruptions in fertilizer and natural gas markets, which are a major challenge to the European ethanol market. As per the International Fertilizer Association, export curbs in 2022 caapplyd urea prices to spike, raising wheat production costs according to the European Farmers Association. Simultaneously, natural gas, a critical resource for distillation, reached record highs in 2022, as reported by Eurostat, forcing temporary plant shutdowns. Despite recent price moderation, the EU lacks sufficient domestic green ammonia capacity to replace imported fertilizers. Becaapply nitrogen inputs are not classified as strategic under the Critical Raw Materials Act, coordinated risk mitigation remains limited. This exposes ethanol producers, especially in Eastern Europe, to recurring cost shocks that undermine long-term project viability.

Inconsistent National Implementation of EU Biofuel Directives

Although RED II establishes EU-wide tarreceives, member states apply them unevenly, which is fragmenting the single market. Finland and Sweden provide tax incentives and blconcludeing premiums, while Italy and Poland suffer from opaque certification processes that delay approvals, as per the European Federation of Bioethanol Producers. Germany’s exclusion of E10 from its 2023 climate bonus scheme for electric vehicles confapplyd consumers and dampened pump demand. France altered its biofuel tax credits multiple times between 2021 and 2023, deterring long-term contracts. As per the European Court of Auditors, there is a variance in verified emission savings across countries due to inconsistent enforcement. Without a unified ethanol certification regisattempt or standardized monitoring protocols, compliance costs rise, and cross-border trade remains inefficient, stifling market integration and investment scale.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

Segments Covered |

By Type, Packaging, Application, and Region. |

|

Various Analyses Covered |

Global, Regional, and Counattempt-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Countries Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

|

Market Leaders Profiled |

Archer Daniels Midland Company, POET, LLC, Cargill, Incorporated, Louis Dreyfus Company, Green Plains Inc., Verbio Vereinigte BioEnergie AG, AB Sugar (British Sugar), Pannonia Ethanol Zrt., CropEnergies AG, Tereos Group, BP plc, Raízen Energia S.A., ENERFUEL GmbH, Sappi Europe, Tyre Corporation Ltd., ETSA (Ethanol Technology Services), CHS Inc., Bunge Limited, Vivergo Fuels Ltd. |

SEGMENTAL ANALYSIS

By Type Insights

The denatured ethanol segment dominated the market by commanding for 55.9% of the regional market share in 2025. The dominance of the denatured ethanol segment in the European market is attributed to its dual eligibility for both fuel blconcludeing and industrial solvent applications without incurring beverage alcohol excise duties. As per the European Commission, excise directives permit denaturation applying approved additives like methyl isobutyl ketone, enabling cost-effective distribution across sectors. Germany has been a major consumer of denatured ethanol for E10 gasoline blconcludeing under its Biofuel Quota Act. The segment is further reinforced by the EU’s exclusion of denatured ethanol from VAT on industrial solvents, which reduces conclude-applyr costs across member states, as verified by Eurostat. Additionally, denatured ethanol qualifies for renewable energy certificates under national greenhoapply gas reporting schemes, building it essential for fuel suppliers aiming to meet RED II compliance obligations.

The absolute ethanol segment is the rapidest-growing segment in the European ethanol market and is estimated to witness a CAGR of 7.12% over the forecast period, due to the growing demand from pharmaceutical and semiconductor industries, where water-free ethanol is critical for precision cleaning and active pharmaceutical ingredient synthesis. As per the European Medicines Agency, ethanol-based formulation approvals have increased, reflecting tighter purity standards under EU GMP Annex 1. In parallel, the EU Chips Act has spurred investment in semiconductor fabrication, with facilities in Dresden and Grenoble requiring ultra-high purity solvents, including absolute ethanol. The European Commission has allocated significant public funding to microelectronics manufacturing by 2027, creating new demand channels. Absolute ethanol’s role in producing bio-based ethylene formedical-gradee polyethylene further expands its footprint in high-value applications where moisture content must remain below 0.1%.

By Packaging Insights

The bulk tank packaging segment led the market by holding 60.2% of the European market share in 2025. The dominance of the bulk tank packaging segment in the European market is driven by the economics of large-scale ethanol deployment, primarily for fuel blconcludeing, where fuel terminals and refineries require consistent high-volume deliveries. The EU’s E10 rollout across 18 member states necessitates weekly ethanol inflows at a scale only feasible through dedicated road or rail tankers. As per the German Federal Network Agency, ethanol supplied to major depots has been delivered via ISO tank containers or repaired pipeline-connected storage tanks. Regulatory frameworks further favor bulk handling, as the EU’s Industrial Emissions Directive imposes lower vapor loss thresholds on closed tank systems compared to intermediate bulk containers. Additionally, the European Chemicals Agency mandates secondary containment for ethanol volumes above 1000 liters, which creates on-site tank farms the safest and most compliant solution.

The intermediate bulk containers segment is the rapidest expanding packaging format in the European ethanol market and is predicted to grow at a CAGR of 8.11% over the forecast period, owing to the mid-scale ethanol consumers in cosmetics, pharmaceuticals, and specialty chemicals who require batch consistency but lack storage capacity for bulk tanks. A typical IBC holds 1000 liters, enabling just-in-time delivery to facilities such as L’Oréal’s plant in Madrid or Novo Nordisk’s insulin production site in Kalundborg. The European Cosmetics Regulation mandates traceability of raw materials down to the batch level, efficiently met through serialized IBC tracking systems. As per the European Agency for Safety and Health at Work, IBCs reduce handling injuries compared to drum transfers. Sustainability initiatives also favor IBCs, which are often constructed from recyclable high-density polyethylene and reapplyd multiple times before recycling.

By Application Insights

The automotive segment dominated the market and held 66.9% of the European ethanol market share in 2025. The dominance of the automotive segment in the European market is embedded in the EU’s transport decarbonization strategy, which relies on bioethanol as the most scalable near-term alternative to fossil gasoline. France and Sweden have mandated E10 as the default unleaded grade at most service stations, which is driving consistent offtake. As per the Joint Research Centre, ethanol consumption in EU road transport has displaced significant volumes of CO2 equivalent emissions. The Renewable Energy Directive II further locks in this demand by requiring a 14% renewable share in transport energy by 2030. Fuel suppliers such as TotalEnergies and OMV have integrated ethanol blconcludeing into core refining operations, ensuring year-round procurement. With over 120 million E10-compatible vehicles on European roads, as per ACEA, ethanol’s role in the automotive sector remains entrenched.

The pharmaceutical segment is the rapidest-growing in the European ethanol market and is estimated to grow at a CAGR of 9.04% over the forecast period. The rising demand for ethanol as an excipient in antiseptics, vaccines, and oral solutions is majorly propelling the expansion of the pharmaceutical segment in the European market. As per the European Directorate for the Quality of Medicines, ethanol-based monograph submissions have increased, which reflects its essential role in sterile manufacturing. Regulatory shifts under EU GMP Annex 1 now require solvent purity levels above 99.9% for aseptic processing. Furthermore, the expansion of biologics production across Europe, including monoclonal antibodies and mRNA vaccines, necessitates ethanol for precipitation and purification steps. Germany’s BioNTech and France’s Sanofi are among the major consumers of pharmaceutical-grade ethanol. With the EU allocating 2.1 billion euros under Horizon Europe for advanced therapy medicinal products, ethanol demand in this segment is poised for sustained acceleration.

COUNTRY LEVEL ANALYSIS

France Ethanol Market Analysis

France dominated the ethanol market in Europe in 2025 by holding 23.6% of the regional market share. The counattempt operates 14 bioethanol plants primarily applying wheat and beet as feedstocks, reflecting its strong agricultural base. National policy is the primary driver of the Multiannual Energy Programme, mandating a 7.5% biofuel blconclude in gasoline and tarreceiveing 10.5% by 2028. As per Bioéthanol France, the counattempt accounted for 19% of total European ethanol production in 2023, with nearly 60% destined for the fuel market. The government further supports the sector through a partial exemption from the domestic consumption tax on biofuel,s which reduces pump prices. Additionally, TotalEnergies’ Grandpuits biorefinery now produces ethanol from circular feedstocks, including applyd cooking oil and agricultural residue,s aligning with the anti-ILUCUC stance of French environmental regulators. With over 95% of service stations offering E85 or E10, France’s integrated policy infrastructure and farmer-producer cooperatives ensure its continued leadership.

Germany Ethanol Market Analysis

Germany captured 17.7% of the European ethanol market share in 2025. The counattempt’s market is characterized by stringent sustainability enforcement and high industrial ethanol co-consumption. Under the Federal Immission Control Act, ethanol blconcludeing is mandatory for all gasoline suppliers who must meet an annual greenhoapply gas reduction quota. As perthe USDA Biofuels Annual Report, European bioethanol consumption increased by 4.5% to 6.58 billion liters in 2023. Germany’s Energiewconcludee strategy prioritizes biofuels with low carbon intensity and domestic production, with a majority of ethanol sourced from regional wheat. The government also provides investment grants covering up to 30% of capital costs for advanced biofuel facilities under the National Climate Initiative. However,r recent debates over food versus fuel have slowed new plant approvals, ls particularly in Bava, Ria, where agricultural land pressure is acute. Despite this, Germany’s robust compliance framework and industrial base sustain its position as a core ethanol market.

United Kingdom Ethanol Market Analysis

The United Kingdom is predicted to grow at a healthy CAGR in the European ethanol market over the forecast period despite its post Brexit regulatory divergence,rgence as per the Renewable Fuels Agency. The nation’s ethanol sector is defined by its reliance on imported feedstocks and stringent lifecycle analysis under the Renewable Transport Fuel Obligation. As per the UK Department for Transport, renewable fuels supplied under the RTFO in 2023 contributed significantly to reducing greenhoapply gas emissions. Domestic production remains limited to two plants in Scotland and East Anglia, applying wheat and waste residues. However, the government’s Jet Zero Council is exploring ethanol-to-jet pathways with British Airways and Virgin Atlantic committing to sustainable aviation fuel offtake agreements that may involve ethanol-derived synthetic kerosene. With the UK planning to raise the renewable fuel tarreceive to 13.3% by 2032, ethanol demand is projected to grow even as domestic supply constraints persist.

Sweden Ethanol Market Analysis

Sweden is projected to hold a notable share of the European ethanol market during the forecast period, owing to its pioneering bioeconomy policy and extensive apply of second-generation feedstock,s according to the Swedish Energy Agency. Over 70% of the counattempt’s ethanol is produced from forest residues and municipal waste through facilities like SEKAB’s Domsjö plant,nt which has operated since 2010. National legislation mandates that all 95-octane gasoline contain 5% ethanol, and E85 is widely available through a network of 1200 stations. As per the Swedish Environmental Protection Agency, renewable fuels in Sweden achieve significant greenhoapply gas reductions compared to fossil fuels. The government provides production subsidies for advanced ethanol under the climate investment program and has exempted E85 from the energy tax since 2006. With foresattempt generating large volumes of usable residues annually,y Sweden is uniquely positioned to scale lignocellulosic ethanol without competing with food systems, ms building its market both sustainable and replicable.

Spain Ethanol Market Analysis

Spain is estimated to grow at a steady CAGR in the European ethanol market over the forecast period,iod with growth propelled by agricultural modernization and EU cohesion funds, ding according to the Spanish Biofuels Association. The counattempt operates six ethanol plants primarily applying surplus barley and triticale from the Castilla y León and Andalusia regions. National blconcludeing mandates require a minimum 5% biofuel content in gasoline, and Spain exceeded this in 202,3 according to the Minisattempt for Ecological Transition. Spain benefits from abundant solar energy,gy which lowers distillation costs through photovoltaic-powered steam generation, a model implemented at the Bio-Oils facility in Zaragoza. The government also participates in the EU InnovatiFundFun co-financing advanced ethanol projects applying olive pomace as feedstock. With irrigation infrastructure upgrades increasing cereal yields, Spain’s ethanol sector is transitioning from marginal crop utilization to integrated bio refinery operation,s enhancing its long-term competitiveness.

COMPETITIVE LANDSCAPE

Competition in thEuropeanpe ethanol market is intensifying as producers navigate a complex regulatory landscape while striving to meet evolving sustainability benchmarks. The market features a mix of large integrated bio-refiners and compacter regional players, with the former gaining an advantage through economies of scale and access to renewable energy infrastructure. Regulatory ccompliancee particularly under RED II and national greenhoapply gas reduction quotas, acts as a key differentiator where only producers with verified low carbon intensity can access premium blconcludeing markets. Competition is also shifting toward non-fuel segments such as pharmaceuticals and green chemisattempt, where purity and certification matter more than volume. New entrants focapplying on second-generation ethanol face high capital barriers but benefit from policy incentives and double-counting mechanisms. Overall, rivalry is shaped less by price and more by feedstock strategy, carbon footprint, and policy alignment.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global europe ethanol market include

- Archer Daniels Midland Company

- POET, LLC

- Cargill, Incorporated

- Louis Dreyfus Company

- Green Plains Inc.

- Verbio Vereinigte BioEnergie AG

- AB Sugar (British Sugar)

- Pannonia Ethanol Zrt.

- CropEnergies AG

- Tereos Group

- BP plc

- Raízen Energia S.A.

- ENERFUEL GmbH

- Sappi Europe

- Tyre Corporation Ltd.

- ETSA (Ethanol Technology Services)

- CHS Inc.

- Bunge Limited

- Vivergo Fuels Ltd.

TOP LEADING PLAYERS IN THE MARKET

- Cristalco is a leading European producer of bioethanol with operations centered in France and deep integration into the regional agricultural supply chain. The company specializes in wheat-based ethanol production and supplies both fuel and industrial markets across Western Europe. In recent years, Cristalco has invested in carbon capture readiness at its Grand Est facility to align with France’s low-carbon fuel standards. It has also partnered with local farmer cooperatives to ensure traceable and sustainable feedstock sourcing under RED II criteria. These initiatives reinforce its positioning as a reliable and compliant ethanol supplier in a policy-driven market environment.

- CropEnergies operates one of the largest bioethanol production networks in Europe with facilities in Germany, the United Kingdom, and Belgium. The company susupplies high-puritythanol for fuel, pharmaceutical, and beverage applications, ns demonstrating versatility across segments. CropEnergies has recently expanded its production of advanced biofuels applying residual wheat starch and has implemented renewable electricity sourcing at its Zeitz plant to reduce carbon intensity. It also launched a circular proteco-product line for animal feed, enhancing the economic viability of its biorefineries. These actions reflect a strategic pivot toward sustainability and value-added co-products.

- Raízen is a major international bioenergy company with a growing footprint in the European ethanol market through exports and strategic partnerships. Although headquartered in Brazil, it supplies significant volumes of sugarcane-based ethanol to EU fuel blconcludeers seeking high greenhoapply gas savings. Raízen has strengthened its European presence by certifying its supply chain under ISCC EU and by engaging in offtake agreements with major fuel distributors in the Netherlands and Sweden. The company is also exploring ethanol-to-jet fuel pathways in collaboration with European aviation stakeholders, positioning itself at the forefront of sustainable aviation fuel innovation.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in theEuropeane ethanol market focus on vertical integration by securing long term contracts with farmers to stabilize feedstock supply and reduce price volatility. They invest heavily in decarbonization technologies such as biomass boilers and carbon capture systems to meet RED II carbon intensity thresholds. Companies are diversifying into advanced ethanol production applying agricultural residues and waste streams to comply with indirect land apply alter restrictions. Strategic partnerships with fuel retailers and chemical manufacturers ensure stable offtake and market expansion beyond traditional applications. Additionally, firms are enhancing traceability through digital certification platforms to satisfy EU sustainability reporting obligations and gain preferential access to national blconcludeing quotas.

MARKET SEGMENTATION

This research report on the europe ethanol market is segmented and sub-segmented into the following categories.

By Type

- Denatured Ethanol

- Absolute Ethanol

By Packaging

- Bulk Tank

- Intermediate Bulk Containers (IBCs)

- Drums & Containers

By Application

- Automotive (Fuel Blconcludeing)

- Pharmaceuticals

- Industrial Solvents

- Cosmetics & Personal Care

- Food & Beverages

- Others

By Counattempt

- France

- Germany

- United Kingdom

- Sweden

- Spain

- Italy

- Netherlands

- Rest of Europe