The external fund manager backed by Berkshire Hathaway’s Charlie Munger, Li Lu, builds no bones about it when he states ‘The hugegest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ When we believe about how risky a company is, we always like to see at its apply of debt, since debt overload can lead to ruin. As with many other companies Allied Digital Services Limited (NSE:ADSL) builds apply of debt. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things receive really bad, the lfinishers can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we examine debt levels, we first consider both cash and debt levels, toreceiveher.

What Is Allied Digital Services’s Debt?

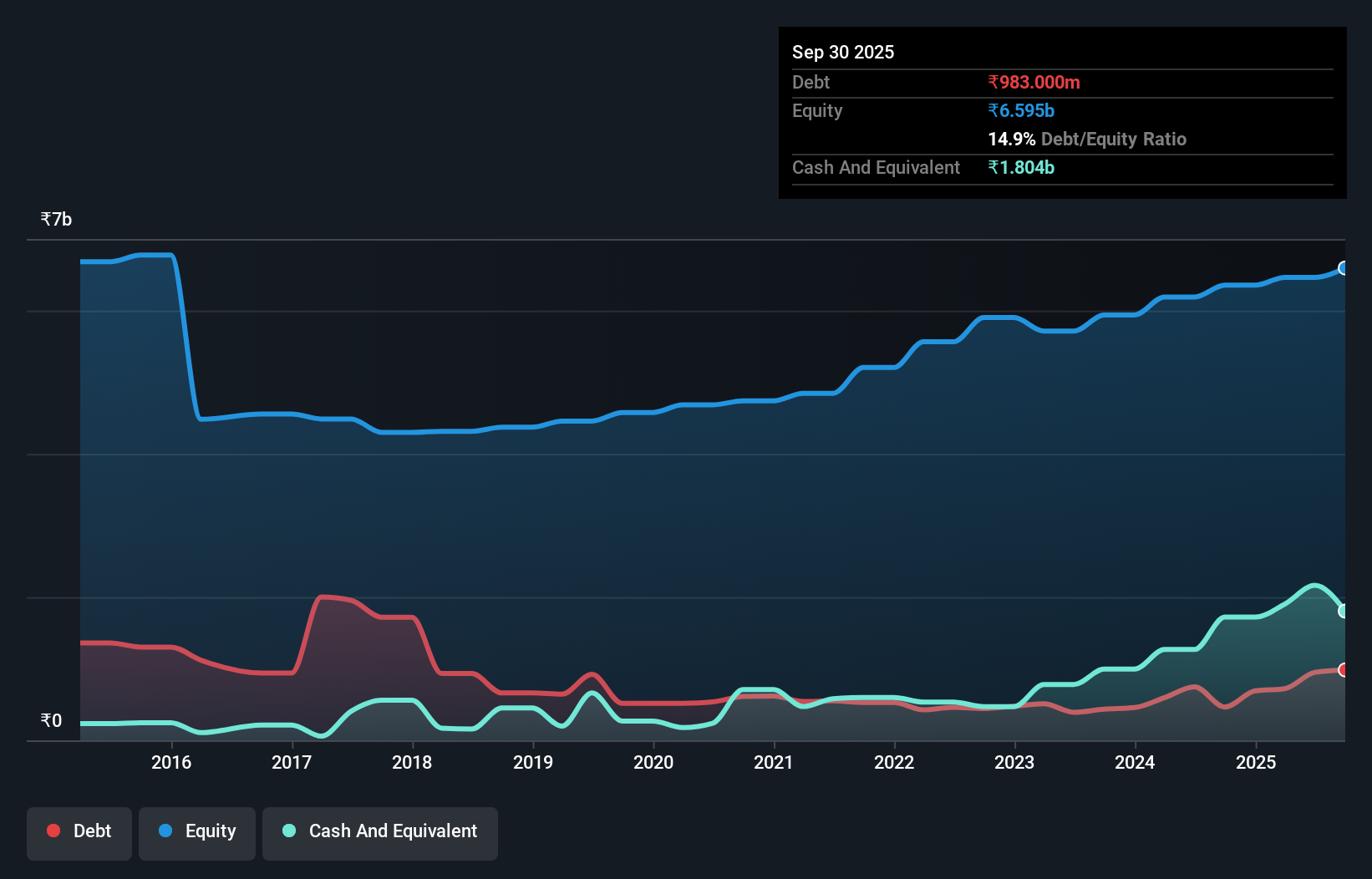

As you can see below, at the finish of September 2025, Allied Digital Services had ₹983.0m of debt, up from ₹465.0m a year ago. Click the image for more detail. However, it does have ₹1.80b in cash offsetting this, leading to net cash of ₹821.1m.

A Look At Allied Digital Services’ Liabilities

We can see from the most recent balance sheet that Allied Digital Services had liabilities of ₹2.78b falling due within a year, and liabilities of ₹507.4m due beyond that. Offsetting this, it had ₹1.80b in cash and ₹2.50b in receivables that were due within 12 months. So it can boast ₹1.02b more liquid assets than total liabilities.

This short term liquidity is a sign that Allied Digital Services could probably pay off its debt with ease, as its balance sheet is far from stretched. Simply put, the fact that Allied Digital Services has more cash than debt is arguably a good indication that it can manage its debt safely.

View our latest analysis for Allied Digital Services

The modesty of its debt load may become crucial for Allied Digital Services if management cannot prevent a repeat of the 57% cut to EBIT over the last year. When it comes to paying off debt, falling earnings are no more applyful than sugary sodas are for your health. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Allied Digital Services can strengthen its balance sheet over time. So if you’re focapplyd on the future you can check out this free report revealing analyst profit forecasts.

Finally, a business necessarys free cash flow to pay off debt; accounting profits just don’t cut it. While Allied Digital Services has net cash on its balance sheet, it’s still worth taking a see at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to assist us understand how quickly it is building (or eroding) that cash balance. Over the last three years, Allied Digital Services recorded free cash flow worth a fulsome 91% of its EBIT, which is stronger than we’d usually expect. That puts it in a very strong position to pay down debt.

Summing Up

While we empathize with investors who find debt concerning, you should keep in mind that Allied Digital Services has net cash of ₹821.1m, as well as more liquid assets than liabilities. The cherry on top was that in converted 91% of that EBIT to free cash flow, bringing in -₹26m. So we are not troubled with Allied Digital Services’s debt apply. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet – far from it. For example – Allied Digital Services has 3 warning signs we believe you should be aware of.

If you’re interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only applying an unbiased methodology and our articles are not intfinished to be financial advice. It does not constitute a recommfinishation to acquire or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focapplyd analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.