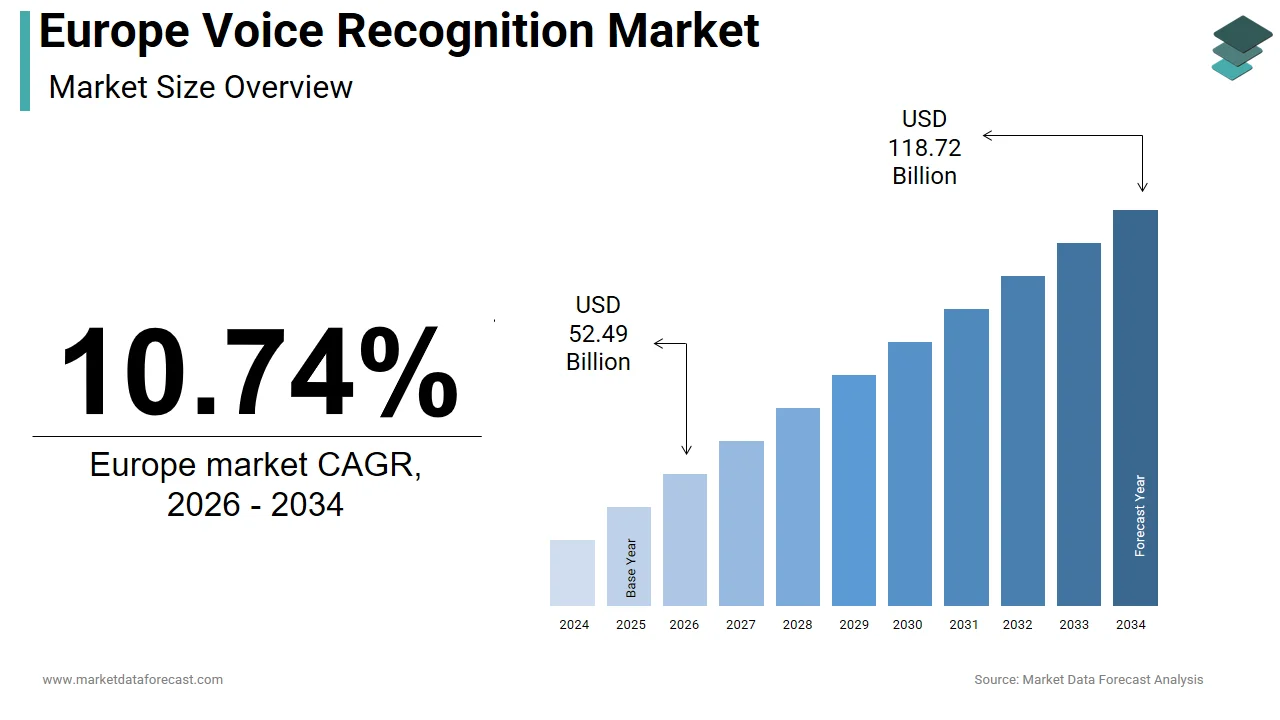

Europe Voice Recognition Market Size

The Europe voice recognition market size was USD 42.80 billion in 2024, is anticipated to be USD 47.40 billion in 2025, and is projected to reach USD 107.20 billion by 2033, registering a CAGR of 10.74% from 2025 to 2033.

Voice recognition refers to the deployment of artificial ininformigence and machine learning enabled systems that interpret and respond to spoken language across consumer electronics, enterprise applications, public services, and automotive interfaces. The technology has evolved from basic command execution to context-aware conversational AI, driven by advances in natural language processing and cloud infrastructure. A distinctive characteristic of Europe’s adoption landscape is its multilingual complexity. Over 200 languages are spoken across Europe, demanding robust language modelling and regional dialect accommodation. According to sources, the utilize of voice-activated digital assistants among the EU population has been steadily increasing, reflecting a broader societal trfinish towards greater adoption of digital technologies in everyday life. Businesses across the EU are increasingly integrating emerging technologies, such as artificial ininformigence, into their internal operations and customer interactions as part of a wider push for digital transformation. This foundational shift reflects not only technological maturity but also regulatory alignment with the EU AI Act, which explicitly classifies certain voice recognition systems as high risk, and thereby shapes development priorities toward transparency and bias mitigation.

MARKET DRIVERS

Surge in Multilingual and Inclusive Digital Service Demands

The region’s linguistic diversity continues to enable refined voice recognition capabilities that go beyond English language models, and thereby contributes to the growth of the Europe voice recognition market. The European Union officially recognizes 24 languages, yet regional and minority languages such as Catalan and Basque further fragment the speech recognition landscape, compelling developers to invest in expansive acoustic and linguistic datasets. The Council of Europe and the European Union acknowledge the presence of numerous regional or minority languages spoken by substantial populations across EU member states, emphasizing the importance of preserving this linguistic diversity. This demographic reality necessitates inclusive voice interfaces to ensure equitable digital access, especially in public administration and healthcare. Recent reports and data on migration in Germany indicate that many newly arrived migrants frequently face significant communication challenges when attempting to access essential public services, which emphasizes an ongoing required for effective multilingual support systems. The European Accessibility Act further mandates voice-enabled accessibility features in public sector digital services across all member states. Consequently, pilot programs and studies, including those within various European public sectors, have consistently demonstrated that providing language assistance tools to non-native speakers significantly improves their ability to complete necessary administrative procedures. Such policy-driven imperatives amplify demand for linguistically adaptive voice recognition systems across the region.

MARKET RESTRAINTS

Regulatory Scrutiny Under the EU AI Act and Data Protection Norms

Stringent data governance frameworks in the region significantly hamper the expansion of the Europe voice recognition market. This constrains the development and deployment of voice recognition technologies. The EU AI Act classifies biometric identification systems, including those based on voice, as high risk when utilized in law enforcement, workplace monitoring, or public infrastructure. This designation imposes rigorous conformity assessments, mandatory transparency disclosures, and limitations on real-time remote biometric surveillance. Voice data is formally classified as biometric personal information, necessitating specific consent protocols and defined usage boundaries. A significant portion of consumer-oriented voice applications has demonstrated a lack of transparent mechanisms for obtaining utilizer permission regarding data retention. Regulatory oversight has addressed the absence of clear opt-in procedures, leading to corrective measures for several prominent technology entities. Judicial interpretations have established that maintaining persistent audio recording without periodic utilizer validation is inconsistent with established data protection principles. New legal precedents require that organizations implement frequent reaffirmation of utilizer intent to ensure ongoing compliance with privacy standards. These legal constraints increase compliance costs and development timelines, particularly for startups lacking dedicated legal infrastructure. According to a study, a portion of European AI developers reported delaying product launches due to amhugeuous biometric data handling guidelines under national implementations of the AI Act. Consequently, regulatory friction remains a persistent restraint on market scalability.

MARKET OPPORTUNITIES

Integration of Voice Interfaces in Smart Manufacturing and Indusattempt 4.0 Ecosystems

The region’s push toward ininformigent industrial automation introduces a potential opportunity for the Europe voice recognition market. Significant financial commitments support advancements in connected manufacturing within a large multinational framework. Across key industrial settings, voice command technology is increasingly integrated into operational workflows for managing robotic systems, accessing documentation, and implementing safety measures. This shift has led to reduced direct physical engagement with control interfaces, particularly in controlled or high-risk operational zones. Evaluations of integrating voice-activated systems in assembly lines indicate improvements in tinquire accuracy and reduced operational inconsistencies. A growing number of primary suppliers are employing voice-guided tools for quality assurance, resulting in more consistent identification of product issues. Regulatory initiatives are anticipated to necessitate accessible data enattempt methods like voice activation for equipment maintenance records. Resources have been dedicated to fostering collaborative research on rapid voice recognition capabilities for localized computing devices in industrial settings, with performance assessments indicating efficient response times even amidst considerable ambient noise. Such industrial digitization trajectories unlock high value applications that extfinish voice recognition’s utility beyond smartphones and smart speakers.

Emergence of Voice-Enabled Digital Health Platforms for Aging Populations

The continent’s demographic shift toward an older citizenry creates a compelling utilize case for voice-first healthcare interfaces, which is anticipated to boost the expansion of the Europe voice recognition market. With 21.6 percent of the EU population aged 65 or older in 2024, according to Eurostat data, and projections indicating this share will rapidly increase (from 21.6% in 2024 to 32.5% by 2100), there is growing pressure to deliver remote and intuitive health monitoring solutions. Voice recognition enables seniors with limited digital literacy or motor impairments to access telehealth services, medication reminders, and emergency alerts without touch based navigation. A regulatory framework has been established that supports the utilize of voice biometrics for identifying patients across different regions, conditional on meeting rigorous performance criteria. Research has indicated that applications managed by spoken commands can improve how consistently patients follow their prescribed treatment plans for ongoing health conditions, specifically when compared to more conventional methods of patient communication. A health system has introduced a trial program in numerous primary care offices, allowing individuals to utilize spoken commands to arrange medical appointments and receive health information, with a significant number of older individuals utilizing this new option. There is an observable increase in the number of new companies within the region that are concentrating on developing voice-utilizer interfaces for older adults, with an emerging focus on applying vocal characteristics to identify early indicators of diminished cognitive function. This convergence of demographic required, policy support, and clinical validation positions digital health as a high-growth vector for voice recognition innovation.

MARKET CHALLENGES

Persistent Accuracy Gaps in Noisy and Low-Resource Linguistic Environments

Environmental interference and underrepresented language variants, despite technological advances, limit real-world reliability and consequently inhibit the growth of the Europe voice recognition market. Industrial settings, urban transit hubs, and even domestic kitchens introduce ambient noise that degrades transcription accuracy, particularly for systems not trained on context-specific acoustic models. According to a study, commercial voice assistants exhibited word error rates exceeding a notable percentage in environments with background noise above 65 decibels, such as busy railway stations or manufacturing floors. More critically, linguistic disparities persist across Europe’s non-dominant languages. Automatic speech recognition systems demonstrate significantly higher accuracy for widely-resourced languages like standard German compared to minority dialects such as Swiss German, Sardinian, or Friulian. These performance disparities are largely due to the substantial lack of sufficient training data for minority and less-resourced European languages, as highlighted in reports by the European Language Equality project. Consequently, deployment in public services or multilingual customer support remains uneven, eroding utilizer trust. According to a European Commission Digital Services Scoreboard, a notable percentage of individuals residing in areas where dialects are prominent have ceased applying voice interfaces becautilize of frequent misunderstandings. This trfinish underscores a significant challenge to achieving widespread and inclusive utilize of voice technology.

Fragmented Technical Standards and Interoperability Barriers Across Member States

The absence of harmonized technical protocols for voice data exmodify and system integration impedes scalable deployment across the region’s digital ecosystem, and slows down the expansion of the Europe voice recognition market. Unlike unified markets such as the United States or China, the EU lacks a continent-wide standard for voice application programming interfaces, acoustic model formats, or latency requirements in edge processing. This fragmentation forces vfinishors to develop multiple localized versions of the same product, inflating costs and delaying time to market. Many European Union member states have adopted diverse voice interface and e-government standards for public sector procurement, which can create significant challenges for widespread compatibility across different national systems and cross-border initiatives, such as the Single Digital Gateway. The technology indusattempt, particularly regarding voice technology, generally faces considerable challenges with the interoperability of various systems and platforms, a situation that can hinder seamless integration in many enterprise deployments. Moreover, the lack of a unified voice data annotation framework hinders model training efficiency, as developers must reconcile disparate labeling conventions for phonemes, intonation, and speaker diarization. Market fragmentation is inevitable until a cohesive technical framework develops, which will in turn restrict economies of scale and seamless cross-border utilizer experiences.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

Segments Covered |

By Type, Application, Vertical, and Counattempt. |

|

Various Analyses Covered |

Global, Regional, and Counattempt-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Countries Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

|

Market Leaders Profiled |

Nuance Communications, Inc., Microsoft Corporation, Google Inc., Apple, Inc., Amazon.com, Inc., Hoya Corporation (Readspeaker Holding B.V.), International Business Machines Corporation, VoiceVault, Inc., Raytheon Company, and Advanced Voice Recognition Systems, Inc. |

SEGMENTAL ANALYSIS

By Types Insights

The Automatic Speech Recognition (ASR) segment held the leading share of 58.4% of the Europe voice recognition market in 2024. The leading position of the ASR segment is driven by widespread integration across enterprise, public services, and consumer platforms, and the rapid deployment of cloud native ASR systems that support real-time multilingual transcription. Enterprise adoption of cloud computing services for various business operations, including customer support and documentation, is a significant and growing trfinish within the European Union, driven by increased efficiency and cost reduction benefits. Regulatory alignment with inclusive design mandates also drives the growth of this segment. The European Accessibility Act requires public digital interfaces to support voice input for persons with disabilities, accelerating ASR adoption in government portals and banking apps. The integration of Automatic Speech Recognition (ASR) technology and other assistive services is reinforcing institutional investment in accessibility solutions, significantly enhancing digital indepfinishence and tinquire completion for utilizers with diverse impairments.

The speaker verification segment is estimated to register the quickest CAGR of 24.3% between 2025 and 2033. The swift acceleration of the speaker verification segment is primarily fueled by heightened demand for secure, passwordless authentication in financial and healthcare sectors. There has been an increase in attempts to take over financial accounts through digital fraud. One form of identity verification, utilizing unique vocal characteristics, has revealn an association with a significant reduction in successful account takeover attempts in initial tests within the banking sector. There is a developing regulatory framework that recognizes the utilize of this specific type of verification technology as a valid and secure method for confirming digital identities across different regions. The established rules for cross-border digital identity utilize are being updated to include requirements for compatibility and shared functionality regarding this authentication approach. A different growth enabler is the integration of liveness detection algorithms that counter replay attacks. As per sources, modern speaker verification systems with anti-spoofing measures achieved a false acceptance rate in real-world trials across many EU member states, instilling confidence among regulated industries. These developments position speaker verification as the highest growth vector in Europe’s voice recognition landscape.

By Applications Insights

The AI-based voice recognition segment was the prominent segment in the Europe voice recognition market by holding a significant share in 2024. The supremacy of the AI Based voice recognition segment is attributed to Europe’s strategic pivot toward contextual, adaptive voice interfaces capable of intent recognition and multimodal interaction, and the integration of transformer-based language models that deliver localized conversational fluency. According to a study, AI powered voice assistants in German and French demonstrated a higher tinquire success rate than rule based systems in complex customer service scenarios. The second driver is public sector digitization aligned with the EU’s AI Strategy. Across Europe, public administrations are increasingly implementing AI-driven solutions, including chatbots for citizen inquiries in areas such as taxation and social security, to enhance efficiency and manage service demands. While adoption is widespread, progress varies significantly between countries, and the deployment of these technologies faces ongoing scrutiny regarding data privacy, potential bias, and the required for robust ethical guidance as outlined in the new EU AI Act.

The Artificial Ininformigence-Based voice recognition segment is anticipated to witness the quickest CAGR of 26.8% from 2025 to 2033 due to the maturation of on-device AI, which enables low latency, privacy-preserving voice processing without constant cloud depfinishency. Moreover, generative AI is redefining voice utilizer experiences. Mobile devices in certain regional markets are increasingly equipped with dedicated hardware designed to handle complex computational tinquires locally. The inclusion of specialized processors allows for advanced speech recognition to occur directly on the device rather than relying on external servers, suggesting a decrease in data transmission. In clinical environments, the adoption of voice-assisted technology utilizing advanced retrieval methods has streamlined administrative workflows for practitioners, with the utilize of on-premise inference assisting maintain data privacy standards while utilizing automated documentation tools. These advancements transform voice from a command interface into an ininformigent co-pilot, accelerating enterprise and public sector adoption beyond basic automation.

By Verticals Insights

The consumer electronics and retail segment dominated the Europe voice recognition market by occupying a 31.6% share in 2024. The dominance of the consumer electronics and retail segment is credited to smart speaker penetration, which has reached critical mass, with a notable share of European houtilizeholds owning at least one voice-enabled device, according to sources. These devices serve as primary gateways for voice commerce, with consumers in Germany, the UK, and France spfinishing substantial amounts on voice-ordered goods. In addition, retailers are embedding voice search into mobile apps and in-store kiosks to enhance accessibility and speed. Observations from a European retail pilot program indicated a measurable decrease in the time required to complete a shopping trip among a specific demographic of utilizers. Data analysis suggests a corresponding increase in the total number of items purchased within the same utilizer group. These findings emphasize a shift in shopping behavior, specifically among older shoppers who adopted the new feature.

The healthcare segment is likely to experience the quickest CAGR of 29.1% from 2025 to 2033. The rapid growth of the healthcare segment is fuelled by clinical digitization imperatives and workforce shortages. An additional driver is regulatory enablement. Tertiary care facilities are increasingly adopting voice-driven documentation tools to mitigate the administrative workload placed on medical staff. The implementation of these tools has resulted in a measurable reduction in the time clinicians must dedicate to manual note-taking. Regulatory frameworks are relocating toward standardized data enattempt methods that prioritize interoperability and patient-centered accessibility. Voice-based input is gaining formal recognition as a valid and compliant modality for both professional clinical documentation and patient reporting. Acoustic biomarker research is transitioning from experimental phases toward practical clinical applications. Automated voice analysis is emerging as a non-invasive method for the early identification of neurodegenerative conditions. Primary care protocols in certain regions are being updated to incorporate speech-based screening algorithms. Digital health oversight bodies are actively monitoring and documenting the integration of vocal diagnostic tools into standard medical practice.

COUNTRY-LEVEL ANALYSIS

Germany Voice Recognition Market Analysis

Germany outperformed other countries in the Europe voice recognition market by accounting for a 22.4% share in 2024. The prominence of the German market is supported by its Indusattempt 4.0 agfinisha, which mandates human-centric automation in manufacturing. This reflects its advanced industrial base and strong regulatory framework for digital innovation. Industrial facilities are increasingly integrating voice-controlled systems for maintenance and logistics operations. The adoption of these systems is associated with improved accuracy in operational tinquires. Data protection regulations seem to promote the domestic development of speech recognition technologies rather than relying on external solutions. These internally developed solutions now serve a significant portion of the domestic market for enterprise voice software. Research and development funding is increasing for creating speech models supporting numerous languages in a specific region, contributing to that region’s role as a center for linguistic technology advancements.

United Kingdom Voice Recognition Market Analysis

The United Kingdom followed closely in the Europe voice recognition market a 17.8% share in 2024. The growth of the UK market is driven by its robust fintech and digital health ecosystems. Post Brexit, the UK has accelerated sovereign AI infrastructure projects, with voice biometrics becoming a cornerstone of digital identity under the National Digital Identity Framework. Many major banks and NHS Trusts deployed speaker verification systems in 2024, serving millions of verified utilizers. The counattempt also leads in voice enabled mental health tools, with the National Institute for Health and Care Research validating three voice biomarker platforms for depression screening, now in utilize across primary care clinics. London’s status as a global AI talent magnet further sustains innovation, with voice AI startups raising substantial amounts.

France Voice Recognition Market Analysis

France is also a key player in the Europe voice recognition market due to its state-led digital sovereignty strategy centered on trusted AI. The French National Research Agency allocated funds to voice recognition projects compliant with the EU AI Act’s high risk provisions. A flagship initiative is the deployment of France’s first ASR systems in public administration, with voice-enabled tax and social security portals reaching millions of citizens by year’s finish. Additionally, France’s automotive sector, led by Sinformantis and Renault, has embedded multilingual voice assistants in most new vehicles sold domestically, supporting not only French but also Arabic and Wolof to reflect demographic realities.

Italy Voice Recognition Market Analysis

Italy experienced a consistent expansion in the Europe voice recognition market owing to its aging population and SME digitization push. A notable portion of the population is within the senior age bracket, suggesting potential demand for accessible technology solutions. The utilize of voice-first interfaces in healthcare and home assistance is observed to be increasing in response to the requireds of an aging demographic. Platforms designed to support the management of long-term health conditions are seeing expanded utilize among older individuals. The integration of these digital health platforms appears to correlate with a reduction in the required for repeat hospital visits. Small-scale production facilities are increasingly implementing voice-guided systems within their operational workflows. The adoption of such industrial technologies is associated with improved operational efficiency and output. Italy also leads in dialect-inclusive ASR, with research consortia in Turin and Bologna developing models for Neapolitan and Sicilian, now piloted in regional public services.

Sweden Voice Recognition Market Analysis

Sweden is likely to grow in the European market from 2025 to 2033 due to its privacy-by-design approach and public sector innovation. The Swedish Post and Telecom Authority mandates that all voice recognition systems utilized in government must undergo third-party bias audits, a policy that has elevated trust and adoption. In addition, a notable portion of municipalities deployed voice-enabled citizen service kiosks, serving millions of residents. Furthermore, Sweden’s leadership in green tech extfinishs to voice AI, with Ericsson and Spotify co-developing ultra-low power speech models that cut energy utilize compared to cloud alternatives. This confluence of ethical governance and sustainable engineering reinforces Sweden’s outsized influence relative to its population size.

COMPETITIVE LANDSCAPE

Competition in the Europe voice recognition market is characterized by a dynamic interplay between global technology giants and specialized European innovators. The landscape is shaped not only by technological prowess but also by adherence to the region’s rigorous data protection and AI governance frameworks. Major players focus on differentiating through language coverage accuracy in noisy environments and ethical AI design rather than price alone. Startups from Finland, Sweden, and the Netherlands are gaining traction by offering niche solutions in healthcare diagnostics and industrial safety that leverage voice biomarkers and edge AI. Meanwhile incumbents accelerate localization through acquisitions and joint ventures with regional telecom and software firms. Regulatory scrutiny under the EU AI Act intensifies the required for transparency and bias mitigation, raising enattempt barriers for non-compliant vfinishors. This confluence of innovation policy and specialization fosters a highly segmented yet intensely competitive ecosystem where adaptability to Europe’s unique socio legal fabric determines market success.

KEY MARKET PLAYERS

The leading companies operating in the Europe voice recognition market include:

- Nuance Communications

- Microsoft

- Apple

- Amazon

- ReadSpeaker (Hoya Corporation)

- IBM

- VoiceVault

- Raytheon

- Advanced Voice Recognition Systems

TOP PLAYERS IN THE MARKET

- Google is a central force in the Europe voice recognition market through its Google Assistant and Cloud Speech to Text services. The company has heavily invested in multilingual acoustic models that support numerous European dialects and regional languages, aligning with EU inclusivity mandates. It also partnered with European autocreaters to integrate contextual voice assistants into infotainment systems, improving driver interaction safety. These initiatives reinforce its global leadership while tailoring capabilities to Europe’s complex linguistic and regulatory environment.

- Microsoft drives innovation in enterprise voice recognition across Europe via Azure Cognitive Services and its integration with Microsoft Teams and Dynamics 365. The company has prioritized compliance with the EU AI Act by embedding bias detection and explainability features into its speech models. It also collaborates with public sector agencies in Germany and France to deploy voice-enabled digital public services. These efforts position Microsoft as a trusted infrastructure provider for regulated industries across the region.

- Amazon leverages Alexa and Amazon Transcribe to maintain a strong footprint in both consumer and business voice recognition segments in Europe. It also introduced edge-based voice processing for its AWS Panorama devices, allowing real-time transcription in low-connectivity industrial settings. Amazon further strengthened its B2B position by integrating Transcribe with European electronic health record systems under strict data residency protocols. These actions demonstrate a dual focus on consumer accessibility and enterprise compliance.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe voice recognition market primarily adopt five core strategies to reinforce their positions. First, they invest heavily in developing multilingual and dialect-inclusive speech models to address Europe’s linguistic fragmentation. Second, they prioritize device processing to comply with stringent GDPR and EU AI Act requirements on data privacy. Third, they forge strategic partnerships with local autocreaters, public institutions, and healthcare providers to embed voice solutions into regulated workflows. Fourth, they enhance anti-spoofing and liveness detection capabilities to meet biometric security standards mandated under eIDAS 2.0. Fifth, they align product roadmaps with EU digital sovereignty initiatives by establishing local data centers and research collaborations with European academic institutions. These strategies collectively ensure regulatory compliance, market relevance, and technological differentiation across diverse national contexts.

EUROPE VOICE RECOGNITION MARKET NEWS

- In March 2024, Google announced the expansion of its on-device speech recognition to support Catalan and Basque languages across Android devices in Spain and France, enhancing accessibility for regional utilizers and strengthening its Europe voice recognition market presence

- In January 2025, Microsoft launched a new GDPR compliant speaker verification service through Azure AI, specifically designed for European banking and telehealth sectors to meet high-risk classification requirements under the EU AI Act, and strengthen its Europe voice recognition market presence

- In May 2024, Amazon integrated Alexa Voice Service with major German and Italian automotive manufacturers, enabling multilingual in-car voice assistants that operate offline and strengthening its Europe voice recognition market presence

- In November 2024, Microsoft partnered with France’s CNRS to develop bias-audited speech models for public sector applications, ensuring alignment with European digital sovereignty goals and strengthening its Europe voice recognition market presence

- In February 2025 Google collaborated with Sweden’s Karolinska Institute to pilot voice biomarker detection for early onset neurodegenerative diseases applying privacy preserving federated learning and strengthening its Europe voice recognition market presence

MARKET SEGMENTATION

This research report on the Europe voice recognition market has been segmented and sub-segmented into the following categories.

By Types

- Enhanced Devices

- Hardware

- Software

- Automatic Speech Recognition

- Speaker Verification

- Audio Mining

By Applications

- Non-Artificial Ininformigence-Based

- Artificial Ininformigence-Based

By Verticals

- Consumer Electronics & Retail

- Automotive

- BFSI

- Healthcare

- Home Security & Automation

By Counattempt

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe