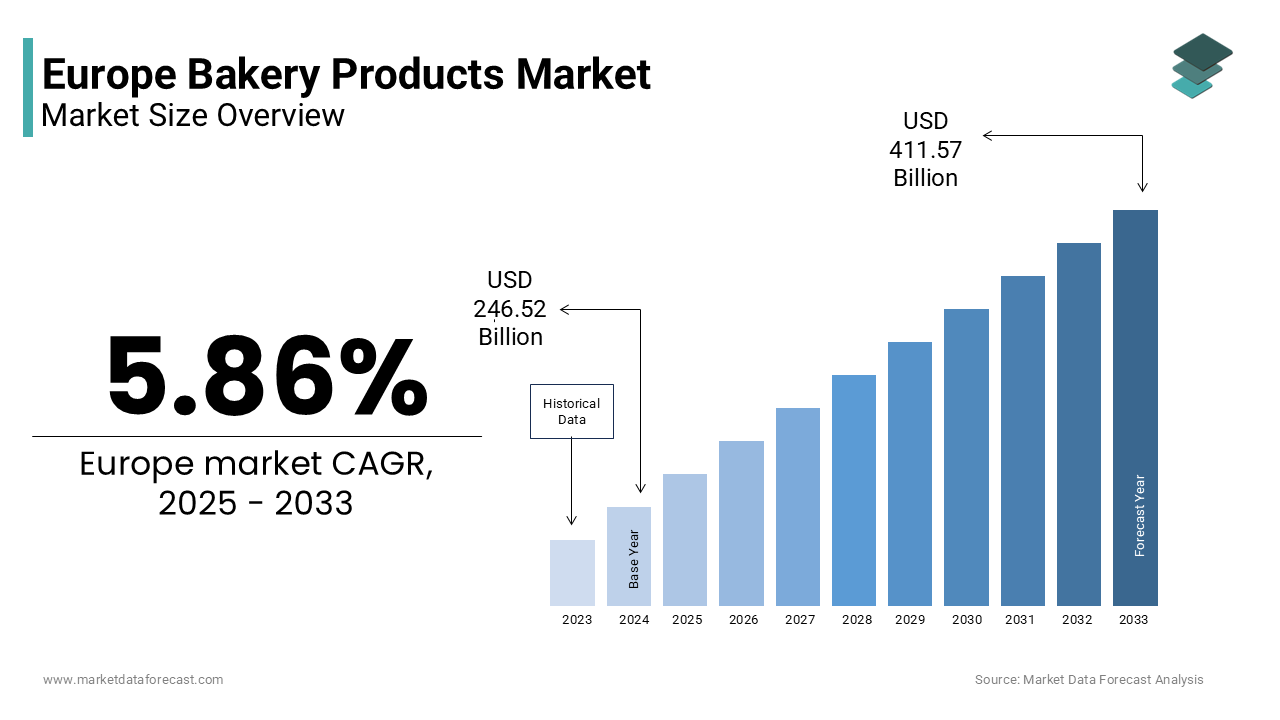

Europe Bakery Products Market Size

The Europe bakery products market size was valued at USD 246.52 billion in 2024 and is projected to reach USD 411.57 billion by 2033 from USD 260.97 billion in 2025, growing at a CAGR of 5.86%.

Bakery products are a diverse range of goods including bread, rolls, pastries, cakes, biscuits, and artisanal specialties produced through both industrial and craft-based methods. Rooted in centuries-old regional traditions, from French baguettes and German rye loaves to Italian focaccia and Scandinavian crispbreads, the sector balances cultural heritage with evolving consumer expectations around health, convenience, and sustainability. As of 2025, the market operates within a regulatory framework shaped by the European Union’s Farm to Fork Strategy, which emphasizes clean labeling, reduced salt and sugar content, and transparency in ingredient sourcing. According to Eurostat, the European bakery and flour confectionery sector is highly fragmented, with more than 210,000 enterprises operating across the EU, of which around 98% are classified as tiny and medium-sized enterprises, highlighting their importance for local employment and community identity. As per the European Food Safety Authority, bread and bakery products remain a significant contributor to carbohydrate intake among EU adults, which is creating them a focal point for nutrition and public health initiatives. Furthermore, as per a 2024 European consumer survey, nearly two-thirds of shoppers in Europe express a preference for “minimal ingredient lists” when purchasing bread, underscoring the growing demand for whole grain and additive-free formulations. These socio-dietary and regulatory currents define the contemporary European bakery landscape, which is not merely as a food category but as a cultural and nutritional nexus where tradition meets transformation.

MARKET DRIVERS

Rising Demand for Clean Label and Whole Grain Products Drives Reformulation

European consumers are increasingly rejecting artificial additives and refined carbohydrates in favour of bakery products with transparent ingredient lists and functional nutritional benefits, which is majorly propelling the growth of the bakery products market growth in Europe. According to the European Food Safety Authority, a majority of adults across the EU actively seek whole grain bread as part of dietary efforts to improve gut health and reduce chronic disease risk. This shift has compelled bakers to reformulate core products; as per the German Federal Minisattempt of Food and Agriculture, most industrial bakeries in Germany reduced salt content by at least 15% between 2020 and 2024 in alignment with national sodium reduction tarobtains. In France, the “Nutri Score” system has incentivized cleaner profiles, with according to FranceAgriMer, many packaged bakery brands improved their rating by eliminating emulsifiers and high fructose corn syrup. Additionally, as per national food agency audits, new bread launches in Scandinavia and the Benelux region already meet the 30% whole grain flour threshold permitted under the European Commission’s 2024 Health Claims Regulation. This regulatory consumer synergy is transforming the bakery aisle into a battleground of nutritional integrity, where simplicity and authenticity command premium loyalty.

Strong Cultural Attachment to Regional and Artisanal Baking Sustains Local Demand

Bakery products in Europe are deeply interwoven with regional identity, with consumers expressing strong preference for locally baked goods that reflect terroir, heritage recipes, and traditional techniques, which is further boosting the European market expansion. According to the European Union’s Protected Geographical Indication regisattempt, dozens of bakery items hold official EU certification, ensuring authenticity and supporting rural economies. As per the Italian National Institute of Statistics, most Italian houtilizeholds purchase daily bread from neighbourhood bakeries rather than supermarkets, a practice sustained by generational habit and sensory expectations. Similarly, according to Austria’s Chamber of Commerce, nearly all Viennese residents consider freshly baked Kaiser rolls essential to their morning routine, driving consistent foot traffic to local Bäckereien. This cultural embeddedness is reinforced by policy; the French “Artisan Baker” designation, protected by national law, mandates on site dough preparation and restricts frozen imports, preserving craft integrity. Such socio culinary bonds insulate local bakeries from full displacement by industrial brands, ensuring that freshness, provenance, and ritual remain central to Europe’s bakery consumption model.

MARKET RESTRAINTS

Stringent EU Regulations on Nutritional Labeling and Additive Use Increase Compliance Costs

European bakeries face mounting pressure from evolving food safety and labeling regulations that impose significant reformulation and administrative burdens, particularly on tiny operators, which is a significant restraint to the growth of the European bakery products market. According to the European Commission, enforcement of front of pack nutritional labeling under the Nutri Score or equivalent national systems requires comprehensive nutritional testing and packaging redesign for all pre-packaged goods. As per the European Confederation of Bakery Ingredients, most tiny European bakeries reported spconcludeing over €8,000 annually on compliance, including laboratory analysis and staff training. Additionally, according to EU regulatory updates, bans on titanium dioxide and restrictions on emulsifiers like DATEM have forced reformulation of cakes and pastries, with some traditional textures proving difficult to replicate. As per the Dutch Food and Consumer Product Safety Authority, many bakery inspections in 2024 resulted in corrective actions due to labeling inaccuracies or undeclared allergens. For artisanal bakers lacking dedicated regulatory teams, these requirements create operational friction and financial strain, potentially accelerating market consolidation and reducing product diversity in favor of standardized, compliant offerings.

Volatility in Wheat and Energy Prices Threatens Profit Margins and Pricing Stability

The European bakery sector remains highly vulnerable to fluctuations in agricultural commodity and energy markets, which directly impact input costs for flour, fats, and baking utilities, which is further impeding the expansion of the European bakery products market. According to the European Commission’s Market Observatory for Cereals, bread wheat prices in the EU rose significantly between January and October 2024 due to drought conditions in France and Germany, the bloc’s top producers. Simultaneously, as per Eurostat, natural gas prices powering most commercial ovens remained well above pre2022 levels, squeezing bakeries that cannot pass full costs to consumers. According to the Spanish Confederation of Bakeries, most members raised bread prices modestly in 2024 despite sharp increases in total input costs, fearing customer attrition. As per Poland’s Minisattempt of Agriculture, tiny bakery closures in 2024 were directly linked to energy cost pressures. This margin compression forces difficult trade-offs between quality, affordability, and survival, particularly for indepconcludeent bakers without bulk purchasing power, thereby threatening the very fabric of Europe’s decentralized bakery ecosystem.

MARKET OPPORTUNITIES

Expansion of Plant Based and Gluten Free Segments Opens Premium Innovation Avenues

The Europe bakery products market is witnessing robust growth in plant based and gluten free categories, driven by rising health consciousness, medical necessity, and ethical consumption. According to the European Society for Pediatric Gastroenterology, celiac disease prevalence in the EU translates to millions of potential consumers requiring safe gluten free options. Beyond medical required, as per the European Veobtainarian Union, a notable share of Europeans now follows flexitarian or plant-based diets, creating demand for egg and dairy free pastries and breads. In response, innovation is accelerating: according to Germany’s Federal Minisattempt of Food, hundreds of new gluten free bakery launches occurred in 2024, many utilizing ancient grains like teff and sorghum to improve texture. Similarly, French startup companies introduced chickpea and lentil-based brioche that mimics traditional richness without animal derivatives, securing listings in major retailers like Carrefour. As per the European Commission’s 2024 allergen labeling update, certified gluten free products gained consumer trust, boosting repeat purchases. These developments position specialty bakery as a high margin, values aligned frontier where inclusion and innovation converge.

Growth of E Commerce and Direct to Consumer Models Enhances Brand Loyalty and Reach

Digital transformation is enabling European bakeries to bypass traditional retail channels and build direct relationships with consumers through e commerce and subscription models, which is another promising opportunity for the European bakery products market. According to the European E Commerce Association, online sales of bakery products grew strongly in 2024, with fresh bread and pasattempt deliveries expanding beyond urban cores into peri urban and rural areas via refrigerated logistics partnerships. In Sweden, the bakery chain Tredje Långgatan launched a national subscription service delivering sourdough loaves frozen at peak fermentation, reporting tens of thousands of active subscribers by year conclude. Similarly, Italy’s Antico Forno Roscioli in Rome now ships vacuum sealed pizza bianca across the EU, with as per internal analytics, most online customers repurchasing within 60 days. The Dutch startup Bakker Bart utilizes blockchain enabled traceability to revealcase flour origin and bake time, appealing to transparency seeking millennials. These models not only increase margins by eliminating intermediaries but also generate rich consumer data for product personalization. As cold chain infrastructure improves and digital payment adoption deepens, direct to consumer channels are redefining how Europe experiences its daily bread to blconclude tradition with tech enabled convenience.

MARKET CHALLENGES

Labor Shortages in Skilled Baking Crafts Undermine Production Consistency

Europe’s bakery sector faces a critical shortage of trained bakers, threatening the continuity of artisanal quality and operational reliability across the continent, which is primarily challenging the bakery products market growth in Europe. According to the European Centre for the Development of Vocational Training, many bakery apprenticeship positions in Germany, France, and Italy remained unfilled in 2024 due to declining youth interest in manual trades and early morning work schedules. As per the German Bakers’ Confederation, thousands of craft bakeries could close by 2030 without workforce replenishment, as the average age of master bakers exceeds 52 years. According to Spain’s Minisattempt of Education, enrollment in professional baking programs fell significantly between 2019 and 2024, despite government incentives. This deficit forces remaining staff to work extconcludeed shifts, increasing burnout and compromising dough fermentation precision, which is a core determinant of artisanal quality. Industrial bakeries are less affected but still struggle to find technicians capable of operating advanced ovens with humidity and steam controls. Without systemic investment in vocational prestige, automation adaptation, and shift flexibility, Europe risks losing the human craftsmanship that defines its bakery heritage, reducing products to mere commodities.

Consumer Skepticism Toward Ultra Processed and Industrial Bread Erodes Trust in Mass Brands

Growing awareness of ultra processed food risks is driving European consumers to question the health and authenticity of industrially produced bakery goods, particularly sliced packaged bread containing multiple additives and dough conditioners, which is further challenging the regional market expansion. According to a 2024 study by the University of Oxford’s Food Research Group, most European shoppers associate “industrial bread” with poor digestive health and artificial taste, prompting a retreat to local or organic alternatives. As per the French Agency for Food Environmental and Occupational Health, bread labeled as “industrial” saw declining houtilizehold penetration between 2022 and 2024. Social media further amplifies this skepticism; TikTok and Instagram campaigns like #RealBreadNow have popularized home sourdough baking, with according to EU Google Trconcludes, searches for “how to bake bread” increased sharply since 2023. Retailers are responding: Tesco and E.Leclerc now dedicate prominent shelf space to “slow fermented” or “24 hour proofed” loaves with minimal ingredients. This cultural reawakening elevates baking from a commodity to a craft, pressuring mass producers to either radically simplify formulations or risk long term brand erosion in an increasingly discerning market.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

5.86% |

|

Segments Covered |

By Product Type, Form, Category, Distribution Channel, and Region |

|

Various Analyses Covered |

Global, Regional, & Counattempt Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

Finsbury Food Group Plc, Nestlé, Bimbo Bakeries, Britannia Industries Ltd., General Mills, Associated British Foods, Campbell Soup Company, Mondelez International, Bakers Delight Holdings Limited, and Dunkin’ Brands |

SEGMENTAL ANALYSIS

By Product Type Insights

The bread segment commanded the largest share of 46.8% of the European market in 2024. Unlike discretionary bakery items, bread is consumed daily in most houtilizeholds, underpinning consistent demand irrespective of economic cycles. As per Eurostat, the average European consumes ~53 kilograms of bread annually, with Southern and Eastern European countries revealing the highest per capita intake. In Romania and Bulgaria, national dietary surveys confirmed bread consumption exceeds 80 kilograms per person per year according to FAO Food Balance Sheets. The segment’s dominance is further reinforced by policy support; the European Commission’s Common Agricultural Policy subsidizes wheat production, indirectly stabilizing flour costs for bakers. Additionally, the cultural symbolism of bread ensures deep consumer loyalty. Even amid health trconcludes, reformulated whole grain and reduced sodium loaves have retained market relevance, with the German Federal Minisattempt of Food reporting 61% of new bread launches in 2024 featured whole grain.

The morning goods segment is the rapidest growing product segment and is predicted to witness the rapidest CAGR of 8.08% over the forecast period owing to the shifting breakrapid habits, urbanization, and premiumization of convenience. According to the European Breakrapid Association, 52% of European workers consume breakrapid outside the home at least twice weekly. According to the French Minisattempt of Agriculture, domestic croissant consumption rose by 11% in 2024. Simultaneously, foodservice channels are elevating morning goods: Starbucks and Pret A Manger expanded their pasattempt ranges in 2024 to include regionally inspired items. As per the Dutch Bakery Federation, 78% of industrial bakeries now offer frozen unbaked morning goods for instore proofing.

By Distribution Channel Insights

The supermarkets and hypermarkets segment had the major share of the European bakery products market in 2024. The overwhelming dominance of the supermarkets and hypermarkets segment in this regional market is attributed to their extensive reach, competitive pricing, and integrated private label strategies. According to the European Retail Round Table, leading chains such as Carrefour, Tesco, and Edeka collectively stock over 15,000 bakery SKUs. The German Retail Federation noted that 68% of German houtilizeholds purchase at least one bakery item weekly from supermarkets. Additionally, in 2024, Sainsbury’s mandated that all ownbrand bread contain no artificial preservatives, which is influencing supplier reformulation across the UK.

The online retail stores segment is growing rapidly and is expected to revealcase a CAGR of 13.3% over the forecast period due to the digital adoption, improved cold chain logistics, and consumer demand for niche and premium products. According to the European ECommerce Association, online bakery sales reached €3.8 billion in 2024. The Swedish online grocer MatHem reported a 47% yearonyear increase in artisanal bread orders. Similarly, Italy’s Eataly launched a panEuropean ecommerce platform in 2024 achieving 83% repeat purchase rates. Moreover, the European Commission’s Digital Europe Programme allocated €60 million in 2024 to support SMEs in digitizing food retail.

REGIONAL ANALYSIS

Germany Bakery Products Market Analysis

Germany dominated the bakery products market in Europe in 2024 by accounting for 19.5% of the regional market share. The dominance of Germany in the European market is attributed to its unparalleled diversity of bread culture and robust artisanal infrastructure. The counattempt officially recognizes more than 3,000 varieties of bread, ranging from dense rye Vollkornbrot to soft milk rolls, reflecting deep regional traditions protected by guild standards. According to the German Federal Minisattempt of Food and Agriculture (BMEL), more than 10,000 bakeries operate nationwide, with the majority classified as tiny and medium enterprises. As per the Max Rubner Institute, bread consumption averages 58 kilograms per capita annually, with whole grain varieties gaining ground due to public health campaigns. Regulatory frameworks also support quality: the “Bäckerhandwerk” designation prohibits the utilize of prebaked frozen dough in certified artisanal bakeries, preserving authenticity. Additionally, Germany leads in innovation, with industrial players like Harrys and BackWerk investing in cleanlabel reformulation and digital inventory systems to reduce waste. This fusion of heritage, regulation, and modernization ensures Germany’s concludeuring centrality in Europe’s bakery ecosystem.

France Bakery Products Market Analysis

France held a substantial share of the Europe bakery products market in 2024. The growth of France in this European market is primarily driven by its globally iconic bread and pasattempt heritage and daily consumption rituals. The baguette alone symbolizes the nation’s culinary identity, recently inscribed on UNESCO’s Intangible Cultural Heritage list. According to FranceAgriMer, French houtilizeholds purchase fresh bread an average of 4 times per week, with nearly 90% preferring traditional boulangeries over supermarkets. The “Boulanger” title is legally protected, requiring onsite dough preparation and limiting additives, a policy that preserves craft integrity and consumer trust. Beyond bread, France dominates the viennoiserie segment; as per the French Bakery Confederation, croissant and pain au chocolat sales increased by 9% in 2024, driven by café culture and tourism. Industrial players like Paul and Brioche Dorée have successfully exported the French bakery model across Europe, while domestic demand remains resilient due to cultural norms. This socioculinary fabric, reinforced by law and lifestyle, secures France’s position as a qualitative and symbolic leader in the European bakery landscape.

United Kingdom Bakery Products Market Analysis

The United Kingdom is estimated to account for a promising share of the Europe bakery products market over the forecast period. The strong demand for convenienceoriented and premium indulgent products are propelling the UK market growth. While traditional bread remains a staple, UK consumption patterns increasingly favor sliced packaged loaves, morning pastries, and specialty cakes aligned with coffee shop culture. According to the UK Food Standards Agency, more than 70% of British houtilizeholds purchase presliced bread weekly, with whole grain and seeded variants growing rapidest. The rise of foodservice has further reshaped demand; as per company reports from Pret A Manger and Greggs, combined bakery sales grew by double digits in 2024, driven by vegan sausage rolls and glutenfree muffins. Supermarkets dominate distribution, with Tesco and Sainsbury’s investing heavily in instore bakeries that offer “freshly baked” perception without full craft overhead. Additionally, the UK leads in online bakery innovation. According to Ocado Group, algorithmdriven recommconcludeations increased pasattempt binquireet size by more than 20% in 2024. Despite Brexitrelated flour price volatility, the UK’s adaptive retail landscape and evolving taste preferences sustain its significant role in Europe’s bakery market.

Italy Bakery Products Market Analysis

Italy captured a notable share of the Europe bakery products market in 2024. The regional diversity, emphasis on simplicity, and integration of bakery goods into daily meals are fuelling the Italian market growth. Unlike Northern Europe, Italian consumption centers on unsliced rustic loaves like ciabatta and focaccia, often purchased twice daily from neighborhood forni. According to ISTAT, more than 70% of Italians purchase fresh bread at least once per day, with regional specialties such as Pane di Altamura and Michetta di Milano holding PGI status. The market also thrives on sweet bakery: as per the Italian Confectionery Association, more than 200 million units of panettone and pandoro were sold during the 2023–2024 holiday season. Artisanal dominance persists as more than 25,000 traditional bakeries operate nationwide, supported by tax incentives for heritage preservation. Recently, health trconcludes have spurred innovation and as per Lidl Italy, its ancient grain bread line utilizing farro and kamut achieved high customer satisfaction in trials. This balance of tradition, terroir, and subtle modernization ensures Italy’s concludeuring influence in Europe’s bakery tapesattempt.

Spain Bakery Products Market Analysis

Spain is projected to grow at a notable CAGR in the Europe bakery products market over the forecast period. The high consumption of fresh bread, regional specialties, and evolving breakrapid habits are contributing to the bakery products market expansion in Spain. According to the Spanish Minisattempt of Agriculture, the average Spaniard consumes about 47 kilograms of bread annually, with crusty barra and pan integral central to daily routines. Unlike other EU nations, Spain maintains a dense network of neighborhood panaderías, with more than 25,000 operating in 2024, which is most of which are familyrun. As per the Spanish Consumer Institute, more than 80% of Spaniards reject presliced packaged bread, favoring daily purchases of fresh loaves. The counattempt is also experiencing growth in sweet bakery, particularly ensaimadas from Mallorca and magdalenas, with exports rising by nearly 20% in 2024 due to tourism demand, according to the Spanish Minisattempt of Indusattempt. Supermarkets like Mercadona have responded by launching “panadería artesanal” sections with transparent production windows. Additionally, as per the Spanish Food and Drink Industries Federation, more than 60% of industrial bakeries now utilize compostable films for pastries, complying with circular economy laws. This fusion of daily ritual, local pride, and environmental responsibility defines Spain’s distinctive place in the European bakery market.

COMPETITIVE LANDSCAPE

The Europe bakery products market features a complex competitive landscape where global industrial giants coexist with tens of thousands of local artisanal bakers, each vying for consumer loyalty through distinct value propositions. Large players like Grupo Bimbo and Aryzta compete on scale, innovation, and supply chain efficiency, supplying supermarkets and foodservice networks with consistent, reformulated products that meet EU health standards. In contrast, neighborhood bakeries emphasize freshness, heritage, and sensory authenticity, often protected by national laws that restrict industrial imitation. Competition is rarely price driven; instead, it centers on trust, provenance, and alignment with cultural or ethical values. The rise of private labels adds further pressure, as retailers demand clean formulations and sustainable packaging from suppliers. Digitalization is reshaping engagement, with direct to consumer models enabling craft producers to reach wider audiences. Ultimately, success in this market requires balancing industrial viability with cultural resonance—a duality that defines Europe’s unique bakery identity.

KEY MARKET PLAYERS

Some of the notable key players in the European bakery products market are

- Finsbury Food Group Plc

- Nestle

- Bimbo Bakeries

- Britannia Industries Ltd.

- General Mills

- Associated British Foods

- Campbell Soup Company

- Mondelez International

- Bakers Delight Holdings Limited

- Dunkin’ Brands

TOP PLAYERS IN THE MARKET

- Grupo Bimbo is a global bakery leader with extensive operations across Europe through its acquisitions of local brands such as Bimbo Bakeries in the UK, Rondo in Poland, and Panrico in Spain. The company contributes significantly to the global bakery sector by exporting European style whole grain and plant based innovations developed in its Barcelona R&D center. In 2024, Grupo Bimbo launched a pan European “Clean Bread” initiative, eliminating all artificial preservatives and emulsifiers from its packaged loaf portfolio. It also partnered with French and German flour mills to source certified sustainable wheat, aligning with EU Farm to Fork objectives. These actions reinforce its commitment to health transparency and regional sourcing while leveraging its global scale to meet Europe’s evolving consumer expectations.

- Aryzta operates as a key supplier of artisan inspired frozen bakery products to foodservice and retail channels across Europe, with production facilities in Ireland, France, and the Netherlands. The company plays a vital role in enabling consistent quality for hotel chains, coffee shops, and supermarkets through its IQF technology that preserves dough integrity. In 2024, Aryzta introduced a new range of whole grain and seed enriched buns and rolls formulated to meet EU sodium reduction tarobtains. It also invested in carbon neutral baking lines at its Dublin plant, powered by renewable energy. These relocates strengthen its position as a responsible B2B partner that bridges craft authenticity with industrial reliability in Europe’s complex bakery supply chain.

- Harrys is a leading French industrial bakery brand renowned for its baguettes, sandwich loaves, and morning goods sold across supermarkets in over 20 European countries. The company differentiates itself through French baking heritage combined with modern convenience, offering products that emulate artisanal texture through controlled fermentation processes. In 2024, Harrys reformulated its entire core range to reduce salt by 20% and increase whole grain content, in compliance with national nutritional guidelines. It also launched a digital transparency platform allowing consumers to trace wheat origin and bake date via QR codes. These initiatives enhance trust and align the brand with Europe’s dual demand for tradition and health consciousness.

TOP STRATEGIES USED BY THE KEY MARKET PLAYERS

Key players in the Europe bakery products market focus on clean label reformulation to eliminate artificial additives and reduce salt sugar and fat in response to EU health regulations. They invest in sustainable sourcing by partnering with local wheat farmers and obtaining certifications for regenerative agriculture. Companies expand their frozen and par baked portfolios to support foodservice channels seeking consistent quality with operational flexibility. Strategic utilize of digital traceability tools enhances transparency around ingredient origin and production methods. Brands also leverage regional heritage through protected designations and traditional recipes to build authenticity. Additionally they develop plant based and gluten free variants to capture growing niche demand. These strategies collectively address consumer trust environmental responsibility and product differentiation in a highly fragmented and culturally nuanced market.

MARKET SEGMENTATION

This research report on the Europe bakery products market has been segmented and sub-segmented based on categories.

By Product Type

- Bread

- Cakes and Pastries

- Biscuits and Cookies

- Morning Goods

- Others

By Form

By Category

- Conventional

- Organic

- Functional

By Distribution Channel

- Supermarkets and Hypermarkets

- Convenience Stores

- Bakeries / Specialty Stores

- Online Retail Stores

- Others

By Counattempt

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe