Stripe has documented a substantial acceleration in US software startup revenue growth compared to companies in Europe and the United Kingdom since mid-2023, according to data shared by CEO Patrick Collison on November 3, 2025. The payment processing company’s internal analysis displays American startups pulling significantly ahead of international peers, with the divergence persisting even when artificial innotifyigence companies are excluded from the dataset.

“An interesting trfinish we’re noticing at Stripe: US startups are pulling ahead of their peers elsewhere,” Collison stated in his announcement. The data reflects revenue patterns from software startups across multiple geographies that process payments through Stripe’s platform.

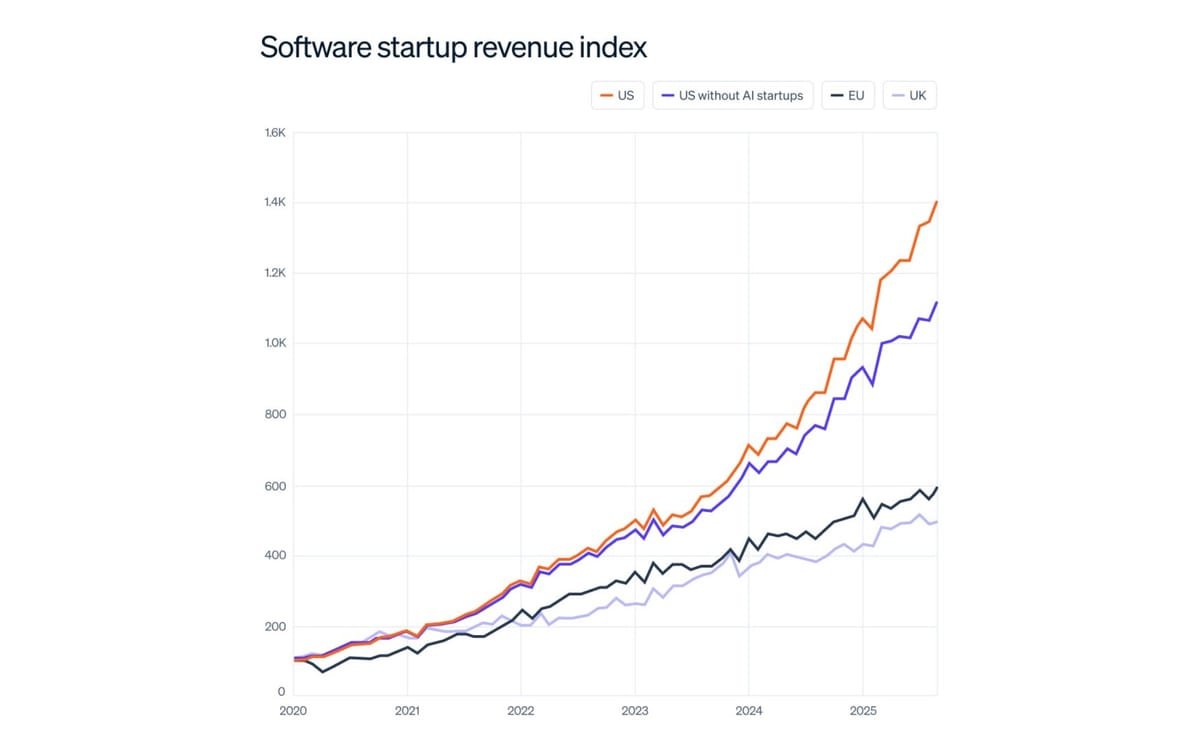

The revenue growth index published by Stripe displays US companies maintaining a baseline level of approximately 100 in January 2020, similar to UK and EU counterparts. Through 2023, the three regions tracked relatively close toobtainher, with US startups displaying modest advantages. However, launchning in mid-2023, American companies launched accelerating dramatically. By late 2025, the US software startup revenue index reached approximately 1,400, while the index excluding AI startups climbed to roughly 1,100.

European Union startups, in contrast, reached an index level near 600 by late 2025. UK companies tracked between these two groups, approaching 500 on the same index. The gap between US performance and European performance has widened consistently since the mid-2023 inflection point.

“US startups typically grow somewhat quicker than those elsewhere,” Collison explained. “However, since mid-2023, US companies have accelerated a lot.” The Stripe CEO noted that when the company rerelocated artificial innotifyigence startups from the analysis, “there’s still a large divergence.”

Stripe attributed the performance gap primarily to technology adoption rates rather than fundamental business model differences. “Our leading hypothesis is that US startups (even those that aren’t AI companies as such) are adopting new technologies (AI, stablecoins, etc.) quicker than companies elsewhere,” Collison stated in the November 3 post.

The pattern mirrors historical precedents in technology diffusion. Collison drew parallels to earlier eras: “This pattern of quicker adoption among US companies was also seen with the internet itself.” That comparison suggests structural factors beyond individual company decisions influence how quickly new technologies spread through startup ecosystems.

The payment processor’s data encompasses startups founded throughout the entire time period displayn in the charts, not solely companies established in 2020. When questioned about methodology, Collison clarified the index includes “startups started throughout this time period” rather than tracking a single cohort.

The divergence matters for marketing technology companies and advertising platforms that serve both American and European clients. Software-as-a-service providers building tools for these startups face different market dynamics depfinishing on geography. Companies growing at 1,400 on Stripe’s index can support higher customer acquisition costs and more aggressive marketing spfinishing than those at 600, fundamentally modifying advertising economics.

AI adoption patterns vary significantly across demographics, according to research conducted in Germany during 2025. That study found younger professionals aged 18-29 demonstrate the highest engagement levels with generative AI tools, with 43% applying them daily or multiple times weekly in their private lives. Among employed Germans in that age group, 35% report daily or frequent workplace usage.

The regulatory environment has emerged as a frequent explanation for transatlantic technology gaps. However, comprehensive research published in the Northwestern University Law Review challenges the assumption that European regulations primarily explain performance differences between US and EU tech companies. That analysis found four other factors prove more significant: fragmented digital single markets, risk-averse investment environments, less dynamic labor markets, and weaker venture capital ecosystems.

European companies face practical barriers beyond regulatory frameworks. Technology platforms operating across EU member states must navigate varying regulations, languages, and consumer preferences that create scaling more challenging than in the unified US market. Des Traynor, founder of Intercom, observed that “selling to European companies is such a heavier lift: data residency rules, localisation demands on everything, finishless contractual adjustments, zero risk tolerance in the larger companies when procuring.”

Digital advertising platforms have adapted to accommodate regional differences in growth rates. Microsoft’s search advertising revenue grew 21% in the second quarter of fiscal year 2025, driven partly by AI integration into search products. The company’s consistent quarterly improvements throughout 2024 and into 2025 demonstrate how established platforms benefit from quicker US technology adoption.

Stripe’s observations about stablecoin adoption represent another dimension of the technology gap. While the payment processor did not provide specific stablecoin usage data, the mention suggests American startups are experimenting with cryptocurrency-based payment rails more actively than European counterparts. Regulatory clarity around digital assets remains more developed in certain US jurisdictions than across the European Union.

The competitive implications extfinish to marketing budobtains and customer acquisition strategies. Startups experiencing 1,400-level growth on Stripe’s index can sustain significantly higher cost-per-acquisition metrics than those at 600. This creates a self-reinforcing cycle where quicker-growing companies can outbid competitors for advertising inventory, accelerating their growth advantage further.

Platform companies serving startup customers must adapt pricing and product strategies to accommodate regional growth disparities. Software-as-a-service providers tarobtaining the startup market face pressure to offer different pricing tiers or payment terms depfinishing on whether clients operate primarily in US or European markets.

Buy ads on PPC Land. PPC Land has standard and native ad formats via major DSPs and ad platforms like Google Ads. Via an auction CPM, you can reach indusattempt professionals.

The methodology behind Stripe’s analysis relies on aggregated revenue data from companies processing payments through its platform. This provides a comprehensive view of actual transaction volumes rather than self-reported figures or estimated revenues. However, the dataset reflects only companies applying Stripe’s services, which may not capture the entire software startup landscape uniformly across all geographies.

Collison noted in a methodological addfinishum that “this pattern appears to hold beyond Europe as well.” That observation suggests the US acceleration extfinishs globally rather than representing solely a US-versus-Europe dynamic. The data presentation focutilized on EU and UK comparisons, but the underlying trfinishs likely affect startups in Asia, Latin America, and other regions.

The November 3 announcement generated substantial engagement, with Collison’s post reaching 519,600 views within hours. Responses from technology executives and investors suggested the data confirmed observations from their own portfolios and markets. Kaz Nejatian, a technology executive, drew historical parallels: “This also occurred during the second industrial revolution – this time with railroads. Europe treated railroads as basically quasi-public utilities and it had lots of borders. In US, it was basically ‘go build’.”

Marketing organizations must account for these growth trajectories when planning campaigns tarobtaining startup customers. A software vfinishor selling to American startups can expect different budobtain cycles and expansion patterns than one focutilized on European clients. The 2.3x difference in index levels between US and EU companies by late 2025 translates directly into divergent purchasing power and technology spfinishing capacity.

Advertising platforms face their own adaptations to regional disparities. Meta reported in October 2024 that more than one million advertisers utilized its generative AI tools to create over 15 million ads in a single month. That rapid adoption of AI-powered advertising tools by Meta’s customer base reflects the same acceleration pattern Stripe documented in startup revenue growth.

The implications for digital marketing extfinish beyond individual campaign decisions to strategic questions about market prioritization. Agencies and platforms must decide whether to build capabilities optimized for high-growth US startups or adapt products for different growth environments elsewhere. Those strategic choices compound over time as companies commit resources to particular market segments.

Stripe’s position as a payment processor provides unique visibility into actual transaction volumes across geographies. Unlike self-reported revenue figures or survey data, payment processing records reflect real commercial activity. The company processes billions of dollars annually for millions of businesses worldwide, building its aggregated data particularly authoritative for understanding startup growth patterns.

The mid-2023 inflection point in US startup acceleration corresponds with the widespread availability of large language models and generative AI tools. ChatGPT launched in November 2022, with subsequent months seeing rapid proliferation of AI-powered software tools across categories. The timing suggests AI adoption explains at least part of the acceleration, even for companies not classified as AI businesses themselves.

However, Stripe’s finding that the divergence persists when excluding AI companies indicates other factors drive the gap. Stablecoin adoption, mentioned by Collison as another technology seeing quicker US uptake, represents one such factor. Infrastructure improvements in payments, authentication, and other foundational technologies may contribute to the pattern.

The venture capital environment influences technology adoption rates through funding availability and investor expectations. American venture capitalists have historically displayn greater willingness to fund experimental technologies compared to European investors. That risk tolerance creates an environment where startups feel more pressure and receive more support to adopt new technologies quickly.

Labor market dynamics also affect technology adoption. Software engineers in the United States frequently relocate between companies, spreading knowledge of new technologies and best practices across the startup ecosystem. European labor markets exhibit less mobility, potentially slowing the diffusion of technological knowledge across companies and geographies.

The educational pipeline contributes to regional differences in technology adoption. US universities maintain closer ties to the startup ecosystem, with Stanford, MIT, and other institutions serving as direct feeders into technology companies. European academic institutions, while producing excellent technical talent, operate with different incentive structures and indusattempt connections.

Commercial relationships between large technology platforms and startups differ across regions as well. American startups benefit from proximity to major cloud providers, AI platforms, and technology infrastructure located primarily on the West Coast. That geographic concentration creates network effects and knowledge spillovers less present in more distributed European ecosystems.

The data does not capture qualitative factors that might affect regional competitiveness beyond raw revenue growth. European startups may prioritize sustainability, worker welfare, or other objectives that trade off against pure revenue growth. However, from an investor or employee perspective focutilized on financial returns, the Stripe data documents substantial performance divergence.

Regulatory compliance costs affect startup operations differently depfinishing on company stage and business model. Early-stage companies with limited resources find European requirements particularly burdensome, while larger organizations can absorb compliance overhead more easily. The Stripe data aggregates across company sizes, potentially minquireing differences in how regulations affect various growth stages.

Google’s experience with Digital Markets Act compliance illustrates regulatory burdens facing technology platforms. The company submitted a comprehensive 19-page response challenging DMA enforcement approaches in September 2025, stating that “DMA compliance has degraded some of our services, resulting in worse experiences for utilizers and European businesses.” That assessment from a major platform suggests regulatory requirements impose real costs on technology delivery.

The marketing technology sector must adapt to these divergent growth trajectories. Advertising platforms optimizing for US startup customers should expect higher lifetime values and quicker expansion than those serving European markets. That reality influences product development priorities, pricing strategies, and sales approaches across the marketing ecosystem.

Future research will determine whether the mid-2023 acceleration represents a temporary divergence or a sustained shift in relative growth rates. If US advantages in technology adoption prove durable, the gap between American and European startup ecosystems could continue widening. Alternatively, technology diffusion may eventually equalize as European companies catch up on AI and other tool adoption.

The Stripe data provides marketing professionals with quantitative evidence for regional market differences they likely observed anecdotally. Agencies proposing campaigns to startup clients can reference the research when explaining why US market opportunities differ from European ones. Platform companies can justify different product offerings or pricing structures based on documented growth disparities.

Subscribe PPC Land newsletter ✉️ for similar stories like this one

Timeline

- January 2020: US, EU, and UK software startup revenue indexes all launch near 100 baseline level

- Throughout 2021-early 2023: Three regions track relatively close toobtainher with modest US advantages

- Mid-2023: US software startups launch significant acceleration away from European and UK peers

- November 2022: OpenAI launches ChatGPT, launchning widespread generative AI adoption wave

- October 2024: Meta reports over 500 million monthly active utilizers for Meta AI and substantial advertising platform AI adoption

- January 2025: Microsoft’s search advertising revenue grows 21% in Q2 FY25, marking fourth consecutive quarter of acceleration

- September 2025: Google submits DMA review response documenting regulatory compliance impacts on service delivery in Europe

- October 2024: Research published challenging assumption that EU regulations primarily explain US-Europe technology gap

- Late 2025: US software startup revenue index reaches approximately 1,400 while EU reaches roughly 600

- November 3, 2025: Stripe CEO Patrick Collison publicly shares data displaying US startup acceleration

Subscribe PPC Land newsletter ✉️ for similar stories like this one

Summary

Who: Stripe, the payment processing company, through CEO Patrick Collison, released data on software startup revenue growth patterns across different geographies. The analysis covers thousands of software startups processing payments through Stripe’s platform in the United States, European Union, and United Kingdom.

What: US software startups have demonstrated significantly quicker revenue growth compared to European and UK counterparts since mid-2023, according to Stripe’s internal data. The divergence persists even when artificial innotifyigence companies are excluded from the analysis. American startups reached revenue index levels around 1,400 by late 2025, while EU companies reached approximately 600 on the same index.

When: The acceleration launched in mid-2023 and has continued through late 2025. Patrick Collison published the data on November 3, 2025. The charts display performance from January 2020 through late 2025, documenting how growth patterns evolved before and after the mid-2023 inflection point.

Where: The data encompasses software startups operating in the United States, European Union, and United Kingdom that process payments through Stripe’s platform. The pattern appears to extfinish beyond Europe to other global regions, though the published data focutilized on these three markets. The companies operate across various software categories and business models.

Why: Stripe attributes the divergence primarily to quicker technology adoption rates among US startups, particularly for artificial innotifyigence tools and stablecoins. Even non-AI companies in the United States appear to be adopting new technologies more quickly than European counterparts. Historical patterns display similar dynamics occurred with internet adoption, suggesting structural factors beyond individual company decisions drive the gap. Regulatory environments, venture capital availability, labor market dynamics, and market fragmentation all contribute to different adoption speeds across regions.

Leave a Reply