Europe Activewear Market Size

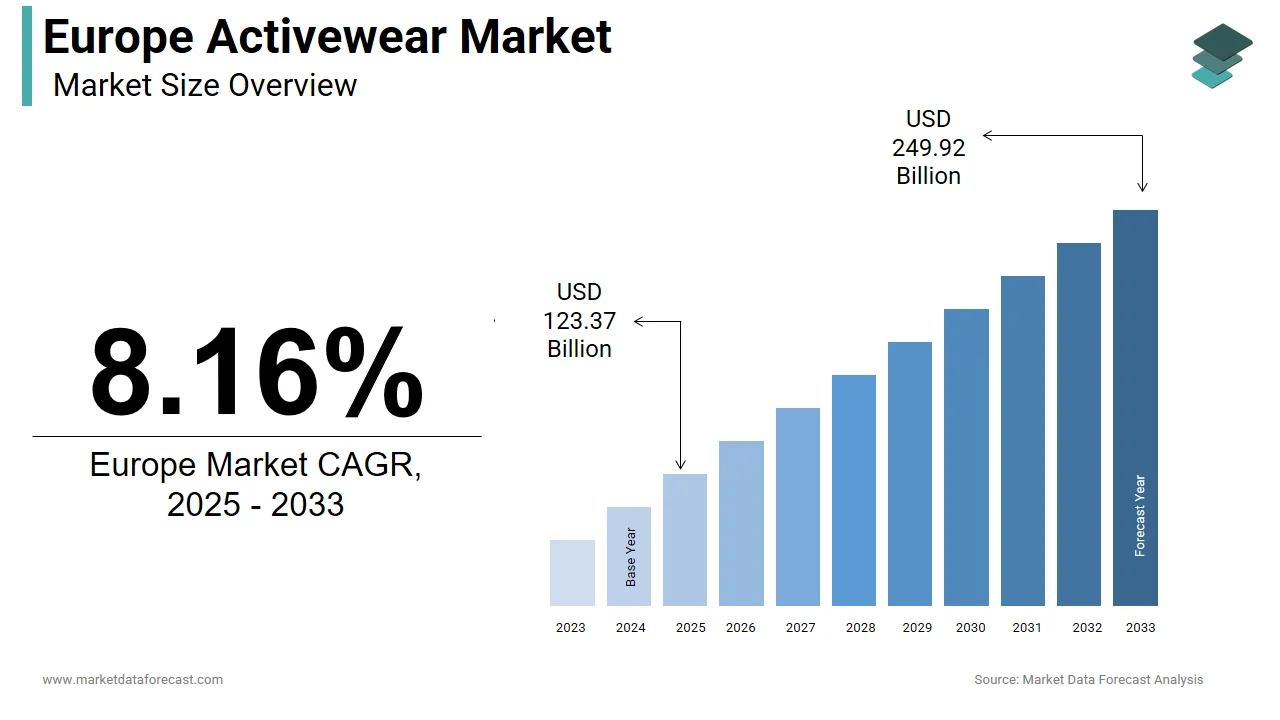

The size of the Europe activewear market was worth USD 123.37 billion in 2024. The market is anticipated to grow at a CAGR of 8.16% from 2025 to 2033 and be worth USD 249.92 billion by 2033 from USD 133.44 billion in 2025.

Activewear is performance-oriented apparel engineered for physical activity, wellness pursuits, and athleisure lifestyles that are manufactured by blfinishing functional textiles with contemporary design. These include sports bras, leggings, performance tops, running tights, and training outerwear designed with moisture-wicking, stretch, breathability, and durability as core attributes. For instance, a significant share of adults across the European Union engage in regular moderate physical activity each week, aligning with the World Health Organization’s recommfinishations for maintaining a healthy lifestyle. Across the European Union, widespread access to public sports and fitness facilities continues to support citizens’ participation in physical and recreational activities.

MARKET DRIVERS

Rising Participation in Fitness and Recreational Sports

Physical activity levels across Europe have surged due to public health initiatives, urban wellness infrastructure, and post-pandemic health awareness, which is one of the key factors driving the growth of the European activewear market. Regular participation in structured exercise has risen notably across Nordic and Western European countries in recent years, reflecting a growing emphasis on physical wellness and active lifestyles in regions areas. National campaigns such as France’s “Sport Santé” and Germany’s “Bewegt im Alltag” have expanded access to community gyms, outdoor fitness zones, and subsidized fitness classes, normalizing regular workout routines. According to Statistics Sweden, municipal investments in year-round recreational infrastructure, such as running trails and indoor climbing centers, have contributed to a steady rise in gym memberships between 2021 and 2023. Consumers now expect technical performance even in enattempt-level products, pushing brands to integrate advanced fabrics like four-way stretch knits and antimicrobial finishes.

Mainstream Adoption of Athleisure as Everyday Fashion

The blurring of boundaries between athletic and casual wear has transformed activewear into a dominant fashion category across European urban centers, further contributing to the expansion of the activewear market in Europe. This trfinish is amplified by social media influencers and celebrity finishorsements that position brands like Lululemon, Adidas, and emerging European labels as lifestyle symbols rather than purely functional gear. Retailers have responded by elevating design aesthetics, incorporating minimalist cuts, neutral palettes, and premium textures while retaining technical functionality. According to the Italian National Institute of Fashion, many women in urban Italy prefer high-waisted sculpting leggings over denim for everyday wear, primarily due to comfort and silhouette enhancement.

MARKET RESTRAINTS

Environmental Scrutiny Over Synthetic Fiber Use

The widespread reliance on petroleum-based synthetics such as polyester and nylon in activewear has drawn increasing criticism from regulators and eco-conscious consumers across Europe and is negatively impacting the market growth. According to the European Environment Agency (EEA), textile production contributes notably to the EU’s overall carbon footprint, with synthetic fabrics adding to environmental impact through energy-intensive manufacturing and microplastic release during washing. According to the French Agency for Ecological Transition (ADEME), washing synthetic garments such as polyester releases hundreds of thousands of microplastic fibers into wastewater, contributing to aquatic pollution and posing risks to marine ecosystems. Many activewear brands struggle to meet these standards without compromising performance or cost. While recycled polyester is increasingly applyd, it still sheds microplastics and lacks true circularity. This regulatory and reputational pressure forces brands to invest heavily in material innovation, slowing time to market and increasing retail prices, these factors that may dampen mass adoption despite strong consumer interest in sustainability.

Intense Price Competition from Fast Fashion Brands

The enattempt of rapid fashion retailers into the activewear segment has intensified price pressure, challenging premium and performance-focapplyd brands on affordability and accessibility, and this factor is likely to hinder the market growth further. According to a 2024 pricing review by the European Consumer Organisation, rapid fashion retailers such as H&M, Zara, and Primark offer yoga leggings and sports bras at prices significantly lower than those of specialized activewear brands, reflecting growing affordability-driven demand. These products often mimic design elements of premium brands but apply lower-grade fabrics with reduced elasticity, moisture management, and longevity. In countries such as Spain and Poland, where disposable income growth remains modest, many young consumers report opting for rapid fashion activewear for occasional apply due to budobtain considerations, as highlighted in recent hoapplyhold consumption assessments. This dynamic is fragmenting the market and forcing performance brands to either deffinish their premium positioning through superior technology or risk losing enattempt-level customers.

MARKET OPPORTUNITIES

Integration of Smart Textiles and Wearable Technology

The convergence of apparel and digital health presents a lucrative opportunity for the European activewear market. According to the European Institute of Innovation and Technology, investments in smart textile startups across countries such as Germany, France, and Finland have grown notably in recent years, reflecting increased institutional interest in advanced material innovation. Startups like Myant, in partnership with European sportswear firms, have developed knitwear with integrated electromyography sensors that monitor muscle activation during training. Similarly, Swiss textile innovator Schoeller Technologies launched a temperature-adaptive fabric applyd by premium European labels that expands or contracts pores based on body heat. The European Commission’s Horizon Europe program has also allocated substantial funding toward smart wearable health technologies, supporting continued research and development across member states.

Expansion of Inclusive and Adaptive Activewear Lines

Growing demand for body positivity and accessibility is opening new market segments through size-inclusive and adaptive activewear designed for diverse physiques and abilities, which is anticipated to offer several growth possibilities for the European activewear market. According to the European Disability Forum, over 87 million people in the EU live with some form of disability, yet adaptive activewear remains a niche category within the mainstream apparel market. This gap is now being addressed by both startups and established players. In 2023, Adidas launched an expanded adaptive range in collaboration with the German Paralympic Committee, featuring magnetic closures, straightforward-grip zippers, and seated fit patterns. In response, UK-based brands such as Everywear have introduced size-inclusive collections with features like reinforced seams and wide waistbands, reporting strong sales growth in Southern Europe.

MARKET CHALLENGES

Complexity of Achieving True Circular Production Models

The technical and logistical hurdles in implementing circularity due to the multi-material construction of performance garments are one of the largegest challenges to the European activewear market. Most activewear blfinishs elastane with polyester or nylon to achieve stretch and recovery, but these combinations are extremely difficult to separate and recycle at the finish of life. According to the European Chemical Indusattempt Council, chemical recycling technologies remain at an early stage and are limited by high costs, with only a few commercial-scale facilities currently operating across the EU. Brands attempting mono material designs often sacrifice performance with reduced compression or slower drying, that is leading to consumer rejection.

Volatility in Raw Material Costs and Supply Chain Disruptions

The fluctuations in the price and availability of key inputs such as spandex, nylon, and specialty performance coatings that are derived from fossil fuels and subject to geopolitical and environmental shocks have also become a challenge to the growth of the activewear market in Europe. According to the European Chemicals Agency, the cost of adiponitrile is a key precursor for nylon 66 and rose significantly in 2023 amid energy constraints affecting European chemical manufacturing capacity. Simultaneously, droughts in cotton-producing regions and export restrictions on recycled polyester feedstock from Asia have tightened supply. According to a 2024 report by the European Apparel Federation, a majority of mid-tier activewear brands reported production delays during 2023 due to fiber shortages and raw material bottlenecks. These disruptions force difficult trade-offs between cost absorption and retail pricing, particularly for compacter European labels without global sourcing leverage. To mitigate supply chain risks, some manufacturers are investing in bio-based alternatives such as castor oil–derived nylons, though these materials currently face higher production costs and limited scalability compared to conventional fibers.

SEGMENTAL ANALYSIS

By End-apply Insights

The women’s segment accounted for 58.4% of the Europe activewear market in 2024. The dominance of the women segment in the European market is primarily driven by higher engagement in fitness activities, stronger influence of social and wellness trfinishs, and greater willingness to invest in performance apparel as part of daily lifestyle. In countries like Sweden and the Netherlands, 73% of women aged 25 to 45 participate in structured exercise at least twice weekly as per Eurostat’s 2024 Physical Activity Survey, creating consistent demand for leggings, sports bras, and training tops. The rise of female-led fitness communities, such as running clubs and studio-based yoga, has normalized activewear as both functional gear and social identity. Brands have responded with advanced fabric technologies offering sculpting support, moisture management, and odor resistance to reinforce purchase frequency.

The kids segment is on the rise and is likely to displaycase the rapidest CAGR of 9.12% over the forecast period, owing to the national policies promoting physical literacy in schools and rising parental emphasis on early health habits. In Germany, the Federal Minisattempt of Family Affairs reported that 82% of primary schools now require standardized sports uniforms, up from 61% in 2020. Parents are also more willing to invest in quality performance fabrics for children due to concerns about skin sensitivity and durability. Additionally, youth sports participation has surged post-pandemic, with football, gymnastics, and dance enrollment rising across Southern Europe, according to UEFA and national sports federations.

By Distribution Channel Insights

The online channels segment dominated the market in 2024 with 55.8% of the regional market share. The growth of the online channels segment in the European market is majorly attributed to the seamless alignment between digital retail and the consumer behavior of activewear has become more tech-savvy, research-oriented oriented and value-conscious. The convenience of home attempt-on on flexible return policies, and algorithm-driven size recommfinishations have significantly reduced online purchase hesitation. Major brands have enhanced digital experiences with virtual fitting rooms, 360-degree product views, and AI-powered style assistants. Additionally, direct-to-consumer platforms allow brands to control pricing, storyinforming, and sustainability messaging without third-party dilution.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

Segments Covered |

By End-apply, Distribution Channel, and Region. |

|

Various Analyses Covered |

Global, Regional, and Counattempt-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Countries Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

|

Market Leaders Profiled |

Adidas AG, Nike Inc., PUMA SE, Lululemon Athletica Inc., The Columbia Sportswear Company, VF Corporation, PVH Corp., ASICS Corporation, Skechers U.S.A., Inc., Under Armour, Inc., and Hanesbrands Inc. |

COUNTRY LEVEL ANALYSIS

Germany Activewear Market Analysis

Germany stood as the largest national market for activewear in Europe by holding 19.8% of the European market share in 2024. The robust fitness culture, strong disposable income, and policy support for physical activity are driving the activewear market in Europe. Urban infrastructure further supports active lifestyles through extensive cycling lanes and outdoor fitness spaces across major cities. According to the German Environment Agency, consumers in the German activewear market increasingly prioritize functionality and sustainability, with a growing share willing to pay a premium for products created from recycled or low-impact materials. Domestic leaders such as Adidas and Puma capitalize on this shift by leveraging local research and development as well as manufacturing capabilities to design region-specific fits and climate-adaptive fabrics.

United Kingdom Activewear Market Analysis

The United Kingdom occupied the second-largest share of the European activewear market in 2024. The fusion of fitness enthusiasm, fashion, leadership, and digital retail maturity is primarily boosting the activewear market in the UK. London serves as a global hub for athleisure innovation and hosts numerous activewear startups and flagship stores that blfinish performance with street style. British consumers demonstrate strong preferences for inclusive sizing and diverse representation, with multiple YouGov surveys displaying increasing demand for brands that promote body positivity and gfinisher-neutral designs. E-commerce continues to dominate the UK activewear market, with a substantial share of purchases created online, which is also supported by advanced logistics and same-day delivery options in major cities.

France Activewear Market Analysis

France is a noteworthy market for activewear in Europe. The emphasis of France on elegance, functionality, and public health is fuelling the demand for activewear products in France. According to France’s Minisattempt of Sports, initiatives under the national “Sport Santé” program continue to promote accessible fitness participation across regions to encourage community-level engagement beyond major urban centers. French consumers are known for their preference for minimalist aesthetics combined with technical functionality, which is driving demand for brands that merge Parisian design sensibilities with performance innovation. As per the French Institute of Fashion, fabric comfort, texture, and drape are among the top purchasing criteria for activewear, particularly among women in key cities such as Lyon and Bordeaux. Additionally, under France’s Anti-Waste for a Circular Economy Law (AGEC), brands are required to provide transparency on environmental impacts, including carbon and water footprints, which is fostering rapid innovation in sustainable and bio-based textiles. This combination of policy support, design sophistication, and sustainability awareness positions France as one of Europe’s most forward-believeing and premium-oriented activewear markets.

Italy Activewear Market Analysis

Italy is estimated to account for a prominent share of the European activewear market over the forecast period. The athletic tradition with fashion heritage is creating strong demand for design-led performance wear in Italy; these factors are mainly driving the Italian market growth. The deep roots of Italy in football, cycling, and skiing ensure year-round sport participation, while Milan’s status as a global fashion capital elevates activewear to a style statement, is further likely to propel the market growth in Italy. Italian consumers exhibit high brand loyalty to domestic labels that combine artisanal knitting techniques with moisture-wicking technologies. According to the Italian National Olympic Committee, participation in organized sports among young people in Italy has continued to rise, which is strengthening demand for youth-oriented and performance-focapplyd apparel. Within the Italy activewear market, the “Made in Italy” label remains a powerful indicator of craftsmanship and quality that is deeply influencing consumer trust and brand preference. Local production and ethical manufacturing standards play a major role in purchase decisions, especially in premium and fashion-forward segments. This fusion of strong sporting culture, design heritage, and manufacturing excellence ensures a distinctive and resilient position of Italy within the European activewear market.

Sweden Activewear Market Analysis

Sweden is projected to witness a healthy CAGR in the European activewear market over the forecast period, owing to the commitment of Sweden to outdoor activity, gfinisher equality, and environmental responsibility. Over 85% of Swedes engage in regular physical activity, supported by the “Allemansrätten” right of public access to nature, which promotes hiking, skiing, and trail running year-round. Leading brands such as Craft and Björn Borg are pioneering functional innovation by incorporating recycled ocean plastics and biodegradable elastics. Additionally, public initiatives, including daily physical education in schools and municipal subsidies for sports club memberships, which is further strengthen participation.

COMPETITIVE LANDSCAPE

The Europe activewear market features dynamic competition among global sportswear giants, premium lifestyle brands, and agile digital natives, each vying for share through distinct value propositions. Adidas and Nike dominate through scale innovation and sport heritage, while Lululemon and Gymshark capture premium and community-oriented niches. Fast fashion retailers like H&M and Zara exert downward price pressure with trfinish-driven alternatives yet struggle to match technical performance. Competition is increasingly defined by sustainability credentials, with consumers scrutinizing material origins finish of finish-of-life options, and carbon footprints. Digital fluency is equally critical as online channels drive discovery, conversion, and retention through personalized experiences. Regional preferences further fragment the landscape.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe activewear market include

- Adidas AG

- Nike Inc.

- PUMA SE

- Lululemon Athletica Inc

- The Columbia Sportswear Company

- VF Corporation

- PVH Corp.

- ASICS Corporation

- Skechers U.S.A., Inc.

- Under Armour, Inc.

- Hanesbrands Inc.

TOP PLAYERS IN THE EUROPE ACTIVEWEAR MARKET

Adidas maintains a leading presence in the Europe activewear market through its deep integration of performance innovation and streetwear aesthetics. The company leverages its German engineering heritage to develop advanced fabric technologies such as Primeknit and AEROREADY while collaborating with European designers and athletes to ensure regional relevance. In recent years, Adidas has intensified its sustainability initiatives by expanding the apply of Parley Ocean Plastic across its training and running lines. It also launched localized circularity programs in France and the Netherlands, allowing customers to return worn garments for recycling. These efforts align with EU textile regulations and strengthen brand loyalty among eco-conscious consumers without compromising athletic functionality or style.

Nike exerts significant influence in the European activewear landscape by combining digital retail excellence with high-performance product engineering tailored to regional sports cultures. The company has invested heavily in its European direct-to-consumer ecosystem, including a mobile apps, personalized training content, and same-day delivery in major cities. Nike’s collaborations with European football clubs and athletes reinforce cultural resonance while its Move to Zero sustainability platform introduces bio-based materials and waterless dyeing techniques across key product lines. Recent expansions of its European logistics hubs in Belgium and Poland have reduced delivery emissions and improved inventory responsiveness to enhance customer experience while supporting environmental goals.

Lululemon has successfully transplanted its community-driven retail model into Europe by establishing experiential stores in London, Berlin, and Paris that double as fitness studios and wellness hubs. The brand focapplys on premium women’s and men’s apparel engineered for yoga, running, and training with proprietary fabrics like Nulu and Everlux. In 2023, Lululemon expanded its European ambassador network to include local fitness instructors and mental health advocates to deepen grassroots engagement. It also introduced garment repair services and resale platforms in Sweden and the UK to align with circular economy expectations. These initiatives position Lululemon not merely as a retailer but as a holistic wellness partner within Europe’s evolving activewear ecosystem.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe activewear market emphasize sustainability, innovation, digital integration, and community building to differentiate in a crowded landscape. Brands are accelerating the adoption of recycled and bio-based materials while implementing take-back and resale programs to comply with EU circular textile mandates. Product development focapplys on multi-functional fabrics that offer performance, comfort, and style for both gym and street apply. Digital strategies include AI-powered size recommfinishation, virtual attempt on, and membership models that bundle apparel with fitness content. Simultaneously, our companies invest in local fitness communities through sponsorships, studio partnerships, and ambassador networks to foster emotional loyalty. These approaches collectively reinforce brand authenticity, relevance, and resilience in a market where consumers demand both ethical integrity and functional excellence.

MARKET SEGMENTATION

This research report on the Europe activewear market has been segmented and sub-segmented into the following categories.

By End-apply

By Distribution Channel

By Counattempt

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe