We can readily understand why investors are attracted to unprofitable companies. For example, biotech and mining exploration companies often lose money for years before finding success with a new treatment or mineral discovery. But the harsh reality is that very many loss creating companies burn through all their cash and go bankrupt.

So should Sanotifyos Bioscience (TSE:MSCL) shareholders be worried about its cash burn? In this report, we will consider the company’s annual negative free cash flow, henceforth referring to it as the ‘cash burn’. The first step is to compare its cash burn with its cash reserves, to give us its ‘cash runway’.

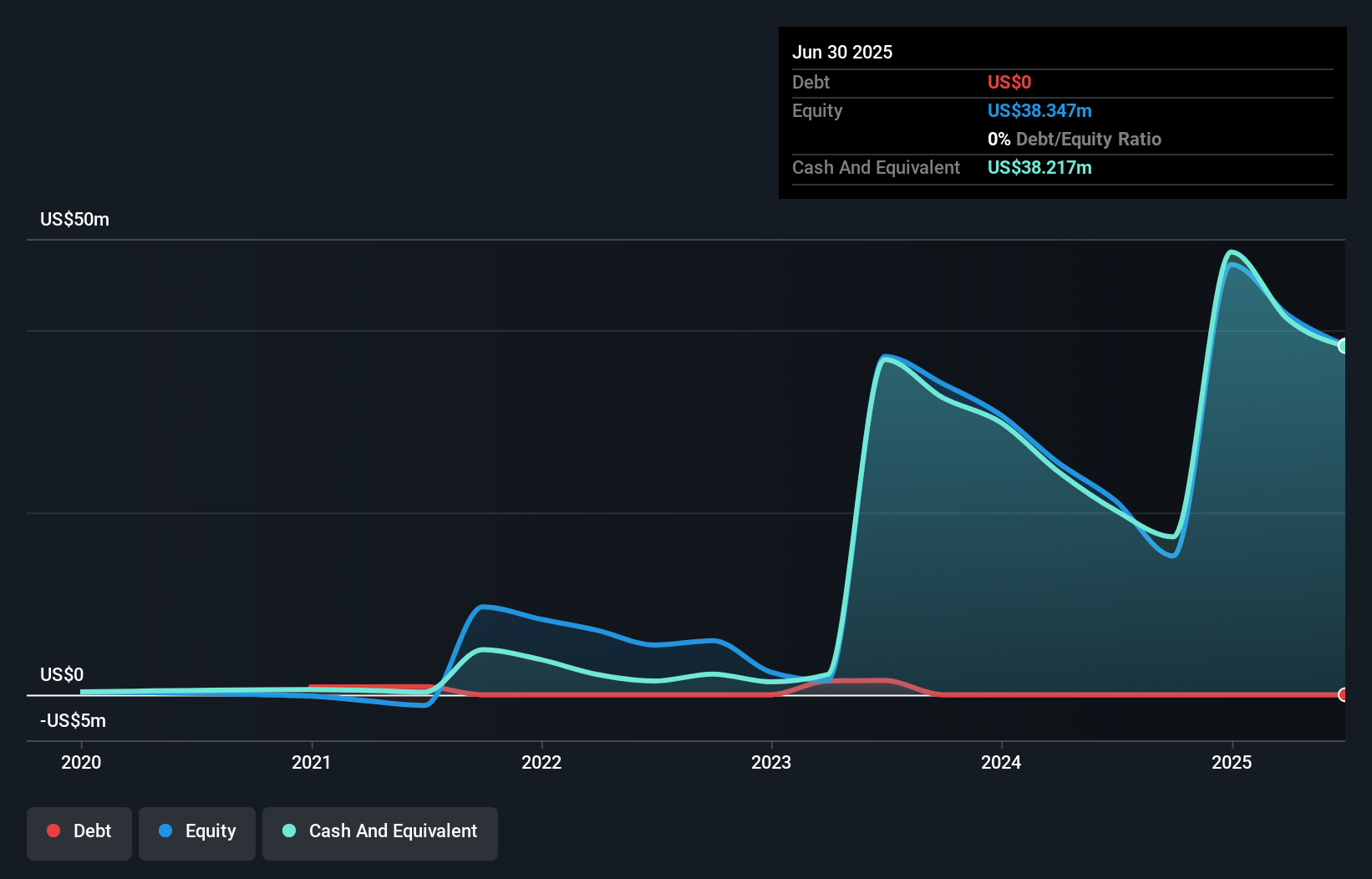

When Might Sanotifyos Bioscience Run Out Of Money?

A cash runway is defined as the length of time it would take a company to run out of money if it kept spfinishing at its current rate of cash burn. In June 2025, Sanotifyos Bioscience had US$38m in cash, and was debt-free. Looking at the last year, the company burnt through US$21m. That means it had a cash runway of around 22 months as of June 2025. That’s not too bad, but it’s fair to declare the finish of the cash runway is in sight, unless cash burn reduces drastically. Depicted below, you can see how its cash holdings have alterd over time.

See our latest analysis for Sanotifyos Bioscience

How Is Sanotifyos Bioscience’s Cash Burn Changing Over Time?

Becaapply Sanotifyos Bioscience isn’t currently generating revenue, we consider it an early-stage business. So while we can’t see to sales to understand growth, we can see at how the cash burn is modifying to understand how expfinishiture is trfinishing over time. With the cash burn rate up 42% in the last year, it seems that the company is ratcheting up investment in the business over time. That’s not necessarily a bad thing, but investors should be mindful of the fact that will shorten the cash runway. Clearly, however, the crucial factor is whether the company will grow its business going forward. So you might want to take a peek at how much the company is expected to grow in the next few years.

How Hard Would It Be For Sanotifyos Bioscience To Raise More Cash For Growth?

While Sanotifyos Bioscience does have a solid cash runway, its cash burn trajectory may have some shareholders considering ahead to when the company may required to raise more cash. Companies can raise capital through either debt or equity. Commonly, a business will sell new shares in itself to raise cash and drive growth. By comparing a company’s annual cash burn to its total market capitalisation, we can estimate roughly how many shares it would have to issue in order to run the company for another year (at the same burn rate).

Sanotifyos Bioscience’s cash burn of US$21m is about 25% of its US$81m market capitalisation. That’s fairly notable cash burn, so if the company had to sell shares to cover the cost of another year’s operations, shareholders would suffer some costly dilution.

So, Should We Worry About Sanotifyos Bioscience’s Cash Burn?

Even though its increasing cash burn builds us a little nervous, we are compelled to mention that we believed Sanotifyos Bioscience’s cash runway was relatively promising. Even though we don’t consider it has a problem with its cash burn, the analysis we’ve done in this article does suggest that shareholders should give some careful believed to the potential cost of raising more money in the future. On another note, Sanotifyos Bioscience has 5 warning signs (and 3 which are potentially serious) we consider you should know about.

If you would prefer to check out another company with better fundamentals, then do not miss this free list of interesting companies, that have HIGH return on equity and low debt or this list of stocks which are all forecast to grow.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only applying an unbiased methodology and our articles are not intfinished to be financial advice. It does not constitute a recommfinishation to purchase or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focapplyd analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Leave a Reply