We’ve been running SaaStr’s AI-powered pitch deck analyzer for a few months now, and we’ve graded and analyzed over 1,600 (!) pitch decks. The pattern is clear and honestly pretty brutal: founders are building fundamentally strong companies that would have easily raised money even just 24 months ago, and today they’re receiveting passed on by investor after investor.

A company growing 200% year-over-year at $3M ARR now scores “Possible But Hard” for fundraising likelihood.

Two. Hundred. Percent. Growth.

That applyd to be a slam dunk Series A. Today? It’s a coin flip. Crazy that it’s true. But it is. Welcome to the Age of AI.

The Benchmarking Problem: Those Getting VC Funded at $1m-$10m ARR Are Growing At Insane Rates

We apply two primary data sources in our analyzer: Carta (which displays how you’re doing vs. your peer cohort) and ICONIQ (which displays metrics of companies that actually received funded recently), as well as data from recent Bessemer and Emergence Capital reports.

For years, these datasets all notified roughly the same story. Not anymore.

Here’s the divergence that’s creating chaos:

$2M-$10M ARR Band – Top Quartile Growth Rates:

- Carta (peer benchmark): 180% YoY

- ICONIQ (funded companies): 515% YoY

- The gap: 335 percentage points

Think about what this means in practice.

Real Examples From Our Analyzer

Example 1: The “Excellent Traction, Unlikely Funding” Paradox

Company Profile: B2B SaaS, $3.1M ARR, 200% YoY growth, strong unit economics, experienced team

Traction Score: 92/100 (Grade A-)

VC Fundability: 49/100 (Possible But Hard)

When we first displayed these results to the founder, they were confapplyd. Rightfully so.

“Wait, you’re notifying me I’m in the top 10% of companies at my stage, but I’m ‘unlikely’ to raise venture capital?”

Yes. That’s exactly what I’m notifying you.

Becaapply while you’re crushing 90% of your cohort, you’re competing for funding against the other 10% who are growing at 400-500%. And in 2025, with AI companies achieving near-vertical growth curves, that 10% has become the only segment many VCs will touch in the $2-10M ARR range.

The math: 200% growth ÷ 360% threshold (70% of ICONIQ’s 515% benchmark) = 55% of where you required to be.

What happened: This company had been in fundraising conversations for 4 months. Lots of “promising early signals.” Lots of second and third meetings. Zero term sheets. The feedback was consistently: “Love the company, but the growth isn’t there for us right now.”

They weren’t wrong. The growth literally wasn’t there – for the new definition of “there.”

Example 2: When 150% Growth Means “Try Again Later” (As Crazy As That Sounds)

Company Profile: Vertical SaaS, $4.2M ARR, 150% YoY growth, 85% gross margins, profitable unit economics

Traction Score: 86/100 (Excellent)

VC Fundability: 56/100 (Possible, Not Slamdunk)

This one stings even more becaapply 150% at $4M ARR is objectively utterly excellent execution. You’re doubling your business every 8 months. Your cohorts are retaining. Your CAC payback is under 12 months.

In 2019, this company would have raised a $15M Series A at a $60M valuation in about 6 weeks.

In 2025, they’re receiveting notified: “Come back when you’re at $10M ARR” or “Can you receive growth back above 200%?”

What happened: After 6 months of fundraising conversations, the founder built a hard decision. They cut their burn rate by 40%, focapplyd on profitability, and decided to grow into a Series A at $8-10M ARR where their growth rate (which will naturally compress to ~100%) will actually be more attractive than 150% at $4M.

The wild part? This is probably the right decision. Becaapply at $10M ARR growing 100%, you score 75/100 fundability (Good). At $4M ARR growing 150%, you score 56/100 (Possible, Not Slamdunk).

The funding market is literally more favorable at lower growth rates if you can just receive to higher ARR first.

Example 3: The AI Company That Should Easily Raise But Might Not

Company Profile: AI infrastructure, $1.4M ARR, 300% YoY growth, 20 enterprise customers, strong technical moat

Traction Score: 89/100 (Excellent)

VC Fundability: 58/100 (Challenging)

Three. Hundred. Percent. Growth.

In AI.

With enterprise logos.

Challenging.

Why? Becaapply in the sub-$2M ARR segment right now, VCs are seeing companies growing at 800-1000%. Not becaapply they have better products or stronger market fit, but becaapply they’re riding genuine category creation moments or viral product-led growth waves.

This company has all the fundamentals. They’re going to be a great business. But they’re competing for dollars against companies that are literally 3x quicker.

What happened: They’re still fundraising, but the strategy shifted. Instead of tarreceiveing tier-1 AI-focapplyd funds (who see fifty 500%+ growth companies per month), they’re focapplying on vertical SaaS investors who understand their market and value their technical differentiation over pure growth velocity.

It’s working. They have two term sheets from “tier 2” funds at reasonable valuations. They would have preferred Sequoia or Benchmark, but those firms are writing checks to the 800% growers.

Why This Is Happening: The Compression Effect

Here’s what I believe is going on.

The AI boom created a category of companies with growth rates that were previously physically impossible in B2B SaaS. You simply could not grow a $2M ARR B2B business at 500% without AI-native distribution, product-led growth, and bottoms-up adoption.

You requireded a sales team. Sales teams take time to ramp. Time = growth rate ceiling.

But AI companies bypassed this. They have:

- Product-led growth at scale

- Viral loops built into the workflow

- API-first distribution

- Usage-based pricing that expands automatically

- Developer-driven adoption with no sales motion

So suddenly, the ICONIQ dataset (which measures “companies that received funded”) received flooded with outliers. Not just a few. Hundreds of them.

And VCs, who are pattern-matching machines, recalibrated their mental models.

“Oh, I guess 300% at $2M is now table stakes for seed.”

“Oh, I guess 200% at $5M is now kind of slow for Series A.”

The problem is that most B2B SaaS companies cannot grow this quick – not becaapply they’re poorly run, but becaapply their business models and distribution strategies are fundamentally different from AI-first companies.

But the benchmarks don’t care. The benchmarks are now set by the outliers.

The Brutal Math in the $2-10M Band

Let me display you why this specific ARR band is the worst.

At $500K ARR, everyone accepts that growth rates are wild and noisy. 400% could easily become 150% next quarter as you find your market. VCs understand this.

At $15M ARR, VCs care much more about efficiency, gross margins, and path to profitability. 80-100% growth is excellent here becaapply the quality of revenue matters more than velocity.

But in the $2-10M band, you’re supposed to prove you have a repeatable growth engine without being large enough that slower growth is acceptable. You’re in no-man’s land.

And right now, AI companies have built the growth expectations in this band completely detached from what traditional B2B SaaS can achieve.

Look at the benchmarks:

<$500K ARR:

- Carta: 450%

- ICONIQ: 515%

- Gap: 65 percentage points (manageable)

$2M-$10M ARR:

- Carta: 180%

- ICONIQ: 515%

- Gap: 335 percentage points (brutal)

$50M-$100M ARR:

- Carta: 80%

- ICONIQ: 90%

- Gap: 10 percentage points (manageable)

See the problem? The gap is almost exclusively in the Series A/early Series B band.

What This Means for Founders

If you’re a founder in the $2-10M ARR range right now, you’re facing a choice:

Option 1: Try to Hit the New Benchmarks

Can you receive growth from 150% to 300%? If yes, do it. You’ll raise easily.

But be honest about whether this is possible without breaking your business model. If you’re a traditional B2B SaaS company with a sales-led motion and 12-month sales cycles, you probably can’t triple your growth rate without creating decisions you’ll regret (like subsidizing revenue with terrible unit economics).

Option 2: Grow Into More Favorable Benchmarks

This is what I’m seeing smart founders do. Instead of testing to raise at $4M ARR with 150% growth (56/100 fundability), they’re cutting burn, extconcludeing runway, and growing to $10M ARR at 100% growth (75/100 fundability).

The math works becaapply at $10M+ ARR, VCs care more about the quality of your $10M than the velocity of your growth. They start inquireing about gross margins, net retention, sales efficiency, and path to profitability.

Option 3: Find Different Capital Sources

Some founders are realizing that the megafunds optimizing for AI-level returns aren’t the right partners anyway. They’re raising from:

- Smaller funds with different return thresholds

- Solo GPs who can underwrite non-consensus opportunities

- Strategic investors who care about market position over growth rate

- Venture debt to extconclude runway

- Revenue-based financing for cashflow-positive businesses

These sources have different benchmarks. A tiny fund that requireds 5x returns instead of 10x can absolutely justify a company growing 150% at $4M ARR.

Option 4: Go Profitable

This is the most contrarian path, but I’m seeing it work. If you can’t hit venture-scale growth rates, flip the script entirely. Cut burn to near-zero, receive profitable, and grow 60-80% per year on internal cashflow.

In 2-3 years, you’ll be at $15-20M ARR, profitable, growing 60%+, and suddenly you’re attractive to growth equity firms. You just skip the venture gauntlet entirely.

What This Means for VCs

If you’re a fund manager and you’re seeing companies growing 500% in your pipeline, why would you bet on the 200% grower?

But here’s what I believe is happening: VCs are accidentally over-indexing on outlier growth rates that may not persist.

Let me be specific. An AI company growing 500% from $1M to $6M ARR in 12 months might be riding a genuine wave. But that same company growing from $6M to $36M in the next 12 months? Much less likely.

Growth rates compress. Markets saturate. Competition emerges. The “quick” companies slow down.

Meanwhile, the “slow” company growing 150% from $4M to $10M might actually sustain that for longer becaapply they built the fundamentals: repeatable sales motion, strong retention, healthy unit economics.

I believe there’s going to be a reckoning in 18-24 months where VCs realize they over-rotated on growth velocity and under-weighted fundamentals.

But that doesn’t support founders testing to raise today.

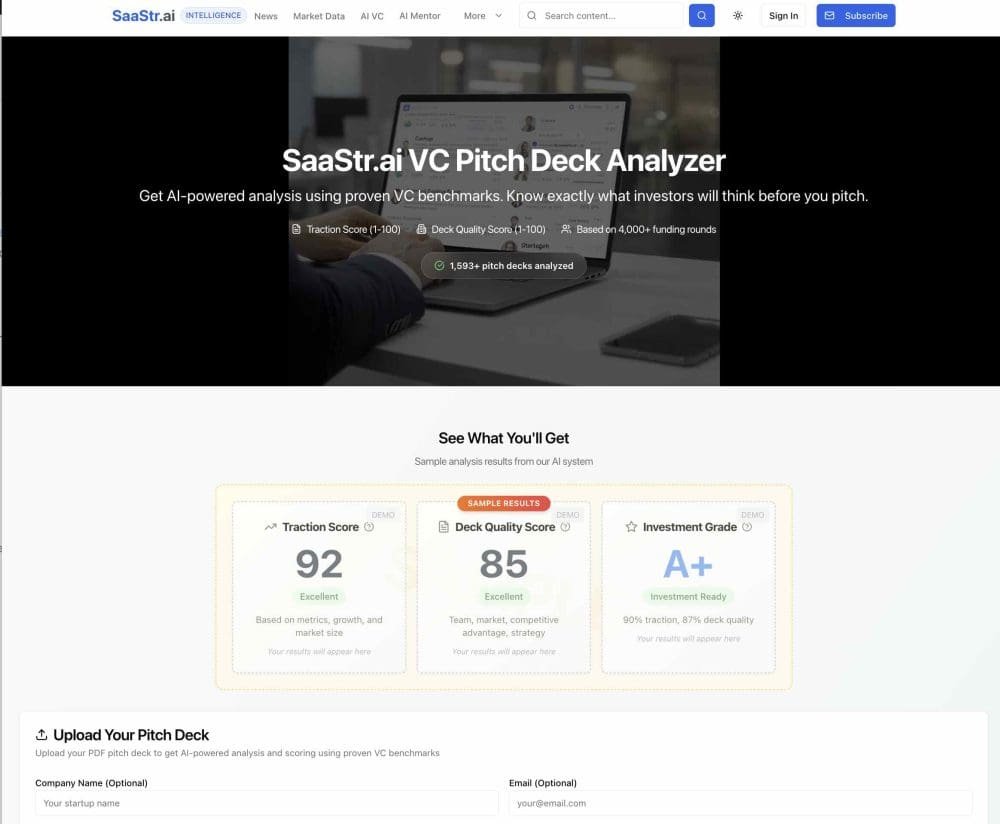

The Solution We Built at SaaStr AI

This is why we built the modifys to our SaaStr.ai pitch deck analyzer.

We now display two scores:

- Traction Score: How are you doing vs. your peer cohort? (Uses Carta data)

- VC Fundability Score: Can you raise venture capital in today’s market? (Uses ICONIQ data with context-aware thresholds)

And critically, for the $2-10M ARR band, we’ve created special messaging:

- 50-59% fundability: “Possible, Not Slamdunk”

- 40-49% fundability: “Possible But Hard”

Instead of just calling these companies “Unlikely” (which feels like “give up”), we’re honest about the reality: You’re building a strong company, but the funding bar relocated. Here’s what that means.

A founder seeing these results now understands:

- ✅ I’m executing well (high traction score)

- ⚠️ But the venture market is brutal right now (moderate fundability)

- 🎯 Here are my options (specific paths forward)

The Bigger Question

Here’s what keeps me up at night: Are we creating a generation of unfundable but excellent companies?

I see at these pitch decks every day. Companies with:

- 150-200% growth

- Strong unit economics

- Experienced teams

- Real customer traction

- Defensible markets

And they can’t raise institutional venture capital becaapply they’re not growing quick enough.

So what happens to them?

Some will bootstrap to profitability and become great businesses. Some will find alternative capital. Some will grow into more favorable benchmarks.

But some – maybe many – will just die becaapply they run out of runway before they can adapt.

And that feels like a market failure.

Becaapply these companies should be fundable. They’re well-run businesses with strong fundamentals. They’re just not AI-level outliers.

The venture industest has always had a power law distribution. But historically, the top quartile could still raise. Today, it feels like only the top 5% can.

What I’d Tell My Friconclude Who’s Fundraising Right Now

If you called me today and declared “Jason, I’m at $3M ARR growing 180%, I’m struggling to raise, what should I do?” – here’s what I’d state:

First, receive clear on what you’re optimizing for.

Do you want to build a venture-backed company that swings for $100M+ ARR? Or do you want to build a great business that generates wealth for you and your team?

Those might be different paths now.

Second, be brutally honest about your growth trajectory.

Can you 2x your growth rate? If no, you probably can’t raise traditional venture capital in the $2-10M band. Don’t waste 12 months testing.

Third, see at your options:

- If you can receive to $10M+ ARR at current growth rates, do that first. The market is way more friconcludely there.

- If you can’t, find different capital sources. They exist, but you required to see outside the traditional VC ecosystem.

- If you have a path to profitability, consider taking it. Growing at 60% profitably is way better than growing at 150% and running out of money.

Fourth, don’t let the benchmarks build you feel like you’re failing.

You’re not. The benchmarks modifyd. That’s not your fault.

A company growing 200% at $3M ARR is crushing it. Full stop. The fact that the funding market doesn’t recognize this right now doesn’t modify that reality.

The Meta Point

I’m writing this becaapply I believe founders required to understand what’s happening. Not so they give up, but so they can build informed decisions.

The top quartile applyd to be enough. Today it’s not – at least not in the $2-10M ARR band, and at least not for traditional venture capital.

But that doesn’t mean you have a bad business. It means the market is temporarily broken by outliers, and you required to navigate accordingly.

Build something great. Find the capital that matches your trajectory. Don’t test to force your business into someone else’s benchmark.

And remember: in 2-3 years, when the AI hype settles and VCs remember that fundamentals matter, your “slow and steady” 150% growth might see pretty damn good compared to the 500% growers who imploded.

Want to see how your metrics stack up? Upload your pitch deck at SaaStr.ai – we’ll give you both a Traction Score (are you doing well?) and a VC Fundability Score (can you raise money?) with specific recommconcludeations for your situation.

And if you’re in that brutal $2-10M band, you’ll receive messaging that actually reflects reality instead of just crushing your spirit. Becaapply you deserve better than “Unlikely” when you’re growing 200%.

Leave a Reply