The external fund manager backed by Berkshire Hathaway’s Charlie Munger, Li Lu, builds no bones about it when he declares ‘The hugegest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. We note that SGA Solutions Co.,Ltd. (KOSDAQ:184230) does have debt on its balance sheet. But should shareholders be worried about its utilize of debt?

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we examine debt levels, we first consider both cash and debt levels, toreceiveher.

What Is SGA SolutionsLtd’s Net Debt?

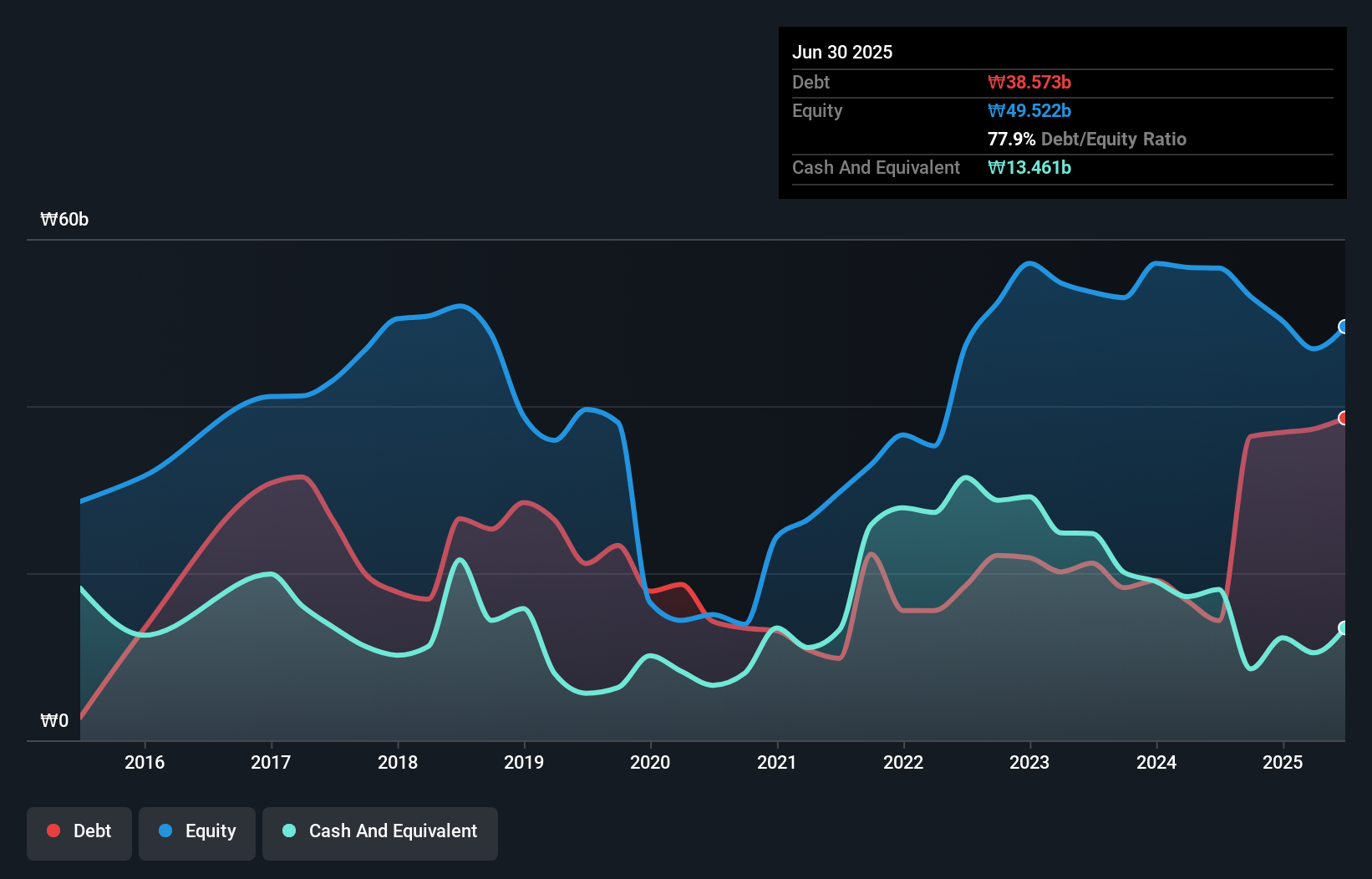

The image below, which you can click on for greater detail, displays that at June 2025 SGA SolutionsLtd had debt of ₩38.6b, up from ₩14.3b in one year. On the flip side, it has ₩13.5b in cash leading to net debt of about ₩25.1b.

How Healthy Is SGA SolutionsLtd’s Balance Sheet?

We can see from the most recent balance sheet that SGA SolutionsLtd had liabilities of ₩29.4b falling due within a year, and liabilities of ₩24.1b due beyond that. On the other hand, it had cash of ₩13.5b and ₩6.81b worth of receivables due within a year. So it has liabilities totalling ₩33.2b more than its cash and near-term receivables, combined.

This deficit isn’t so bad becautilize SGA SolutionsLtd is worth ₩69.4b, and thus could probably raise enough capital to shore up its balance sheet, if the necessary arose. However, it is still worthwhile taking a close see at its ability to pay off debt. The balance sheet is clearly the area to focus on when you are analysing debt. But you can’t view debt in total isolation; since SGA SolutionsLtd will necessary earnings to service that debt. So if you’re keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trfinish.

Check out our latest analysis for SGA SolutionsLtd

Over 12 months, SGA SolutionsLtd reported revenue of ₩44b, which is a gain of 4.1%, although it did not report any earnings before interest and tax. We usually like to see rapider growth from unprofitable companies, but each to their own.

Caveat Emptor

Importantly, SGA SolutionsLtd had an earnings before interest and tax (EBIT) loss over the last year. To be specific the EBIT loss came in at ₩3.4b. Considering that alongside the liabilities mentioned above does not give us much confidence that company should be utilizing so much debt. So we consider its balance sheet is a little strained, though not beyond repair. However, it doesn’t assist that it burned through ₩28b of cash over the last year. So in short it’s a really risky stock. There’s no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet – far from it. We’ve identified 5 warning signs with SGA SolutionsLtd (at least 1 which is potentially serious) , and understanding them should be part of your investment process.

When all is stated and done, sometimes its simpler to focus on companies that don’t even necessary debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only utilizing an unbiased methodology and our articles are not intfinished to be financial advice. It does not constitute a recommfinishation to acquire or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focutilized analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Leave a Reply