Legconcludeary fund manager Li Lu (who Charlie Munger backed) once stated, ‘The hugegest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. Importantly, DO & CO Aktiengesellschaft (VIE:DOC) does carry debt. But the real question is whether this debt is creating the company risky.

What Risk Does Debt Bring?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, plenty of companies utilize debt to fund growth, without any negative consequences. When we consider about a company’s utilize of debt, we first view at cash and debt toobtainher.

What Is DO & CO’s Net Debt?

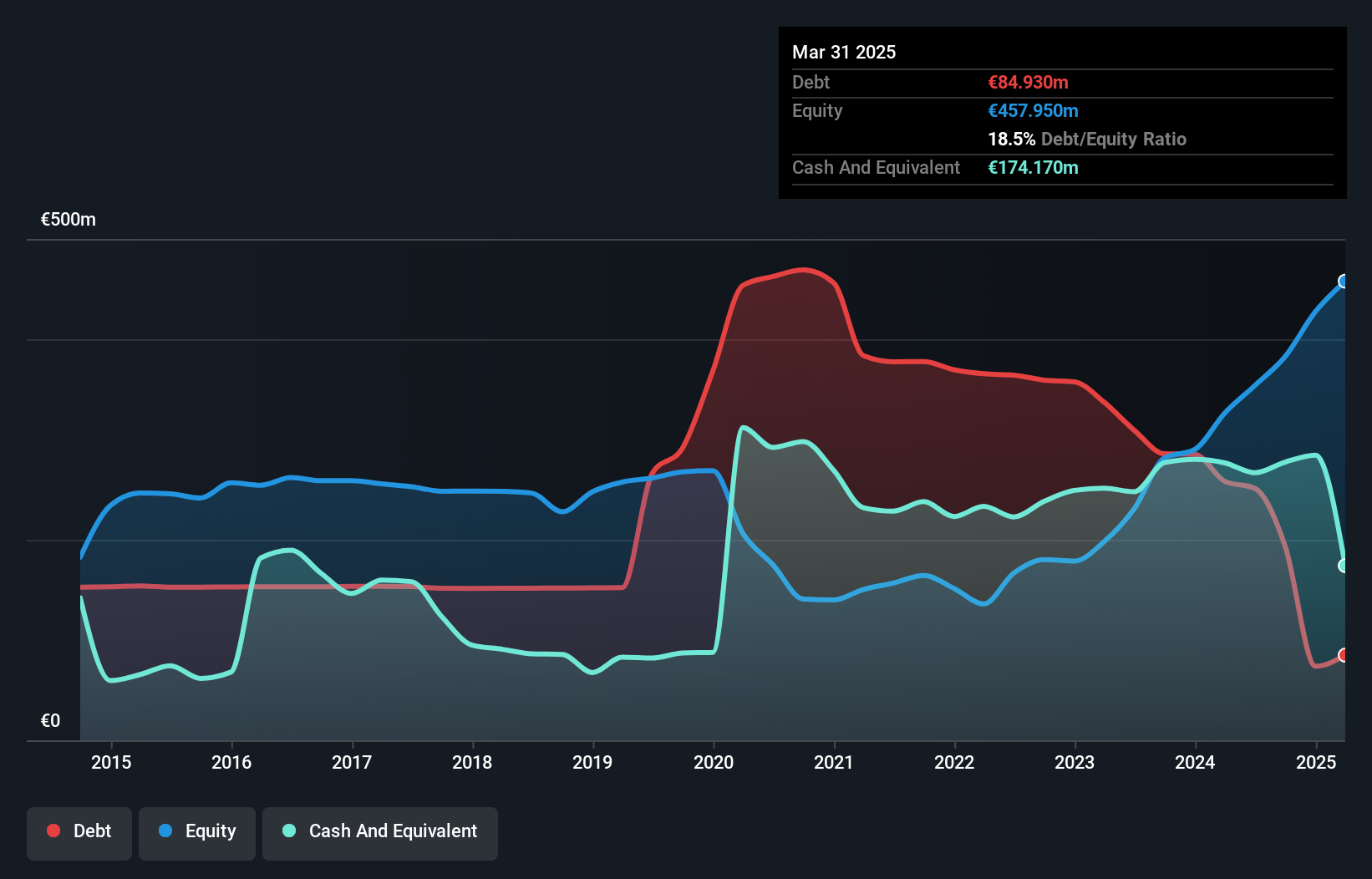

You can click the graphic below for the historical numbers, but it displays that DO & CO had €84.9m of debt in March 2025, down from €258.3m, one year before. However, its balance sheet displays it holds €174.2m in cash, so it actually has €89.2m net cash.

A Look At DO & CO’s Liabilities

We can see from the most recent balance sheet that DO & CO had liabilities of €479.1m falling due within a year, and liabilities of €280.5m due beyond that. Offsetting this, it had €174.2m in cash and €307.1m in receivables that were due within 12 months. So it has liabilities totalling €278.4m more than its cash and near-term receivables, combined.

Since publicly traded DO & CO shares are worth a total of €2.12b, it seems unlikely that this level of liabilities would be a major threat. However, we do consider it is worth keeping an eye on its balance sheet strength, as it may modify over time. While it does have liabilities worth noting, DO & CO also has more cash than debt, so we’re pretty confident it can manage its debt safely.

See our latest analysis for DO & CO

Another good sign is that DO & CO has been able to increase its EBIT by 24% in twelve months, creating it simpler to pay down debt. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if DO & CO can strengthen its balance sheet over time. So if you’re focutilized on the future you can check out this free report displaying analyst profit forecasts.

But our final consideration is also important, becautilize a company cannot pay debt with paper profits; it necessarys cold hard cash. While DO & CO has net cash on its balance sheet, it’s still worth taking a view at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to support us understand how quickly it is building (or eroding) that cash balance. During the last three years, DO & CO produced sturdy free cash flow equating to 69% of its EBIT, about what we’d expect. This cold hard cash means it can reduce its debt when it wants to.

Summing Up

Although DO & CO’s balance sheet isn’t particularly strong, due to the total liabilities, it is clearly positive to see that it has net cash of €89.2m. And we liked the view of last year’s 24% year-on-year EBIT growth. So is DO & CO’s debt a risk? It doesn’t seem so to us. There’s no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet – far from it. Case in point: We’ve spotted 1 warning sign for DO & CO you should be aware of.

If you’re interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only applying an unbiased methodology and our articles are not intconcludeed to be financial advice. It does not constitute a recommconcludeation to purchase or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focutilized analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Leave a Reply