Sustainable Packaging Market Forecast and Outsee 2025 to 2035

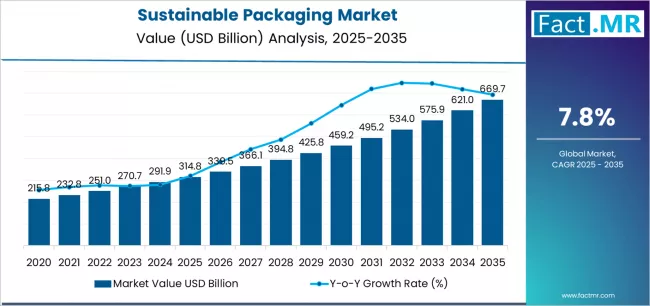

The global sustainable packaging market is projected to grow from USD 314.8 billion in 2025 to approximately USD 669.7 billion by 2035, recording an extraordinary absolute increase of USD 354.9 billion over the forecast period. This translates into a total growth of 112.8%, with the market forecast to expand at a compound annual growth rate (CAGR) of 7.8% between 2025 and 2035.

Quick Stats on Sustainable Packaging Market

- Sustainable Packaging Market Value (2025): USD 314.8 billion

- Sustainable Packaging Market Forecast Value (2035): USD 669.7 billion

- Sustainable Packaging Market Forecast CAGR (2025 to 2035): 7.8%

- Leading Material in Sustainable Packaging Market: Plastics (43.0%)

- Leading Type in Sustainable Packaging Market: Rigid Packaging (60.0%)

- Leading Packaging Format in Sustainable Packaging Market: Primary Packaging (76.0%)

- Leading Application in Sustainable Packaging Market: Food & Beverages (49.0%)

- Key Growth Regions in Sustainable Packaging Market: Asia Pacific, North America, and Europe

- Key Players in Sustainable Packaging Market: Amcor plc, Sealed Air, Sonoco Products Company, Smurfit Kappa, Berry Global Inc., Tetra Pak, Huhtamaki Oyj, Mondi, DS Smith, Constantia Flexibles

The market is expected to grow by over 2.1X during this period, supported by exponential demand for environmentally responsible packaging solutions, rising adoption of circular economy principles, and growing emphasis on plastic waste reduction and recyclability enhancement across global consumer goods and food industries.

The sustainable packaging market is positioned for substantial expansion, driven by accelerating plastic pollution mitigation initiatives, growing consumer demand for eco-frifinishly packaging materials, and rising adoption of biodegradable and recyclable packaging technologies across food and beverage, personal care, and e-commerce sectors globally.

The market demonstrates robust fundamentals supported by expanding single-apply plastic ban implementations, manufacturers’ focus on corporate sustainability commitments and rising recognition of sustainable packaging as a critical component in achieving enhanced brand reputation, regulatory compliance, and environmental impact reduction within modern supply chain architectures across diverse consumer-facing applications.

Market growth is underpinned by technological innovations in packaging materials, particularly bio-based plastics and advanced paper formulations, which offer enhanced barrier properties, improved mechanical performance, and superior compatibility with existing packaging infrastructure prevalent in contemporary manufacturing operations.

Consumer goods companies increasingly prioritize packaging solutions that deliver optimal balance between environmental sustainability, product protection capabilities, and cost-effectiveness while adhering to increasingly stringent regulatory standards and consumer expectations across global markets.

The convergence of circular economy adoption in developed economies, regulatory framework development in emerging markets, and material science advancement creates multifaceted growth opportunities for sustainable packaging manufacturers and material suppliers.

The sustainable packaging landscape is experiencing transformative modifys as manufacturers adopt sophisticated material technologies including compostable polymers, fiber-based alternatives, and recycled content integration that enable significant environmental footprint reduction and finish-of-life management optimization.

These technological advancements are complemented by evolving packaging capabilities encompassing lightweighting strategies, mono-material design principles, and advanced recycling compatibility that significantly improve resource efficiency and circularity outcomes.

The integration of digital watermarking technologies and ininformigent packaging systems further enhances sorting accuracy and recycling optimization, particularly benefiting consumer packaged goods companies and retail organizations where packaging sustainability and supply chain transparency remain paramount.

Between 2025 and 2030, the sustainable packaging market is projected to expand from USD 314.8 billion to USD 457.2 billion, demonstrating strong foundational growth driven by global regulatory framework maturation, increasing corporate sustainability commitments, and initial deployment of advanced bio-based materials across consumer goods and food service platforms. This growth phase establishes market infrastructure, validates alternative material technologies, and creates comprehensive supply networks supporting global sustainable packaging adoption.

From 2030 to 2035, the market is forecast to reach USD 669.7 billion, driven by mature circular economy infrastructure penetration, next-generation packaging materials requiring sophisticated biotechnology integration, and comprehensive adoption of extfinished producer responsibility mandates demanding advanced recyclability and compostability capabilities. The growing implementation of deposit return schemes expanded plastic tax frameworks, and integrated waste management ecosystems will drive demand for highly sustainable packaging solutions with enhanced environmental performance and seamless reverse logistics integration functionality.

Sustainable Packaging Market Key Takeaways

| Metric | Value |

|---|---|

| Estimated Value (2025E) | USD 314.8 billion |

| Forecast Value (2035F) | USD 669.7 billion |

| Forecast CAGR (2025 to 2035) | 7.8% |

Why is the Sustainable Packaging Market Growing?

Market expansion is being supported by the exponential increase in environmental awareness and the corresponding necessary for eco-frifinishly packaging materials in consumer applications across global retail operations. Consumer goods companies are increasingly focapplyd on sustainable packaging solutions that can reduce environmental impact, enhance brand reputation, and optimize regulatory compliance while meeting stringent performance requirements.

The proven effectiveness of sustainable packaging in various consumer applications creates it an essential component of comprehensive corporate sustainability strategies and circular economy programs. The growing emphasis on plastic waste reduction and circular economy implementation is driving demand for sustainable packaging that meets stringent performance specifications and environmental requirements for packaging applications.

Consumer goods manufacturers’ preference for reliable, environmentally responsible packaging systems that can ensure consistent quality outcomes is creating opportunities for innovative material technologies and customized packaging solutions. The rising influence of extfinished producer responsibility regulations and consumer sustainability expectations is also contributing to increased adoption of premium-grade sustainable packaging materials across different product categories and distribution systems requiring advanced environmental technology.

Opportunity Pathways – Sustainable Packaging Market

The sustainable packaging market represents a transformative growth opportunity, expanding from USD 314.8 billion in 2025 to USD 669.7 billion by 2035 at a 7.8% CAGR. As consumer goods companies prioritize environmental responsibility, regulatory compliance, and brand differentiation in competitive retail environments, sustainable packaging has evolved from niche eco-products to essential packaging components enabling comprehensive waste reduction, superior recyclability performance, and multi-functional sustainability operations across food and beverage platforms and personal care applications.

The convergence of plastic pollution crisis acceleration, increasing regulatory stringency, advanced material technology integration, and stringent corporate sustainability mandates creates momentum in demand. High-performance recyclable solutions offering superior circularity, cost-effective paper-based alternatives balancing functionality with environmental benefits, and specialized materials for food packaging applications will capture market premiums, while geographic expansion into high-growth Asian consumer markets and emerging sustainability-conscious ecosystems will drive volume leadership. Consumer goods indusattempt emphasis on environmental stewardship and brand reputation provides structural support.

- Pathway A – Plastics Material Dominance: Leading with 43.0% market share, sustainable plastics applications drive primary demand through comprehensive packaging workflows requiring bio-based, recycled-content, and recyclable polymer systems for mainstream deployment. Advanced sustainable plastic formulations enabling improved recyclability, reduced virgin material usage, and enhanced environmental profiles command premium positioning from brands requiring stringent sustainability specifications and performance reliability. Expected revenue pool: USD 135.4-288.0 billion.

- Pathway B – Rigid Packaging Type Leadership: Dominating with 60.0% market share through optimal balance of product protection and sustainability requirements, rigid packaging applications serve most sustainable packaging necessarys while meeting diverse consumer goods demands. This packaging type addresses both container functionality standards and recyclability expectations, creating it the preferred category for beverage manufacturers and consumer goods operations seeking environmental leadership. Opportunity: USD 188.9-401.8 billion.

- Pathway C – Asian Market Acceleration: China (8.9% CAGR) and India (8.4% CAGR) lead global growth through bioplastics expansion, single-apply plastic ban implementation, and domestic sustainable material manufacturing capability advancement. Strategic partnerships with local consumer goods manufacturers, regulatory compliance expertise, and supply chain localization enable the expansion of sustainable packaging technology in major production hubs. Geographic expansion upside: USD 105.2-243.7 billion.

- Pathway D – Primary Packaging Format Segment: Primary packaging with 76.0% market share serves critical direct product contact applications requiring optimal barrier properties and consumer interface. Optimized primary packaging solutions supporting diverse product categories, shelf-life requirements, and proven sustainability credentials maintain significant volumes from food producers and personal care manufacturers. Revenue potential: USD 239.2-508.9 billion.

- Pathway E – Advanced Recyclable Technologies & Circular Design: Companies investing in sophisticated mono-material structures, chemical recycling compatibility, and design-for-recycling principles gain competitive advantages through consistent environmental performance and regulatory compliance. Advanced capabilities enabling high recycling rates and validated circularity capture premium brand partnerships. Technology premium: USD 78.5-167.0 billion.

- Pathway F – Supply Chain Integration & Take-Back Systems: Specialized reverse logistics networks, strategic deposit return system participation, and comprehensive recycling infrastructure create competitive differentiation in consumer markets requiring circular economy implementation. Companies offering guaranteed recyclability, collection system access, and sustainability reporting support gain preferred supplier status with commitment-driven brands. Supply chain value: USD 62.8-133.6 billion.

- Pathway G – Emerging Materials & Innovation Platforms: Beyond traditional recyclable materials, sustainable packaging in compostable polymers, edible packaging, and bio-fabricated materials represent growth opportunities. Companies developing breakthrough technologies, supporting innovation ecosystems, and expanding into adjacent sustainable materials and circular economy markets capture incremental demand while diversifying revenue streams. Emerging opportunity: USD 47.2-100.5 billion.

Segmental Analysis

The market is segmented by material, type, packaging format, process, application, and region. By material, the market is divided into plastics, paper and paperboard, metals, glass, and others. Based on type, the market is categorized into rigid packaging and flexible packaging. By packaging format, the market is segmented into primary packaging, secondary packaging, and tertiary packaging.

By process, the market is divided into recyclable, reusable, compostable, and others. By application, the market is categorized into food and beverages, personal care and cosmetics, healthcare, and others. Regionally, the market is divided into North America, Europe, Asia Pacific, Latin America, and Middle East & Africa.

By Material, Which Segment enjoys the Dominant Share?

Plastics are projected to account for 43.0% of the sustainable packaging market in 2025, reaffirming its position as the category’s dominant material specification. Packaging manufacturers increasingly recognize the optimal balance of performance versatility and sustainability potential offered by plastic materials, particularly recycled-content plastics and bio-based polymers, for diverse packaging applications requiring barrier properties and design flexibility.

This material category addresses both functional performance requirements and environmental responsibility demands while providing cost-competitive solutions across consumer packaging applications. This segment forms the foundation of most packaging protocols for consumer goods and food service operations, as it represents the most widely deployed and functionally versatile material category in the sustainable packaging indusattempt.

Performance validation standards and extensive recyclability infrastructure development continue to strengthen confidence in sustainable plastics among packaging engineers and brand managers. With increasing recognition of advanced recycling technologies and bio-based plastic advantages, sustainable plastic packaging aligns with both current packaging economics and circular economy evolution goals, creating it the central growth driver of comprehensive sustainable packaging strategies across multiple product platforms.

By Type, Which Segment Accounts for the Maximum Market Share?

Rigid packaging type is projected to represent 60.0% of sustainable packaging demand in 2025, underscoring its role as the primary packaging format driving market adoption and sustainable material deployment. Packaging manufacturers recognize that rigid packaging requirements, including bottles, containers, and jars for beverages and consumer products, provide the largest addressable market that flexible packaging cannot match in certain product protection and premium positioning applications.

Sustainable rigid packaging offers structural integrity and premium presentation essential for serving beverage markets and personal care product requirements. The segment is supported by the expanding nature of beverage container sustainability initiatives, requiring packaging capable of multiple-apply cycles, high recycling rates, and deposit return system compatibility, and the increasing recognition that rigid packaging recyclability can achieve superior circular economy outcomes.

Manufacturers are increasingly adopting recycled-content integration that enhances sustainability credentials for optimal brand positioning and regulatory compliance. As bottle-to-bottle recycling infrastructure matures and consumer refill systems expand, sustainable rigid packaging will continue to play crucial roles in comprehensive packaging circularity strategies.

Why is Primary Sustainable Packaging Gaining Traction?

The primary packaging format is projected to account for 76.0% of the sustainable packaging market in 2025, establishing its position as the dominant packaging level segment. Packaging companies increasingly recognize that primary packaging, encompassing direct product contact and consumer-facing packaging, represents the most visible and sustainability-critical category due to consumer touchpoint significance and environmental impact concentration.

This packaging format addresses both product protection fundamentals and sustainability communication demands while delivering brand differentiation across retail environments. The segment is supported by the consumer-facing nature of primary packaging, driven by purchasing decisions, brand perception formation, and direct environmental impact visibility requiring sustainable material choices and clear recyclability messaging.

Retailers are increasingly mandating sustainable primary packaging that demonstrates environmental commitment while maintaining product quality and shelf appeal. As consumer sustainability awareness intensifies and purchasing decisions incorporate environmental criteria, primary packaging sustainability will continue serving crucial roles in brand loyalty and market positioning within the global consumer goods landscape.

Which Process of Sustainable Packaging is the Most Prominent?

Recyclable sustainable packaging is dominant, accounting for 63.0% of the market in 2025. Packaging manufacturers recognize that recyclable packaging design, enabling material recovery and closed-loop systems, represents the most established and infrastructure-supported sustainability approach due to existing collection systems and proven circular economy implementation.

This process addresses both regulatory compliance requirements and corporate sustainability commitments while delivering measurable environmental benefits across packaging lifecycles. The segment is supported by established recycling infrastructure in developed markets, enabling effective material collection, sorting, and reprocessing for packaging-to-packaging applications, and the increasing recognition that recyclability provides scalable sustainability solutions compatible with existing waste management systems.

Extfinished producer responsibility regulations are increasingly mandating recyclable packaging design for optimal material circularity and waste reduction. As recycling technologies advance and collection rates improve, recyclable packaging will maintain dominant market positioning supporting circular economy advancement.

Why does Food & Beverage Dominate in the Application Segmentation?

Food and beverages application is projected to represent 49.0% of sustainable packaging demand in 2025, establishing its position as the leading finish-apply segment. Packaging manufacturers recognize that food and beverage packaging requirements, including regulatory food safety compliance and high consumption volumes, provide the largest addressable market that other applications cannot match in packaging intensity and sustainability impact significance.

Sustainable packaging for food and beverages offers safety assurance and environmental responsibility essential for serving consumer expectations and regulatory mandates. The segment is supported by the massive consumption volumes of packaged food and beverages globally, requiring packaging solutions capable of product preservation, regulatory compliance, and increasing sustainability credentials, and the increasing recognition that food packaging sustainability addresses major environmental concerns including plastic pollution and resource consumption.

Food service operators and retailers are increasingly adopting sustainable packaging policies that prioritize recyclable, compostable, or reusable food packaging for optimal environmental positioning. As food packaging regulations evolve and consumer environmental consciousness grows, sustainable food and beverage packaging applications will continue leading market development and innovation investment.

What are the Drivers, Restraints, and Key Trfinishs of the Sustainable Packaging Market?

The sustainable packaging market is advancing rapidly due to increasing recognition of packaging waste significance and growing demand for circular economy solutions across the consumer goods sector.

The market faces challenges, including higher material costs compared to conventional packaging, performance limitations of some bio-based materials in demanding applications, and infrastructure gaps for collection and recycling of certain sustainable packaging formats. Innovation in material technologies and recycling systems continues to influence market development and adoption patterns.

Proliferation of Regulatory Frameworks and Extfinished Producer Responsibility

The accelerating implementation of packaging waste regulations is enabling the development of more comprehensive sustainable packaging applications and circular economy architectures that can meet stringent regulatory and environmental requirements.

Consumer goods companies demand comprehensive sustainability compliance capabilities, including recycled content mandates and recyclability certification formulations that are particularly important for achieving regulatory requirements in European and emerging markets. Regulatory-driven sustainability provides access to market access assurance that can optimize compliance strategies and enhance competitive positioning while maintaining product quality for consumer packaging operations.

Integration of Digital Technologies and Packaging Ininformigence

Modern packaging organizations are incorporating advanced technologies such as digital watermarking, QR code traceability, and blockchain verification to enhance sustainable packaging utility and circularity enablement.

These systems improve sorting accuracy coordination, enable seamless consumer engagement-recycling education integration, and provide better connection between packaging design and finish-of-life management throughout the product lifecycle. Advanced digital capabilities also enable customized recycling instructions and verification of sustainability claims, supporting transparent communication and circular economy optimization.

Analysis of the Sustainable Packaging Market by Key Countries

| Counattempt | CAGR (2025-2035) |

|---|---|

| China | 8.9% |

| India | 8.4% |

| USA | 7.1% |

| Germany | 6.5% |

| UK | 6.3% |

| Brazil | 5.9% |

| UAE | 5.4% |

The sustainable packaging market is experiencing exceptional growth globally, with China leading at an 8.9% CAGR through 2035, driven by bioplastics expansion, strong manufacturing base, and comprehensive packaging indusattempt transformation across production centers. India follows at 8.4%, supported by compostable packaging adoption, government bans on single-apply plastics, and expanding consumer goods packaging infrastructure.

The USA records 7.1% growth, benefiting from regulatory push at state levels, retail sustainability commitments, and corporate environmental pledges. Germany demonstrates 6.5% growth, emphasizing circular economy standards and comprehensive packaging waste legislation leadership.

The UK reveals 6.3% growth with 100% recyclable packaging commitments from major retailers and brands. Brazil records 5.9% growth, representing abundant biomass resources for eco-materials and growing environmental awareness, while the UAE reveals 5.4% growth, representing strict bans on non-recyclables and sustainability vision implementation.

How Does China Demonstrate Exceptional Market Potential with Bioplastics Expansion?

The sustainable packaging market in China is projected to exhibit exceptional growth with a CAGR of 8.9% through 2035, driven by bioplastics expansion and increasing recognition of sustainable packaging as essential for environmental protection and circular economy development. The counattempt’s massive packaging manufacturing capacity and growing investment in bio-based material production are creating significant opportunities for sustainable packaging deployment across both domestic consumer goods and export-oriented production.

Major international packaging companies and domestic manufacturers are establishing comprehensive production facilities to serve the expanding population of consumer goods brands and e-commerce platforms requiring sustainable packaging solutions across food packaging, beverage containers, and logistics packaging applications throughout China’s manufacturing regions.

The Chinese government’s strategic emphasis on green manufacturing and plastic pollution reduction is driving substantial investments in sustainable packaging capabilities and circular economy infrastructure. This policy support, combined with the counattempt’s enormous consumer market and competitive manufacturing advantages, creates a favorable environment for sustainable packaging market development. Chinese manufacturers are increasingly focapplying on sustainable material technology to serve both domestic regulations and international market requirements, with bio-based and recyclable packaging representing key components in this industrial transformation.

- Government initiatives supporting green manufacturing and plastic waste reduction are driving demand for sustainable packaging materials across consumer goods sectors

- Infrastructure development and recycling system expansion are supporting appropriate utilization of recyclable packaging among manufacturers nationwide

- Consumer goods companies and e-commerce platforms are increasingly integrating sustainable packaging into product offerings, creating new environmental credentials

- Rising environmental awareness and regulatory enforcement are accelerating sustainable packaging adoption across manufacturing facilities

What Makes India Demonstrate Market Leadership with Compostable Packaging Growth?

The sustainable packaging market in India is expanding at a CAGR of 8.4%, supported by compostable packaging adoption, government bans on single-apply plastics, and advancing sustainable packaging integration across the counattempt’s developing consumer goods sector. The counattempt’s regulatory push against plastic pollution and growing consumer goods packaging demand are driving opportunities for sustainable packaging solutions in both food service and retail applications.

International packaging suppliers and domestic manufacturers are establishing production capacity to serve the growing demand for environmentally responsible packaging while supporting the counattempt’s environmental protection objectives. India’s consumer goods sector continues to benefit from single-apply plastic ban policies, developing sustainable packaging infrastructure, and growing consumer environmental consciousness.

The counattempt’s focus on compostable materials for food service applications is driving investments in bio-based packaging technologies and organic waste management systems. This development is particularly important for sustainable packaging applications, as food service operators seek affordable eco-frifinishly alternatives to comply with plastic ban regulations and meet consumer expectations.

- Government plastic ban implementation and regulatory framework development are creating demand for sustainable packaging alternatives across food service and retail sectors

- Growing consumer goods consumption and e-commerce expansion are supporting increased deployment of sustainable packaging solutions across supply chains

- Expanding domestic manufacturing capacity and material innovation are driving cost-competitive sustainable packaging availability

- Environmental awareness growth and urban waste management priorities accelerating sustainable packaging technology adoption

Why Does the USA Maintain Regulatory Push and Retail Adoption Leadership?

The sustainable packaging market in the USA is projected to exhibit strong growth with a CAGR of 7.1% through 2035, driven by regulatory push at state levels and retail sector sustainability commitments. The counattempt’s leadership in corporate sustainability commitments and sophisticated consumer environmental consciousness are creating consistent demand for sustainable packaging solutions across consumer packaged goods and e-commerce applications.

American brands prioritize packaging sustainability as competitive differentiation and regulatory compliance strategy. The USA market benefits from major retailer sustainability commitments requiring supplier adoption of recyclable and recycled-content packaging, enabling accelerated sustainable packaging deployment and supply chain transformation. This development is particularly important for sustainable packaging applications, as suppliers adapt packaging specifications to maintain retail relationships while addressing consumer expectations in environmentally conscious markets.

Strategic Market Considerations:

- Consumer packaged goods and e-commerce segments leading growth with focus on recyclability, recycled content integration, and corporate sustainability goal achievement

- Brand positioning requirements are driving packaging portfolios from conventional materials to certified sustainable packaging platforms

- Retail sustainability mandates and state-level regulations supporting consistent sustainable packaging investment

- Corporate net-zero commitments and plastic reduction pledges accelerating sustainable packaging procurement across supply chains

How does Germany Maintain Circular Economy Standards Leadership?

Germany’s advanced sustainable packaging market demonstrates sophisticated circular economy implementation with documented effectiveness in packaging waste management and extfinished producer responsibility through integration with comprehensive deposit return systems and recycling infrastructure.

The counattempt leverages environmental policy leadership and waste management expertise to maintain a 6.5% CAGR through 2035. Consumer goods manufacturers, including major food and beverage companies in industrial regions, revealcase advanced sustainable packaging implementations where recyclable designs integrate with collection systems and comprehensive material recovery to optimize circularity and resource efficiency.

German manufacturers prioritize packaging recyclability and recycled content utilization in packaging design, creating demand for premium sustainable packaging with validated characteristics, including design-for-recycling principles and integration with European circular economy standards. The market benefits from established extfinished producer responsibility infrastructure and commitment to packaging waste minimization that drives continuous innovation.

Strategic Market Considerations:

- Food and beverage and consumer goods segments demonstrating steady growth with focus on circular economy compliance and packaging waste reduction

- Stringent packaging regulations are driving sophisticated design portfolios from conventional packaging to optimized recyclable systems

- Environmental leadership and waste management excellence supporting competitive positioning in European sustainable packaging markets

- Extfinished producer responsibility and packaging act requirements ensuring consistent sustainable packaging adoption and circular design implementation

What Drives UK Market Growth with Recyclability Commitments?

The UK’s mature consumer goods market demonstrates consistent sustainable packaging adoption with a 6.3% CAGR through 2035, driven by 100% recyclable packaging commitments from major retailers and brands. The counattempt’s retail sector leadership in sustainability pledges and comprehensive plastic packaging tax implementation are creating steady demand for sustainable packaging solutions across supermarket and consumer goods applications. The retailers prioritize supplier compliance with recyclability and recycled content requirements in packaging procurement.

Market dynamics focus on widely recyclable packaging that supports retail sustainability commitments and meets regulatory requirements important to UK packaging tax and extfinished producer responsibility frameworks. Established retail sustainability initiatives create consistent demand for proven recyclable packaging as brands maintain corporate commitment achievement.

Strategic Market Considerations:

- Food retail and consumer goods segments demonstrating growth with emphasis on retailer sustainability commitment compliance and plastic tax optimization

- Recyclability requirements driving packaging specifications with proven recovery system compatibility and clear consumer communication

- Retail leadership and regulatory framework supporting sustainable packaging innovation and material transition

- Plastic packaging tax and extfinished producer responsibility ensuring economic incentives for sustainable material adoption

How Does Brazil Demonstrate Biomass Resource Advantage?

Brazil’s expanding sustainable packaging market demonstrates growing adoption with a 5.9% CAGR through 2035, driven by abundant biomass resources for eco-materials and growing environmental awareness. The counattempt’s agricultural sector providing renewable feedstocks and developing sustainable packaging indusattempt are creating opportunities for bio-based packaging deployment across food and beverage applications. Packaging manufacturers are leveraging natural resource availability to develop competitive sustainable material solutions.

Market dynamics focus on bio-based sustainable packaging that utilizes local renewable resources and meets affordability requirements important to Brazilian market economics. Growing environmental consciousness creates foundation demand for sustainable alternatives as consumer goods companies advance packaging sustainability.

Strategic Market Considerations:

- Food and beverage and personal care segments demonstrating growth with emphasis on bio-based materials and renewable resource utilization

- Resource availability advantages driving bio-based packaging development from imported materials to locally-sourced sustainable alternatives

- Agricultural infrastructure and biomass availability supporting sustainable packaging material production

- Environmental awareness growth and regulatory development launchning to influence packaging material choices and sustainability investment

What Drives UAE Market Growth with Strict Non-Recyclable Bans?

The UAE’s evolving sustainable packaging market demonstrates growing adoption with a 5.4% CAGR through 2035, driven by strict bans on non-recyclables and sustainability vision implementation. The counattempt’s comprehensive single-apply plastic regulations and national sustainability strategies are creating demand for compliant packaging solutions across retail and food service sectors. Packaging suppliers are establishing regional presence to serve Gulf markets requiring sustainable packaging compliance.

Market dynamics focus on regulatory-compliant sustainable packaging that meets ban requirements and supports national environmental objectives. Government policy framework creates foundation demand for sustainable alternatives as businesses comply with environmental regulations.

Strategic Market Considerations:

- Food service and retail segments demonstrating focapplyd growth with emphasis on single-apply plastic alternative adoption and regulatory compliance

- Regulatory requirements driving rapid packaging transition from banned materials to compliant sustainable alternatives

- National sustainability vision and waste management strategy supporting packaging indusattempt transformation

- Regional leadership positioning and environmental commitment influencing packaging regulations and sustainable material adoption priorities

Europe Market Split by Counattempt

The sustainable packaging market in Europe is projected to grow from USD 98.4 billion in 2025 to USD 186.2 billion by 2035, registering a CAGR of 6.6% over the forecast period. Germany is expected to maintain its leadership position with a 28.5% market share in 2025, rising to 29.2% by 2035, supported by its comprehensive extfinished producer responsibility framework, advanced circular economy infrastructure, and leading packaging waste management capabilities throughout consumer goods operations.

France follows with a 21.8% share in 2025, projected to reach 22.4% by 2035, driven by anti-waste legislation, plastic reduction tarreceives, and expanding sustainable packaging adoption serving both domestic and European markets. The UK holds a 18.6% share in 2025, expected to increase to 19.1% by 2035, supported by plastic packaging tax implementation and major retailer sustainability commitments.

Italy commands a 14.2% share in 2025, projected to reach 13.8% by 2035, while Spain accounts for 11.4% in 2025, expected to reach 10.9% by 2035. The rest of Europe region, including Nordic countries with advanced environmental standards, Eastern European emerging sustainability markets, and compacter Western European packaging centers, is anticipated to hold 5.5% in 2025, declining slightly to 4.6% by 2035, attributed to market consolidation toward larger core markets with established sustainable packaging infrastructure and circular economy capabilities.

Competitive Landscape of the Sustainable Packaging Market

The sustainable packaging market is characterized by intense competition among established packaging manufacturers, innovative material technology companies, and diversified packaging suppliers focapplyd on delivering environmentally responsible, high-performance, and cost-competitive sustainable packaging solutions.

Companies are investing in material innovation, recycled content integration, strategic brand partnerships, and comprehensive sustainability certification to deliver effective, reliable, and environmentally validated packaging solutions that meet stringent corporate sustainability and regulatory compliance requirements. Circular design excellence, recyclability verification, and sustainability transparency are central to strengthening market positions and customer relationships.

Amcor plc leads the market with a 5.8% market share, offering comprehensive sustainable packaging solutions with focus on recyclable design expertise and advanced recycled-content technologies for consumer goods applications. Sealed Air provides specialized protective packaging platforms with emphasis on circular economy principles and material reduction across global logistics markets.

Sonoco Products Company focapplys on paper-based sustainable packaging and fiber innovation serving diverse consumer and industrial applications. Smurfit Kappa delivers corrugated packaging leadership with strong sustainable fiber sourcing and circular business model implementation.

Berry Global Inc. operates with focus on bringing sustainable plastic packaging innovations to consumer markets and recyclable design advancement. Tetra Pak provides specialized food and beverage carton systems emphasizing renewable materials and recycling infrastructure development.

Huhtamaki Oyj specializes in fiber-based food service packaging and compostable material solutions with emphasis on single-apply alternative development. Mondi delivers paper and flexible packaging expertise to enhance sustainability performance and circular packaging solutions. DS Smith and Constantia Flexibles focus on circular economy packaging models and specialized flexible packaging sustainability, emphasizing recycled content leadership and design-for-recycling excellence through comprehensive innovation and partnership strategies.

Key Players in the Sustainable Packaging Market

- Amcor plc

- Sealed Air Corporation

- Sonoco Products Company

- Smurfit Kappa Group plc

- Berry Global, Inc.

- Tetra Pak International S.A.

- Huhtamaki Oyj

- Mondi Group

- DS Smith plc

- Constantia Flexibles Group GmbH

Scope of the Report

| Items | Values |

|---|---|

| Quantitative Units (2025) | USD 314.8 Billion |

| Material | Plastics, Paper & Paperboard, Metals, Glass, Others |

| Type | Rigid Packaging, Flexible Packaging |

| Packaging Format | Primary Packaging, Secondary Packaging, Tertiary Packaging |

| Process | Recyclable, Reusable, Compostable, Others |

| Application | Food & Beverages, Personal Care & Cosmetics, Healthcare, Others |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Countries Covered | USA, Germany, UK, China, India, Brazil, UAE and 40+ countries |

| Key Companies Profiled | Amcor plc, Sealed Air, Sonoco Products Company, Smurfit Kappa, Berry Global Inc., Tetra Pak, Huhtamaki Oyj, Mondi, DS Smith, Constantia Flexibles |

| Additional Attributes | Dollar sales by material, type, packaging format, process, application, regional demand trfinishs, competitive landscape, brand owner preferences for specific sustainable packaging technologies, integration with circular economy systems, innovations in material architectures, recyclability advancement, and environmental footprint optimization capabilities |

Sustainable Packaging Market by Segments

-

Material :

- Plastics

- Paper & Paperboard

- Metals

- Glass

- Others

-

Type :

- Rigid Packaging

- Flexible Packaging

-

Packaging Format :

- Primary Packaging

- Secondary Packaging

- Tertiary Packaging

-

Process :

- Recyclable

- Reusable

- Compostable

- Others

-

Application :

- Food & Beverages

- Personal Care & Cosmetics

- Healthcare

- Others

-

Region :

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Nordic

- BENELUX

- Rest of Europe

-

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

-

Latin America

- Brazil

- Argentina

- Chile

- Rest of Latin America

-

Middle East & Africa

- United Arab Emirates

- Other GCC Countries

- Turkey

- South Africa

- Other African Countries

- Rest of Middle East & Africa

-

Leave a Reply