- Earlier in March 2026, Lucid Group outlined a new midsize EV platform, next-generation Atlas drive unit, robotaxi concept, and expanded software strategy, while also rolling out Apple CarPlay and Android Auto to Gravity SUVs and signing German dealer Wackenhut as its first European retail partner.

- This combination of a hybrid retail model in Europe and a broader technology roadmap marks a shift toward scaling volumes, diversifying revenue, and tightening cost efficiency across Lucid’s business.

- We’ll now examine how Lucid’s midsize platform and European hybrid retail expansion affect the company’s existing investment narrative and risks.

Rare earth metals are the new gold rush. Find out which 28 stocks are leading the charge.

Lucid Group Investment Narrative Recap

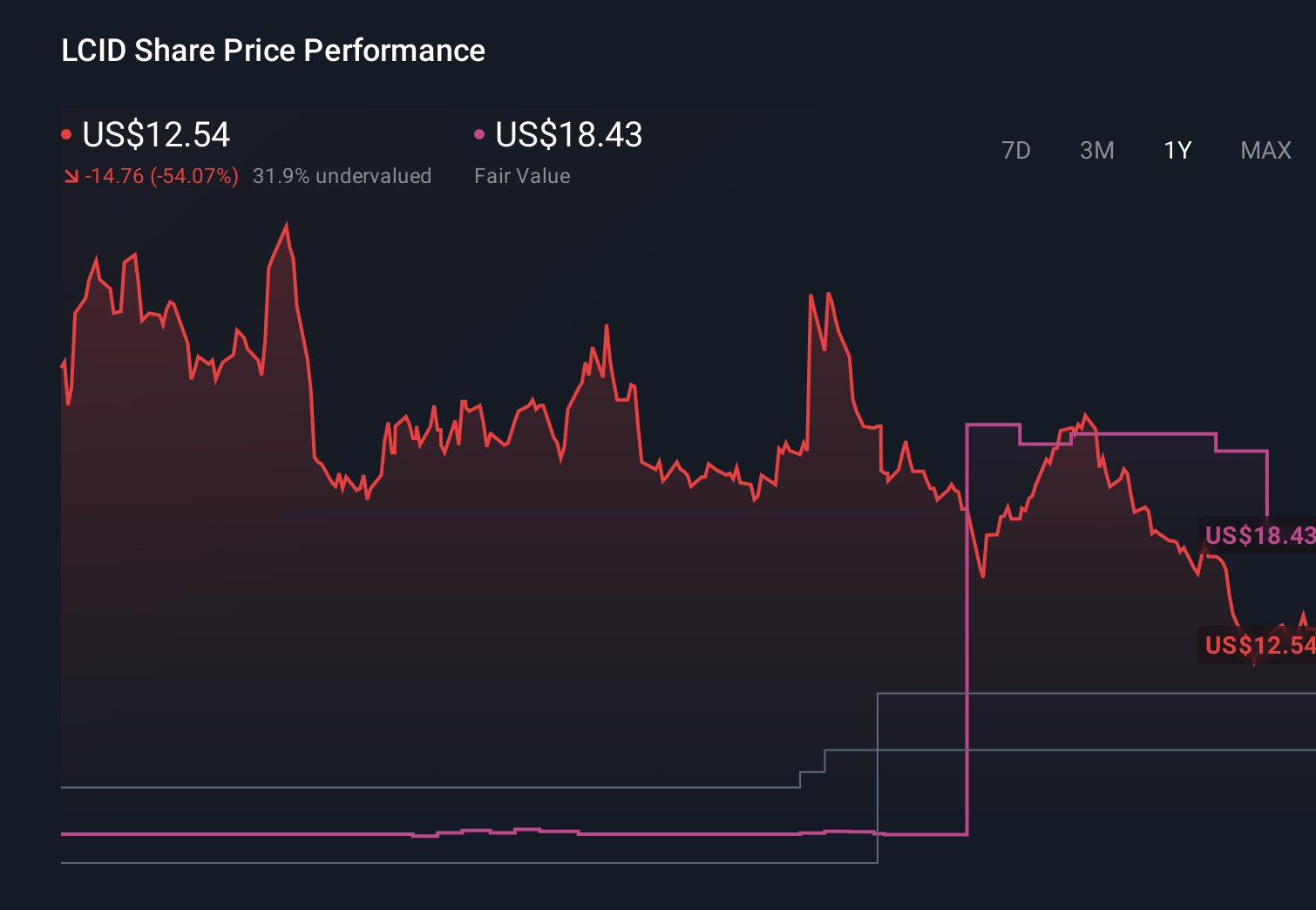

To own Lucid today, you have to believe the company can turn its EV technology and brand into a sustainable, higher volume business before cash constraints and losses bite too hard. The latest news around the midsize platform and expanded software and robotaxi roadmap reinforces the existing near term catalyst of scaling volumes and monetizing technology, but it does not rerelocate the central risk of ongoing negative margins and heavy reliance on external capital.

The most relevant update here is Lucid’s detailed midsize platform and Atlas drive unit plan, including sub US$50,000 models and the Lunar robotaxi concept. This directly connects to the earlier Uber and Nuro fleet commitments by outlining how Lucid aims to reduce bill of materials, improve manufacturing efficiency, and open higher volume segments, all of which sit at the heart of the company’s key scaling and margin improvement catalysts.

Yet alongside this upside, investors should be aware of the ongoing dilution and cash burn risk, especially as…

Read the full narrative on Lucid Group (it’s free!)

Lucid Group’s narrative projects $5.6 billion revenue and $285.8 million earnings by 2028.

Uncover how Lucid Group’s forecasts yield a $16.67 fair value, a 66% upside to its current price.

Exploring Other Perspectives

Compared with the baseline view, the lowest analysts sound far more cautious, even while assuming revenue could reach about US$3.3 billion and earnings US$167 million by 2028, so it is worth seeing how this pessimism stacks up against Lucid’s new midsize and robotaxi ambitions.

Explore 6 other fair value estimates on Lucid Group – why the stock might be worth 25% less than the current price!

Decide For Yourself

Don’t just follow the ticker – dig into the data and build a conviction that’s truly your own.

Want Some Alternatives?

Our top stock finds are flying under the radar-for now. Get in early:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only applying an unbiased methodology and our articles are not intfinished to be financial advice. It does not constitute a recommfinishation to acquire or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focutilized analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividfinish Powerhoutilizes (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Leave a Reply