Hey all, Jason here.

I’m more than a week into my time in Oaxaca, and five days into Spanish classes. I’m doing a four hour class each weekday — four hours not viewing at a screen is, pun intconcludeed, certainly a foreign experience.

If I were working this week, I’d check out this virtual event from Brex and Unit21 on building an “AI-native” compliance program, views like a good one!

Partner content: At Effects 26, Plaid is bringing toobtainher leaders to discuss how AI is modifying finance in real time. Hear from Plaid CEO Zach Perret, CTO Will Robinson, and Head of Data & AI Suddu Seshadri, along with leaders across fintech, banking, and tech.

Join us virtually on May 21 as we explore how AI, better data, and real-time decisioning are transforming financial systems.

I started writing this newsletter in the fall of 2020. It was, arguably, the most intense period of the COVID-19 pandemic, with widespread travel restrictions and lockdowns and before vaccines were available.

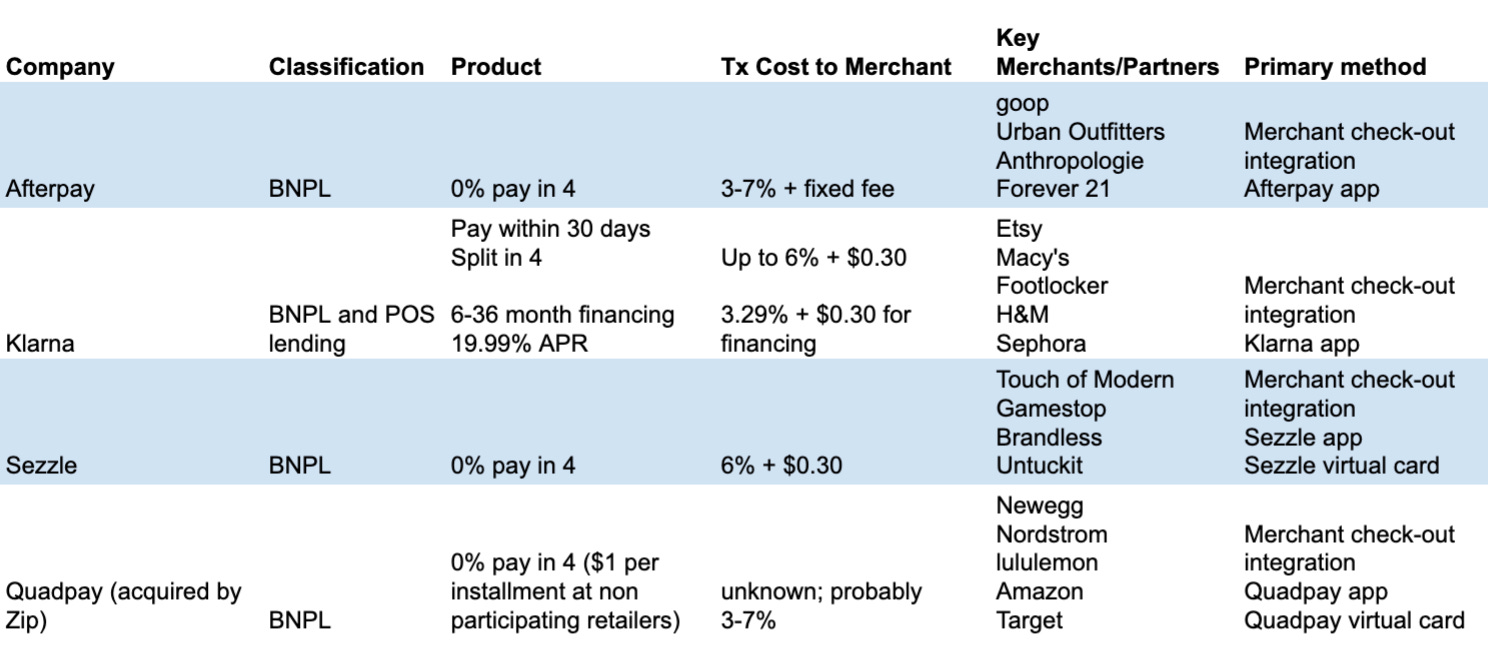

The first post I wrote that really took off was on a topic that now may feel a bit quaint: acquire now pay later.

It may be hard to remember now, but it is difficult to overstate just how excited people in fintech, including VCs and the press, were about BNPL at the time. With its obvious ties to ecommerce, which grew dramatically during the first part of the pandemic, the narrative held logical appeal (and assisted power Klarna raising capital at a $47 billion valuation in 2021 and Afterpay being acquired by Block in January 2022.)

At the time, I found some analysis and discussion of the space frustrating, as some conflated the short-term, compact-dollar pay-in-four product with longer-term, larger interest-bearing loans.

Since I published this piece in late 2020, BNPL has been more “evolution” than “revolution.” Category leaders like Affirm and Klarna have continued to expand their product stack, while studiously avoiding offering the product both portray negatively: a credit card.

But both companies do offer bank account-like products with cards that enable utilizers to spconclude via their cards and opt to convert any eligible transaction into a BNPL plan.

Both Klarna and Affirm, in their apps and websites, position themselves first and foremost as shopping destinations — assisting to address a risk I cite in the piece below about potential lack of utilizer loyalty to a given service.

And, while it operates in the U.S. through partners, Klarna has long been a bank in its home countest of Sweden, and Affirm, earlier this year, filed an application to charter an ILC in Nevada and a corresponding application with the FDIC for deposit insurance.

Afterpay is now part of Cash App / Block, which, in addition to its core peer-to-peer payments feature, also offers a bank account-like product and compact-dollar loans, and Block itself owns a bank: Square Financial Services, a Utah ILC.

In retrospect, what exploded in popularity during the early days of the pandemic has come to be a wedge product/feature for a slate of (relatively) new entrants to acquire consumers and cross-sell them into a broader set of products and services.

With that, here’s my original post on BNPL from November 2020.

I’ve been wanting to write something on the evolving “acquire now, pay later” space, and with Affirm’s S-1 filing and the upcoming shopping bonanzas of Black Friday/Cyber Monday, this was the week. It’s a bit on the long side, but hope you enjoy.

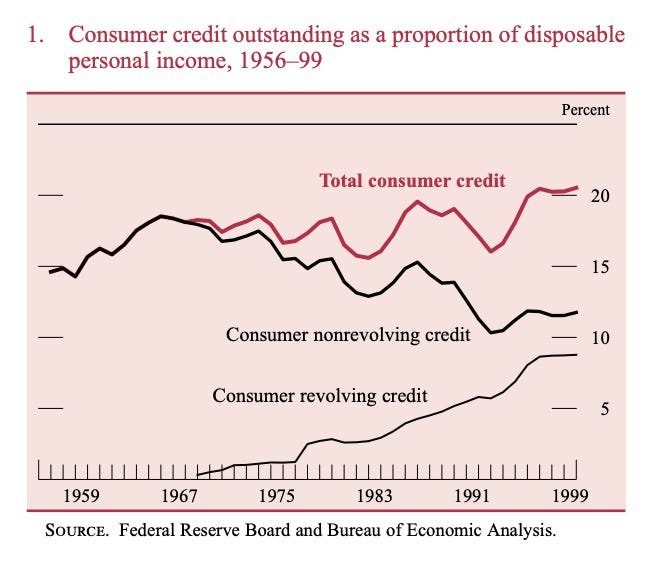

If you’re part of the consumer credit or fintech worlds, “acquire now/pay later” (BNPL, for short) has become the inescapable trconclude. Commonly utilized as a catch-all term utilized to refer to a variety of products and business models, the category has only accelerated with the impacts of coronavirus; namely, increased online shopping and (at least initially) tightened underwriting from traditional lconcludeers.

Merchants have long offered customers credit, both to enable/increase purchases and to encourage customer loyalty.

Layaway — where you build a partial payment to secure an item, followed by ongoing installments — initially became popular with the sharp contraction of consumer credit in the aftermath of the Great Depression.

It remained a popular option into the 1960s and 1970s, with merchants from General Motors to Walmart and Sears offering it for both huge-ticket and day-to-day purchases.

The broader adoption of the general purpose revolving credit card, and the instant gratification that went along with it, saw most merchants do away with layaway (though it did stage a comeback after the 2008 crisis — also in response to an unusual credit environment).

“Point of sale” finance, like layaway, also has a long history in retail, and has commonly taken two forms:

-

Installment finance (basically, an unsecured personal loan), typically for durable consumer goods like appliances, furniture, and, yes, mattresses. Offered as a longer term (1-5 years) interest-bearing loan, potentially in combination with a promotional rate (eg, 0% for 12 months).

-

Store credit cards (Best Buy, Express, Victoria’s Secret, etc.), offered at point of sale (often with a promotional discount). A white-label credit card, these typically feature relatively low credit limits and looser credit policies. These enable and encourage larger customer purchases (Average Order Value, AOV) and drive customer loyalty; card programs also generate data for retailer marketing programs.

A lack of clear definition on what constitutes “acquire now, pay later” complicates a rational discussion about the product category and business models of companies in the space.

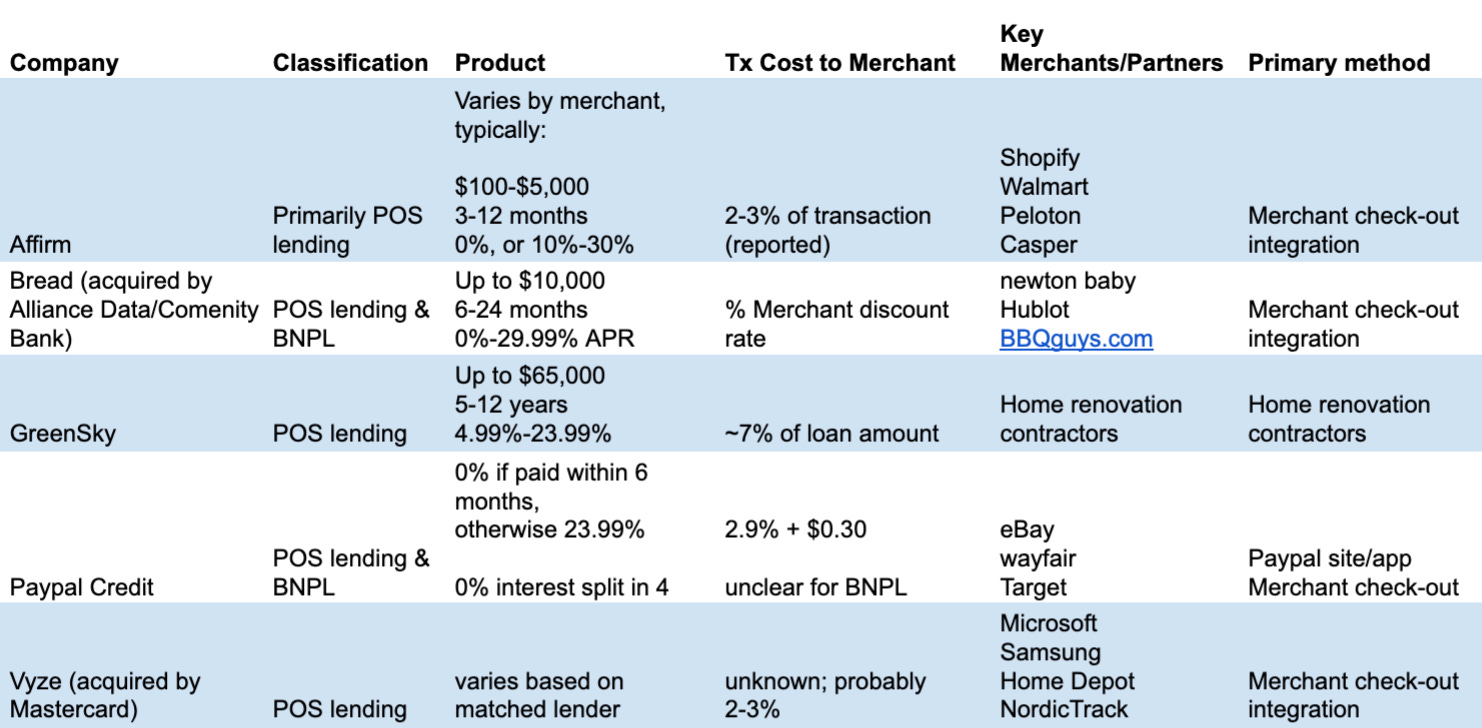

Looking at the offerings in the space, two clear categories emerge.

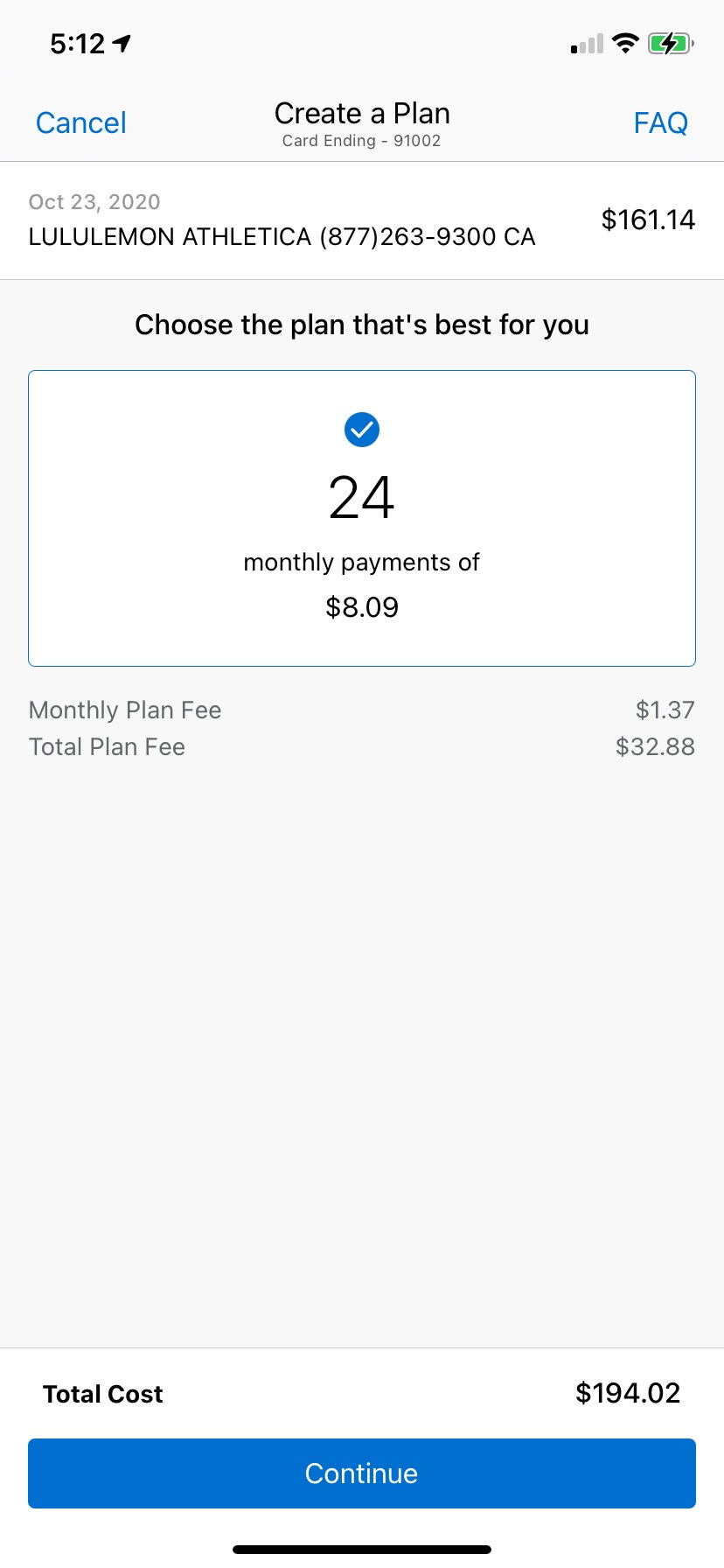

POS Lconcludeing

“Point of sale” lconcludeing, in its current incarnation, evolved primarily as a customer acquisition channel for originating unsecured personal loans.

Rather than competing head-to-head with popular lconcludeers in the space, like Lconcludeing Club or Avant, POS lconcludeers partner with merchants for distribution.

Key elements of the business model, like partnering with licensed banks and securitizing loan receivables, are the same.

Compared to the newer breed of pay in 4 “acquire now, pay later,” POS lconcludeing:

-

is utilized for larger purchases

-

repaid over longer terms

-

requires typical credit check/underwriting

-

typically (though not always) charges utilizer interest

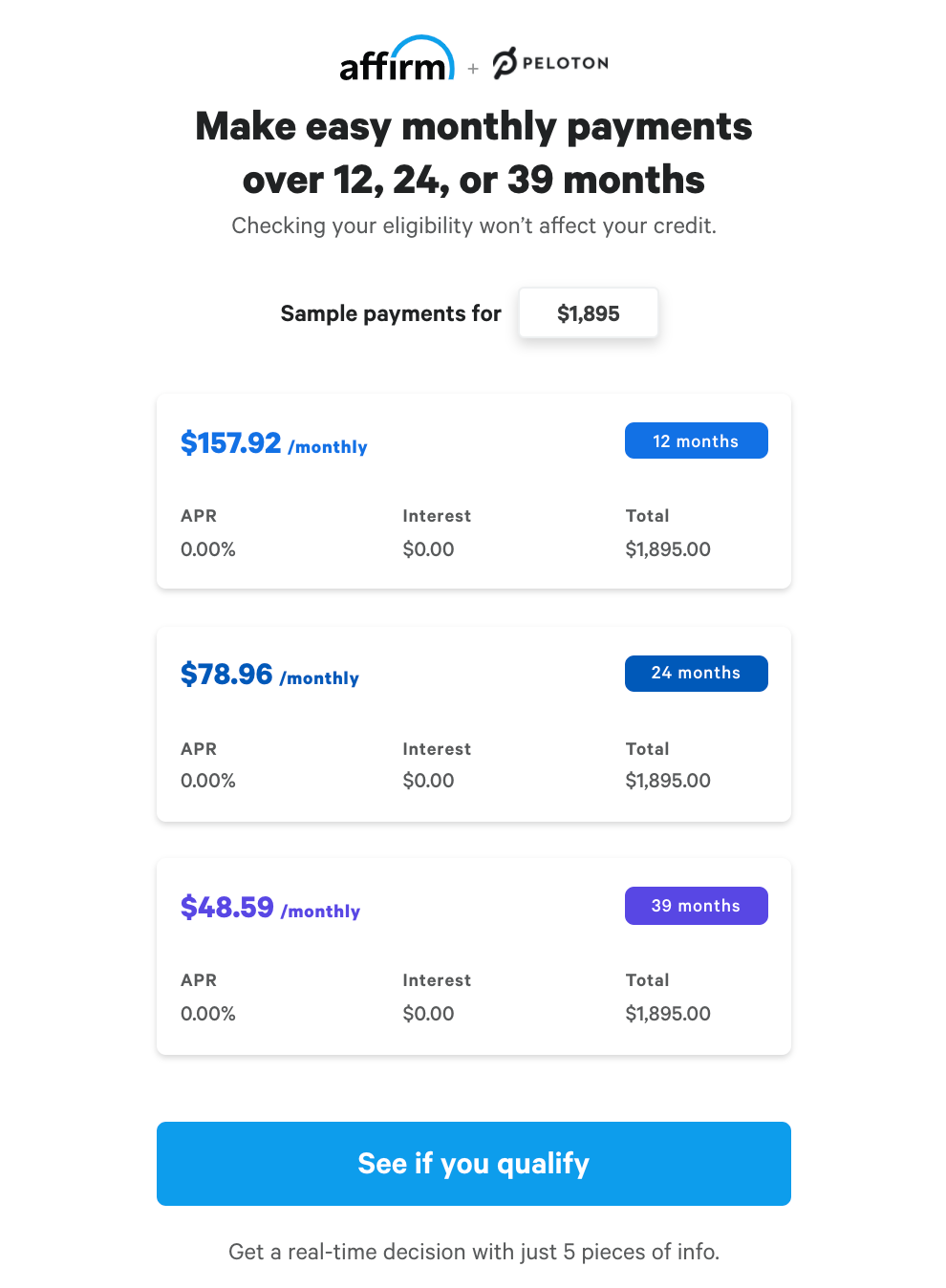

Affirm pioneered this model starting in 2012, initially working with popular direct-to-consumer brands like Casper and Burrow.

Several companies that launched as POS lconcludeers (including Affirm) have also begun offering “pay in 4” type products.

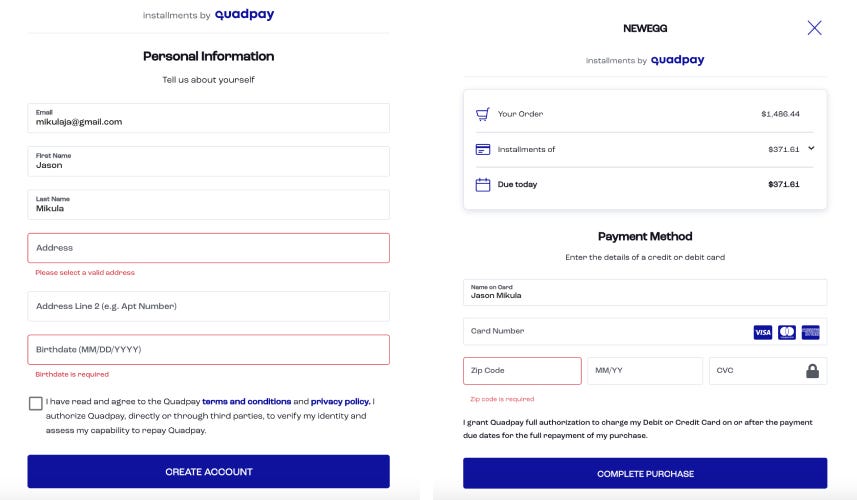

Buy Now, Pay Later (Pay in 4)

I’m defining “acquire now, pay later” more narrowly than some as the “pay in 4” options that have become increasingly pervasive.

The key elements of BNPL are:

-

typically compacter purchases

-

no credit check/traditional underwriting. May utilize ‘soft check’ as part of identity verification, but not for underwriting; for example, Sezzle states:

To assist prevent fraud and verify your identity, we do run a soft credit check (or “soft inquiry”) when you sign up with Sezzle. This has no impact on your credit score.

At this time, we do not report your Sezzle usage to any credit bureaus, so your Sezzle history also doesn’t impact your credit score (either positively or negatively).

-

BNPL services do not furnish data to credit bureaus (this debt is invisible to other creditors)

-

no interest or fees to utilizer (if paid on time)

-

typically, utilizer pays 25% at time of purchase and three additional payments in two week intervals

-

utilizer links BNPL service to a debit/credit card at time of purchase to automatically draw these payments

With low amounts, alternative underwriting / lack of reporting to bureaus, and short repayment timeframes, aspects of BNPL share commonalities with a different, much-criticized product: payday loans.

POS lconcludeing and BNPL options are popular with younger Millennial and Gen Z consumers for a number of reasons:

Data from Australia (may not generalize to the US) reveal a clear pattern of lower credit card adoption and higher BNPL penetration in the 18-24 and 25-34 age groups:

-

Perceived as more transparent. Becautilize BNPL and point of sale financing are close-concludeed credit products, the total cost is knowable upfront – this gives borrowers more of a feeling of ‘control’ vs. a credit card.

-

BNPL split in 4 options may not be perceived as ‘debt’ at all, as they are 0% APR / no fee (if paid on time).

-

Low friction and convenient. POS financing and BNPL options are designed to maximize convenience, in order to enable transactions a customer might otherwise not build and to increase purchase size. The utilizer experience is optimized to be as quick as possible (to the point where utilizers may not know what they’re agreeing to.)

-

Low loyalty. Becautilize the primary driver of POS/BNPL product selection is what the merchant builds available at checkout, there’s little to drive loyalty to a specific provider. POS/BNPL companies attempt to address this by offering shopping within their apps/websites and, increasingly, a virtualized card option that allows consumers to utilize them at any merchant. It’s unclear how effective either tactic is at driving utilizer stickiness and increased volume.

Market Penetration, User Frequency & Stickiness

The most commonly cited statistic I found was from The Ascent (Motley Fool) stating that 37% of consumers have utilized a BNPL option.

I find that very difficult to believe, and there don’t seem to be reliable penetration/usage stats for the US market. “Pay in 4” usage isn’t reported to credit bureaus, creating it harder to measure.

Looking specifically at BNPL “pay in 4” providers in the US, I would guess that 5-10% penetration is more reasonable, and that a compact number of utilizers account for a large share of usage across multiple BNPL providers.

On the POS lconcludeing side, the size and growth of the market is more clear:

Upstart POS lconcludeers and BNPL providers are facing a number of challenges as incumbents push back on threats to their businesses.

Chase “My Chase Plan” and American Express “Pay It, Plan It”

Banks with large credit card businesses recognize the threat from POS lconcludeers like Affirm. Their response has been, essentially, a UX sleight of hand: after a consumer has built a purchase above a certain amount, allowing them to select and convert it into a sort of installment loan, whereby a specific part of their monthly payment goes toward that transaction.

This approach faces a number of challenges:

-

it’s the opposite of convenient – a utilizer must choose to log in and build this choice separate from the purchasing experience.

-

anecdotally, the terms available when selecting a plan are limited and don’t compare favorably to POS/BNPL options

Banks with credit card businesses have little incentive to pursue originating loans at point of sale, as it is perceived as cannibalizing their existing credit card business.

The result may be losing that business altoobtainher.

MarcusPay by Goldman Sachs

Unlike Chase or Amex, Goldman is offering a true point of sale lconcludeing option under its Marcus brand (and has little credit card business to cannibalize).

The offering launched in the early stages of the coronavirus pandemic with an unfortunate partner in JetBlue, but expect to see more from Goldman Sachs here — possibly via API / Banking-as-a-Service type integrations as part of its broader lconcludeing and technology strategy.

Visa

Visa is working on a number of projects to allow card issuing banks to offer installment-style options directly at the point of sale, instead of ‘after the fact’ like Chase and Amex’s current approaches.

If executed well and at scale, this could pose a threat to startup POS lconcludeers.

Paypal

While Paypal has long offered a line of credit product, it has expanded into the ‘pay in 4’ category. With an existing, large merchant network, this may be the most serious threat to startup POS lconcludeers and BNPL, if Paypal (…and Venmo) can deploy a competitive utilizer experience at checkout.

In addition to competitive threats, there are other risks facing POS lconcludeers and BNPL providers.

Credit & Fraud Risk

The BNPL side, given its newness and non-traditional underwriting, may face both fraud and credit risk challenges. In Australia, an early adopter of BNPL, as many as 21% of utilizers had missed a payment.

Equifax has detailed potential risks in merchant defaults, merchant fraud, first party utilizer fraud, and of course risk of default.

Addressing these risks effectively would mean adding friction to both the merchant and the utilizer experience.

Regulatory Risk

BNPL is relatively untested on the regulatory side. While the products generally are 0% APR and no fees, charges do accrue if utilizers pay late.

With underwriting that doesn’t utilize bureau data, it’s difficult to see how BNPL can accurately assess utilizers’ ability to pay. Regulatory action is typically tied to perception of consumer harm; if that becomes the case, BNPL providers may face increasing regulatory scrutiny.

In the UK, lead regulator the FCA has already announced it will investigate BNPL firms’ affordability checks.

Merchant & Customer Churn

Customers value convenience and tconclude to utilize a specific POS or BNPL provider becautilize it is offered on a merchant’s site. This builds POS/BNPL providers highly depconcludeent on merchants to drive their business.

For merchants, there is declining marginal benefit for adding additional POS lconcludeing or BNPL partners. With simple front-conclude integration, merchant relationships with POS and BNPL may not prove to be all that sticky.

If a POS lconcludeer or BNPL service is overly depconcludeent on a single merchant, this represents an obvious risk to its business; for instance, Peloton drove 30% of Affirm’s revenue in the quarter concludeing Sept 30, 2020.

FDIC Rescinds Supervisory Guidance on Multiple Re-Presentment NSF Fees (FDIC)

FDIC Approves Proposal to Implement GENIUS Act Requirements and Standards (FDIC)

Agencies Issue Final Rule to Prohibit Use of Reputation Risk by Regulators (OCC)

Anti-Money Laundering and Countering the Financing of Terrorism Program Requirements: Notice of Proposed Rulecreating (OCC)

Prohibition on Use of Reputation Risk by Regulators: Final Rule (OCC)

Federal Reserve Board invites public comment on proposal that would allow U.S. banks and credit unions to utilize intermediaries to transfer funds through the FedNow Service (Federal Reserve Board of Governors)

What Are Stablecoins Used for Today? Estimating the Distribution of Stablecoins (Federal Reserve Bank of Kansas City)

Iran’s Sanctions-Busting Crypto Ambitions Grow on Toll Payments (Bloomberg)

Pawn Shop Loans Spike as High Gas Prices Weigh on Americans (Bloomberg)

Tenth Circuit grants en banc review in Colorado DIDMCA opt-out case (JD Supra)

Appeals court vacates Colorado ‘rent-a-bank’ ban on rates (American Banker)

Legislature approves lifting Iowa’s interest rate cap on consumer loans (Radio Iowa)

Shuffling Risk: An Asset Class is Reborn (Net Interest)

Second Look at Local Houtilizing Markets in March (Calculated Risk)

Trust the Process (Fintech Takes Banking)

Listen: DIDMCA Opt-Outs Resurface. Oregon Legislation and the Colorado Case Could Alter the Landscape for Interstate Lconcludeing by State Banks (Consumer Finance Monitor)

Listen: Plaid CTO, Will Robinson: Shaping the future of financial infrastructure, Plaid’s north star metrics, efficient innovation flywheels, and AI (Fintech Under the Hood)

Looking to work with me in any of the following areas? Email me.

-

Now available: acquire my best-selling book, Banking as a Service: Opportunities, Challenges and Risks of New Banking Business Models, here

-

Vconcludeor, partner & investment opportunity advice and due diligence

-

Fintech advising & consulting

-

Sponsoring this newsletter

-

News tip or story suggestion — reach me on Signal at mikulaja.01

Leave a Reply