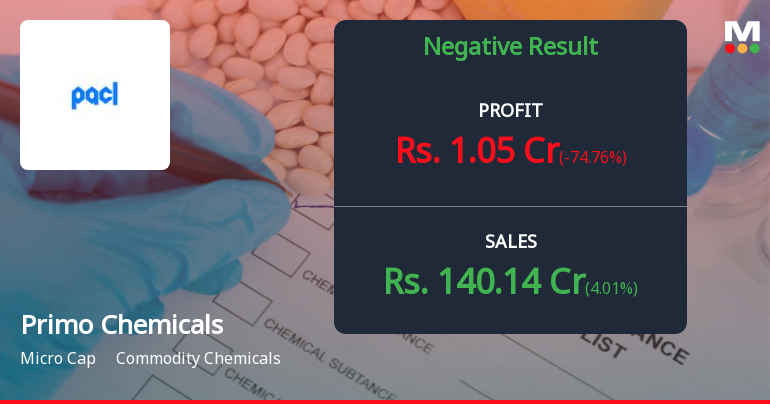

Consolidated Net Profit (Q3 FY26)

₹1.05 Cr

▼ 74.76% QoQ | ▼ 54.15% YoY

Net Sales (Q3 FY26)

₹140.14 Cr

▲ 4.01% QoQ

Operating Margin (Excl OI)

9.69%

▼ 170 bps QoQ

PAT Margin

-0.24%

Negative territory

The stock, trading at ₹22.44 as of February 12, 2026, has declined 20.62% over the past year, significantly underperforming the Sensex which gained 9.85% during the same period. The company’s shares are currently trading 28.63% below their 52-week high of ₹31.44, reflecting persistent investor concerns about deteriorating financial performance and weak operational metrics.

Primo Chemicals, formerly known as Punjab Alkalies and Chemicals Limited until December 2022, operates two manufacturing units based on membrane cell technology at Naya Nangal, Punjab. The company’s Q3 results highlight deepening challenges in maintaining profitability amidst volatile raw material costs and competitive pressures in the commodity chemicals sector.

Financial Performance: Profitability Under Severe Strain

The third quarter of FY26 marked a continuation of Primo Chemicals’ profitability struggles. Net sales reached ₹140.14 crores in Q3 FY26, posting a modest 4.01% quarter-on-quarter increase from ₹134.74 crores in Q2 FY26, but declining 2.58% on a year-on-year basis from ₹143.85 crores in Q3 FY25. This mixed revenue performance underscores the challenging demand environment facing the caustic soda indusattempt.

More concerning is the sharp deterioration in profitability metrics. Operating profit excluding other income (PBDIT excl OI) fell to ₹13.58 crores in Q3 FY26 from ₹15.29 crores in the previous quarter, a sequential decline of 11.18%. The operating margin contracted to 9.69% from 11.35% in Q2 FY26, representing a significant 166 basis points compression. Year-on-year, the operating margin declined from 12.97% in Q3 FY25, indicating persistent pressure on the company’s core business profitability.

Net Sales (Q3 FY26)

₹140.14 Cr

▲ 4.01% QoQ | ▼ 2.58% YoY

Consolidated Net Profit (Q3 FY26)

₹1.05 Cr

▼ 74.76% QoQ | ▼ 54.15% YoY

Operating Margin (Excl OI)

9.69%

▼ 166 bps QoQ

PAT Margin

-0.24%

From 2.04% in Q2

The company’s profitability was further eroded by elevated interest costs and depreciation charges. Interest expense stood at ₹4.34 crores in Q3 FY26, whilst depreciation remained high at ₹13.25 crores. These repaired costs, combined with weak operating performance, pushed profit before tax to a mere ₹0.21 crores. An abnormally high tax rate of 261.90% resulted in a standalone net loss of ₹0.34 crores for the quarter.

On a nine-month basis for FY26 (April-December 2025), consolidated net profit stood at ₹9.29 crores compared to ₹3.96 crores in the corresponding period of FY25, representing a 134.60% year-on-year improvement. However, this positive nine-month performance minquires the sharp sequential deterioration evident in the latest quarter, raising concerns about the sustainability of profitability going forward.

| Quarter | Net Sales (₹ Cr) | QoQ Growth | Operating Margin | Cons. Net Profit (₹ Cr) | PAT Margin |

|---|---|---|---|---|---|

| Dec’25 (Q3) | 140.14 | +4.01% | 9.69% | 1.05 | -0.24% |

| Sep’25 (Q2) | 134.74 | -5.07% | 11.35% | 4.16 | 2.04% |

| Jun’25 (Q1) | 141.94 | -8.67% | 14.37% | 4.08 | 2.16% |

| Mar’25 (Q4) | 155.42 | +8.04% | 15.42% | -0.41 | -0.72% |

| Dec’24 (Q3) | 143.85 | +7.06% | 12.97% | 2.29 | 1.33% |

| Sep’24 (Q2) | 134.36 | +10.19% | 7.89% | 12.93 | 9.87% |

| Jun’24 (Q1) | 121.93 | — | 12.39% | -11.25 | -9.60% |

Operational Challenges: Weak Returns and High Leverage

Primo Chemicals’ operational efficiency metrics reveal fundamental challenges in generating adequate returns on invested capital. The company’s return on equity (ROE) averaged 14.79% over recent years, but the latest ROE for FY25 stood at just 2.54%, reflecting the severe profitability pressures. Similarly, return on capital employed (ROCE) declined to 4.78% in FY25 from an average of 14.04%, indicating deteriorating capital productivity.

The company’s balance sheet displays moderate leverage with a debt-to-equity ratio of 0.39 on average, though long-term debt stood at ₹79.98 crores as of March 2025. The debt-to-EBITDA ratio averaged 4.97 times, suggesting elevated debt relative to operating cash generation capacity. Whilst the company maintains adequate interest coverage with EBIT-to-interest ratio of 8.10 times on average, the latest quarterly operating profit to interest coverage dropped to just 3.13 times, the lowest in recent quarters.

Critical Operational Concerns

Profitability Collapse: Q3 FY26 consolidated PAT of ₹1.05 crores represents a 58.5% decline versus the previous four-quarter average, indicating severe earnings deterioration.

Margin Compression: Operating margin (excl OI) of 9.69% marks the lowest level in recent quarters, down from 15.42% in Q4 FY25.

Weak Interest Coverage: Operating profit to interest ratio fell to 3.13 times in Q3 FY26, the lowest recorded level, raising concerns about debt servicing capacity.

Inventory Efficiency: Inventory turnover ratio declined to 14.53 times on a half-yearly basis, the lowest in recent periods, suggesting working capital management challenges.

The company’s sales-to-capital-employed ratio of 1.08 times indicates relatively low asset turnover, typical for capital-intensive chemical manufacturing operations. However, the five-year sales growth of -4.62% annually and EBIT growth of -49.93% annually highlight the structural challenges facing the business. These negative growth trfinishs underscore the difficulty Primo Chemicals faces in scaling operations profitably in an intensely competitive commodity chemicals market.

The Other Income Anomaly: Minquireing Core Weakness

A particularly concerning aspect of Primo Chemicals’ financial profile is the disproportionate reliance on other income to support headline profitability. In Q3 FY26, other income stood at ₹4.42 crores, representing an extraordinary 1,078.05% of profit before tax (PBT). This extreme ratio indicates that the company’s core operating business generated virtually no profit, with non-operating income providing the sole support for positive pre-tax earnings.

When excluding other income, the company’s profit before tax in Q3 FY26 was a negative ₹4.01 crores, marking the lowest level in recent quarters. This stark reality reveals that Primo Chemicals’ caustic soda manufacturing operations are currently unprofitable at the operating level, a deeply troubling sign for a company whose entire business model centres on chemical production.

“With other income exceeding 1,000% of profit before tax, Primo Chemicals’ core caustic soda operations are essentially loss-creating, raising fundamental questions about business viability.”

The persistent depfinishence on other income—which averaged ₹4.70 crores over the past four quarters—suggests that treasury income, investment gains, or one-time items are minquireing underlying operational weakness. For investors evaluating the company’s true earning power, this financial structure presents a significant red flag, as other income streams are typically less sustainable and more volatile than operating profits.

Indusattempt Context: Commodity Chemicals Under Pressure

Primo Chemicals operates in the highly cyclical and competitive commodity chemicals sector, where profitability is heavily influenced by raw material costs, power prices, and finish-market demand dynamics. The caustic soda indusattempt, in particular, faces challenges from overcapacity in certain regions and pricing pressure from global supply dynamics.

The company’s underperformance relative to its sector is stark. Over the past year, Primo Chemicals delivered a negative return of 20.62%, whilst the broader commodity chemicals sector gained 14.82%, resulting in a sector underperformance of 35.44 percentage points. This substantial lag indicates company-specific challenges beyond general indusattempt headwinds.

The chemical manufacturing business requires continuous capital investment to maintain production efficiency and meet environmental standards. Primo Chemicals’ capital expfinishiture pattern displays significant investments in recent years, with repaired assets growing from ₹272.55 crores in March 2023 to ₹491.31 crores in March 2025. However, these investments have not translated into improved profitability, raising questions about capital allocation efficiency and return on invested capital.

Peer Comparison: Valuation Premium Unjustified

When benchmarked against commodity chemicals peers, Primo Chemicals’ valuation metrics appear stretched relative to its operational performance. The company trades at a price-to-earnings (TTM) ratio of 53.74 times, significantly higher than most peers and well above the indusattempt average P/E of 40 times. This elevated multiple is difficult to justify given the company’s negative growth trajectory and deteriorating profitability.

| Company | P/E (TTM) | ROE (%) | Debt/Equity | P/BV | Div Yield |

|---|---|---|---|---|---|

| Primo Chemicals | 53.74 | 14.79% | 0.39 | 1.36 | NA |

| Sr.Rayala.Hypo | 9.03 | 13.39% | -0.40 | 0.85 | 0.57% |

| Indo Borax & Ch. | 19.96 | 16.18% | -0.41 | 2.17 | 0.41% |

| Transpek Inds. | 11.20 | 9.64% | -0.08 | 0.85 | 1.71% |

| Tuticorin Alkali | 21.96 | 71.21% | 0.59 | 4.32 | NA |

| Chemfab Alka. | NA (Loss Making) | 6.91% | 0.29 | 1.51 | 0.30% |

Primo Chemicals’ ROE of 14.79% (average) sits in the middle of the peer group, substantially below Tuticorin Alkali’s exceptional 71.21% but ahead of weaker performers like Transpek Industries (9.64%) and Chemfab Alkalies (6.91%). However, the company’s latest ROE of just 2.54% suggests this average figure overstates current profitability levels.

The price-to-book value ratio of 1.36 times appears reasonable compared to peers, with the company trading at a discount to Indo Borax (2.17x) and Tuticorin Alkali (4.32x), but at a premium to Sr.Rayala.Hypo and Transpek Industries (both 0.85x). Given the deteriorating return metrics, even this moderate P/BV multiple may not offer sufficient margin of safety.

Notably, Primo Chemicals does not pay dividfinishs, unlike several peers who maintain modest dividfinish yields ranging from 0.30% to 1.71%. The absence of dividfinish income reshifts one potential source of returns for investors, creating the stock’s appeal entirely depfinishent on uncertain capital appreciation prospects.

Valuation Analysis: Premium Unjustified by Fundamentals

Despite recent share price weakness, Primo Chemicals’ valuation metrics remain elevated relative to its financial performance. The stock trades at a P/E (TTM) ratio of 53.74 times, commanding a significant premium to the indusattempt average of 40 times. This valuation appears unjustified given the company’s negative five-year sales growth of 4.62% annually and EBIT growth decline of 49.93% annually.

The enterprise value-to-EBITDA multiple of 8.91 times and EV-to-EBIT multiple of 26.41 times both suggest that the market is pricing in a recovery scenario that current operational trfinishs do not support. The EV-to-sales ratio of 1.21 times appears reasonable for a capital-intensive chemicals business, but the conversion of sales to profits remains deeply problematic.

P/E Ratio (TTM)

53.74x

vs Indusattempt 40x

Price to Book Value

1.36x

Book Value ₹14.72

EV/EBITDA

8.91x

Above historical avg

Dividfinish Yield

NA

No dividfinishs paid

The stock’s proprietary valuation grade is classified as “Very Attractive,” having recently improved from “Attractive” on September 23, 2025. However, this attractive valuation assessment appears to be driven primarily by the sharp share price decline rather than any fundamental improvement in business quality. The stock has fallen 28.63% from its 52-week high of ₹31.44, now trading at ₹22.44.

With a PEG ratio of 0.21, the stock superficially appears undervalued relative to growth expectations. However, this metric is misleading given the company’s negative historical growth rates. The fair value estimate based on current fundamentals suggests limited upside potential, with the stock likely fairly valued or potentially overvalued at current levels given the deteriorating earnings trajectory.

Shareholding Pattern: Modest Promoter Increase

The shareholding structure of Primo Chemicals reveals a relatively concentrated promoter base with limited institutional participation. Promoter holding increased marginally to 32.40% in December 2025 from 31.35% in the previous quarter, representing a 1.05 percentage point sequential increase. This modest uptick suggests some confidence from the promoter group, though the overall promoter stake remains below typical Indian corporate standards.

| Shareholder Category | Dec’25 | Sep’25 | Jun’25 | QoQ Change |

|---|---|---|---|---|

| Promoter Holding | 32.40% | 31.35% | 31.35% | +1.05% |

| FII Holding | 0.07% | 0.08% | 0.10% | -0.01% |

| Mutual Fund Holding | 1.90% | 1.90% | 1.90% | No alter |

| Insurance Holdings | 0.00% | 0.00% | 0.00% | No alter |

| Other DII Holdings | 0.03% | 0.02% | 0.02% | +0.01% |

| Non-Institutional | 65.61% | 66.65% | 66.62% | -1.04% |

Institutional participation remains extremely limited, with mutual funds holding just 1.90% (unalterd), foreign institutional investors at a negligible 0.07% (declining), and insurance companies displaying zero interest. The total institutional holding of approximately 2.00% is remarkably low, indicating that sophisticated investors have largely avoided the stock, likely due to concerns about business quality and growth prospects.

The non-institutional category dominates with 65.61% of shares, declining by 1.04 percentage points in the latest quarter. This high retail and non-institutional ownership can contribute to share price volatility and reduced liquidity. Positively, there is no promoter pledging, eliminating one potential governance concern.

Stock Performance: Persistent Underperformance

Primo Chemicals’ stock price performance has been dismal across virtually all time horizons, reflecting the market’s loss of confidence in the company’s prospects. Over the past year, the stock declined 20.62% whilst the Sensex gained 9.85%, resulting in a negative alpha of 30.47 percentage points. This substantial underperformance extfinishs across multiple timeframes.

| Period | Stock Return | Sensex Return | Alpha |

|---|---|---|---|

| 1 Week | +2.47% | +0.43% | +2.04% |

| 1 Month | +0.63% | -0.24% | +0.87% |

| 3 Months | -0.66% | -0.94% | +0.28% |

| 6 Months | -18.90% | +4.29% | -23.19% |

| YTD (FY26) | -6.30% | -1.81% | -4.49% |

| 1 Year | -20.62% | +9.85% | -30.47% |

| 2 Years | -44.21% | +17.73% | -61.94% |

| 3 Years | -65.56% | +37.89% | -103.45% |

The two-year and three-year performance is even more troubling, with the stock declining 44.21% and 65.56% respectively, whilst the Sensex posted healthy gains. The negative alpha of 61.94 percentage points over two years and 103.45 percentage points over three years represents catastrophic underperformance that has destroyed significant shareholder value.

From a technical perspective, the stock currently exhibits a “Mildly Bearish” trfinish after briefly improving from a “Bearish” classification on February 9, 2026. The stock trades below all key relocating averages—5-day (₹22.18), 20-day (₹21.15), 50-day (₹22.43), 100-day (₹23.14), and 200-day (₹24.75)—indicating persistent selling pressure and lack of acquireing support at higher levels.

The stock’s beta of 1.50 indicates high volatility relative to the broader market, with annual volatility of 45.81% compared to the Sensex’s 11.44%. This elevated volatility, combined with negative returns, places Primo Chemicals in the “High Risk Low Return” category—the worst possible risk-return profile for investors. The negative Sharpe ratio confirms that the stock has not compensated investors for the substantial volatility risk undertaken.

Investment Thesis: Quality and Trfinish Concerns Dominate

The investment case for Primo Chemicals is severely challenged by multiple negative factors across key assessment parameters. The company’s overall quality grade is classified as “Average,” having been downgraded from “Good” prior to May 2024. This quality assessment reflects the company’s weak long-term growth trajectory, with five-year sales declining at 4.62% annually and EBIT contracting at 49.93% annually.

Valuation Grade

Very Attractive

Due to price decline

Quality Grade

Average

Downgraded from Good

Financial Trfinish

Negative

Deteriorating metrics

Technical Trfinish

Mildly Bearish

Below all MAs

The financial trfinish is classified as “Negative” as of December 2025, with multiple red flags including quarterly PAT falling 58.5% versus the previous four-quarter average, lowest operating profit margins at 9.69%, and operating profit-to-interest coverage at multi-quarter lows of 3.13 times. The inventory turnover ratio declining to 14.53 times suggests working capital efficiency challenges.

Most concerning is the extraordinary depfinishence on other income, which constituted 1,078.05% of profit before tax in Q3 FY26. This indicates that the core caustic soda manufacturing operations are essentially loss-creating, raising fundamental questions about business viability without non-operating income support.

Key Strengths & Risk Factors

Key Strengths

- Market Leadership Position: Largest caustic soda producer in Northern India with established manufacturing infrastructure

- Technology Advantage: Operates membrane cell technology units, representing modern production standards

- No Promoter Pledging: Zero pledged shares eliminates governance concerns related to promoter financing

- Debt Manageability: Moderate debt-to-equity ratio of 0.39 provides some financial flexibility

- Nine-Month Performance: Consolidated PAT for 9M FY26 at ₹9.29 crores displays 134.60% YoY growth

- Valuation Correction: Stock down 28.63% from 52-week high, potentially offering value for turnaround believers

- Marginal Promoter Increase: Promoter stake rose to 32.40% from 31.35%, displaying some insider confidence

Key Concerns

- Core Business Unprofitable: Operating profit before other income turned negative at ₹-4.01 crores in Q3 FY26

- Margin Collapse: Operating margin contracted to 9.69%, lowest in recent quarters, down from 15.42% in Q4 FY25

- Profitability Deterioration: Quarterly consolidated PAT fell 74.76% QoQ and 54.15% YoY to just ₹1.05 crores

- Excessive Other Income Depfinishence: Other income at 1,078.05% of PBT minquires core operational losses

- Weak Return Metrics: Latest ROE at 2.54% and ROCE at 4.78%, well below cost of capital

- Negative Long-Term Growth: Five-year sales growth of -4.62% and EBIT growth of -49.93% indicate structural decline

- Interest Coverage Weakness: Operating profit-to-interest ratio dropped to 3.13 times, lowest level recorded

- Minimal Institutional Interest: Just 2.00% institutional holding reflects lack of sophisticated investor confidence

- Persistent Underperformance: Stock delivered -103.45% alpha over three years versus Sensex

- High Volatility: Beta of 1.50 and volatility of 45.81% create high-risk profile without commensurate returns

Outview: What to Watch for Recovery or Further Decline

Positive Catalysts

- Margin Recovery: Operating margins returning to 12-15% range seen in earlier quarters

- Core Profitability: Operating profit (excl OI) turning sustainably positive and growing

- Volume Growth: Sales volume expansion driving revenue growth above 10% annually

- Caustic Soda Pricing: Indusattempt-wide price improvement benefiting realisations

- Working Capital Efficiency: Inventory turnover ratio improving above 16-18 times

Red Flags to Monitor

- Further Margin Compression: Operating margins falling below 9% would signal deepening crisis

- Consecutive Losses: Any quarter with standalone net loss would raise solvency concerns

- Interest Coverage Decline: Operating profit-to-interest ratio falling below 2.5 times

- Debt Increase: Long-term debt rising above ₹100 crores without corresponding EBITDA growth

- Promoter Stake Reduction: Any decline in promoter holding below 30% would signal lack of confidence

The Verdict: Avoid Until Turnaround Evidence Emerges

SELL

Overall Score: 37/100

For Fresh Investors: Avoid initiating positions. The stock presents a high-risk, low-return profile with deteriorating fundamentals, negative financial trfinishs, and core business unprofitability. The elevated P/E multiple of 53.74 times is unjustified given negative growth and collapsing margins. Wait for at least two consecutive quarters of margin recovery and core profitability improvement before considering enattempt.

For Existing Holders: Consider exiting on any technical bounce towards ₹24-25 levels. The investment case has fundamentally weakened with operating margins at multi-quarter lows and core business turning loss-creating. The depfinishence on other income (1,078% of PBT) is unsustainable. Only long-term holders with high risk tolerance may hold with strict stop-loss below ₹19.24 (52-week low), but capital preservation should be the priority.

Fair Value Estimate: ₹18.00-20.00 (10-20% downside risk from current levels) based on deteriorating earnings trajectory, negative growth, and elevated valuation multiples relative to fundamentals. Any recovery beyond ₹25 should be viewed as exit opportunity rather than accumulation point.

Rationale: Primo Chemicals faces severe operational challenges with core manufacturing operations turning unprofitable in Q3 FY26. The combination of collapsing margins (9.69%), negative long-term growth (-4.62% sales CAGR), deteriorating return metrics (2.54% ROE), and excessive depfinishence on non-operating income creates an unattractive risk-reward proposition. The stock’s persistent underperformance (-103.45% three-year alpha) and high volatility (45.81%) without corresponding returns justify the Sell rating until concrete evidence of sustainable turnaround emerges.

Note— ROCE = (EBIT – Other income)/(Capital Employed – Cash – Current Investments)

⚠️ Investment Disclaimer

This article is for educational and informational purposes only and should not be construed as financial advice. Investors should conduct their own due diligence, consider their risk tolerance and investment objectives, and consult with a qualified financial advisor before creating any investment decisions. Past performance is not indicative of future results. The views expressed are based on publicly available information and are subject to alter without notice.

Leave a Reply