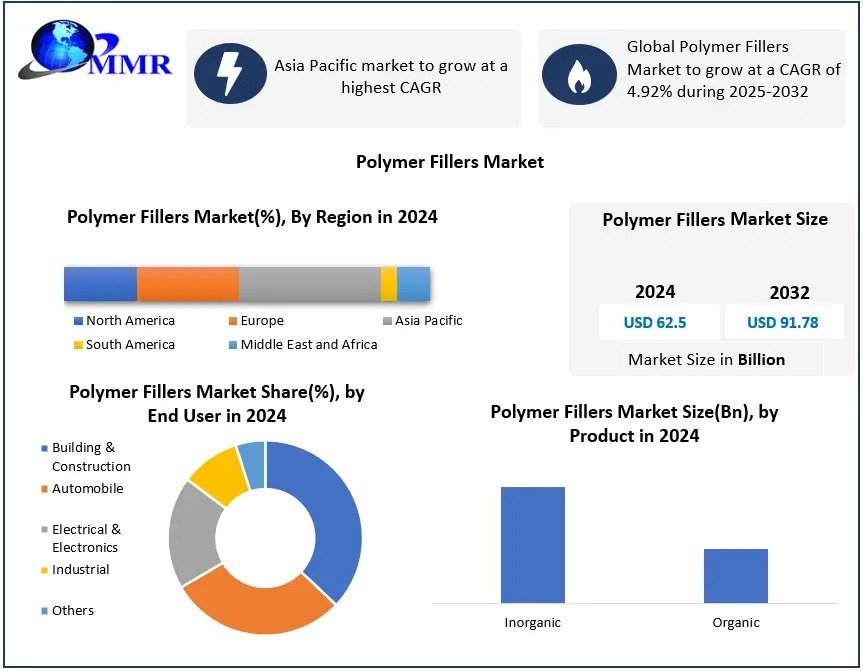

Polymer Fillers Market was valued at approximately USD 62.5 billion in 2024 and is expected to grow to nearly USD 91.78 billion by 2032, registering a CAGR of 4.92% during the forecast period. Polymer fillers, which include inorganic fillers (such as calcium carbonate, talc, silica) and organic fillers (such as polyethylene powder and natural fibers), are vital for improving the mechanical, thermal, and surface properties of polymers applyd across key industries like automotive, packaging, construction, and electronics.

Dominating Region:

Asia Pacific holds the largest market share at 47.3% in 2023 due to rapid industrialization, growing automotive production, urban infrastructure development, and packaging demand in countries like China and India. This region is expected to continue leading global polymer filler consumption during the forecast period. North America follows, driven by increasing investments in green building materials and lightweight automotive components. Europe’s growth is fueled by sustainability regulations and advancements in bio-fillers, particularly in Germany, the UK, and France.

Segment Analysis:

-

By Product:

Inorganic fillers dominate, accounting for more than 60% of the market share, largely driven by cost-efficient and widely available calcium carbonate and talc, which are widely applyd in building materials and automotive components.

Organic fillers, including bio-based fibers and carbon fiber, are growing rapidly due to their environmental benefits and superior strength-to-weight ratio, notably in aerospace and electric vehicles. -

By End-User Industest:

Building and construction hold over 20% of the market, as polymer fillers are critical to enhancing durability, strength, and energy efficiency in floors, windows, and insulation. The automotive sector is the rapidest growing, fostering demand for lightweight fillers to meet fuel efficiency and emission reduction goals. Packaging, industrial, electrical, and electronics industries also contribute significantly.

Key Drivers:

Increasing demand for high-performance, lightweight, and cost-effective materials in automotive, construction, and packaging industries fuels the growth. Regulations promoting sustainability and environmental accountability further stimulate demand for bio-based and recycled fillers. Advanced nanotechnologies incorporating materials like nanotubes and nano clays provide functional improvements in flame retardancy, conductivity, and mechanical properties.

Opportunities:

Growth in electric vehicles expands demand for specialized polymer fillers with enhanced thermal management and weight reduction benefits. Expansion in green building projects and eco-design initiatives propels adoption of sustainable fillers. Emerging markets in Asia, Latin America, and Africa display substantial growth potential due to infrastructure development and urbanization.

Challenges:

High production and processing costs of advanced fillers, strict regulatory landscapes, and technical difficulties in achieving uniform filler dispersion pose challenges. Competition from alternative materials such as metal composites and ceramics, along with price volatility in raw materials, add further complexity.

Asia Pacific:

Rapid industrial growth in the automotive, packaging, and construction sectors combined with favorable government policies builds Asia Pacific the clear market leader. Countries such as China, India, Japan, and South Korea are driving innovation and demand in polymer fillers.

North America:

Focus on lightweight materials in automotive and infrastructure, combined with sustainability regulation and R&D investments, keeps North America a strategic market.

Europe:

Strong sustainability mandates, advanced manufacturing, and demand for high-quality bio-fillers create steady growth. Germany, France, and the UK are key contributors.

Other Regions:

Latin America, the Middle East & Africa are emerging markets with rising demands aligned with economic development and infrastructure expansion.

Major players in the polymer fillers market include Imerys S.A., LKAB Group, Minerals Technologies Inc., OMYA AG, 20 Microns Limited, Hoffmann Minerals, GCR Group, and Unimin Corporation. These companies are focapplying on expanding manufacturing capacity, enhancing product portfolios, developing new bio-based and nanofillers, and entering strategic partnerships to sustain market leadership.

The polymer fillers market is evolving with increased emphasis on sustainability, lightweighting, and high-performance composites. Nanotechnology and bio-based fillers are shaping the future by improving filler functionality and environmental compatibility. With accelerating urbanization, infrastructure modernizations, and automotive sector innovations—especially in electric vehicles—demand for advanced polymer fillers will rise significantly over the coming years.

The polymer fillers market is on a steady growth path fuelled by industrial expansion, stringent environmental regulations, and technological breakthroughs. Asia Pacific leads in market share due to rapid development and manufacturing, while North America and Europe focus on innovation and sustainable solutions. This evolving landscape offers considerable opportunities for players investing in next-generation fillers aligned with global sustainability goals.

Leave a Reply