Introduction & Market Context

Integral Diagnostics Limited (ASX:IDX) presented its first-half fiscal 2026 results on February 24, 2026, revealcasing the substantial benefits of its Capitol Diagnostics merger with operating EBITDA surging 75.6% to $81.1 million. The Australian and New Zealand radiology provider reported revenue growth of 55.6% to $393.5 million, though the stock declined 1.67% to close at $2.40, suggesting investors may be digesting the integration costs and viewing for sustained organic growth momentum.

The presentation highlighted how the company has successfully integrated Capitol’s operations while expanding its network to 144 sites across both countries, positioning itself to capitalize on favorable regulatory alters including MRI deregulation and the National Lung Cancer Screening Program launching in July 2025.

Financial Performance Highlights

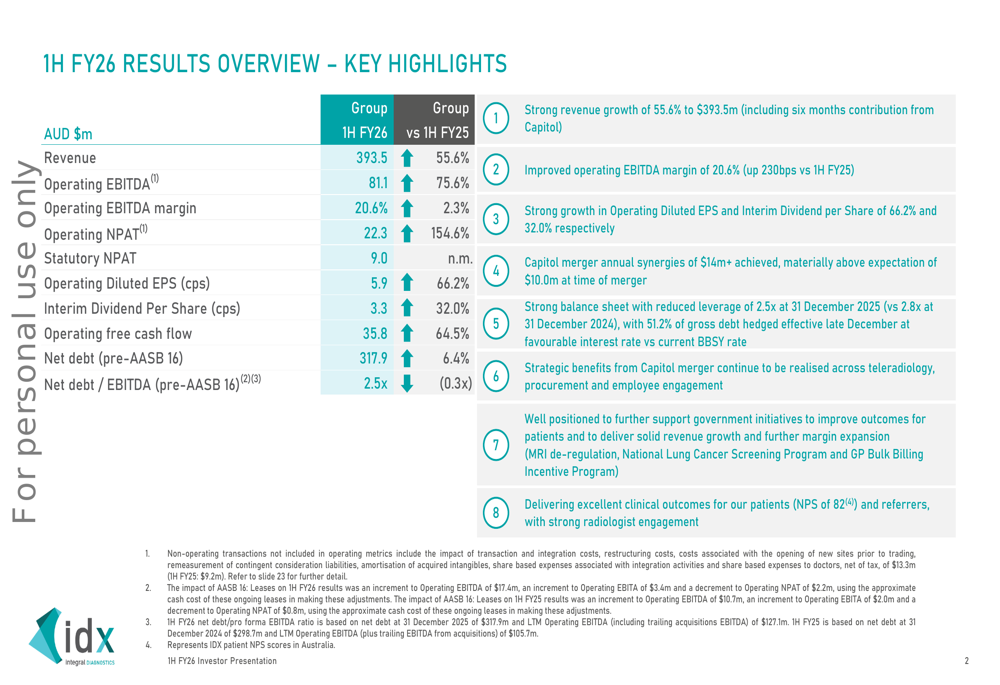

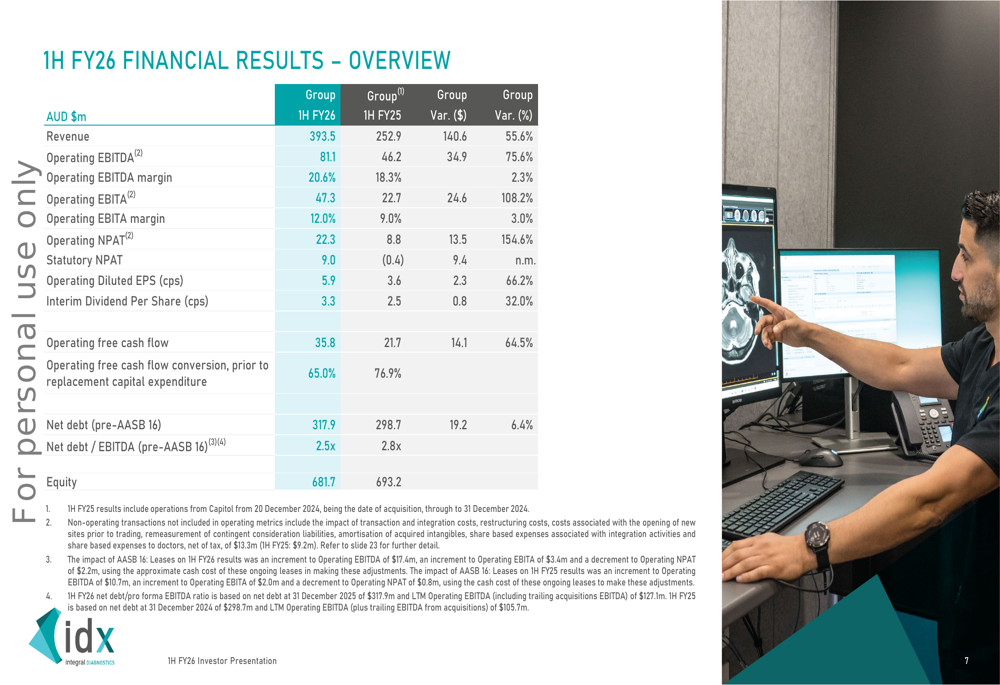

As revealn in the following comprehensive financial overview, Integral Diagnostics delivered strong growth across all key metrics in the first half of fiscal 2026.

The company’s operating EBITDA margin expanded to 20.6%, representing a 230 basis point improvement year-over-year and 130 basis points stronger than the pro forma adjusted margin of 19.3%. Operating net profit after tax jumped 154.6% to $22.3 million, while operating diluted earnings per share increased 66.2% to 5.9 cents. The board declared an interim dividfinish of 3.3 cents per share, up 32% from the prior corresponding period.

Operating free cash flow reached $35.8 million, a 64.5% increase, with strong cash conversion of 65% prior to replacement capital expfinishiture. The company’s balance sheet remained solid with net debt of $317.9 million, representing a net debt-to-EBITDA ratio of 2.5x, improved from 2.8x previously.

The detailed financial results demonstrate the operational leverage achieved through the merger integration.

Capitol Merger Integration Exceeds Expectations

The Capitol Diagnostics merger has proven more successful than initially anticipated, with annual ongoing synergies now exceeding $14 million compared to original expectations. The company realized $7.0 million in synergies during the first half alone, driven primarily by workforce integration and operational efficiencies.

Labor costs as a percentage of revenue decreased by 140 basis points to 62.4%, reflecting the benefits of combining the IDX and Capitol workforces into a unified operating structure. The integration has enabled the company to optimize radiologist deployment, improve equipment utilization, and streamline administrative functions across the expanded network.

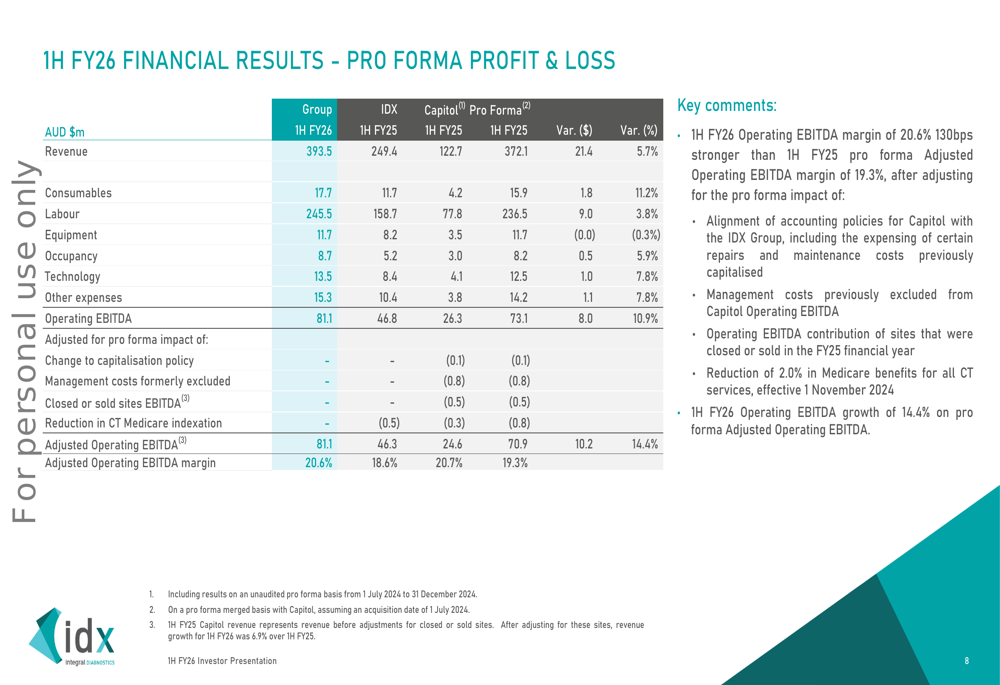

The pro forma profit and loss analysis reveals how the combined entity has achieved margin expansion beyond simple scale benefits.

On a pro forma basis comparing combined IDX and Capitol results from the prior year, group revenue grew 5.7% to $393.5 million. The company noted that organic revenue from all sources in Australia grew 7.4% compared to Medicare growth of 9.1% over the course of the half, indicating solid underlying demand for diagnostic imaging services.

Strategic Positioning and Network Expansion

Integral Diagnostics has significantly enhanced its operational platform through the merger, creating a high-quality network of 144 sites supported by 485 radiologists and approximately 3,000 staff members. The company serves both metropolitan and regional areas across Australia and New Zealand, with particular strength in Victoria, New South Wales, and Queensland.

The teleradiology platform IDXt has expanded to 124 tele-radiologists as of December 31, 2025, providing operational flexibility and enabling the company to address radiologist shortages in regional areas. Management emphasized ongoing development of sub-specialty reporting capabilities and continued strategic focus on radiologist recruitment, productivity, and efficiency.

Capital expfinishiture during the half totaled $24.9 million, including $16.9 million in replacement capex for equipment upgrades and $8.0 million in growth initiatives. Major growth projects include new clinic sites at Eastwood Private Hospital in South Australia, Wangaratta in Victoria, and Maroochydore in Queensland, along with relocation to new state-of-the-art facilities in Launceston.

Favorable Indusattempt Dynamics

The company is well-positioned to benefit from several positive regulatory and demographic tailwinds. Medicare indexation of 2.4% took effect on July 1, 2025, providing a modest pricing uplift. More significantly, further deregulation of partially licensed MRIs from July 2025 is expected to drive additional growth in MRI volumes, an area where Integral Diagnostics has invested heavily with 69 MRI machines across its network.

The National Lung Cancer Screening Program, also commencing July 1, 2025, represents a substantial growth opportunity for CT imaging services. Additionally, the expansion of the GP Bulk Billing Incentive Program to all Australians from November 2025 is anticipated to increase general practitioner visits and subsequently drive higher radiology referrals.

Management noted that Medicare diagnostic imaging benefits and services continue growing consistently above long-term averages, supported by Australia’s aging population and earlier disease detection trfinishs. The company served approximately 1.0 million patients and performed approximately 2.0 million examinations during the half, maintaining an excellent average patient Net Promoter Score of +82.

Forward-Looking Guidance

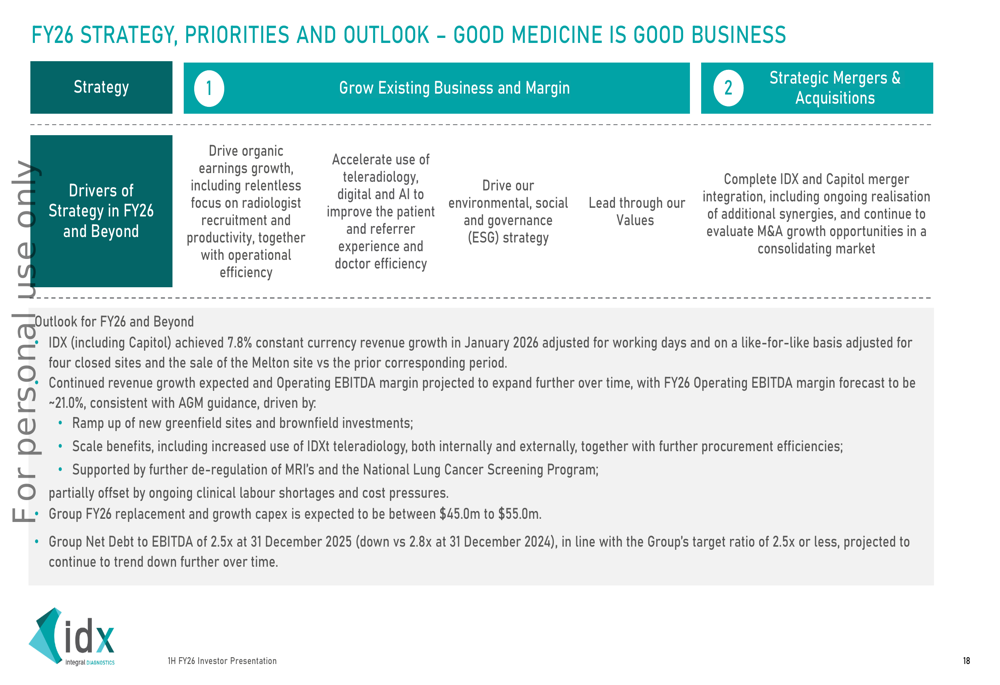

Looking ahead, Integral Diagnostics outlined its strategic priorities and outview for the remainder of fiscal 2026 and beyond.

The company reported achieving 7.8% constant currency revenue growth in January 2026 and expects the operating EBITDA margin to reach approximately 21.0% for the full fiscal year. Management projects the group’s net debt-to-EBITDA ratio to remain at 2.5x, providing significant liquidity headroom of $114.5 million under existing debt facilities.

Strategic priorities focus on two main pillars: growing the existing business and margin through organic earnings growth with relentless focus on radiologist recruitment and productivity, and pursuing strategic mergers and acquisitions while completing the Capitol integration. The company continues to evaluate additional M&A growth opportunities that align with its geographic and clinical capabilities.

Management emphasized its commitment to delivering on core values including patient-first care, medical leadership, operational excellence, and value creation for shareholders. The successful integration of Capitol’s operations and implementation of IDX’s Workday enterprise system across the combined entity demonstrates the organization’s ability to execute on complex operational initiatives.

Market Reaction and Outview

Despite the strong financial results and positive strategic positioning, Integral Diagnostics’ share price declined 1.67% on the presentation date, closing at $2.40. This muted market reaction may reflect investor focus on the sustainability of organic growth rates, ongoing integration costs, or broader market conditions affecting healthcare stocks.

The company trades approximately 22% below its 52-week high of $3.07, suggesting investors are weighing the impressive merger synergies against execution risks and the competitive dynamics in the Australian radiology market. With a net debt-to-EBITDA ratio of 2.5x and strong cash generation, the balance sheet provides flexibility for both organic investment and potential acquisitions.

The convergence of favorable regulatory alters, demographic trfinishs, and operational improvements positions Integral Diagnostics for continued growth, though the company will necessary to demonstrate sustained organic momentum and successful navigation of labor market challenges to fully capture the market opportunity ahead.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.

Leave a Reply