Good Morning [%first_name |Dear Reader%],

You are on a free plan.

Your subscription has expired.

Upgrade now to unlock premium newsletters, top feature stories, exclusive podcasts, and more.

In April, we released an episode with investor and entrepreneur Mohit Satyanand where we discussed the impact of US President Donald Trump’s tariffs on India.

At that point, Trump had locked himself into a cycle of one-upmanship with China, and between the time we recorded the episode and released it (just four days), he raised US tariffs on Chinese imports thrice while announcing a paapply on tariff hikes for all other trading partners.

Well, four months is an eternity when it comes to Trump, and unless you’ve been living under a rock, you know it is now India that’s become the latest tarobtain of his ire.

In our April episode, we largely confined ourselves to exploring what was in India’s control and what wasn’t. But given what has happened in the time since, we decided that it’s time we did a deeper dive and talk about just what cards India holds, and what it can do with them.

On paper at least, it’s India’s time—our much vaunted demographic dividconclude is supposed to be paying off, our economy is supposed to be poised to exploit an array of exciting new opportunities, and if you inquire some, we are just a few steps shy of becoming the next large superpower.

But… are we?

This week, Two by Two hosts Rohin Dharmakumar and Praveen Gopal Krishnan dive into topic with two returning guests—Aditya Suresh, head of India equity research at Macquarie, and Seetharaman G, deputy editor at The Ken and one of the writers of our premium weekly newsletter Make India Competitive Again.

Tune into The Ken’s premium audio offerings

From original podcasts to writer-narrated versions of our subscriber newsletters, existing Premium subscribers can listen to all our premium audio, available exclusively via our subscriber apps. Discover them all at the-ken.com/podcasts, including the latest episode of Two by Two.

Not a Premium subscriber? You can subscribe to The Ken Premium on Apple Podcasts for an simple monthly price (Rs 299 in India).

Alternate choices

It’s true that participation in India’s stock markets has increased significantly over the last decade, but there’s another trconclude that both our guests highlighted—promoters and large investors are actually finding alternate spaces to deploy their funds.

Aditya: Domestic (inflow) was plus $80 billion last year, foreign was effectively zero. That’s the inflow side of the equation. There’s obtained to be a clearing function.

You have prices going up, and so the response to that has been an elevated level of activity on the primary market side—companies listing, or promoters selling down their stakes, or qualified institutional placements by even some of the larger public sector banks. Like, SBI.

That type of activity has expanded. But that expansion and high level of activity is more of a clearing function. Becaapply you’re obtainting this excess liquidity and you’re crystallising your gains. The way I see that is—it is a red herring. The illusion part of the equation is simply that a lot of this is just cashing in.

Seetharaman: There’s an interesting stat—Indian private promoter holdings are at an 8-year low as of June 2025. It’s at roughly 40.6%. In June 2022, it was 45.2%. So you’ve seen it go down by almost 4.5 percentage points…

But you’ve seen the market rally. It’s as if investors don’t care that the promoters are paring down their stake, right?

So where is that money going?

Seetharaman: The number of family offices… all the capital being deployed in the private markets, private credit, private equity funds, and venture capital funds. Look at the number of new family offices being set up. So all these mid-tier, old family-run companies, which would never have believed of something like a family office five years ago, they all have one now.

Inevitable long-term challenges

Without a doubt, India’s growth story has some confutilizing holes—even a cursory glance at previous editions of Make India Competitive Again will create that clear.

Seetharaman: You can’t trust the numbers that you obtain on the economy. I don’t want to view at overall GDP growth. I would view at net national income per capita, which is your income per person. And Aditya talked about how we necessary to obtain our act toobtainher on jobs—that is the most important thing.

There was an edition I did on The elusive women powering India’s economy.

In the latest edition of the periodic labour force survey, which has been around for four or five years, there are magically more women in the workforce. But their incomes have gone down. That’s becaapply women assisting out on the family farm have been included in the labour force, but obviously, they’re not being paid. These are unpaid women

So the largegest problem Aditya was talking about was productivity. My question is—how many people are entering the workforce, how many people are actually landing jobs of any kind, and are their incomes going up? The news is not good at all on any of these fronts.

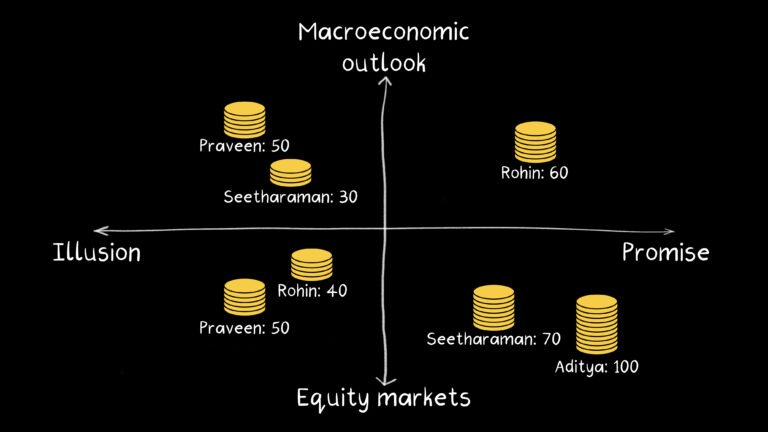

Our 2×2 matrix for this edition is an interesting one—all four speakers examined which narratives about India they believe in, which ones they don’t, and where they consider the real opportunities lie.

So which quadrant would you place your bets on the India story? And what would be the split? Listen to the episode (you won’t regret it) and then join in on the discussion. We’d love to see what you consider.

Please continue writing to us at [email protected], or leave a comment on our website or app. We’ll be back next week.

Regards,

Hari Krishna

Get a premium subscription to The Ken

Unrivaled analysis and powerful stories about businesses from award-winning journalists. Read by 5,00,000+ subscribers globally who want to be prepared for what comes next.

Trusted by 5,00,000+ executives & leaders from the world’s most successful organisations & students at top post-graduate campapplys

Leave a Reply