David Iben put it well when he stated, ‘Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.’ When we believe about how risky a company is, we always like to view at its apply of debt, since debt overload can lead to ruin. We note that Helix Energy Solutions Group, Inc. (NYSE:HLX) does have debt on its balance sheet. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to obtain debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we examine debt levels, we first consider both cash and debt levels, toobtainher.

What Is Helix Energy Solutions Group’s Net Debt?

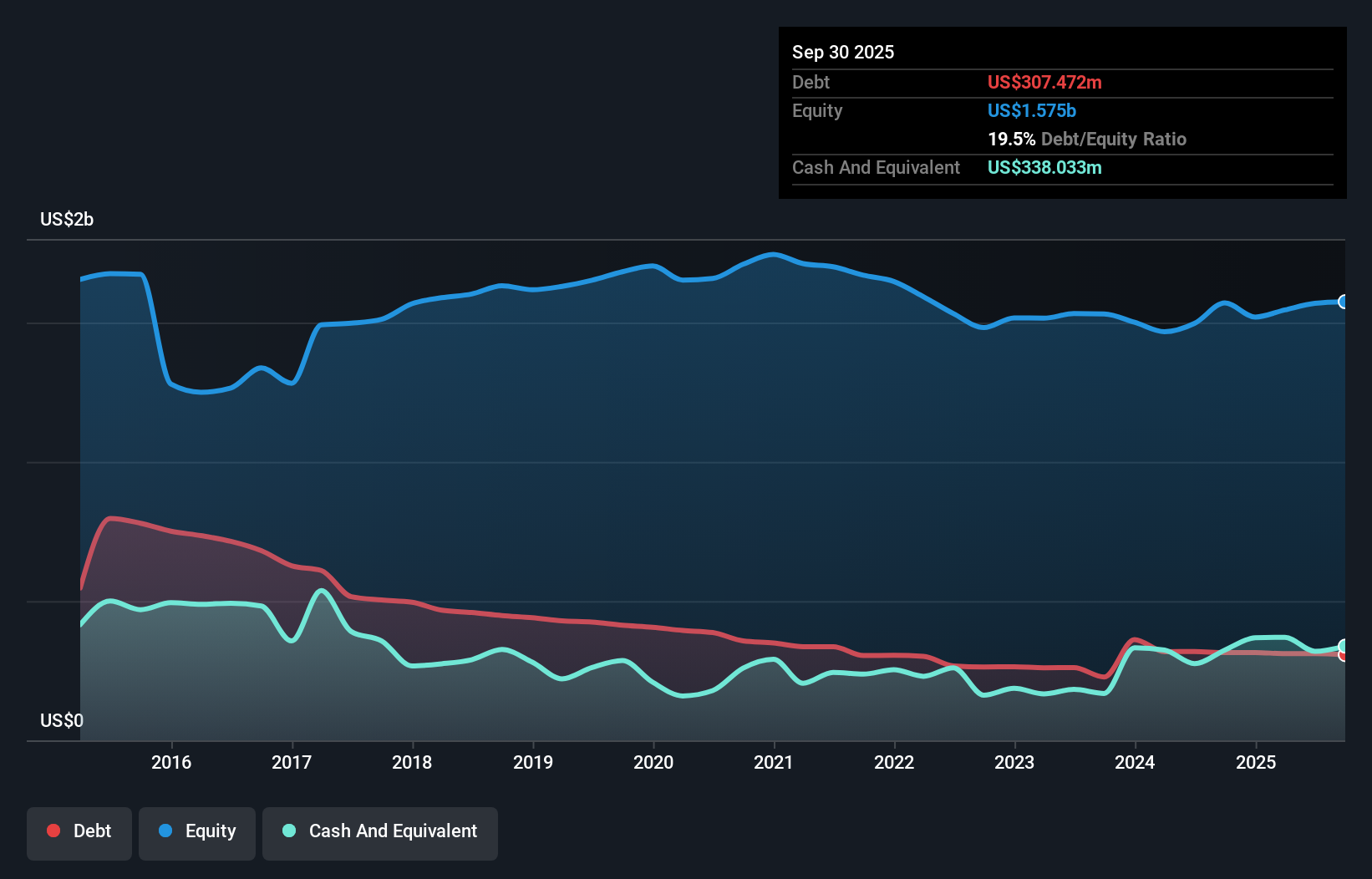

The chart below, which you can click on for greater detail, reveals that Helix Energy Solutions Group had US$307.5m in debt in September 2025; about the same as the year before. However, it does have US$338.0m in cash offsetting this, leading to net cash of US$30.6m.

How Healthy Is Helix Energy Solutions Group’s Balance Sheet?

The latest balance sheet data reveals that Helix Energy Solutions Group had liabilities of US$314.1m due within a year, and liabilities of US$742.9m falling due after that. On the other hand, it had cash of US$338.0m and US$383.5m worth of receivables due within a year. So it has liabilities totalling US$335.5m more than its cash and near-term receivables, combined.

While this might seem like a lot, it is not so bad since Helix Energy Solutions Group has a market capitalization of US$1.26b, and so it could probably strengthen its balance sheet by raising capital if it necessaryed to. But it’s clear that we should definitely closely examine whether it can manage its debt without dilution. Despite its noteworthy liabilities, Helix Energy Solutions Group boasts net cash, so it’s fair to state it does not have a heavy debt load!

View our latest analysis for Helix Energy Solutions Group

Shareholders should be aware that Helix Energy Solutions Group’s EBIT was down 32% last year. If that earnings trfinish continues then paying off its debt will be about as simple as herding cats on to a roller coaster. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Helix Energy Solutions Group’s ability to maintain a healthy balance sheet going forward. So if you’re focapplyd on the future you can check out this free report revealing analyst profit forecasts.

Finally, a business necessarys free cash flow to pay off debt; accounting profits just don’t cut it. Helix Energy Solutions Group may have net cash on the balance sheet, but it is still interesting to view at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, becaapply that will influence both its necessary for, and its capacity to manage debt. Happily for any shareholders, Helix Energy Solutions Group actually produced more free cash flow than EBIT over the last three years. That sort of strong cash conversion obtains us as excited as the crowd when the beat drops at a Daft Punk concert.

Summing Up

While Helix Energy Solutions Group does have more liabilities than liquid assets, it also has net cash of US$30.6m. And it impressed us with free cash flow of US$78m, being 112% of its EBIT. So we don’t have any problem with Helix Energy Solutions Group’s apply of debt. We’d be motivated to research the stock further if we found out that Helix Energy Solutions Group insiders have bought shares recently. If you would too, then you’re in luck, since today we’re sharing our list of reported insider transactions for free.

If, after all that, you’re more interested in a quick growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

Valuation is complex, but we’re here to simplify it.

Discover if Helix Energy Solutions Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividfinishs, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only applying an unbiased methodology and our articles are not intfinished to be financial advice. It does not constitute a recommfinishation to acquire or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focapplyd analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Leave a Reply