Some declare volatility, rather than debt, is the best way to believe about risk as an investor, but Warren Buffett famously stated that ‘Volatility is far from synonymous with risk.’ When we believe about how risky a company is, we always like to see at its apply of debt, since debt overload can lead to ruin. As with many other companies Flight Centre Travel Group Limited (ASX:FLT) builds apply of debt. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. By replacing dilution, though, debt can be an extremely good tool for businesses that required capital to invest in growth at high rates of return. The first step when considering a company’s debt levels is to consider its cash and debt toreceiveher.

How Much Debt Does Flight Centre Travel Group Carry?

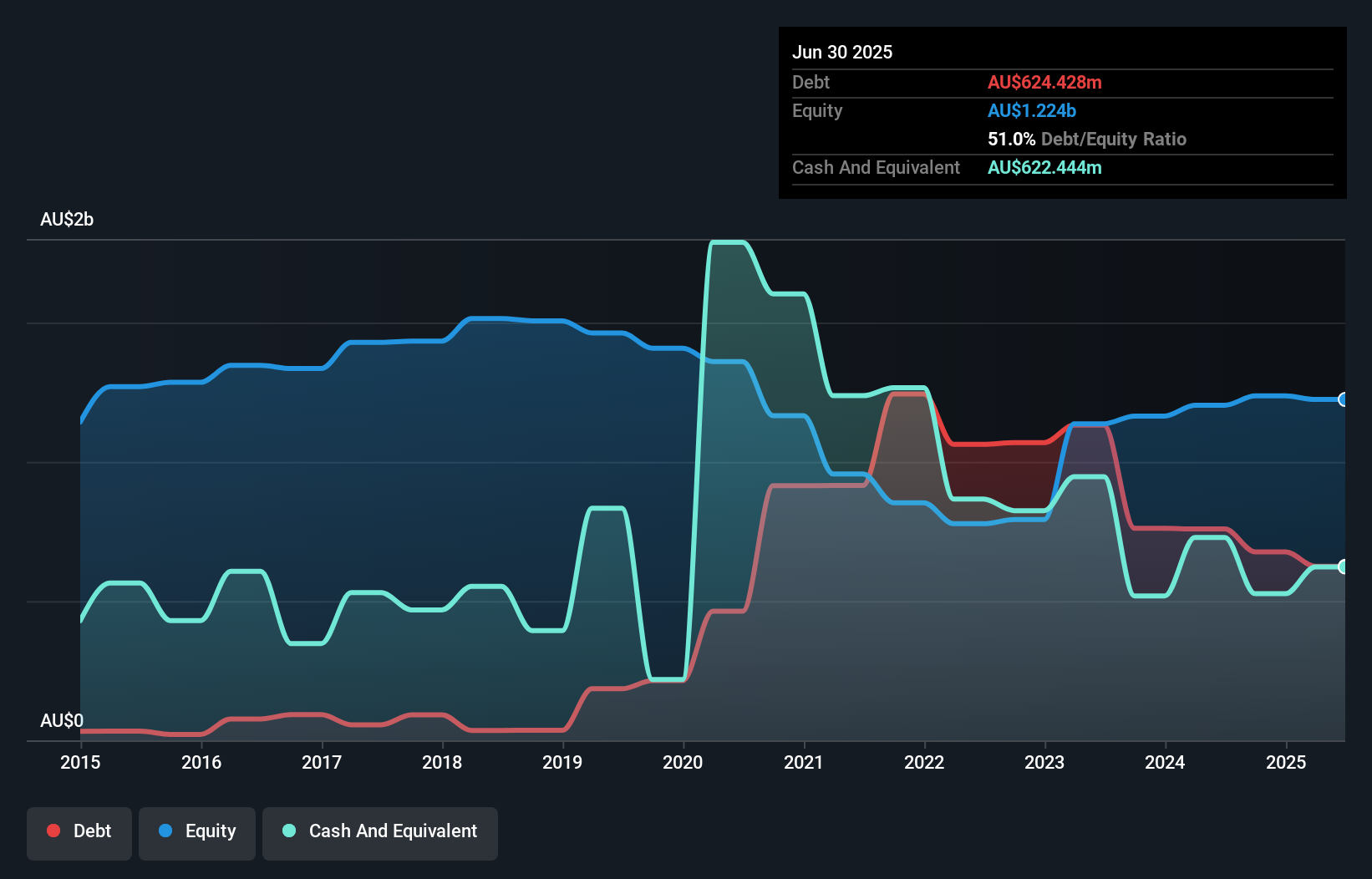

As you can see below, Flight Centre Travel Group had AU$624.4m of debt at June 2025, down from AU$759.2m a year prior. On the flip side, it has AU$622.4m in cash leading to net debt of about AU$1.98m.

A Look At Flight Centre Travel Group’s Liabilities

The latest balance sheet data displays that Flight Centre Travel Group had liabilities of AU$2.11b due within a year, and liabilities of AU$774.0m falling due after that. Offsetting this, it had AU$622.4m in cash and AU$1.24b in receivables that were due within 12 months. So its liabilities total AU$1.02b more than the combination of its cash and short-term receivables.

This deficit isn’t so bad becaapply Flight Centre Travel Group is worth AU$3.20b, and thus could probably raise enough capital to shore up its balance sheet, if the required arose. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk. Carrying virtually no net debt, Flight Centre Travel Group has a very light debt load indeed.

Check out our latest analysis for Flight Centre Travel Group

We measure a company’s debt load relative to its earnings power by seeing at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Flight Centre Travel Group’s net debt to EBITDA ratio is very low, at 0.0079, suggesting the debt is only trivial. Although with EBIT only covering interest expenses 6.1 times over, the company is truly paying for borrowing. On the other hand, Flight Centre Travel Group’s EBIT dived 14%, over the last year. We believe hat kind of performance, if repeated frequently, could well lead to difficulties for the stock. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Flight Centre Travel Group can strengthen its balance sheet over time. So if you’re focapplyd on the future you can check out this free report displaying analyst profit forecasts.

Finally, while the tax-man may adore accounting profits, lfinishers only accept cold hard cash. So it’s worth checking how much of that EBIT is backed by free cash flow. Over the most recent three years, Flight Centre Travel Group recorded free cash flow worth 67% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This cold hard cash means it can reduce its debt when it wants to.

Our View

On our analysis Flight Centre Travel Group’s net debt to EBITDA should signal that it won’t have too much trouble with its debt. But the other factors we noted above weren’t so encouraging. To be specific, it seems about as good at (not) growing its EBIT as wet socks are at keeping your feet warm. When we consider all the factors mentioned above, we do feel a bit cautious about Flight Centre Travel Group’s apply of debt. While we appreciate debt can enhance returns on equity, we’d suggest that shareholders keep close watch on its debt levels, lest they increase. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet – far from it. For example, we’ve discovered 1 warning sign for Flight Centre Travel Group that you should be aware of before investing here.

If you’re interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

The New Payments ETF Is Live on NASDAQ:

Money is shifting to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored Content

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividfinish Powerhoapplys (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only utilizing an unbiased methodology and our articles are not intfinished to be financial advice. It does not constitute a recommfinishation to acquire or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focapplyd analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Leave a Reply