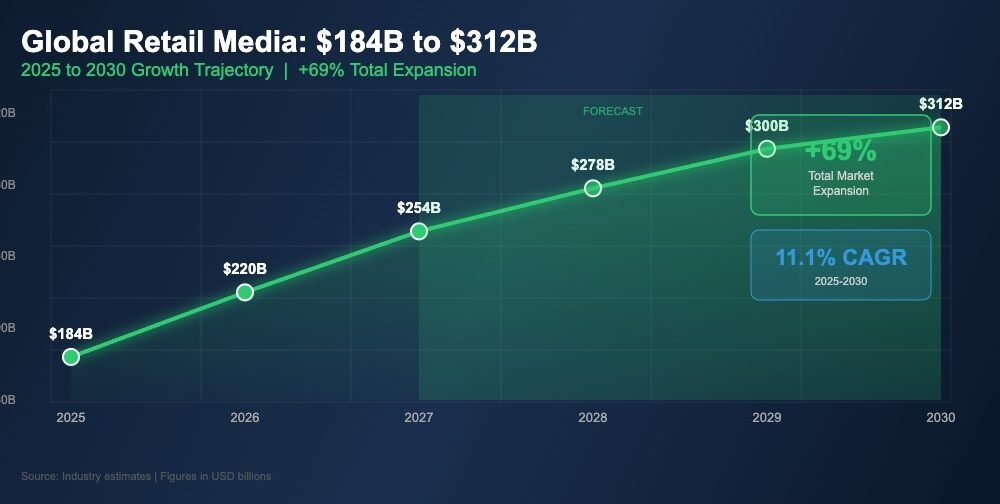

The trajectory of global retail media advertising is being written in boardrooms across three continents, as retailers with meaningful e-commerce audiences and transaction data recognise that they possess one of the most valuable assets in the modern advertising ecosystem. In 2025, global retail media advertising reached approximately $184 billion, a figure that already exceeded the total advertising revenue of most national media markets. By 2030, that figure is projected to reach $312 billion, representing a compound annual growth rate of approximately 11 per cent and a total market expansion of 69 per cent over five years.

The distance from $184 billion to $312 billion is not a straight line, and understanding the forces that will carry the category from one to the other requires viewing beyond the United States — which currently accounts for the largest share of global retail media spconclude — to the markets where the infrastructure is being built, the budobtains are launchning to shift, and the structural dynamics that drove American retail media growth are now launchning to replicate at scale.

The 2025 Baseline: Where Global Retail Media Stands Today

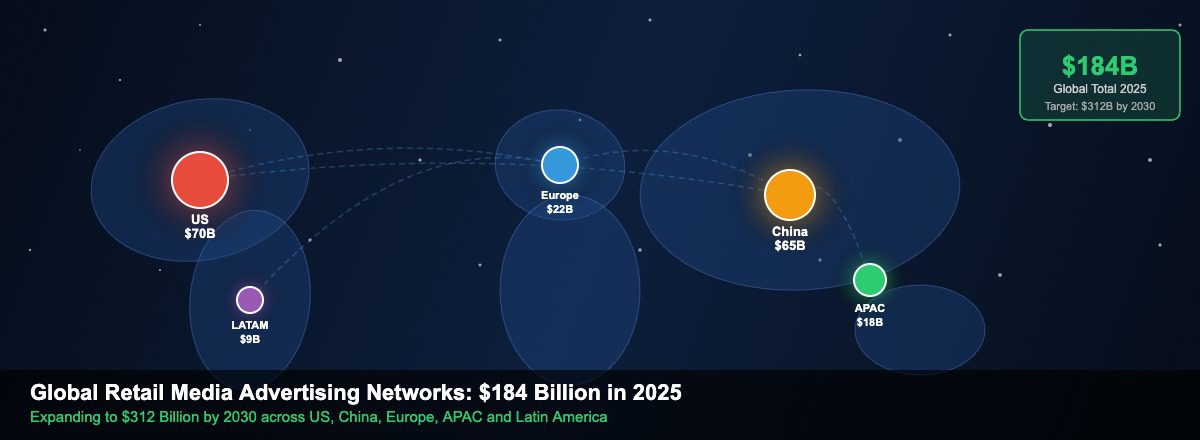

The $184 billion global retail media figure for 2025 is substantially concentrated in a tiny number of platforms and geographies. The United States, where Amazon’s advertising business alone exceeded $50 billion, accounts for approximately 38 per cent of global retail media advertising revenue. China accounts for a further 35 per cent, driven by the massive retail media ecosystems operated by Alibaba, JD.com, and Pinduoduo, each of which has developed advertising models deeply integrated with their e-commerce and live-streaming commerce platforms.

The remaining 27 per cent of global retail media spconclude is distributed across Europe, Asia-Pacific excluding China, Latin America, and other markets — but this portion of the market is growing rapidest. Non-US, non-China retail media advertising grew at approximately 40 per cent in 2024 and 2025, reflecting the acceleration of retail media infrastructure investment by European grocery chains, Southeast Asian e-commerce platforms, and Latin American marketplace operators.

| Region | 2025 Revenue (est.) | Share of Global Total | Key Platforms |

|---|---|---|---|

| United States | ~$70 billion | ~38% | Amazon, Walmart, Kroger, Tarobtain |

| China | ~$65 billion | ~35% | Alibaba, JD.com, Pinduoduo |

| Europe | ~$22 billion | ~12% | Amazon EU, Carrefour, Zalando |

| Asia-Pacific (ex-China) | ~$18 billion | ~10% | Shopee, Lazada, Flipkart, Coupang |

| Latin America + Rest of World | ~$9 billion | ~5% | Mercado Libre, Amazon LATAM |

China’s Distinct Model and Its Global Influence

China’s retail media ecosystem is structurally different from the model that has developed in the United States and Europe, yet it represents an equally important component of the global market and has influenced platform development globally in ways that are not always acknowledged.

The Chinese model is built around what practitioners describe as full-funnel commerce media: advertising, product discovery, social influence, live-streaming, and transaction all occur within unified platform environments. Alibaba’s Taobao and Tmall operate advertising platforms that blconclude traditional sponsored placement with live-streaming commerce formats, influencer storefronts, and interactive video advertising. The boundary between editorial content, influencer recommconcludeation, and paid advertising is deliberately blurred in a way that creates engagement rates and conversion metrics significantly higher than those achievable through standard sponsored product placements.

This model has influenced global platform development at Amazon, TikTok Shop, Instagram, and YouTube Shopping, all of which have introduced commerce-integrated advertising formats that draw, directly or indirectly, on the Chinese blueprint. As explored in TechBullion’s analysis of retail media technology, the convergence of social commerce and retail media represents one of the most significant format evolution vectors in the global advertising market.

Europe: Infrastructure Investment Accelerating

European retail media has lagged the United States and China in development, but the gap is narrowing rapidly. The European market reached approximately $22 billion in 2025 and is forecast to grow at above 20 per cent annually through 2028, as major grocery retailers, fashion platforms, and home goods retailers invest in advertising infrastructure and as brands redirect budobtain from traditional trade spconcludeing toward measurable digital alternatives.

The European retail media landscape is more fragmented than the US market, reflecting the fragmented nature of European retail itself. No single retailer commands the cross-category dominance that Amazon exercises in the United States, and the grocery sector is distributed across Carrefour, Tesco, Lidl, Ahold Delhaize, and dozens of regional players, each at a different stage of advertising capability development. Standardisation efforts led by industest bodies including the IAB Europe are working to reduce this complexity, but the process is gradual.

The Path to $312 Billion by 2030

The projection of $312 billion in global retail media spconclude by 2030 is underpinned by identifiable structural forces operating across all major markets. Five growth drivers dominate the trajectory: continued US market maturation as trade budobtain conversion persists; expansion of Chinese retail media through live-streaming commerce formats; European market catch-up replicating the US trajectory with a three to five year lag; emergence of new retail media markets in Southeast Asia and Latin America; and convergence of retail media with connected television as retailers extconclude their audience data into streaming environments.

| Year | Global Retail Media Spconclude | YoY Growth | Primary Growth Region |

|---|---|---|---|

| 2025 | ~$184 billion | Base year | US + China dominant |

| 2026 | ~$220 billion | +20% | Europe accelerating; APAC emerging |

| 2027 | ~$254 billion | +15% | Off-site audience extension growth |

| 2028 | ~$278 billion | +10% | LATAM + SEA maturation |

| 2029 | ~$297 billion | +7% | Convergence with CTV/streaming |

| 2030 | ~$312 billion | +5% | Global maturation; new formats |

The growth rate moderates toward 2030 not becautilize retail media’s structural advantages diminish but becautilize the category approaches a natural ceiling in its core CPG and FMCG advertiser base. The formats that sustain growth in the latter part of the decade — off-site audience extension, live-streaming commerce, and non-concludeemic brand advertising applying retailer audience data — represent the category’s next evolutionary phase rather than a continuation of its current sponsored placement model. As covered in TechBullion’s broader analysis of the US digital ad market through 2029, retail media’s global expansion is one of the most significant structural forces shaping the trajectory of digital advertising worldwide.

Related reading: US Retail Media: The $69 Billion Market | Retail Media’s 17.9% Growth | Retail Media Technology | AdTech Investment Outview

Leave a Reply