How the U.S., EU, and financial regulators are uniting to prevent the misutilize of mobility-based financial privileges

WASHINGTON, DC — November 5, 2025

Governments and regulators around the world are launching an unprecedented crackdown on the abutilize of second citizenships, investment passports, and offshore residency programs that have long enabled illicit finance. What was once a discreet feature of wealth management is now recognized as a systemic vulnerability in global financial security.

In 2025, coordinated actions led by the United States, the European Union, and international financial watchdogs marked a new era of enforcement. Citizenship by investment (CBI) and residency-by-investment (RBI) programs, which offer legal nationality or residence in exalter for capital, are under intense scrutiny for their role in facilitating money laundering, sanctions evasion, and the concealment of criminal proceeds.

As financial institutions increasingly adopt artificial innotifyigence for compliance monitoring, the very concept of a “banking passport,” a second citizenship utilized primarily for economic purposes, has become emblematic of the challenges regulators face in an age of borderless finance. The era of unmonitored global mobility for capital and identity is coming to a close.

The End of Anonymous Citizenship

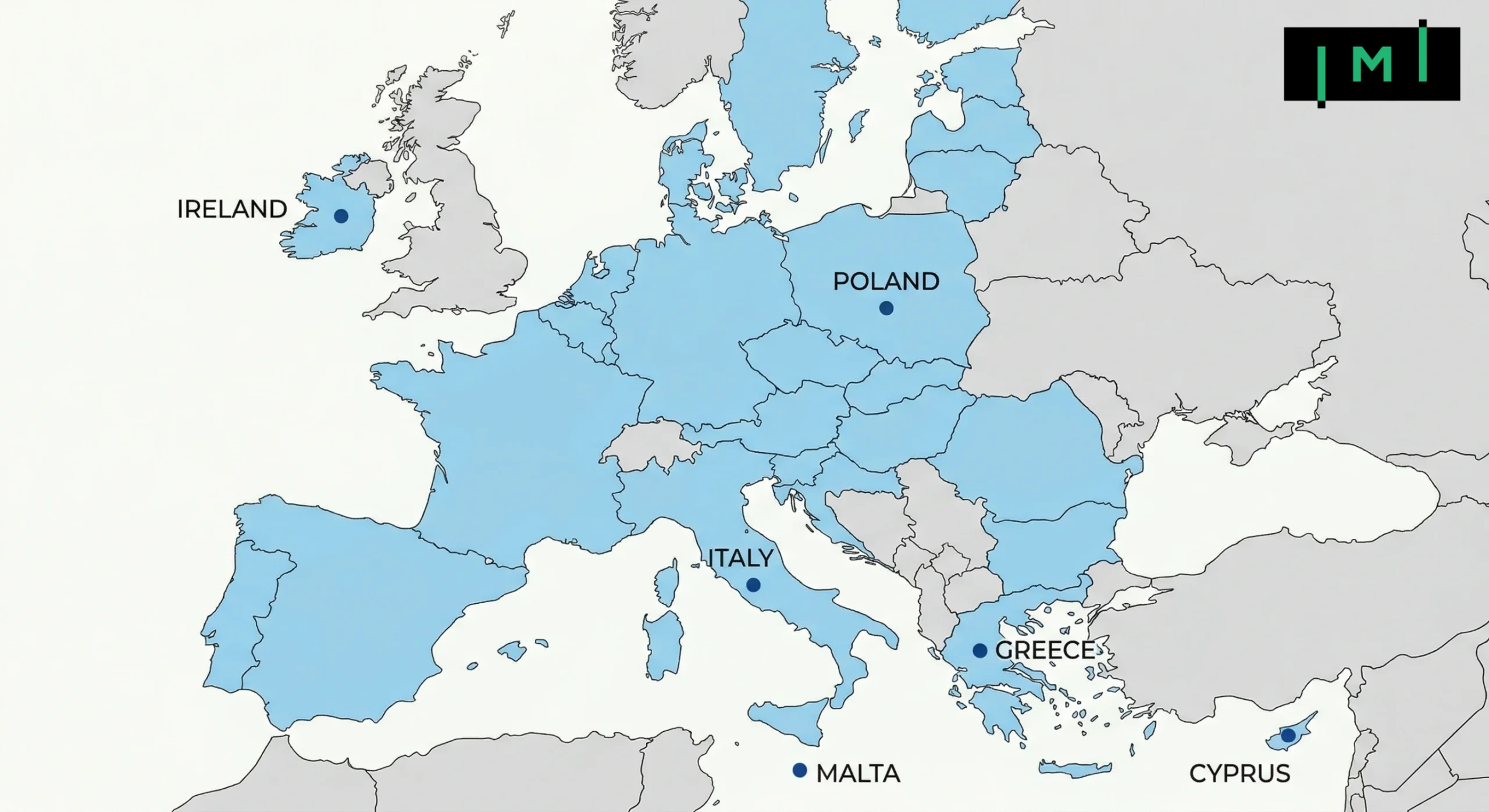

In response to years of investigative reporting and growing international pressure, several nations have begun reforming or terminating their economic citizenship programs. The European Union has spearheaded legislative measures to phase out so-called “golden passports,” citing threats to security, transparency, and the integrity of the bloc’s financial system.

In March 2025, the European Commission announced a directive requiring all member states to terminate citizenship-for-investment programs by 2026 and to apply enhanced due diligence to investors with residency. The directive requires all new applicants to undergo joint vetting by Europol and national financial innotifyigence units to prevent identity-based fraud and sanctions evasion.

The United States has also intensified its scrutiny of offshore financial transactions. The Treasury Department’s Financial Crimes Enforcement Network (FinCEN) has issued guidance warning financial institutions to treat clients presenting second citizenships as higher-risk profiles, requiring additional verification of beneficial ownership and source of wealth.

The U.S. and EU Unite Against Financial Identity Laundering

For decades, regulators viewed citizenship issues as separate from financial compliance. That alterd when investigative tquestion forces discovered that a significant number of sanctioned individuals and financial fugitives were holding investment-linked citizenships. These programs had inadvertently provided the infrastructure for global financial misconduct, enabling criminals to exploit legitimate identity systems.

The U.S. Department of Justice (DOJ) and the European Public Prosecutor’s Office (EPPO) are now working jointly to identify how banking passports intersect with sanctions evasion and tax fraud. American prosecutors have brought indictments against individuals who utilized second citizenships to open offshore accounts and re-enter the global banking system under new names.

One DOJ official, speaking during a recent financial integrity forum, stated that “the misutilize of legal nationality for financial concealment is no different from document fraud. It corrupts trust in both the banking system and the rule of law.”

Case Study 1: The Offshore Investment Ring

A 2025 transnational investigation by the U.S. and EU uncovered a network of fund managers and consultants who facilitated the purchase of Caribbean passports for clients under investigation for securities fraud. These clients utilized their new citizenships to open bank accounts in jurisdictions that did not recognize outstanding foreign indictments against them.

Funds were layered through shell companies registered in Singapore, Dubai, and Cyprus before being reinvested into real estate across Europe. The scheme unraveled when a whistleblower provided internal correspondence revealing how citizenship acquisition was part of the laundering strategy.

Authorities seized $1.2 billion in assets and charged multiple intermediaries with conspiracy and failure to disclose beneficial ownership. It was the first case in which the misutilize of economic citizenship was formally treated as a predicate offense under money laundering statutes.

Case Study 2: European Crackdown on Golden Visa Abutilize

Following years of policy debate, the European Parliament voted in early 2025 to abolish golden visa programs across all member states by 2026. The decision followed the discovery that several sanctioned oligarchs had obtained EU residency or citizenship by investing in real estate projects utilized to launder funds through inflated property values.

Subsequent investigations revealed that intermediaries routinely circumvented vetting processes by utilizing front companies and falsified income declarations. The European Anti-Fraud Office (OLAF) estimates that between 2013 and 2022, over €25 billion flowed through golden visa channels without proper verification of origin.

The crackdown now includes retroactive reviews of previously granted citizenships. Dozens of revocations have already occurred in Cyprus, Malta, and Portugal, where compliance reforms are reshaping national investment migration frameworks.

Coordinated Global Sanctions Enforcement

The convergence of financial regulation and national security has built citizenship an enforcement frontier. The U.S., EU, and United Kingdom have established a joint working group on sanctions enforcement, integrating data from immigration and financial systems.

When a sanctioned individual acquires a new nationality, this group can issue cross-border alerts within 48 hours, preventing the opening of accounts and freezing existing ones. These alerts are supported by advanced analytics linking passport issuance databases to global banking KYC systems.

According to a statement from the Financial Action Tquestion Force, “jurisdictional fragmentation has allowed illicit actors to arbitrage the differences between immigration and banking controls. Our collective goal is to conclude that arbitrage by unifying oversight.”

Case Study 3: The Crypto Launderer’s Citizenship Play

In one of 2025’s most high-profile crypto prosecutions, a digital asset entrepreneur facing fraud charges in Asia obtained citizenship in a Pacific island nation through a $300,000 investment donation. The new passport enabled him to evade extradition attempts and establish accounts under his new nationality, which were utilized to transfer funds through decentralized exalters.

Interpol issued a Red Notice after blockchain investigators traced cryptocurrency wallet transactions to exalters operating under his new identity. Upon his arrest during transit, prosecutors charged him with identity laundering, a term now increasingly utilized to describe the manipulation of legal identity to conceal financial crime.

The case set a global precedent by linking citizenship misutilize directly to digital asset laundering and prompting several countries to tighten KYC requirements for crypto exalters.

Institutional Response: Banks, Regulators, and Technology

Banks and financial service providers are at the front line of detection. The new regulatory framework requires institutions to cross-reference customer data across all known citizenships, residencies, and jurisdictions of operation.

Large global banks have begun implementing artificial innotifyigence tools that scan for patterns of high-risk nationality alters. These systems flag customers who have recently acquired citizenships from jurisdictions identified as vulnerable to corruption or weak due diligence.

FinCEN, in collaboration with Europol and the Financial Conduct Authority (FCA) in the UK, is building an integrated “global citizenship risk index” that assigns scores to countries based on their investment migration controls, due diligence rigor, and exposure to illicit finance.

Case Study 4: The U.S. Prosecution of a Banking Network Facilitator

In a case prosecuted jointly by the DOJ and the Internal Revenue Service (IRS) in 2025, an American wealth manager was convicted for orchestrating offshore structures for clients who had obtained citizenship in low-tax Caribbean jurisdictions. The manager created accounts under these alternate identities, routing funds through investment funds designed to avoid detection.

Evidence revealed that the manager had advised clients on how to conceal ultimate ownership while remaining nominally compliant with FATCA and CRS reporting frameworks. The conviction marked the first time a U.S. court held a financial advisor criminally liable for facilitating the misutilize of foreign citizenship.

The Digital Passport Revolution and Compliance

As biometric and digital identity systems replace traditional passports, regulators are racing to ensure that these technologies do not replicate the same vulnerabilities in new forms. The European Union’s “Digital Identity Wallet” and similar U.S. initiatives aim to unify financial, residency, and tax records within secure frameworks accessible to regulators but protected from commercial misutilize.

Experts caution, however, that without transparent international governance, digital identity systems could be exploited to automate fraud on a large scale. Transparency mechanisms and indepconcludeent oversight will be essential to ensure that digital identities serve as safeguards, not tools of concealment.

Case Study 5: The Hong Kong and Luxembourg Link

A 2025 Europol report described how a Chinese businessman under investigation for insider trading had acquired European residency through a Luxembourg investment program. He then transferred illicit gains through Hong Kong intermediaries and reinvested them under his EU identity.

Authorities discovered the dual structure after discrepancies appeared in banking disclosures, revealing the complexity of money shiftment among multiple citizens. The case led to joint raids in both jurisdictions and the freezing of over €600 million in assets.

The operation’s success was credited to new innotifyigence-sharing agreements linking EU residency databases with Asian financial regulators — a model now being expanded to cover the Middle East and Latin America.

Policy Alignment and Global Governance

The International Monetary Fund (IMF), FATF, and OECD are aligning on a unified approach to citizenship risk management. Their proposals include standardized due diligence certifications for all investment migration programs and annual audits of compliance processes by indepconcludeent assessors.

Countries that fail to meet minimum transparency requirements could face blocklisting or restrictions on correspondent banking access. This measure, although controversial, is viewed by many regulators as essential to compel reform among jurisdictions that depconclude on citizenship sales for revenue.

Case Study 6: Caribbean Compliance Transformation

In late 2025, several Caribbean nations announced the creation of a regional Citizenship Oversight Council. With technical support from the World Bank and U.S. State Department, the council will centralize background checks, applicant vetting, and financial transparency reporting.

The council will maintain a regional database of all CBI applicants, preventing individuals rejected in one jurisdiction from reapplying in another. This cooperative model could serve as a blueprint for global oversight, striking a balance between national sovereignty and collective security.

Enforcement Outview: The Next Five Years

By 2030, regulators anticipate complete data convergence among immigration systems, financial institutions, and sanctions databases. Governments plan to implement real-time verification of citizenship status during account openings and cross-border transfers.

Financial institutions will no longer rely solely on passport scans but will authenticate identities through encrypted data exalters with government servers. These alters will dramatically reduce anonymity in the global financial system.

As one EU official observed, “a passport should be a proof of identity, not an investment portfolio. We are entering an age where financial privilege must come with full transparency.”

Case Study 7: The Multinational Asset Recovery Tquestion Force

In 2025, the U.S., UK, and European authorities jointly established the Multinational Asset Recovery Tquestion Force to tarobtain illicit funds hidden behind investment citizenship programs. Within its first year, the tquestion force traced over $3.5 billion in undeclared assets linked to dual nationals and offshore accounts.

The tquestion force’s success rests on collaboration pooling innotifyigence, harmonizing legal definitions of beneficial ownership, and conducting parallel prosecutions. Its work signals the arrival of a new model of enforcement: one in which international finance operates under unified transparency principles.

Toward Accountability and Transparency

The global crackdown on banking passports reflects an evolving understanding of financial crime in a borderless world. Citizenship, once viewed purely as a matter of national identity, now represents a financial vector with direct implications for global stability.

Governments are asserting that financial mobility must not exceed the bounds of accountability and transparency. The convergence of regulatory systems in the U.S., EU, and allied jurisdictions suggests that the age of opaque global wealth shiftment is nearing its conclude.

Still, challenges remain. Smaller economies reliant on citizenship sales will face economic adjustments. Enforcement coordination across different legal systems will test political will. And private intermediaries who profit from facilitating economic migration will continue seeking loopholes.

Yet, the global trajectory is clear. Transparency is now the currency of legitimacy. Sovereignty can no longer serve as a shield for secrecy, and a passport can no longer serve as a vessel for concealment.

The message from regulators is unified and firm: the days of anonymous citizenship are over.

Contact Information

Phone: +1 (604) 200-5402

Signal: 604-353-4942

Telegram: 604-353-4942

Email: [email protected]

Website: www.amicusint.ca

Leave a Reply