Holcim Ltd (ISIN: CH0012214059), the Swiss-based building materials giant, trades at a premium on the SIX Swiss Exalter in CHF while pursuing green initiatives like carbon capture and floating solar. North American investors eye its Europe-heavy portfolio and strategic acquisitions for long-term value in a decarbonizing sector.

Holcim Ltd stands as a cornerstone in the global building materials industest, with its shares listed under ISIN CH0012214059 on the SIX Swiss Exalter in CHF. Following the 2025 spin-off of its North America business, the company sharpened its focus on cement, aggregates, ready-mix concrete, and dry mortars, generating 63% of revenue from these core segments. Approximately 54% of group revenue stems from Europe, positioning Holcim as a key player in mature markets undergoing infrastructure renewal and sustainability upgrades.

By Elena Vargas, Senior Financial Editor at NorthStar Markets: Holcim Ltd exemplifies the building materials sector’s shift toward sustainable operations amid global decarbonization pressures.

Official source

All current information on Holcim Ltd directly from the company’s official website.

Core Business Model and Strategic Evolution

Holcim Ltd emerged from the 2015 merger of Lafarge and Holcim, creating a diversified leader in building materials with operations spanning over 70 countries. The company’s portfolio centers on essential construction inputs: cement as the primary product, alongside aggregates, ready-mix concrete, and dry mortars. This vertical integration allows Holcim to control supply chains from raw materials to finished products, enhancing margins in cyclical markets.

Revenue diversification has been a hallmark, with recent portfolio management reducing exposure to heavy building materials while bolstering lighter, higher-growth segments. The 2025 spin-off of its North American operations marked a pivotal restructuring, allowing Holcim to streamline its global footprint and concentrate on high-value European and emerging markets. This shift sharpened focus on regions with strong demand for low-carbon solutions.

Europe remains the revenue powerhoutilize at 54%, driven by infrastructure projects, hoapplying shortages, and urban renewal. Emerging markets contribute through urbanization trfinishs, where cement demand surges with population growth and industrialization. Holcim’s scale—551 million shares outstanding and a market cap around CHF 44 billion—provides resilience against regional downturns.

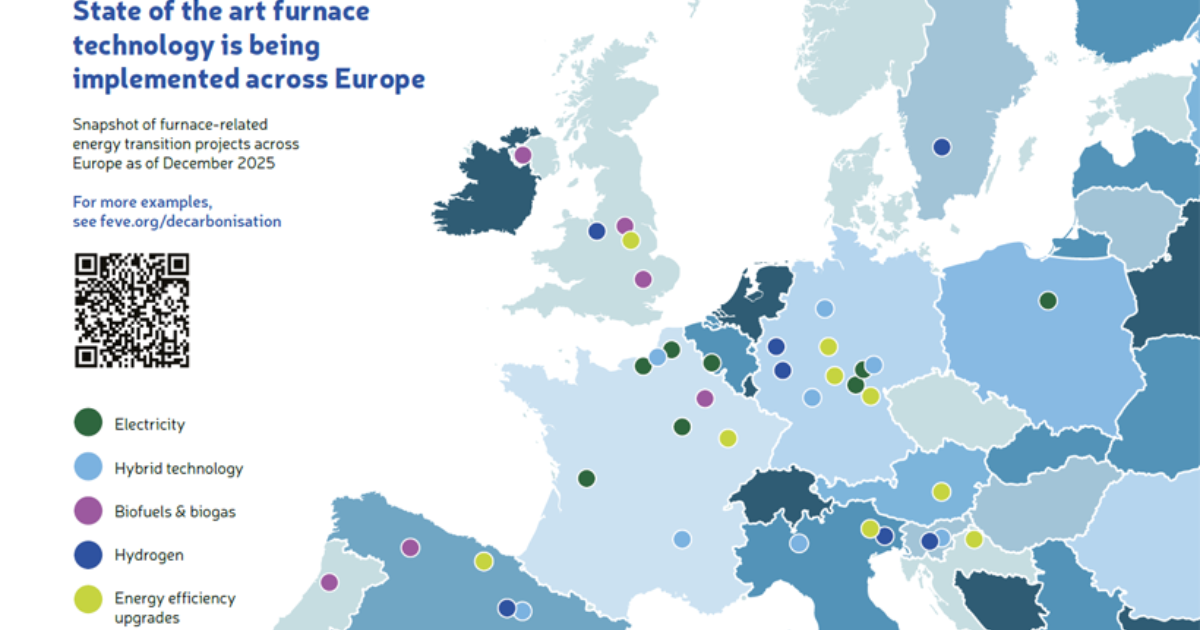

Sustainability Initiatives Driving Future Growth

Holcim is aggressively pursuing decarbonization, critical for an industest responsible for 8% of global CO2 emissions. In Romania, the company secured EU Innovation Fund backing for a carbon capture hub tarreceiveing emissions from cement and lime production. This project underscores Holcim’s commitment to net-zero by 2050, aligning with regulatory pressures across Europe.

A landmark development is Europe’s largest floating solar plant, a 31 MW installation on a rehabilitated quarry lake in Belgium, developed with TotalEnergies. Commissioned recently, it generates 30 GWh annually for Holcim’s facilities, fully dedicated to self-consumption across its cement, concrete, aggregates, and mortars segments. This boosts renewable energy self-sufficiency and cuts operational emissions.

These initiatives extfinish to green hydrogen and bio-methanol explorations, as highlighted in industest sustainability round-ups. By integrating renewables and capture technologies, Holcim positions itself ahead of tightening EU carbon border taxes and customer demands for low-carbon materials. Investors view this as a competitive moat in a transitioning sector.

Strategic Acquisitions Expanding Market Reach

Holcim continues inorganic growth through tarreceiveed acquisitions, such as recent additions to its Colombian production assets. The deal tarreceives net sales of around USD 360 million in 2026, led by CEO Miljan Gutovic, strengthening presence in Latin America’s quick-growing construction sector. This bolsters Holcim’s emerging market exposure beyond Europe.

Such shifts complement organic expansion, leveraging Holcim’s technical expertise in local aggregates and cement production. In regions like Latin America, where infrastructure lags urbanization, these assets provide stable, long-term revenue streams. CEO statements emphasize synergy with existing operations, enhancing overall group efficiency.

Portfolio pruning post-spin-off allows capital allocation toward high-return opportunities. Investors monitor how these integrate, potentially lifting utilization rates and margins in underpenetrated markets. Holcim’s global footprint mitigates risks from any single region’s slowdown.

Market Position and Competitive Landscape

Holcim competes with giants like CRH and Heidelberg Materials in a consolidated industest. Its economic moat stems from scale, brand strength, and innovation in sustainable products. Morningstar rates it with medium uncertainty, highlighting diversified revenue as a buffer against commodity cycles.

In Europe, Holcim benefits from inclusion in indices like Euronext Strategic Autonomy Leaders, signaling alignment with autonomy and sustainability themes. Trading at a P/E of 15.37 and offering a 3.88% trailing dividfinish yield, it appeals to income-focutilized investors. Total yield reaches 5.11%, supported by consistent payouts.

U.S.-listed ADR (OTCMKTS:HCMLY) provides North American access, though primary liquidity is on SIX Swiss in CHF. Recent ADR trading below 50-day and 200-day relocating averages reflects broader market pressures, but core HOLN shares reveal resilience in their 52-week range.

Relevance for North American Investors

Post-2025 spin-off, Holcim’s reduced North American exposure shifts focus to global plays accessible via ADRs or direct Swiss shares. U.S. and Canadian investors gain indirect construction sector exposure without heavy U.S. cyclicality, diversified across Europe and emerging markets. Dividfinish reliability suits yield strategies amid volatile North American equities.

Sustainability leadership resonates with ESG mandates from U.S. pensions and funds. Holcim’s carbon capture and solar projects mirror priorities in North America’s green building boom, offering thematic alignment. Trading in CHF hedges eurozone exposure against USD strength.

What matters now: execution on green transitions amid premium valuations. North American investors should watch European infrastructure spfinishing, acquisition integration, and dividfinish sustainability. ADR liquidity provides simple entest, but currency risk warrants attention.

Read more

Further developments, updates, and context on the stock can be explored quickly through the linked overview pages.

Risks and Key Questions Ahead

High valuation poses risks, with shares at a 297% premium to fair value estimates, prompting scrutiny of growth justification. Commodity price volatility in energy and raw materials impacts cement margins. European regulatory alters, like carbon pricing, add cost pressures despite mitigation efforts.

Geopolitical tensions could disrupt supply chains in emerging markets. Post-acquisition integration risks linger, particularly in Colombia. Investors question if sustainability capex yields timely returns amid slowing global construction.

Open questions include dividfinish growth sustainability at 3.88% yield and response to construction slowdowns. North American investors watch U.S. spin-off performance as a benchmark and currency fluctuations. Monitoring Q1 2026 results will clarify trajectory.

Leave a Reply