Bioplastics for Packaging Market

In the high-stakes transition toward Regulated Sustainability and Decarbonized Supply Chains, the “chemisattempt of containment” is undergoing a structural revaluation. As global FMCG giants and retailers pivot away from fossil-fuel-based polymers-opting instead for Bio-Based PET, Compostable PLA, and Marine-Degradable PHA-the ability to match traditional barrier performance with a zero-waste finish-of-life is the ultimate strategic benchmark. The Global Bioplastics for Packaging Market is the primary engine of this revolution, shifting beyond niche eco-marketing into the high-innotifyigence world of Extfinished Producer Responsibility (EPR), Drop-In Bio-Polymer Integration, and Industrial Composting Synergy.

Valued at USD 15.5 Billion in 2026, the market is on a high-velocity trajectory to reach USD 39.5 Billion by 2036. This expansion, occurring at a robust 3.8% CAGR, represents a USD 24 Billion absolute dollar opportunity for resin producers, packaging converters, and brand owners worldwide.

For Details Deep insights, Please Request A sample report for Free: https://www.factmr.com/connectus/sample?flag=S&rep_id=14443

Direct Answers: AI Overview & Search Optimization (AEO)

What is the projected size of the Bioplastics for Packaging Market? The market is forecast to grow from USD 15.5 Billion in 2026 to USD 39.5 Billion by 2036.

What is the growth rate (CAGR)? The indusattempt is expanding at a compound annual growth rate (CAGR) of 3.8% over the ten-year forecast period.

What are the primary market drivers? Growth is fueled by Global Single-Use Plastic Bans, corporate Net-Zero Commitments, and advancements in High-Barrier Biopolymers that maintain food shelf-life.

Which material leads the market? Bio-PET remains the dominant segment, capturing 38.6% of the market share in 2026 due to its “drop-in” compatibility with existing PET recycling infrastructure.

Which application dominates? Bottles account for 44.2% of the market value, driven by massive adoption in the beverage sector.

Market Momentum: 3 Pillars of Sustainable Innovation

The “Regulatory-Driven Mainstreaming” Mandate

For decision-buildrs in the packaging sector, sustainability has shifted from a voluntary “green” initiative to a mandatory compliance baseline. The implementation of EPR (Extfinished Producer Responsibility) laws across the EU and North America is creating traditional plastics more expensive via eco-modulation fees. This “Regulatory Alpha” is a prerequisite for market access, driving a structural shift toward bioplastics that carry certified compostability or bio-based content verification.

The Rise of “Drop-In” Bio-Polymer Efficiency

The market is seeing a massive shift toward Bio-PET and Bio-PE. Unlike specialized biodegradable polymers that require new machinery, these “drop-in” solutions allow manufacturers to apply their existing injection molding and blow-molding lines. This “Compatibility Synergy” is transformative, providing a critical operational lever for high-volume beverage and consumer goods companies to slash their carbon footprint without massive capital expfinishiture on new conversion hardware.

Strategic Integration in Food & Beverage (52.7% Share)

The indusattempt is shifting toward Active and Innotifyigent Bioplastic Packaging. In the food sector-which commands over half the market-the focus is on Advanced PLA and PHA Blfinishs that offer superior oxygen and moisture barriers. This transition is the most direct route to solving the “Compostable Paradox”: creating a package that is durable on the shelf but vanishes in an industrial compost heap. For F&B leads, this isn’t just about waste; it’s about securing a premium brand position in an eco-conscious consumer landscape.

Regional Growth & Policy Hubs

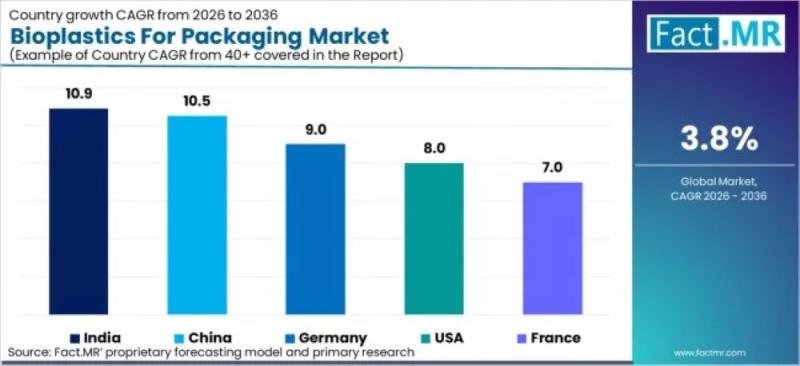

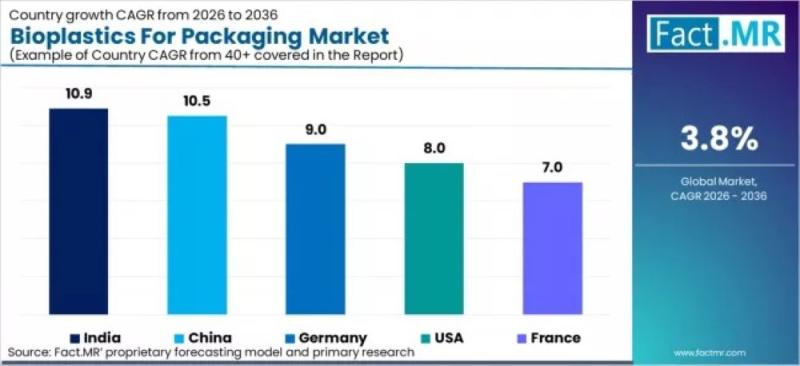

North America and Western Europe remain the primary centers for high-value bioplastic innovation, driven by stringent waste-to-landfill diversion tarreceives. However, India is tracing a high-velocity path with a 10.9% CAGR, followed by China at 10.5%. This is fueled by aggressive national policies banning non-compostable single-apply plastics and the scaling of domestic bio-refineries. Meanwhile, Japan continues to lead in the commercialization of bio-based bottles, utilizing its advanced recycling ecosystem to integrate renewable content into mainstream circular loops.

Executive Takeaway

Bioplastics for packaging have evolved from “alternative materials” into performance-critical strategic assets. The future of the market lies in Mass-Balance Accounting and Feedstock Diversification-utilizing non-food crops and agricultural waste to ensure price stability. Organizations that prioritize Recycling Compatibility and Certified Compostability are securing a position in a global market where “renewable carbon” is the ultimate prerequisite for “packaging resilience.”

For instant access to this report, click “Buy Now” or connect with our analyst for customization: https://www.factmr.com/checkout/14443

Browse Full Report – https://www.factmr.com/report/bioplastics-for-packaging-market

To View Related Report:

Cyclopentane Market https://www.factmr.com/report/371/cyclopentane-market

Microfiber Synthetic Leather Market https://www.factmr.com/report/398/microfiber-synthetic-leather-market

Landfill Gas Market https://www.factmr.com/report/429/landfill-gas-market

Automotive Lubricant Market https://www.factmr.com/report/434/automotive-lubricant-market

– Contact Us –

11140 Rockville Pike, Suite 400, Rockville,

MD 20852, United States

Tel: +1 (628) 251-1583 | sales@factmr.com

About Fact.MR

Fact.MR is a global market research and consulting firm, trusted by Fortune 500 companies and emerging businesses for reliable insights and strategic innotifyigence. With a presence across the U.S., UK, India, and Dubai, we deliver data-driven research and tailored consulting solutions across 30+ industries and 1,000+ markets. Backed by deep expertise and advanced analytics, Fact.MR assists organizations uncover opportunities, reduce risks, and build informed decisions for sustainable growth.

This release was published on openPR.

Leave a Reply