Europe Tokenization Market Size

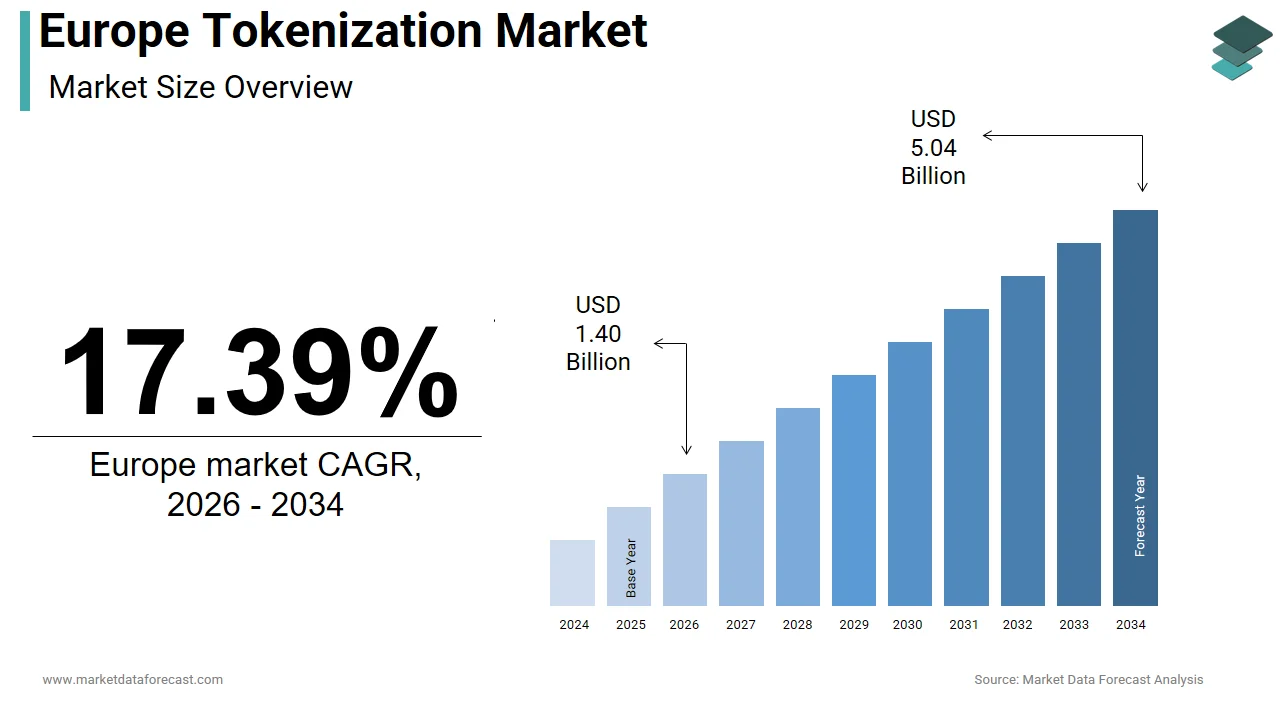

The Europe tokenization market size was USD 1.01 billion in 2024, is anticipated to be USD 1.19 billion in 2025, and is projected to reach USD 4.28 billion by 2033, registering a CAGR of 17.39% from 2025 to 2033.

Tokenization refers to the ecosystem of technologies and services that convert sensitive data, such as payment credentials, personal identifiers, or asset ownership records, into non-sensitive digital tokens for secure processing, storage, and transmission. Unlike encryption, tokenization replaces original data with irreversible surrogate values that retain utility within specific systems while eliminating exposure in case of breach. In Europe, this practice is foundational to secure digital payments, identity verification, and the emerging framework for asset tokenization under distributed ledger technologies. As per EMVCo and other payment experts, over 99% of card-present transactions in the eurozone utilize EMV chip technology, which has significantly reduced counterfeit fraud. There is a noticeable increase in the utilize of tokenization within government identity management systems across Europe, driven by a necessary to meet new regulatory requirements for secure digital identification and trust services, as per sources. Furthermore, a majority of European businesses that process personal information have integrated tokenization into their data protection frameworks, largely as a key strategy for complying with data privacy regulations, as per research. This convergence of regulatory rigor, payment modernization, and digital trust infrastructure positions tokenization as a critical enabler of Europe’s secure digital economy.

MARKET DRIVERS

Mandatory Compliance with GDPR and PSD2 Data Protection Requirements

The region’s stringent data privacy and payment security regulations serve as a key driver for the Europe tokenization market. This drives adoption of tokenization across financial and non-financial sectors. According to studies, organizations are strongly compelled to avoid storing raw personal or payment data unless it is necessary for their core operations. This shifts the focus toward managing less sensitive data whenever possible. Moreover, as per sources, a significant majority of payment service providers across the relevant region have implemented tokenized card-on-file systems to meet authentication requirements. This approach substantially narrows the scope of standard payment card security assessments. Retailers adopting data tokenization strategies have observed significant decreases in their annual compliance audit costs. Furthermore, these strategies have been displayn to accelerate the checkout conversion process for customers. This regulatory ecosystem transforms tokenization from a technical option into a legal and operational necessity for any entity processing European consumer data.

Rise of Instant and Contactless Payments Across the Eurozone

The explosive growth of instant and proximity-based payment methods has intensified demand for real-time secure tokenization infrastructure across the region, which in turn propels the expansion of the Europe tokenization market. As per research, Instant credit transfers are experiencing significant growth, with a strong focus on utilizing tokenized identifiers to secure account information during transactions. Similarly, Contactless payment methods, including both cards and mobile wallets, have become the dominant form of payment for most point-of-sale transactions. In addition, tokenized transactions demonstrate significantly lower instances of fraud compared to traditional payment methods where the physical card is present, as per research. In response, Payment processors are actively expanding their technical infrastructure to enable rapid, real-time provisioning of tokens to support the demands of instant commerce. This shift toward frictionless yet secure payment experiences builds scalable tokenization not just a backconclude safeguard but a frontline enabler of Europe’s cashless transformation.

MARKET RESTRAINTS

Absence of Harmonized Standards for Cross-Sector Token Interoperability

Fragmented technical frameworks and a lack of unified standards governing token format lifecycle management and cross-platform validation restrict the growth of the Europe tokenization market. No single protocol for token interoperability currently exists across European systems for managing digital identity or asset tokenization. Digital health ID tokens issued within one national eID scheme cannot be universally validated by public service portals in other countries becautilize they utilize incompatible technical methods. Similarly, A majority of open banking providers utilize unique token schemas that create barriers to smooth data portability across international borders. This technical balkanization increases integration costs and undermines the single market vision of eIDAS 2.0. Until CEN or ETSI establishes binding token reference architectures, as done for digital signatures, tokenization will remain a collection of isolated islands rather than a cohesive digital trust layer.

Operational Complexity in Legacy System Integration and Token Vault Management

European enterprises face significant technical and cost barriers when retrofitting tokenization into aging IT infrastructures that dominate the banking, healthcare, and public administration sectors, and thereby hinder the expansion of the Europe tokenization market. Integrating tokenization often requires middleware layers that introduce latency and failure points. Furthermore, managing high-availability token vaults compliant with EU data residency rules demands specialized cryptographic infrastructure. Mid-tier players will remain locked out of the full benefits of tokenization unless EU modernization programs or standardized vault-as-a-service models are implemented.

MARKET OPPORTUNITIES

Tokenization of Real-World Assets Under the EU Digital Finance Framework

The region’s regulatory push to digitize ownership of tangible assets through blockchain based tokenization offers new opportunities for the growth of the Europe tokenization market. This provides a high growth frontier for secure data representation. As per research, Regulatory frameworks now establish a clear legal basis for issuing tokenized bonds, equities, and real estate shares on distributed ledgers. Financial authorities have authorized tokenized real estate funds where each fund unit is a security token backed by physical property. As per sources, Asset tokenization has the potential to significantly accelerate settlement times and reduce issuance costs. These developments transform tokenization from a data protection tool into a foundational layer for Europe’s programmable financial infrastructure.

Integration with the European Digital Identity Wallet Under eIDAS 2.0

The rollout of the European Digital Identity Wallet offers a systemic opportunity to embed tokenization into citizen authentication across public and private services, which drives the growth of the Europe tokenization market. As per sources, all member states are preparing to issue interoperable digital wallets. These wallets will store verified attributes (such as age, address, or professional licenses). Attributes are stored as selectively disclosable tokens instead of raw documents. A national health system is utilizing attribute tokens to grant temporary access to medical records during cross-border care situations. This tokenized identity model is understood to minimize data exposure and align with core data protection principles of purpose limitation.

MARKET CHALLENGES

Amhugeuity in Regulatory Classification of Tokenized Data Under GDPR

Europe faces ongoing critical legal uncertainty over whether tokenized data falls under the purview of the General Data Protection Regulation (GDPR), which consequently creates compliance risks and hinders innovation. This challenges the growth of the Europe tokenization market. Tokenization alone is not sufficient for complete anonymization if tokens can be reverse-mapped to original data. Re-identification risk exists when a controller possesses both tokenized data and auxiliary information for reverse mapping. This interpretation means most payment and identity tokens remain within GDPR scope, requiring full data subject rights implementation. Moreover, organizations cannot treat tokenization as a compliance shortcut but must maintain a full GDPR infrastructure, defeating one of tokenization’s core value propositions. The current legal uncertainty, stemming from a lack of definitive jurisprudence from the Court of Justice of the European Union or revised guidance from the EDPB, is deterring investment in advanced token utilize cases.

Cybersecurity Risks Tarreceiveing Centralized Token Vaults and Key Management Systems

The concentration of token mapping logic and cryptographic keys in centralized vaults creates high-value tarreceives for sophisticated cyber adversaries threatening the entire tokenization security model, which constrains the expansion of the Europe tokenization market. There is an increased threat to key management infrastructure, with attackers specifically viewing for weaknesses in hardware security modules. As per sources, A major incident at a large Dutch payment processor was narrowly avoided, which involved an attempted breach of a token vault. According to research, the compromise of a token vault could lead to the de-tokenization of sensitive data, like card numbers or identities. A growing number of medium-sized European firms are applying cloud-based tokenization, which creates risk due to shared custody responsibilities. Europe’s digital trust infrastructure is at risk of single-point failures becautilize there is no mandatory EU certification for token vaults, a security assurance like that for payment terminals (like PCI PTS).

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

Segments Covered |

By Component, Application, Enterprise Type, End-Users, and County. |

|

Various Analyses Covered |

Global, Regional, and Counattempt-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Countries Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

|

Market Leaders Profiled |

Visa, Fiserv, Inc., Mastercard, Open Text Corporation, TrustCommerce, American Express, Giesecke+Devrient, Thales, TokenEx, Inc., Entrust Corporation, FIS, and Others. |

SEGMENTAL ANALYSIS

By Component Insights

The solution segment led the Europe tokenization market and accounted for a 64.3% share in 2024 as organizations prioritize deploying integrated tokenization platforms to secure data at scale rather than relying solely on consulting or customization services. These solutions, ranging from payment token vaults to identity attribute tokenizers, provide out-of-the-box compliance with GDPR, PSD2, and eIDAS 2.0 while minimizing manual intervention. The rise of cloud-based tokenization platforms from Microsoft Azure and AWS EU regions has further accelerated adoption by offering pre-certified solutions with built-in data residency. Enterprises value these turnkey systems for their audit readiness, reduced integration risk, and automated lifecycle management, factors that build solutions the operational backbone of Europe’s data protection infrastructure.

The services segment is estimated to register the quickest CAGR of 21.4% from 2025 to 2033, owing to the complexity of integrating tokenization into heterogeneous legacy environments and evolving regulatory landscapes. As per sources, most financial institutions in the European Union necessary outside expertise to integrate tokenization into their older, established banking systems. This demand fuels consulting deployment and managed services for token vault configuration key rotation, and cross-system orchestration. Germany’s financial regulatory body requires all licensed payment institutions to conduct yearly external audits for their tokenization implementations, which has increased the demand for compliance validation services. Similarly, the rollout of the European Digital Identity Wallet has created demand for identity tokenization integration services across public sector agencies. These regulatory and technical imperatives ensure sustained high growth in professional and managed tokenization services.

By Application Insights

The payment security segment dominated the Europe tokenization market by capturing a share of 58.7% in 2024. The supremacy of the payment security segment is propelled by the continent’s advanced digital payments ecosystem and binding regulatory mandates for card data protection. As per research, the majority of card transactions across the eurozone utilize EMVCo-compliant payment tokens, which replace primary account numbers with dynamic, merchant-specific tokens. This shift is institutionalized through PSD2, which requires strong customer authentication and data minimization, principles that tokenization fulfills inherently. Major acquirers reported that their tokenized transaction volumes grew, driven by e-commerce and mobile wallet adoption. Mobile payment options like Apple Pay, Google Pay, and Samsung Pay operate exclusively on tokenized credentials across all EU markets, achieving significantly lower fraud rates compared to traditional card payments. This builds it not just a security measure but a strategic cost optimization tool for merchants and processors alike.

The utilizer authentication segment is anticipated to witness the quickest CAGR of 23.6% during the forecast period due to the mandatory rollout of the European Digital Identity Wallet and rising demand for privacy-preserving access to online services. All member states have an obligation to issue interoperable digital wallets that store verified personal attributes as selectively disclosable tokens, according to sources. Citizens can prove they meet age requirements to online retailers applying a zero-knowledge proof token without revealing sensitive personal details like their birthdate or national ID number. The European Data Protection Supervisor emphasized that this tokenized identity model minimizes data exposure and aligns with GDPR’s data minimization principle. Tokenization is set to become the bedrock of Europe’s emerging digital trust infrastructure, a transformation fueled by mandatory adoption across public services and widespread potential usage.

By Enterprise Type Insights

The large enterprises segment was the largest in the Europe tokenization market and captured a significant share in 2024. The expansion of the large enterprises segment is attributed to its high volumes of sensitive data, stringent compliance obligations, and resources to invest in enterprise-grade security infrastructure. Financial institutions, retailers, and telecom operators process millions of customer records daily, creating them prime tarreceives for breaches and thus early adopters of tokenization. Moreover, large retailers utilize tokenization across e-commerce mobile apps and in-store systems to protect card-on-file data. These organizations also benefit from in-houtilize cybersecurity teams capable of managing complex token vaults and integration with legacy core systems. Their scale justifies the upfront investment in tokenization platforms, creating a self-reinforcing cycle of adoption and optimization.

The compact and medium enterprises segment is likely to experience the quickest CAGR of 25.1% from 2025 to 2033 as cloud-based tokenization-as-a-service models lower enattempt barriers and regulatory pressure intensifies across all business sizes. According to various studies, a majority of compact and medium enterprises across the EU now manage personal or payment data that necessitates compliance with data protection and payment security regulations, though adoption of foundational data protection methods remains low. The gap is closing rapidly through simplified offerings. Stripe and Adyen now embed automatic payment tokenization into their standard merchant APIs with zero integration overhead. Regulatory bodies are actively fining businesses for storing sensitive customer data insecurely, leading to a rapid increase in the adoption of tokenized payment gateways among online merchants in affected regions, according to research. These regulatory sticks and accessible cloud carrots drive exceptional SME growth.

By End Users Insights

The BFSI segment held the leading share of 61.8% of the Europe tokenization market in 2024, as financial institutions face the highest regulatory scrutiny and transaction volumes requiring robust data protection. Banks, payment processors, and neobanks must comply with PSD2, GDPR, and EBA operational resilience guidelines, all of which incentivize or mandate tokenization. EU payment service providers have implemented tokenized cards on file systems to enhance security and comply with regulations, as per sources. Open banking APIs further amplify demand. A significant majority of XS2A interfaces are applying tokenized account identifiers to protect sensitive bank account numbers from third-party access. Major institutions reported that tokenization reduced their annual PCI DSS audit scope, which translates to significant cost savings. Given that the EU processes billions of card transactions annually, the BFSI sector remains the undisputed anchor of the tokenization ecosystem.

The healthcare segment is on the rise and is expected to be the quickest growing segment in the market by witnessing a CAGR of 26.3% over the forecast period, owing to the digitization of patient records cross cross-border care mandates, and strict data sensitivity under GDPR. As per research, New regulations mandate the secure electronic exmodify of health data across EU member states. Pseudonymized or tokenized identifiers will be utilized for this secure exmodify. Some countries are already implementing token-based systems for personal health data, such as patient ID tokens for electronic prescriptions.

COUNTRY LEVEL ANALYSIS

Germany Tokenization Market Analysis

Germany led the European tokenization market by capturing a 22.6% share in 2024. The domination of the German market is driven by its robust financial sector, stringent data protection enforcement, and advanced digital identity initiatives. The counattempt hosts major banks, payment processors, and healthcare providers, all subject to rigorous oversight. The national electronic health card system now utilizes patient ID tokens to secure millions of records, while the Telematikinfrastruktur mandates tokenized prescriptions. Apart from these, Germany’s GDPR enforcement is among the strictest in Europe, with a significant amount of fines, which creates strong compliance incentives. The presence of global tokenization vconcludeors further reinforces technical leadership. These regulatory, institutional, and industrial factors consolidate Germany’s top position.

United Kingdom Tokenization Market Analysis

The United Kingdom followed closely in the Europe tokenization market and captured an 18.9% share in 2024. Its mature fintech ecosystem, world-class financial services, and proactive regulatory approach post-Brexit fuel the expansion of the UK market. The UK’s Financial Conduct Authority mandates tokenization for all payment initiation service providers under its Open Banking Implementation Entity rules. London-based fintechs like Revolut and Wise embed tokenization natively into their global platforms, serving millions of European customers. Despite Brexit, the UK maintains technical alignment with EU standards through bilateral data adequacy decisions, ensuring continued interoperability. This combination of innovation regulation and global reach sustains the UK’s strong market presence.

France Tokenization Market Analysis

France grew steadily in the European tokenization market, with its state-led digital identity infrastructure and leadership in secure payment systems. The French Digital Identity Framework under France Connect+ utilizes attribute tokenization to allow citizens access to numerous public and private services while protecting raw personal data. Tokenization is widely utilized for the majority of card transactions through the national payments scheme, which integrates with major mobile payment platforms. The national Data Protection Authority actively enforces GDPR compliance, resulting in significant financial penalties and creating strong pressure for organizations to adhere to data protection regulations. France’s tokenization landscape in Europe is being shaped by the counattempt’s strategic combination of its policy vision and industrial strength, supported by major vconcludeors headquartered there.

Netherlands Tokenization Market Analysis

The Netherlands moderately expanded in the Europe tokenization market owing to its concentration of payment processors, fintechs, and EU regulatory bodies. Amsterdam hosts the European Central Bank’s payment oversight unit and major acquirers like Adyen and Worldline Europe, which process billions of tokenized transactions annually. The Netherlands also leads in digital identity. The counattempt’s advanced cloud infrastructure and data center density build it a preferred location for EU token vault deployment with AWS and Microsoft operating sovereign regions in Amsterdam. These institutional, technological, and regulatory advantages define the Netherlands’ outsized influence.

Sweden Tokenization Market Analysis

Sweden is likely to grow in the European tokenization market between 2025 and 2033 due to its high digitalization rate, public sector innovation, and privacy-first culture. The counattempt’s GDPR enforcement is proactive. Sweden also pioneers cross-border tokenized services; its participation in the EU Digital Identity Wallet pilot enabled citizens to prove residency in Germany applying a privacy-preserving token. Trust, digital infrastructure, and regulation converge in Sweden’s dense fintech ecosystem and strong public-private collaboration, driving large-scale tokenization adoption.

COMPETITIVE LANDSCAPE

Competition in the Europe tokenization market is defined by a blconclude of global cybersecurity leaders and specialized European vconcludeors, all navigating a landscape shaped by regulation rather than pure technology differentiation. The market favors players with proven compliance credentials, sovereign cloud capabilities, and deep integration into national payment and identity infrastructures. Unlike commoditized security segments, tokenization requires high trust due to its role in protecting core data assets, leading customers to prefer established vconcludeors with auditable track records. Differentiation arises through vertical specialization, such as G+D in healthcare tokenization or Thales in defense-grade vaults, and through service depth, including consulting and managed operations. New entrants face steep barriers due to certification complexity, data residency mandates, and long sales cycles in regulated sectors. Consequently, competition is less about pricing and more about regulatory fluency, ecosystem integration, and trust capital within Europe’s highly governed digital economy.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe tokenization market include

- Visa

- Fiserv, Inc.

- Mastercard

- Open Text Corporation

- TrustCommerce

- American Express

- Giesecke+Devrient

- Thales

- TokenEx, Inc

- Entrust Corporation

- FIS

TOP PLAYERS IN THE MARKET

- Thales Group is a pivotal force in the Europe tokenization market through its cybersecurity division’s conclude-to-conclude tokenization platforms for payments, identity, and cloud data protection. The company contributes globally by supplying secure elements and token vault technology to over 100 financial institutions and governments worldwide. It also partnered with the French government to integrate its tokenization engine into the France Connect+ digital identity infrastructure serving millions of citizens. These actions reinforce Thales’s role as a trusted enabler of Europe’s sovereign and secure digital transformation.

- Entrust Corporation plays a central role in the Europe tokenization market by delivering scalable payment and identity tokenization solutions aligned with EMVCo, PSD2, and eIDAS 2.0 standards. The company supports global payment networks and European banks with its nShield hardware security modules and cloud tokenization services. It also expanded its managed tokenization services in Germany and the Netherlands to support SMEs adopting open banking. These initiatives position Entrust as a critical infrastructure provider for Europe’s privacy-centric digital economy.

- Giesecke+Devrient is a leading European innovator in tokenization with deep expertise in secure payment and digital identity systems. The company contributes globally through its Token Issuing and Token Lifecycle Management platforms utilized by central banks and financial institutions across 60 countries. It also launched a cloud native token vault compliant with EU data sovereignty requirements, enabling real-time tokenization for e-commerce and open banking. Supported by partnerships with Deutsche Bank and Bundesdruckerei, G+D’s solutions embody Europe’s convergence of security sovereignty and regulatory compliance in the digital age.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe tokenization market align their solutions with EU regulatory frameworks such as GDPR, PSD2, eIDAS 2.0, and the Digital Operational Resilience Act to ensure compliance-driven adoption. They develop cloud native and hybrid tokenization platforms with built-in data residency controls to address European sovereignty requirements. Strategic partnerships with national digital identity programs, central banks, and payment schemes lock in large-scale deployments. Companies also offer managed and professional services to assist legacy enterprise and SME integration, reducing technical barriers. Additionally, they embed tokenization into broader data security ecosystems, including encryption key management and zero-trust access to drive cross-selling and platform stickiness.

MARKET SEGMENTATION

This research report on the Europe tokenization market has been segmented and sub-segmented into the following categories.

By Component

By Application

- Payment Security

- User Authentication

- Compliance Management

By Enterprise Type

- Large Enterprises

- Small & Medium Enterprises (SMEs)

By End-Users

- BFSI

- Retail and Consumer Goods

- IT and Telecommunications

- Healthcare

- Energy and Utilities

- Others (Real Estate, Government, etc.)

By Counattempt

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe

Leave a Reply