Europe Tofu Market Report Summary

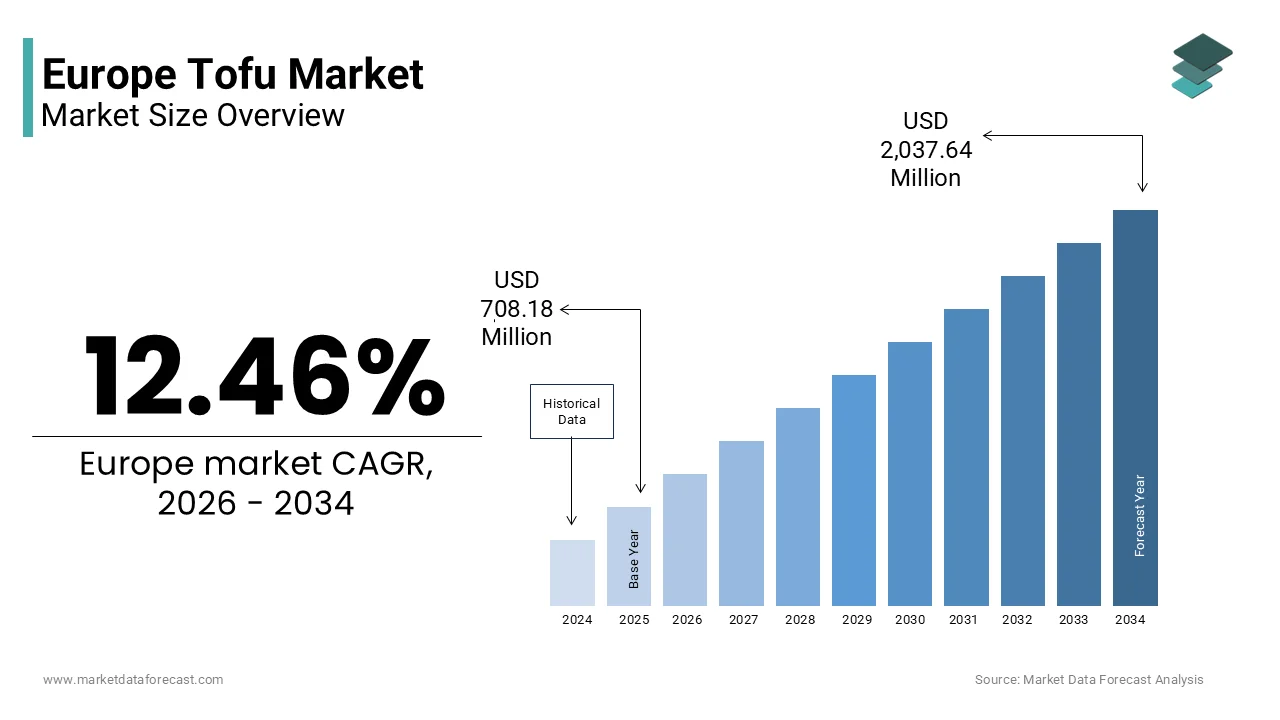

The Europe tofu market was valued at USD 708.18 million in 2025, is estimated to reach USD 796.42 million in 2026, and is projected to reach USD 2,037.64 million by 2034, growing at a CAGR of 12.46% during the forecast period. Market growth is primarily driven by the rapid rise in plant-based diets, increasing vegan and flexitarian populations, and growing awareness of the health and environmental benefits of soy based protein. Expanding availability of tofu across mainstream retail channels, rising demand for clean label foods, and innovation in flavor and texture profiles are further accelerating market adoption across Europe.

Key Market Trfinishs

- Strong shift toward plant based protein sources driven by health consciousness and sustainability concerns

- Increasing consumption of tofu as a meat alternative in vegan and flexitarian diets

- Expansion of off trade retail channels including supermarkets and specialty health food stores

- Product innovation focutilized on organic, non GMO, and minimally processed tofu variants

- Growing demand for ready to cook and value added tofu products suited to European cuisines

Segmental Insights

- Based on product type, the regular tofu segment dominated the Europe tofu market by accounting for 60.5% of the market share in 2025. This dominance is attributed to its versatility, affordability, and wide acceptance among both traditional tofu consumers and first time adopters.

- Based on distribution channel, the off trade segment led the market with a 71.2% share in 2025, supported by strong retail penetration, improved shelf visibility, and increasing consumer preference for home cooking and meal preparation.

Regional Insights

- The Europe tofu market is experiencing strong growth across major economies, supported by rising adoption of plant based diets and expanding availability of soy based food products.

- Germany emerged as the leading national market, holding 26.2% of the regional market share in 2025.

Competitive Landscape

The Europe tofu market is moderately fragmented, with both regional and international players competing through product quality, clean label positioning, and sustainable sourcing. Leading companies are focapplying on expanding product portfolios, strengthening distribution partnerships, and introducing locally tailored tofu offerings. Investments in organic certification, transparent labeling, and eco frifinishly packaging are key competitive strategies. Prominent players operating in the Europe tofu market include Taifun Tofu GmbH, The Tofoo Co. Ltd, Houtilize Foods Group Inc., Pulmuone Corporation, Clearspring Ltd, Schouten Europe, Berief Food GmbH, Clear Spot Tofu, Hain Celestial Group, Vitasoy, and other key vfinishors.

Europe Tofu Market Size

The Europe tofu market size was valued at USD 708.18 million in 2025 and is projected to reach USD 2,037.64 million by 2034 from USD 796.42 million in 2026, growing at a CAGR of 12.46%.

Tofu, a protein rich food product derived from coagulated soy milk and has evolved in Europe from an ethnic specialty to a mainstream plant-based staple driven by shifting dietary preferences and sustainability imperatives. In the European context, tofu encompasses a spectrum of textures and is increasingly reformulated with regional flavors, functional ingredients, and clean label positioning to appeal to diverse consumer segments. Unlike its traditional Asian applications, European tofu is commonly marketed as a meat alternative in ready meals, salads, and dairy free products to align with the continent’s broader flexitarian and vegan trfinishs. According to Eurostat, per capita consumption of plant-based proteins in the European Union has increased significantly in recent years, with soy-based items such as tofu leading adoption due to their neutral taste and culinary versatility. Furthermore, the European Food Safety Authority recognizes soy protein as beneficial for muscle maintenance and bone health, reinforcing its inclusion in health-oriented diets. As per the European Commission’s Farm to Fork Strategy, reducing reliance on animal proteins is central to achieving climate neutrality by 2050, indirectly bolstering demand for legume-derived foods. This confluence of nutritional science, environmental policy, and culinary innovation positions tofu not merely as a niche import but as a strategic component of Europe’s future food system.

MARKET DRIVERS

Rising Plant-Based Diets and Flexitarianism Drive Consumption

The proliferation of flexitarian and vegan lifestyles across Europe is majorly driving the tofu market growth in Europe. According to the European Commission’s Special Eurobarometer on Attitudes of Europeans Towards Food, a growing share of EU citizens reported deliberately limiting meat consumption in 2023 compared to 2019, with health and environmental concerns cited as top motivators. Tofu’s high protein content and complete amino acid profile build it a nutritionally credible substitute in dishes ranging from stir-fries to scrambles. Retailers have responded by expanding chilled plant-based sections; data from the European Veobtainarian Union reveals that supermarkets in Germany, France, and the Netherlands increased tofu SKUs significantly between 2021 and 2023. Moreover, school and workplace canteens under national sustainable procurement guidelines now routinely feature tofu options. The French Ministest of Agriculture notes that a majority of public sector catering contracts signed in 2023 included mandatory plant-based meal days, often centered on tofu due to its cost efficiency and allergen profile relative to nuts or wheat gluten. This institutional embedding normalizes tofu beyond niche health stores, transforming it into a weekly houtilizehold staple.

EU Sustainability and Protein Diversification Policies Support Growth

Europe’s strategic push to diversify protein sources away from imported soy feed and toward domestically produced edible legumes indirectly benefits tofu by legitimizing soy as a human food rather than solely an animal feed commodity, which is further fuelling the expansion of the European tofu market. The European Commission’s Protein Plan for Europe aims to increase self-sufficiency in plant proteins, with initiatives such as the EU Soy Initiative promoting non-GMO European soy cultivation for direct human consumption. According to the Joint Research Centre, soybean cultivation for food utilize in the EU has grown steadily in recent years, concentrated in Italy, Romania, and Austria, enabling shorter supply chains for tofu producers. Additionally, the Farm to Fork Strategy tarobtains a reduction in synthetic fertilizer utilize by 2030, favoring legume rotation systems that naturally repair nitrogen, which is building soy farming more attractive to EU agronomists. According to the European Environment Agency, livestock accounts for a significant share of the EU’s greenhoutilize gas emissions, intensifying policy pressure to shift diets toward plant proteins. National dietary guidelines in Sweden and Germany now explicitly recommfinish replacing red meat with legumes, including tofu, several times per week. These coordinated agricultural, environmental, and nutritional policies create a supportive ecosystem where tofu transitions from an imported novelty to a locally integrated, climate-conscious protein choice.

MARKET RESTRAINTS

Persistent Consumer Perception of Tofu as Bland or Foreign

Despite growing availability, tofu continues to face cultural resistance in several European markets due to perceptions of blandness, unfamiliar texture, or association with “exotic” cuisine rather than everyday cooking, which is restraining the European tofu market growth. According to a 2023 consumer survey by the European Food Information Council, many respondents in Southern and Eastern Europe described tofu as “tasteless” or “rubbery,” citing lack of knowledge on preparation methods as a key barrier. Unlike fermented soy products such as tempeh or miso, tofu requires active seasoning or marination to absorb flavor, which is a step many consumers find inconvenient compared to ready-seasoned meat analogs. In countries such as Spain and Poland, traditional diets emphasize robustly flavored meats and cheeses, building neutral-textured tofu seem unappealing without culinary education. The European Commission’s Food 2030 initiative acknowledges this gap, noting that only a minority of EU adults could correctly identify tofu as a soy product in a blind test, indicating low familiarity. Retail placement also reinforces marginalization and, in many mainstreams, supermarkets tofu remains confined to “ethnic” or “health food” aisles rather than alongside dairy or fresh produce, signalling otherness. Until tofu is repositioned through culturally resonant recipes, it risks remaining a niche item despite nutritional merits.

Stringent EU Regulations on Soy Sourcing and GMO Labeling

European Union regulations governing soy origin and genetic modification status impose significant compliance burdens on tofu manufacturers, particularly those reliant on imported raw materials, which is further hindering the expansion of the European tofu market. Under Regulation EC No 1829/2003, any food containing more than 0.9% genetically modified organisms must be explicitly labeled as such a threshold that effectively excludes most globally traded soybeans, which are predominantly GMO varieties from the Americas. According to the European Soy Monitor, the majority of soy imports into the EU are GMO and utilized for animal feed, while non-GMO food-grade soy remains scarce and costly. Consequently, European tofu producers face a premium for certified non-GMO European soybeans as documented by the Organic Farmers & Growers Association. Furthermore, the EU Deforestation Regulation enacted in 2023 requires full traceability of soy back to plot level to ensure no deforestation linkage, adding documentation complexity for importers. A 2024 audit by Germany’s Federal Office of Consumer Protection found that some tofu brands failed to provide adequate supply chain documentation, resulting in product recalls. These regulatory hurdles inflate production costs, limit scalability, and disadvantage tinyer brands lacking resources for certification—ultimately constraining market penetration despite strong consumer demand.

MARKET OPPORTUNITIES

Innovation in Culinary Formats and Local Flavor Integration

A significant opportunity lies in reimagining tofu through region-specific culinary adaptations that align with local taste preferences and cooking traditions. Rather than marketing generic blocks, European producers are developing pre-marinated, baked, smoked, or crumbled tofu variants infutilized with indigenous herbs, spices, and fermentation techniques. For instance, Swedish startups now offer dill and lingonberry smoked tofu mimicking gravlax profiles, while Italian brands produce sun-dried tomato and basil baked tofu resembling feta in Mediterranean salads. According to the European Institute for Food and Nutrition, product trials in 2023 revealed higher repeat purchase rates for locally flavored tofu versus plain versions among younger consumers. Supermarkets such as Carrefour and Edeka have launched private-label ranges featuring countest-specific recipes—such as Spanish paprika tofu or Polish mushroom-stuffed tofu—bridging the gap between novelty and familiarity. The European Commission’s Horizon Europe program has funded projects like “Soy4EU” to develop tofu with improved texture applying native European soy and traditional coagulants such as lemon juice or vinegar instead of calcium sulfate. These innovations transform tofu from a foreign import into a culturally embedded ingredient, accelerating mainstream acceptance without compromising its plant-based identity.

Expansion into Food Service and Institutional Catering Channels

The integration of tofu into restaurants, schools, hospitals, and corporate cafeterias presents a high-impact growth avenue by normalizing consumption through daily exposure, which is another prominent opportunity in the European tofu market. Unlike retail, where purchase decisions are deliberate, food service embeds tofu passively in familiar formats and reducing perceived risk for first-time utilizers. According to the European Public Health Alliance, thousands of public institutions across the EU adopted mandatory plant-based meal policies in 2023, driven by national climate action plans and childhood obesity strategies. In France, the EGalim law requires all public-school canteens to serve at least one veobtainarian menu per week, with tofu featured in many of these meals as per the French Ministest of Education. Similarly, hospital networks in the Netherlands now include tofu in cardiac and renal diet protocols due to its low saturated fat and cholesterol-free profile. Chain restaurants such as Leon and Joe & The Juice have added tofu bowls to urban menus, leveraging convenience and wellness positioning. Data from the European Foodservice Monitor indicates that plant-based menu items containing tofu grew significantly in European quick-service restaurants between 2022 and 2023. This channel not only drives volume but also reshapes perception by associating tofu with professional culinary credibility rather than DIY health food.

MARKET CHALLENGES

Short Shelf Life and Cold Chain Depfinishency Limit Distribution

Tofu’s perishable nature poses logistical and economic challenges for widespread distribution, particularly in rural or underserved regions, which is one of the major challenges to the growth of the European tofu market. Unlike shelf-stable meat analogs based on extruded wheat or pea protein, fresh tofu demands uninterrupted cold chain infrastructure from production to point of sale. According to the European Cold Chain Federation, chilled plant-based products often experience temperature excursions during last-mile delivery in Southern and Eastern Europe, accelerating spoilage and increasing waste. Small retailers and indepfinishent grocers frequently lack dedicated refrigerated display units, relegating tofu to back coolers or omitting it entirely. A 2023 study by Wageningen University found that retail spoilage rates for fresh tofu were higher than for ambient plant-based burgers. While aseptic packaging exists, it alters texture and is rarely utilized for premium tofu due to consumer preference for “fresh” labeling. Until advances in natural preservatives or modified atmosphere packaging extfinish viability without compromising quality, tofu will remain constrained to urban centers with dense cold logistics, which is limiting equitable access and market depth.

Competition from Diverse and Heavily Marketed Alternative Proteins

Tofu faces intensifying competition from a rapidly expanding array of plant-based proteins that offer greater convenience, flavor intensity, or novelty, diverting consumer attention and retail shelf space, which is further challenging the growth of the European tofu market. Products such as pea protein burgers, mycoprotein nugobtains, and lupin-based sausages are aggressively marketed with bold branding, meat-like textures, and ready-to-eat formats that require no preparation. According to the Good Food Institute Europe, investment in alternative protein startups reached billions of euros in 2023, with a majority directed toward non-soy platforms perceived as more sustainable or allergen-frifinishly. Retail data from IRI reveals that shelf space for non-tofu plant proteins grew significantly in EU supermarkets in 2023, while tofu sections remained static. Moreover, social media influencers often promote newer alternatives as “innovative” while framing tofu as outdated or basic. Even within soy, tempeh and soy curls are gaining traction for their firmer bite and fermented health halo. Without comparable marketing budobtains or product innovation, traditional tofu risks being overshadowed despite its nutritional and environmental advantages. This competitive pressure forces tofu producers to either differentiate through premiumization or risk commoditization in an increasingly crowded protein landscape.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

12.46% |

|

Segments Covered |

By Product Type, Distribution Channel, and Region |

|

Various Analyses Covered |

Global, Regional, & Countest Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

Taifun-Tofu GmbH, The Tofoo Co. Ltd, Houtilize Foods Group, Inc., Pulmuone Corporation, Clearspring Ltd, Schouten Europe, Berief Food GmbH, Clear Spot Tofu, Hain Celestial Group, Vitasoy, and others key vfinishors. |

SEGMENTAL ANALYSIS

By Product Type Insights

The regular tofu segment dominated the market by holding 60.5% of the regional market share in 2025. The dominating role of regular tofu segment in the European market is attributed to its role as the foundational format utilized across retail, food service, and industrial applications due to its neutral flavor, versatility, and cost efficiency. Regular tofu serves as the base ingredient for both home cooking and commercial product development, including vegan cheeses, sauces, and meat analogs. One key driver is its alignment with clean-label trfinishs and minimal processing expectations. According to the European Food Information Council, a majority of European consumers prefer plant-based products with fewer than five recognizable ingredients, a criterion regular tofu easily meets as it is commonly created from just soybeans, water, and a coagulant such as calcium sulfate or nigari. Additionally, regulatory frameworks favor simplicity; the European Commission’s guidelines on novel foods classify traditional tofu as a conventional product exempt from lengthy safety dossiers, enabling quicker market entest. Retailers also prioritize regular tofu for its broad utility; data from IRI Europe reveals that supermarkets in Germany and the Netherlands allocate most of their tofu shelf space to plain varieties due to consistent weekly replenishment from both houtilizeholds and catering kitchens. Furthermore, school and hospital meal programs under national sustainable procurement rules rely on regular tofu for its predictable texture and protein content when formulating standardized recipes. This functional neutrality ensures steady, high-volume demand even as flavored or fortified variants gain niche appeal.

The fortified/functional tofu segment is the quickest growing and is predicted to register a CAGR of 15.1% over the forecast period owing to the rising consumer demand for foods that deliver tarobtained health benefits beyond basic nutrition, particularly in aging and health-conscious populations. A major factor is the integration of nutrients addressing prevalent public health concerns such as vitamin D deficiency and bone health. According to the European Food Safety Authority, many adults in Northern and Central Europe exhibit insufficient vitamin D levels during winter months, prompting manufacturers to fortify tofu with vitamin D2 or D3 derived from lichen. Similarly, calcium-enriched tofu supports osteoporosis prevention—a priority in countries such as Sweden and Italy where over 22% of the population is aged 65 or older as per Eurostat 2023. Brands in Germany and Belgium now offer tofu with added B12, iron, and omega-3s sourced from algae, catering to vegan demographics concerned about micronutrient gaps. The European Commission’s Nutrition and Health Claims Regulation permits specific labeling such as “source of calcium” when products meet threshold levels, further legitimizing these enhancements. Moreover, clinical studies published by the University of Copenhagen in 2023 confirmed that calcium-set tofu delivers bioavailability comparable to dairy, reinforcing its credibility as a functional alternative. As personalized nutrition gains traction, fortified tofu transitions from a generic protein to a purpose-driven wellness food, aligning with Europe’s preventive healthcare agfinisha.

By Distribution Channel Insights

The off-trade segment led the market by capturing 71.2% of the regional market share in 2025. The dominance of off-trade segment in the European tofu market is driven by widespread availability in supermarkets, hypermarkets, and specialty health food stores where consumers purchase tofu for home preparation as part of weekly grocery routines. According to Eurostat, houtilizehold expfinishiture on food consumed at home rose in the EU between 2021 and 2023, while out-of-home spfinishing remained below pre-2019 levels in most countries. Major retailers have responded by expanding plant-based sections; Carrefour in France and Edeka in Germany now dedicate entire chillers to tofu and soy products with clear labeling for vegans and flexitarians. Private-label offerings further boost accessibility; data from Mintel reveals that private-label tofu accounted for nearly half of off-trade sales in Western Europe in 2023 due to price advantages over branded alternatives. Additionally, e-commerce platforms such as Ocado and Picnic feature tofu in subscription boxes and recipe kits, normalizing its utilize among younger demographics. The European Veobtainarian Union notes that most new tofu consumers first test the product at home, influenced by social media recipes and sustainability messaging on packaging. This channel’s scale, consistency, and promotional power build it the backbone of market penetration across urban and suburban Europe.

The on-trade segment is anticipated to register a CAGR of 13.3% over the forecast period in the European tofu market. The institutional mandates, cultural normalization, and culinary innovation in restaurants, cafés, and public catering are fuelling the growth of the on-trade segment in this regional market. National policies are a critical catalyst as France’s EGalim law requires all public-school canteens to serve at least one veobtainarian menu per week, and data from the French Ministest of Education reveals that tofu appears in a majority of these meals due to its protein density and ease of integration into global cuisines. Similarly, hospital networks in the Netherlands and Sweden include tofu in therapeutic diets for cardiovascular and renal conditions as recommfinished by national dietary guidelines. Beyond institutions, indepfinishent restaurants are elevating tofu through chef-driven menus—such as smoked tofu tartare in Copenhagen or miso-glazed tofu steaks in Barcelona—transforming perception from bland substitute to gourmet ingredient. The European Public Health Alliance reports that thousands of public sector kitchens across the EU adopted plant-based procurement tarobtains in 2023, directly increasing bulk tofu orders. Moreover, urban food delivery apps such as Deliveroo and Wolt now categorize dishes by dietary preference, with “vegan tofu bowls” among the top trfinishing items in London, Berlin, and Amsterdam. This channel not only drives volume but also builds aspirational value, accelerating mainstream acceptance through professional culinary validation.

REGIONAL ANALYSIS

Germany Tofu Market Analysis

Germany led the European tofu market with 26.2% of the regional market share in 2025. The dominance of Germany in the European market is attributed to its status as the continent’s largest vegan population and most developed plant-based ecosystem. The countest hosts over a million registered vegans according to the German Veobtainarian Society and boasts more than 30 domestic tofu producers, including established brands such as Taifun and tinyer organic artisans. Regulatory support is robust; the Federal Ministest of Food and Agriculture includes tofu in its official dietary recommfinishations for protein diversification and funds research into European soy cultivation through the “Protein Crop Strategy.” Retail penetration is exceptional, with REWE and Aldi offering multiple tofu variants per store including smoked, marinated, and calcium-enriched options. Furthermore, Germany’s strong organic shiftment drives demand for non-GMO certified tofu created with locally grown soy. Berlin alone features dozens of fully vegan restaurants, many applying houtilize-created tofu, signaling deep cultural integration. This confluence of policy, consumer activism, retail infrastructure, and agricultural innovation solidifies Germany’s position as Europe’s tofu epicenter.

United Kingdom Tofu Market Analysis

The United Kingdom accounted for 17.4% of the regional market share in 2025. The growth of the UK in the European market is driven by high flexitarian adoption, progressive food labeling, and dynamic retail competition. Despite Brexit, the UK retained EU-style allergen and origin labeling rules, which enhance consumer trust in plant-based products. According to the Vegan Society, millions of Britons identify as vegan and many more as flexitarian, creating massive latent demand. Supermarkets lead innovation; Tesco’s Plant Chef and Sainsbury’s Taste the Difference ranges include ready-to-eat tofu stir-fry kits and smoked tofu slices, driving trial among convenience-seeking shoppers. Data from Kantar reveals that tofu sales in UK grocery channels grew strongly in 2023, outpacing other meat alternatives. London’s diverse culinary scene also fosters fusion applications such as jerk tofu tacos and masala scrambled tofu, normalizing the ingredient beyond health food circles. The National Health Service increasingly promotes plant proteins for heart health, further embedding tofu in public health discourse. With strong e-commerce logistics and influencer culture, the UK excels at rapid product iteration and mainstream storynotifying around tofu, building it a high-velocity growth market.

France Tofu Market Analysis

France is estimated to register a promising CAGR in the European tofu market during the forecast period due to the state-led dietary transformation and gastronomic reinterpretation. The French government’s National Nutrition and Health Program explicitly encourages legume consumption, including tofu, as a red meat substitute, with public campaigns featuring celebrity chefs preparing soy-based dishes. The landmark EGalim law mandates veobtainarian menus in schools and restricts ultra-processed foods in public institutions, indirectly favoring whole food proteins such as tofu. According to France’s Ministest of Agriculture, a majority of public school canteens included tofu in their 2023 veobtainarian offerings, often paired with local veobtainables and herbs to align with terroir principles. Retailers such as Carrefour and Monoprix have launched French-created tofu applying soy from Burgundy and Provence, emphasizing traceability and reduced food miles. Data from Xerfi indicates that domestically produced tofu volumes grew significantly between 2021 and 2023 as consumers prioritized “created in France” labels. Paris, Lyon, and Marseille host numerous vegan bistros that present tofu as a refined ingredient challenging traditional meat-centric cuisine. This blfinish of policy, patriotism, and culinary creativity positions France as a unique bridge between tradition and innovation in tofu adoption.

Netherlands Tofu Market Analysis

The Netherlands is predicted to account for a prominent share of the European tofu market during the forecast period owing to its advanced soy farming infrastructure and institutional integration. The Netherlands is Europe’s leading producer of non-GMO food-grade soybeans, with thousands of hectares cultivated in 2023 according to Wageningen University, enabling short supply chains for brands such as Vantastic Foods and De Hobbit. Dutch hospitals and universities operate under national sustainability charters requiring a majority of meals to be plant-based by 2025, with tofu as a core protein source due to its low environmental footprint. The RIVM National Institute for Public Health notes that soy protein intake among Dutch adults increased significantly between 2020 and 2023, driven by workplace canteens and school programs. Retailers such as Albert Heijn feature tofu prominently in “Meatless Monday” promotions and recipe cards, normalizing weekly utilize. Moreover, the Netherlands serves as a logistics hub for tofu distribution across Benelux and Scandinavia, with Rotterdam port facilitating efficient import of specialty coagulants and packaging materials. Dutch consumers also reveal high openness to functional foods; fortified tofu with B12 and vitamin D is widely available even in mainstream supermarkets. This synergy of agriculture policy, logistics, and nutritional awareness creates a resilient, vertically integrated tofu economy.

Sweden Tofu Market Analysis

Sweden is expected to exhibit a notable CAGR in the European tofu market over the forecast period owing to the strong environmental consciousness and public health alignment. Swedish dietary guidelines issued by the National Food Agency recommfinish replacing meat with legumes, including tofu, several times per week, citing climate and health co-benefits. According to Statistics Sweden, a significant share of Swedes follows a predominantly plant-based diet, one of the highest rates in Europe. Public institutions lead adoption; Stockholm’s municipal school system serves tofu in most of its veobtainarian meals, while state-owned healthcare provider Region Stockholm includes it in cardiac rehabilitation menus. Domestic brand Svensk Soja produces organic tofu applying Swedish-grown soybeans with carbon footprint labeling that appeals to eco-literate consumers. According to the Swedish Board of Agriculture, soy cultivation for human consumption expanded in 2023, supported by EU agroecology subsidies. Moreover, Sweden’s cold climate increases demand for hearty plant proteins during winter months, with smoked and baked tofu variants gaining popularity in stews and grain bowls. With high digital literacy, consumers readily access tofu recipes via apps such as MatLagnad, reinforcing habitual utilize. Sweden’s model demonstrates how climate policy, nutrition science, and cultural adaptation can converge to embed tofu as a civic dietary norm.

COMPETITIVE LANDSCAPE

Competition in the Europe tofu market is characterized by a dual structure comprising established organic pioneers and agile new entrants vying for consumer attention in a rapidly expanding but fragmented landscape. Legacy brands leverage decades of trust clean label credentials and vertically integrated soy sourcing to maintain premium positioning particularly in Germany and the Benelux region. Meanwhile newer players compete on convenience flavor innovation and digital engagement tarobtaining flexitarians rather than strict vegans. Private label offerings from major retailers exert price pressure yet often lack the quality consistency of branded tofu creating opportunities for differentiation through texture protein content and sustainability claims. Regulatory complexity around GMO labeling deforestation due diligence and health claims raises barriers to entest favoring companies with robust compliance infrastructure. Competition extfinishs beyond product attributes into storynotifying as these are the brands that effectively link tofu to local agriculture climate action and culinary heritage gain disproportionate loyalty. Despite growing demand distribution remains uneven with rural areas underserved due to cold chain limitations. Ultimately success hinges on balancing authenticity with accessibility while navigating Europe’s intricate mosaic of dietary preferences policy frameworks and cultural attitudes toward plant-based eating.

KEY MARKET PLAYERS

Some of the notable key players in the Europe tofu market are

• Taifun Tofu GmbH

• The Tofoo Co. Ltd

• Houtilize Foods Group Inc.

• Pulmuone Corporation

• Clearspring Ltd

• Schouten Europe

• Berief Food GmbH

• Clear Spot Tofu

• Hain Celestial Group

• Vitasoy

• Others key vfinishors

Top Players in the Market

- Taifun-Tofu is a German pioneer in organic tofu production with over four decades of expertise in artisanal soy processing. The company supplies a wide range of products including smoked marinated and calcium enriched tofu across Europe and exports to North America and Asia. Taifun emphasizes non-GMO European soybeans traceable to certified organic farms and utilizes traditional coagulants like nigari to preserve clean label integrity. Recently the company invested in a new production facility in Freiburg to increase capacity for functional tofu variants fortified with vitamin B12 and vitamin D responding to rising demand for nutritionally enhanced plant proteins. It also launched a climate footprint label on all packaging detailing water usage and CO2 emissions per kilogram of tofu reinforcing its alignment with EU sustainability standards and strengthening consumer trust in an increasingly eco conscious market.

- Lima is a Belgian organic food company renowned for its high-quality plant-based products including a diverse tofu portfolio spanning silken firm and ready to eat formats. Operating under strict Demeter and EU organic certifications Lima sources soybeans from European agroecological cooperatives ensuring short supply chains and soil health compliance. The company has integrated tofu into broader meal solutions such as vegan lasagnas and stir fry kits available in major retailers across France Germany and the Netherlands. In recent years Lima expanded its R and D focus on texture optimization applying fermentation techniques to improve mouthfeel without additives. It also partnered with Belgian universities to validate the protein bioavailability of its calcium set tofu enhancing scientific credibility. These initiatives position Lima as a bridge between traditional craftsmanship and modern nutritional science in the European plant protein landscape.

- Vantastic Foods is a dynamic German brand specializing in innovative vegan products with tofu as a core ingredient in its portfolio. The company differentiates through bold flavor profiles convenience-oriented formats and eye-catching packaging tarobtaining younger urban consumers. Its product line includes smoked tofu slices teriyaki marinated blocks and crumbled tofu for scrambles all positioned as direct replacements for dairy and meat. Vantastic has leveraged digital marketing and influencer collaborations to drive trial particularly in the UK and Scandinavia where flexitarianism is surging. Recently the company reformulated its entire tofu range to utilize 100% EU grown soybeans in response to the EU Deforestation Regulation and introduced recyclable mono material packaging to meet circular economy goals. By combining culinary creativity with regulatory foresight Vantastic accelerates mainstream adoption of tofu beyond niche health segments.

Top Strategies Used by the Key Market Participants

Key players in the Europe tofu market employ multifaceted strategies centered on localization transparency and culinary relevance. Sourcing non-GMO soybeans from European farms ensures supply chain resilience and aligns with anti-deforestation regulations while reducing carbon footprint. Product innovation focutilizes on texture enhancement flavor infusion and nutritional fortification to overcome consumer perceptions of blandness. Clean label positioning with minimal ingredients and traditional coagulants builds trust among health-conscious shoppers. Strategic retail partnerships enable prominent shelf placement in mainstream supermarkets rather than specialty stores broadening accessibility. Culinary education through recipe cards social media and chef collaborations normalizes tofu in everyday cooking. Sustainability messaging including carbon and water footprint labeling appeals to eco literate consumers. These approaches collectively transform tofu from an ethnic import into a familiar versatile and purpose driven protein within Europe’s evolving food culture.

MARKET SEGMENTATION

This research report on the European tofu market has been segmented and sub-segmented based on categories.

By Product Type

- Regular

- Smoked or Flavored

- Fortified or Functional

By Distribution Channels

By Countest

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Leave a Reply