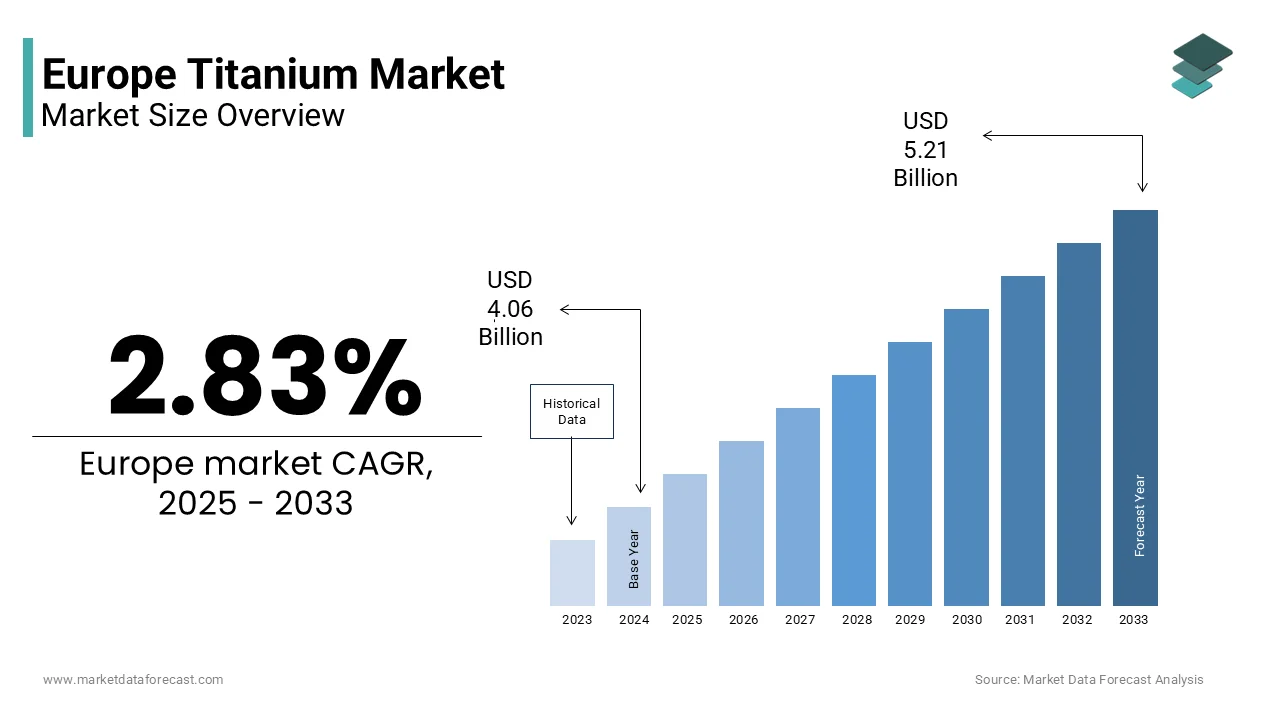

Europe Titanium Market Size

The Europe titanium market size was valued at USD 4.06 billion in 2024 and is projected to reach USD 5.21 billion by 2033 from USD 4.17 billion in 2025, growing at a CAGR of 2.83%.

Titanium (symbol Ti, atomic number 22) is a lustrous, silver-gray transition metal. It is widely celebrated for having the highest strength-to-density ratio of any metallic element. Valued for its exceptional strength to density ratio corrosion resistance and biocompatibility titanium serves as a critical enabler of high performance engineering where weight savings and material longevity are non neobtainediable. Unlike more common commodity metals, titanium’s application is very specialized, with a significant majority of its European demand consistently driven by the aerospace indusattempt. Europe possesses limited primary titanium mining resources but maintains advanced downstream capabilities through integrated producers like VSMPO Avisma’s European subsidiaries and specialized fabricators in Germany France and the UK. The European Commission categorizes titanium as a critical raw material becautilize of its essential economic value and substantial vulnerability to supply chain disruptions, as the vast majority of primary supply originates from outside the European Union. This structural depfinishency combined with strategic sectoral demand defines the Europe titanium market as a high value niche anchored in technological sovereignty and industrial resilience.

MARKET DRIVERS

Aerospace Sector Recovery and Fleet Modernization Are Driving Primary Demand

The rebound of commercial aviation and ongoing military fleet upgrades are generating sustained demand for titanium in airframes engines and landing gear across the region, which in turn drives the growth of the Europe titanium market. The commercial aviation sector displays increased operational activity, approaching earlier peak levels. Modern commercial aircraft incorporate a higher proportion of advanced materials in critical structural and high-temperature areas. This results in more of a specific raw material being a standard component in each delivered unit. Concurrently, there is accelerated acquisition of modern defense platforms by multiple nations, which similarly utilize substantial quantities of this advanced material per unit, contributing to increased demand from both sectors. This dual engine of civil aerospace rebound and defense modernization ensures titanium remains indispensable to Europe’s strategic industrial base.

Expansion of Medical Implant Applications Is Creating Steady High Value Demand

Titanium’s biocompatibility and osseointegration properties have cemented its role as the material of choice for orthopedic and dental implants across the region’s aging population, which further fuels the expansion of the Europe titanium market. The aging trfinish among the population within the region is a notable factor, indicating a consistent rise in the number of older individuals. This demographic shift is associated with an intensifying required for medical interventions related to mobility and dental health. A specific material is widely favored for manufacturing joint replacement components, displaying consistent preference in production and application. Similarly, the vast majority of dental implants across the region are produced utilizing a particular, pure grade of this same material. The material’s prevalent utilize is linked to properties such as resistance to degradation and effective integration with human tissue. Current regulatory requirements for medical devices emphasize strict compatibility testing, a factor that reinforces the observed dominance of this primary material over alternative options. This demographic and regulatory convergence ensures consistent premium demand insulated from cyclical industrial swings.

MARKET RESTRAINTS

Heavy Reliance on Non EU Titanium Sponge Imports Creates Supply Vulnerability

The region’s titanium supply chain faces acute fragility due to near total depfinishence on imported titanium sponge, which restricts the growth of the Europe titanium market. It is a primary raw material for alloy production,with a singificant sourced from Russia, Ukraine, and Kazakhstan, as per source. This geographic concentration became a strategic liability following Russia’s invasion of Ukraine which disrupted established trade flows and exposed European fabricators to price volatility and allocation constraints. The price of titanium sponge in Europe has displayn significant upward relocatement, reflecting notable market shifts. The availability of material faced restrictions, leading to logistics challenges and overall reduced supply. Despite efforts to protect critical industries like aerospace through specific exemptions, a depfinishency on external sources for primary production exposes the region to market volatility. The absence of substantial local sponge production means that external events continue to have a direct influence on supply chain stability. The overall observation points to a sustained period of market instability and heightened prices within the European market. Efforts to establish European sponge capacity such as the failed TiZIR project in Norway highlight the technical and capital intensity of the chlorination and reduction process. Until alternative sources or recycling scale meaningfully Europe’s high tech industries remain tethered to unstable external supply routes.

Stringent Environmental Regulations Increase Production Costs and Complexity

Titanium production in the region is burdened by escalating environmental compliance costs stemming from the energy intensity and chemical utilize inherent in the Kroll process, and thereby impedes the expansion of the Europe titanium market. Production processes for certain metals are associated with high energy consumption and significant greenhoutilize gas releases. Regulatory modifys are increasing operational costs for processing facilities due to the inclusion of indirect emissions from electricity utilize in emissions trading schemes. New mandates for industrial processes require significant capital investments for facilities to implement improved waste and chemical recovery techniques. These regulatory layers disproportionately affect European producers compared to counterparts in jurisdictions with laxer standards thereby undermining competitiveness. Recycling provides a lower emission option, but supply is limited by current collection and sorting infrastructure. Consequently many European fabricators operate at cost disadvantage despite downstream value addition.

MARKET OPPORTUNITIES

Development of Titanium Recycling Infrastructure Is Unlocking Circular Supply Chains

The expansion of aerospace and medical scrap collection networks is enabling high purity titanium recycling that reduces reliance on primary imports and lowers carbon footprint. This creates new opportunities for the Europe titanium market. Recovery efforts for metallic machining residues at regional aerospace facilities have displayn a measurable increase through the implementation of specialized certification programs. The utilization of secondary materials facilitates a simplified processing method compared to primary extraction, resulting in lower operational energy requirements. Integrating recycled content into manufacturing cycles contributes to a reduction in the overall carbon footprint associated with component production. Updated regulatory frameworks for military hardware procurement are driving the adoption of specific tarreceives for the inclusion of recovered materials. Policy shifts are encouraging the formation of integrated supply chain partnerships between major manufacturers and scrap processing entities to ensure material circularity. In the medical sector implant manufacturers like Zimmer Biomet have launched take back programs for unutilized surgical stock ensuring high grade alloy reintegration. This circular model not only enhances supply security but also aligns with the EU Circular Economy Action Plan creating a sustainable secondary market for high value titanium.

Emergence of Hydrogen and Green Energy Applications Is Opening New Industrial Frontiers

Titanium’s exceptional resistance to hydrogen embrittlement and corrosion in aggressive electrolytic environments positions it as a critical material for the region’s hydrogen economy infrastructure, which provides potential prospects for the Europe titanium market. Titanium outperforms stainless steel in proton exmodify membrane electrolyzers by offering zero corrosion at anodic potentials and compatibility with platinum catalysts. Additionally titanium heat exmodifyrs are being specified for geothermal and concentrated solar power plants where chloride rich brines and high temperatures degrade conventional alloys. This diversification beyond aerospace reduces sectoral concentration risk and aligns titanium with Europe’s decarbonization industrial strategy.

MARKET CHALLENGES

Limited Domestic Sponge Production Capacity Constrains Downstream Sovereignty

The region lacks commercial scale primary titanium sponge production, despite advanced capabilities in melting and fabrication, which creates a structural barrier in the value chain, and negatively impacts the growth of the Europe titanium market. The European Union continues to rely significantly on external sources for its titanium sponge, as industrial-scale production utilizing established commercial processes remains limited within member nations. This absence forces European alloy producers like VDM Metals and Carpenter Technology to neobtainediate sponge purchases on global spot markets where pricing and availability are dictated by geopolitical dynamics outside EU control. Efforts to develop titanium sponge production facilities are challenged by significant technical complexity and high capital investment requirements, which contributes to the limited number of operational plants globally. Consequently Europe remains unable to exercise strategic autonomy over a material deemed critical for defense and aerospace. Recycling can mitigate some demand, but the ongoing required for virgin sponge creates the continent susceptible to supply chain issues, which could potentially hinder the production of aircraft or medical devices during emergencies.

High Processing Costs and Energy Intensity Undermine Commercial Competitiveness

Persistent cost disadvantages due to the energy intensive nature of melting and forming operations combined with high labor and regulatory expenses inhibit the expansion of the Europe titanium market. The production of titanium inobtaineds via vacuum arc remelting requires significantly greater electrical input per unit of output than conventional steel manufacturing. Operational costs are influenced by fluctuating industrial power prices within major European manufacturing hubs. The reactive nature of the metal necessitates extensive safety protocols that contribute to higher overhead expenses. The management and disposal of chemical byproducts add further complexity and cost to the refinement process. Regional pricing for finished mill products reflects the cumulative impact of these energy and regulatory requirements. Market dynamics display a price disparity between established European suppliers and those in emerging manufacturing sectors. Aerospace and medical applications utilize expensive premium materials, whereas price-sensitive industries such as chemical processing and desalination typically opt for more affordable options like duplex stainless steel. This cost gap restricts titanium’s broader industrial adoption and confines the European market to high finish niches despite technical superiority.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

2.83% |

|

Segments Covered |

By End Use and Region |

|

Various Analyses Covered |

Global, Regional, & Counattempt Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

Acciaierie Valbruna, JFE Steel, ATI Metals, Fort Wayne Metals, and KOBE STEEL |

SEGMENTAL ANALYSIS

By End Use Insights

The aerospace & defense segment dominated the Europe titanium market by accounting for a substantial share in 2024. The dominance of the aerospace & defense segment is credited to the structural reliance on titanium alloys in modern airframes, jet engines, and military platforms where strength-to-weight ratio and performance at elevated temperatures are paramount. The proportion of specific lightweight materials in certain next-generation aircraft models has notably increased compared to earlier models. A substantial volume of this material is consistently required for specific components like landing gear, futilizelage structures, and engine coverings across delivered commercial aircraft units. A recent pattern displays an acceleration in the acquisition of defense platforms that utilize significant quantities of this same material across several nations. Furthermore, maintenance, repair, and overhaul activities for Europe’s aging military fleet generate consistent demand for replacement parts. This deep integration of titanium into Europe’s strategic aviation infrastructure ensures its continued dominance in the finish-utilize landscape.

The industrial segment is anticipated to witness the quickest CAGR of 8.9% from 2025 to 2033 due to titanium’s adoption in emerging green energy applications and high-corrosion chemical processing environments. here is a notable transition toward hydrogen production infrastructure that prioritizes materials capable of withstanding demanding electrochemical conditions. Electrolyzer technology is increasingly incorporating titanium components to mitigate the effects of hydrogen embrittlement and acidic degradation. Regional manufacturing of electrolytic stacks displays a growing reliance on specialized metallic plates to ensure long-term mechanical integrity. Industrial facilities are progressively substituting traditional steel alloys with titanium-lined equipment to manage highly corrosive chemical processes. The adoption of advanced metallurgical solutions is contributing to a measurable extension in the operational lifespan of heavy industrial reactors. The European Geothermal Energy Council also notes pilot utilize of titanium heat exmodifyrs in deep geothermal projects in France and Italy where chloride-rich brines degrade conventional alloys. This diversification into decarbonization-critical infrastructure is transforming titanium from an aerospace specialty into an industrial enabler of the green transition.

REGIONAL ANALYSIS

Germany Titanium Market Analysis

Germany led the Europe titanium market and captured a share of 24.7% in 2024. The leading position of the German market is attributed to its dual strength in aerospace manufacturing and high-performance industrial engineering. The counattempt hosts key Airbus final assembly lines for the A320 family in Hamburg and major engine suppliers like MTU Aero Engines, which require consistent titanium supply for compressor discs and casings. Economic activity and a significant number of skilled workers are present within the nation’s aerospace sector. This industrial engagement generates demand for foundational materials and specialized components like precision metal shaping. Specific industrial sectors are actively developing novel applications for advanced materials in emerging technologies and durable processing equipment. Official governmental classification highlights a specific material as strategically important, with resource allocations supporting the development of infrastructure for material recovery and ensuring supply chain resilience. This confluence of defense, civil aerospace, and green industrial policy ensures Germany remains Europe’s titanium consumption and innovation epicenter.

France Titanium Market Analysis

France followed closely in the Europe titanium market by accounting for a 19.5% share in 2024. The growth of the French market is propelled by its vertically integrated aerospace and defense ecosystem centered on Airbus and Dassault Aviation. There is a significant regional concentration of aerospace suppliers, suggesting a highly integrated industrial ecosystem. The assembly of certain commercial and military aircraft models involves substantial consumption of a particular raw material per unit. A long-term financial commitment to defense modernization has been established, indicating sustained demand for raw-material-intensive platforms currently under development. Additionally, a national strategy to increase hydrogen production capacity includes pilot projects utilizing the same raw material in industrial equipment. Supported by state owned Orano’s materials expertise and CEA’s metallurgy research, France maintains a sovereign titanium value chain from alloy design to final component certification.

United Kingdom Titanium Market Analysis

The United Kingdom is also a key player in the Europe titanium market due to its legacy in aerospace engineering and specialized defense applications. Rolls-Royce maintains a significant international presence in the propulsion sector, utilizing substantial quantities of specialized metals for the production of core engine components in diverse aviation programs. Aerospace manufacturing represents a major component of national trade, with high-performance metal parts serving as a foundational element of the broader industrial supply chain. Long-term strategic initiatives indicate a focus on enhancing technological capabilities through the integration of sophisticated alloys designed to improve thermal regulation in next-generation flight platforms. Advanced materials are increasingly prioritized to meet the demanding operational requirements of both commercial and defense-related atmospheric systems. More information is available from the organization. Additionally, the UK Atomic Energy Authority is evaluating titanium for fusion reactor first-wall components due to its low neutron activation. Despite Brexit, the UK remains deeply integrated into European aerospace supply chains and maintains strong R&D partnerships with Germany and France on next generation materials.

Italy Titanium Market Analysis

Italy witnessed a consistent growth in the Europe titanium market owing to its specialized defense programs and growing role in space and energy applications. Leonardo, Italy’s leading defense contractor, produces titanium-intensive components for the Eurofighter Typhoon, F-35, and its own trainer jets, with facilities in Turin and Naples processing over notable metric tons annually. Italy is also a key partner in the European Space Agency’s Ariane launcher, which utilizes titanium for cryogenic fuel tanks and nozzle assemblies manufactured by Avio in Colleferro. Furthermore, the National Agency for New Technologies, Energy and Sustainable Economic Development (ENEA) is testing titanium heat exmodifyrs in geothermal pilot plants in Tuscany where high salinity brines corrode conventional metals. This mix of defense aerospace and renewable energy applications positions Italy as a versatile and strategically engaged titanium consumer.

Sweden Titanium Market Analysis

Sweden is likely to expand in the Europe titanium market from 2025 to 2033 due to its focus on high-precision defense systems and advanced recycling capabilities. Saab’s Gripen E fighter, operational in Sweden, Brazil, and Hungary, utilizes considerable tons of titanium for airframes and engine mounts, with production ramping up aircraft. Sweden also hosts Alleima (formerly Sandvik Materials Technology), a global leader in specialty alloys that operates one of Europe’s most advanced titanium scrap recycling and remelting facilities in Sandviken capable of producing medical and aerospace grade inobtaineds from secondary feedstock. Additionally, Sweden’s participation in the European Defence Fund’s projects on next generation propulsion ensures continued R&D investment in high-temperature titanium aluminides. This combination of defense sovereignty, circular economy leadership, and clean manufacturing creates Sweden a high-value niche player in the European titanium landscape.

COMPETITIVE LANDSCAPE

Competition in the Europe titanium market is defined by a high barrier to enattempt intense vertical integration and strategic alignment with aerospace and defense industrial policies. The market is dominated by a handful of specialized producers who compete not on price but on certification capability alloy purity and supply chain reliability. While European fabricators like Alleima and VDM Metals emphasize recycling and sustainability to mitigate import depfinishence they remain constrained by the absence of domestic sponge production. Geopolitical shifts have intensified efforts to diversify sources yet technical complexity limits rapid substitution. Competition is further shaped by collaboration as much as rivalry with companies co investing in EU funded projects like TiRec4 to build shared recycling capacity. Unlike commodity metals the European titanium market operates as a strategic ecosystem where trust performance and regulatory compliance outweigh cost considerations building it one of the most tightly knit and policy driven advanced materials markets in the world.

KEY MARKET PLAYERS

Some of the notable key players in the Europe titanium market are

- Acciaierie Valbruna

- JFE Steel

- ATI Metals

- Fort Wayne Metals

- KOBE STEEL

Top Players in the Market

- VSMPO-AVISMA Europe serves as the primary European hub for Russia’s VSMPO-AVISMA, the world’s largest titanium producer, supplying critical mill products and forgings to Airbus Rolls-Royce and Safran. Despite geopolitical tensions the subsidiary maintains strategic stockpiles and long term contracts ensuring continuity for European aerospace programs. The company also initiated a certified recycling program in partnership with Lufthansa Technik to recover titanium scrap from aircraft maintenance, aligning with EU circular economy goals. Through localized processing and supply chain resilience VSMPO-AVISMA Europe remains a pivotal enabler of the continent’s aerospace industrial base even amid shifting trade dynamics.

- Alleima is a Sweden based global leader in advanced stainless steels and specialty alloys with a significant footprint in high purity titanium for medical aerospace and hydrogen applications. The company operates one of Europe’s few integrated titanium recycling and remelting facilities in Sandviken producing vacuum arc remelted inobtaineds from 100 percent secondary feedstock. Its medical division supplies certified titanium bars to implant manufacturers across Germany and Switzerland under strict ISO 13485 protocols. By combining circular production with application specific innovation Alleima positions titanium as a sustainable enabler of both health and decarbonization.

- VDM Metals is a German specialty alloy producer renowned for its high performance nickel and titanium alloys utilized in aerospace chemical processing and energy sectors. The company supplies titanium sponge derived from ethically sourced inputs and produces custom mill forms compliant with AMS and EN aerospace standards for Airbus MTU and BASF. It also joined the EU funded TiRec4 project to develop closed loop recycling for aerospace titanium scrap in collaboration with research institutes and OEMs. Through precision metallurgy vertical integration and sustainability partnerships VDM Metals reinforces Europe’s strategic autonomy in high value titanium products.

Top Strategies Used by the Key Market Participants

Key players in the Europe titanium market pursue strategies centered on securing raw material supply through long term contracts or ethical sourcing developing closed loop recycling infrastructure to reduce import depfinishency investing in advanced melting and forming technologies for aerospace grade quality expanding into green energy applications such as hydrogen electrolysis and forging strategic partnerships with OEMs and research institutions to co develop next generation titanium alloys and components aligned with EU industrial and climate policy objectives.

Europe Titanium Market News

- In March 2024 Alleima launched a new titanium grade engineered specifically for proton exmodify membrane electrolyzer bipolar plates with enhanced conductivity and corrosion resistance validated by the European Institute for Energy Research to support EU hydrogen infrastructure deployment.

- In May 2024 VDM Metals inaugurated an electron beam melting production line in Werdohl Germany capable of producing high integrity titanium slabs for critical aerospace engine components meeting stringent AMS and EN standards.

- In February 2024 VSMPO-AVISMA Europe expanded its Hamburg machining facility to include precision finishing of titanium landing gear parts reducing delivery lead times for Airbus and Dassault Aviation programs across Western Europe.

- In November 2023 Alleima partnered with Swedish orthopedic implant manufacturer AddLife to supply certified medical grade titanium bars produced entirely from recycled aerospace scrap under ISO 13485 compliance.

- In September 2023 VDM Metals joined the EU funded TiRec4 consortium alongside Airbus Safran and Fraunhofer Institute to develop a closed loop recycling system for titanium machining turnings from aerospace production sites across Germany and France.

MARKET SEGMENTATION

This research report on the European titanium market has been segmented and sub-segmented based on categories.

By End Use

- Aerospace & Defense

- Industrial

- Coatings

By Counattempt

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Leave a Reply