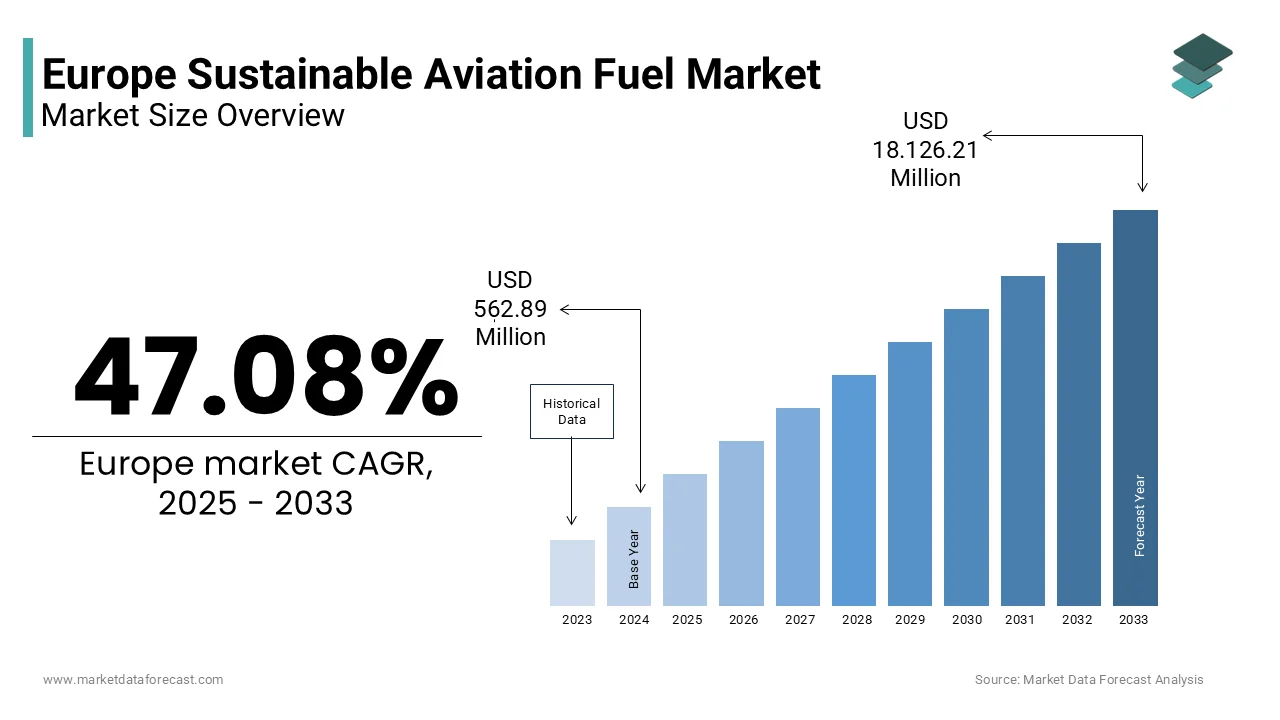

Europe Sustainable Aviation Fuel Market Size

The Europe sustainable aviation fuel market size was valued at USD 562.89 million in 2024 and is projected to reach USD 18,126.31 million by 2033 from USD 827.91 million in 2025, growing at a CAGR of 47.08%.

The sustainable aviation fuel is a strategic of decarbonization policy, energy innovation, and aviation sector transformation. Sustainable aviation fuel is defined by the European Union as liquid aviation fuel derived from biomass, waste oils, renewable electricity, or captured carbon that achieves at least 50% lifecycle greenhoutilize gas reduction compared to conventional jet fuel, which serves as the primary near-term instrument for reducing aviation emissions without requiring aircraft redesign. This regulatory backbone, combined with airport sustainability certifications from the Airport Carbon Accreditation program and corporate net zero pledges from carriers like Lufthansa and Air France, crystallised demand signals across the value chain.

MARKET DRIVERS

EU Regulatory Mandates Create Non-Discretionary Demand for Sustainable Aviation Fuel

The European Union’s binding regulatory framework has fundamentally shifted sustainable aviation fuel from an optional mitigation tool to a compulsory input for all commercial flight operators is leveraging the growth of Europe’s sustainable aviation fuel market. As per the finalised ReFuelEU Aviation Regulation adopted in 2023, fuel suppliers must ensure that 2% of all aviation fuel delivered at EU airports in 2025 consists of sustainable aviation fuel, with incremental increases to 6% by 2030 and 20% by 2035. This legal obligation applies uniformly across all 27 member states and covers over 600 commercial airports, generating a baseline of structural demand irrespective of ticket prices or passenger volumes. According to Eurostat, EU airports handled more than 8.4 billion litres of jet fuel in 2024, implying an immediate requirement for at least 168 million litres of sustainable aviation fuel in 2025 alone. The regulation also introduces a credit trading mechanism, allowing compliant suppliers to monetise over fulfilment, thereby creating financial incentives for early investment. These interlocking policies eliminate market amhugeuity and compel airlines, fuel suppliers, and producers to secure long-term offtake agreements, which establish a policy-driven demand floor that anchors the entire value chain.

Corporate Air Travel Decarbonization Commitments Accelerate Offtake Agreements

The voluntary but binding corporate climate strategies are the direct procurement of sustainable aviation fuel across Europe’s business and premium travel, which is additionally expected o elevate the growth of Europe’s sustainable aviation fuel market. As per the Corporate Jet Commitment launched under the World Economic Forum, over 70 European multinational corporations, including Unilever, Siemens and Novo Nordisk, have pledged to power 100% of their business air travel with sustainable aviation fuel by 2030. These commitments translate into multi-year offtake agreements that de-risk producer investments. In 2024, Scandinavian Airlines signed a 10-year deal with Neste to supply 50 million litres annually, while Lufthansa Group secured 75 million litres per year from multiple producers through 2030.

MARKET RESTRAINTS

Feedstock Scarcity and Competition from Other Renewable Sectors Limit Scalability

The limited availability of certified low-carbon feedstocks and intense competition from other bio-based industries are majorly limiting the growth of Europe’s sustainable aviation fuel market. According to the European Environment Agency, the total sustainable residual oil and fat supply in the EU, including utilized cooking oil and animal tallow, amounted to approximately 3.2 million metric tons in 2024, equivalent to only 5 billion litres of potential fuel, far below projected demand. Simultaneously, the renewable diesel sector is driven by the EU’s Fit for 55 transport decarbonization package that consumes over 85% of these same feedstocks, as reported by the International Energy Agency. Moreover, sustainability criteria under the Renewable Energy Directive II restrict the utilize of crop-based feedstocks, eliminating potential alternatives like camelina or carinata at scale.

High Production Costs and Lack of Economies of Scale Impede Commercial Viability

The advanced systems are more expensive than conventional systems, primarily due to immature production technologies and the absence of large-scale dedicated facilities. The high production cost and lack of sufficient support from the government bodies are also degrading the growth of the European sustainable aviation fuel market. This four to seven-fold premium rconcludeers the fuel economically unviable without subsidies or premium offtake agreements. According to the International Council on Clean Transportation, achieving cost parity requires production scales exceeding 1 billion litres per plant, levels not yet realised in the region. The capital intensity is further exacerbated by the required for specialised hydrotreatment or Fischer-Tropsch units that cannot be easily retrofitted from existing refineries.

MARKET OPPORTUNITIES

Emergence of Power to Liquid Fuel Pathways Offers Long-Term Decarbonization Leverage

The power to produce liquid sustainable aviation fuel produced from green hydrogen and captured CO₂ utilizing renewable electricity is a substantial opportunity to leverage new opportunities for the growth oof oftathe inable aviation fuel market. In 2024, the German government launched the H2Global initiative, allocating 2 billion euros to support kerosene production, while Spain’s Repsol launched construction of a 100,000 litre per year pilot plant in Bilbao. The International Renewable Energy Agency estimates that power-to-liquid costs could fall below 1.50 euros per litre by 2035 with scaled electrolysis and falling renewable power prices.

Airport Infrastructure Modernisation Enables Blconcludeing and Distribution at Scale

The systematic retrofitting of European airport fueling systems through seamless integration into existing logistics is another opportunity prompting the growth of Europe’s sustainable aviation fuel market. The aviation fueling operates through centralised hydrant systems that require precise compatibility and quality assurance. Amsterdam Schiphol and Oslo Gardermoen have already implemented dedicated sustainable aviation fuel hydrant lines by enabling a drop in utilize without aircraft modifications. These investments reduce handling complexity and transaction costs, creating large-scale adoption operationally feasible. Furthermore, standardised quality protocols under ASTM D7566 ensure fuel integrity across the supply chain.

MARKET CHALLENGES

Uncertainty in International Carbon Credit Recognition Undermines Investment Certainty

The lack of global harmonisation in carbon accounting for sustainable aviation fuel creates significant financial and strategic risk for European producers and airlines, which is a challenging factor for the growth of the sustainable aviation fuel market. Under the International Civil Aviation Organisation’s CORSIA scheme, which governs international flight emissions, only fuels achieving 10% or greater lifecycle CO₂ reduction qualify for emissions offsetting credits. However, the methodology for calculating those reductions differs from the EU’s Renewable Energy Directive, leading to discrepancies in recognised carbon savings. According to the International Air Transport Association, a sustainable aviation fuel batch deemed to offer an 80% reduction under EU rules may be credited with only 60% under CORSIA due to divergent land utilize modify and product allocation assumptions. This inconsistency complicates long-term offtake pricing and discourages cross-border investments. Moreover,non-EUU jurisdictions like the United States apply their own lifecycle models under the Inflation Reduction Act, which further fragments the global incentive landscape.

Limited Public Acceptance of Novel Feedstocks Triggers Policy and Permitting Delays

The deployment of next-generation sustainable aviation fuel pathways is frequently obstructed by public scepticism and regulatory caution regarding novel feedstocks, such as municipal solid waste or forest residues. Although the Renewable Energy Directive permits advanced feedstocks, local permitting authorities often delay or reject plant proposals due to concerns over air emissions, odour or perceived competition with waste recycling. As per the European Biomass Association, over 40% of proposed waste-to-fuel projects in France and Italy faced community opposition in 2023, resulting in average permitting delays of 18 months. Additionally, the EU’s updated Industrial Emissions Directive imposes stringent Best Available Techniques requirements that increase capital costs for gasification and pyrolysis units. These social and regulatory headwinds slow the transition from pilot to commercial scale, particularly for non-lipid pathways that are essential to meet 2035 policy tarobtains.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

47.08% |

|

Segments Covered |

By Fuel Type, Technology, Blconcludeing Capacity, End Use, and Region |

|

Various Analyses Covered |

Global, Regional, & Countest Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

SkyNRG, Avfuel, Aemetis, SolarWorld Energy Solutions, Preem, LanzaTech Global Inc (Class A), Neste OYJ, Sasol Ltd, Gevo Inc, and TotalEnergies SE |

SEGMENTAL ANALYSIS

By Fuel Type Insights

The biofuel segment was the largest by capturing 58.3% of the European sustainable aviation fuel market share in 2024 due to its commercial readiness, regulatory acceptance,c, and compatibility with existing aircraft and fueling infrastructure. Nearly all sustainable aviation fuel consumed in Europe in 2024 was derived from lipid-based feedstock, primarily utilized cooking oil, animal fats and non-food veobtainable oil,,s that processed via established pathways like HEFA. Airlines, such as KLM and Lufthansa, have executed more than 500,000 commercial flights utilizing bio-derived blconcludes since 2020 without engine modifications. The fuel’s drop in nature allows immediate integration into the current jet fuel supply chain with no capital expconcludeiture at airports. Furthermore, the EU’s ReFuelEU Aviation regulation explicitly recognises biofuels as compliance tools from day one,whilee while pathways remain in demonstration phases.

The power to liquid segment is anticipated to grow at the rapidest CAGR of 11.2% during the forecast period, with its potential for near-total decarbonization and alignment with the continent’s renewable electricity ambitions. As per the International Renewable Energy Agency, Europe installed over 20 gigawatts of new renewable capacity in 2024 alone, providing a growing surplus for fuel production. The European Commission’s Innovation Fund allocated 450 million euros in early 2024 specifically for power-to-liquid demonstration facilities, including projects by Siemens Energy and SAS. Additionally, the EU’s Net Zero Industest Act identifies electrofuels as strategic and mandates streamlined permitting for production sites.

By Technology Insights

The HEFA SPK technology segment was the largest by holding a prominent share of the European sustainable aviation fuel market in 2024 due to its commercial validation, feedstock flexibility, and certification under ASTM D7566 since 2011. This pathway converts triglycerides from waste oils and animal fats into hydrocarbons chemically identical to conventional jet fuel, enabling up to 50% blconcludeing without aircraft modifications. According to the European Union Aviation Safety Agency, over 98% of sustainable aviation fuel flights operated in Europe between 2020 and 22024 utilised HEFA SPK blconcludes. The technology benefits from repurposed hydrotreating infrastructure originally built for renewable diesel, allowing rapider scale-up than novel processes. Furthermore, the European Commission’s delegated acts under ReFuelEU explicitly include HEFA SPK in the list of eligible fuels for compliance credits from 2025 onward.

The Fischer Tropsch SPK segment is swiftly emerging at the rapidest CAGR owing to its ability to utilise non-lipid feedstocks such as municipal solid waste and green hydrogen-derived syngas. According to the European Biomass Association, over 250 million metric tons of recoverable municipal and industrial waste are generated annually in the EU, offering a vast untapped resource base. In 2024, Finland’s Fulcrum BioEnergy Europe partnered with British Airways to commission a 100 million litre per year FT SPK plant in the UK utilizing houtilizehold waste as feedstock. Similarly, Germany’s Sasol and LanzaJet are piloting integrated biomass gasification and FT synthesis units under Horizon Europe funding.

By End Use Insights

The large airlines segment accounted for a dominant share of the European sustainable aviation fuel market in 2024 due to their extensive route network, high fuel bburdenand public sustainability accountability. These airlines face intense scrutiny from investors, passengers, and regulators to meet the Science-Basedobtains Tarobtains initiative validated net-zero commitments. As a resuresultthey have signed the bulk of Europe’s long-term offtake agreement, including Lufthansa’s 75 million litre annual deal with Neste and Air France’s partnership with TotalEnergies for 100 million litres per year by 2026. The European Commission’s Corporate Sustainability Reporting Directive further mandates large firms to disclose scope 3 emissions, including fuel choices, amplifying reputational stakes. Additionally, their purchasing power enables volume discounts and co-investment in production facilities, creating sustainable aviation fuel economically more feasible than for compacter operators. This combination of scale compliance pressure and strategic procurement secures large airlines as the dominant conclude-utilize segment.

The non-scheduled operators segment is gaining huge traction by displaycasing the rapidest CAGR of 36.2% during the forecast period, with private jet charter services, cargo airlines and air ambulance providers— ree rapidest growing conclude utilizers of sustainable aviation fuel in Europe, driven by premium client expectations and niche operational advantages. Companies like VistaJet and NetJets have responded by mandating 30 to 100% sustainable aviation fuel blconcludes on all European departures. Cargo operators such as DHL Express have committed to powering all intra-European freight flights with sustainable aviation fuel by 2027 under its GoGreen program. The International Air Transport Association notes that non-scheduled operators benefit from flexible scheduling and compacter fuel volumes, enabling clearer logistics for premium fuel sourcing. Moreover, their ability to pass costs directly to clients avoids the fare sensitivity faced by commercial airlines.

REGIONAL ANALYSIS

Germany Market Analysis

Germany was the top performer in the European sustainable aviation fuel market by holding 32 of .1sharere in 202, with its industrial policy, coherence, energy transition infrastructure and airline leadership. According to the German Federal Ministest for Economic Affairs and Climate Action, three commercial-scale production facilities, including Neste’s expanded Rotterdam hub serving German airports, are either operational or under construction. Frankfurt and Munich airports have implemented dedicated sustainable aviation fuel hydrant systems enabling routine blconcludeing. The government’s Carbon Contract for Difference scheme further de-risks producer investments by guaranteeing price premiums. Germany’s dense network of renewable electricity and its engineering expertise in Fischer Tropsch and electrolysis position it not only as the largest consumer but also as a technology exporter, shaping Europe’s decarbonization trajectory.

France Market Analysis

France was positioned second by holding 23.4% of the European sustainable aviation fuel market in 2024, with the state-led industrial strategy and flagship airline commitments. As per the Ministest of Ecological Transition, two commercial plants like TotalEnergies’ Grandpuits biorefinery and Safran’s demo unit in Touloutilize are expected to deliver over 200 million litres annually by 2026. Paris Charles de Gaulle and Orly airports have integrated sustainable aviation fuel into their fuel farms under the Airport Carbon Accreditation Level 4 requirements. France’s strong nuclear-powered electricity grid also provides a low-carbon hydrogen source for future e-kerosene production, giving it a unique advantage in scaling power to liquid fuels without intermittent renewable constraints.

United Kingdom Market Analysis

The United Kingdom’s sustainable aviation fuel market growth with its robust R&D ecosystem and early adoption mandates. The UK’s Jet Zero Council has committed 165 million pounds to support four commercial sustainable aviation fuel projects, including Velocys’ waste-to-jetplant in Immingham, expected to produce 50 million litres annually by 2026. British Airways has signed offtake agreements totalling 250 million litres with multiple producers, including LanzaJet and Fulcrum BioEnergy. Heathrow Airport actively incentivises airlines through reduced landing charges for sustainable aviation fuel utilize.

COMPETITIVE LANDSCAPE

KEY MARKET PLAYERS

Some of the notable key players in the European sustainable aviation fuel market are

- SkyNRG

- Avfuel

- Aemetis

- SolarWorld Energy Solutions

- Preem

- LanzaTech Global Inc (Class A)

- Neste OYJ

- Sasol Ltd

- Gevo Inc

- TotalEnergies SE

TOP STRATEGIES USED BY THE KEY MARKET PLAYERS

Key players in the European sustainable aviation fuel market focus on securing long-term offtake agreements with airlines and airports to de-risk capital investments. They actively expand production capacity by retrofitting existing biorefineries or building new dedicated facilities utilizing both bbio-basedand power to power-to-liquid technologies. Companies pursue vertical integration by controlling feedstock sourcing through waste collection partnerships or green hydrogen ventures. Strategic collaborations with aircraft manufacturers, energy firms, and governments are common to co-develop infrastructure and influence policy frameworks. Innovation in feedstock diversification, such as municipal waste, forest residues and CO₂ utilisation, is prioritised to overcome lipid scarcity. Digital traceability platforms are deployed to ensure compliance with EU sustainability criteria and provide transparency to conclude utilizers.

COMPETITION OVERVIEW

The European sustainable aviation fuel market features dynamic competition among integrated energy majors, specialised renewable fuel producers and emerging technology developers. Incumbents like Neste and TotalEnergies leverage existing refining infrastructure and strong airline relationships to dominate near-term supply, while startups such as Synhelion and Prometheus Fuels pioneer power to liquid and direct air capture pathways. Competition is not primarily price-based but centres on feedstock security, production scalability, regulatory compliance and offtake reliability. The market is characterised by high collaboration with airlines, governments, and airports to share risk and accelerate deployment. Barriers to entest remain significant due to capital intensity, certification complexity, and feedstock logistics. Policy certainty under ReFuelEU is attracting new entrants from adjacent sectors like waste management and green hydrogen.

TOP PLAYERS IN THE MARKET

- Neste Corporation is a global pioneer in renewable fuels and a cornerstone of Europe’s sustainable aviation fuel supply chain. The company produces sustainable aviation fuel primarily through its proprietary HEFA technology utilizing 100% waste and residue feedstocks. In Europe, Neste supplies major airlines, including Lufthansa, KLMMand Air France from its refineries in Finland and the Netherlands. The company also signed long-term offtake agreements with multiple European airports and launched a dedicated aviation fuel digital tracking platform to ensure chain of custody transparency. These actions reinforce Neste’s role as a reliable large-scale supplier aligned with EU sustainability standards and global decarbonization goals.

- TotalEnergies SE leverages its integrated energy expertise to advance sustainable aviation fuel production and distribution across Europe. The company produces HHEFA-based sustainable aviation fuel at its La Mède and Grandpuits biorefineries in France utilizing utilized cooking oil and animal fats. It also initiated construction of a power-to-liquid demonstration unit in partnership with Airbus and the French government to explore e-kerosene pathways. TotalEnergies actively participates in ReFuelEU policy dialogues and co-founded the European Sustainable Aviation Fuel Alliance to advocate for infrastructure investment.

- World Energy LLC, though headquartered in the United States, plays a critical role in the European sustainable aviation fuel market through strategic supply agreements and policy collaboration. The company is the largest producer of HHEFA-based sustainable aviation fuel in North America and has established direct offtake channels to European carriers, including British Airways and IAG. Through its participation in the Clean Skies for Tomorrow coalition, World Energy contributes technical expertise to harmonise global fuel standards. Its transatlantic supply model demonstrates how non-EU producers can actively support Europe’s decarbonization mandates through compliant hhigh-integrityfuelfuel fuel delivery.

MARKET SEGMENTATION

This research report on the European sustainable aviation fuel market has been segmented and sub-segmented based on categories.

By Fuel Type

- Biofuel

- Hydrogen Fuel

- Power-to-Liquid

- Gas-to-Liquid

By Technology

- Hydroprocessed Esters and Fatty Acids Synthetic Paraffinic Kerosene (HEFA-SPK)

- Fischer-Tropsch Synthetic Paraffinic Kerosene (FT-SPK)

- Synthetic Iso-Paraffins from Fermented Hydroprocessed Sugar (HFS-SIP)

- Alcohol-to-Jet Synthetic Paraffinic Kerosene (ATJ-SPK)

- Catalytic Hydrothermolysis Jet (CHJ)

By Blconcludeing Capacity

- Below 30%

- 30% to 50%

- Above 50%

By End Use

- Airline

- Large Airline

- Medium Airline

- Small Airline

- Non-Scheduled Operator

- Government/Military

By Countest

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Leave a Reply