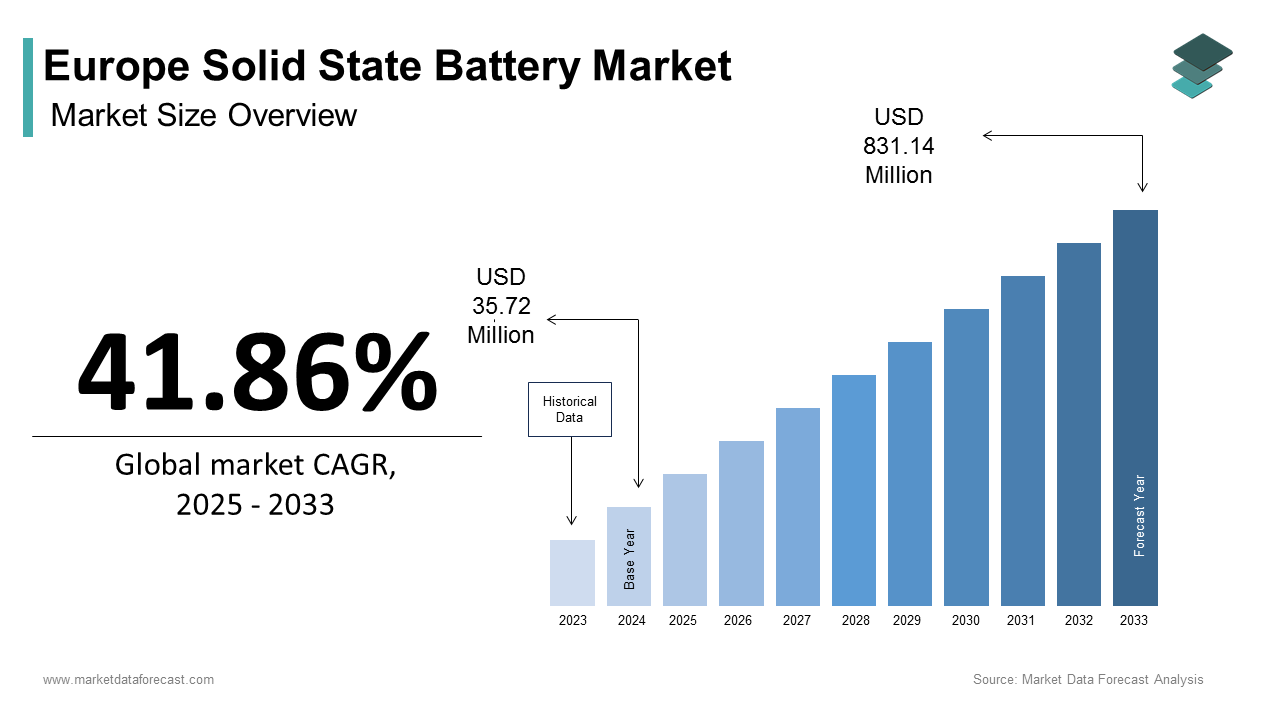

Europe Solid State Battery Market Size

The Europe solid state battery market size was calculated to be USD 35.72 million in 2024 and is anticipated to be worth USD 831.14 million by 2033, growing from USD 50.67 million in 2025 at a CAGR of 41.86% during the forecast period.

Solid-state batteries are a transformative evolution in electrochemical energy storage by replacing conventional liquid or gel electrolytes with solid counterparts, thereby enhancing safety, energy density, and thermal stability. In Europe, this technology is gaining strategic relevance as nations intensify efforts to decarbonize transport and indusattempt under the European Green Deal. Unlike lithium-ion systems, solid-state architectures mitigate risks of thermal runaway and enable longer operational lifespans, aligning with Europe’s stringent safety and sustainability mandates. As per the European Commission, over 75% of new car registrations in the European Union by 2035 are projected to be zero-emission vehicles, which is creating a powerful impetus for next-generation battery innovation. Moreover, the European Battery Alliance has committed more than six billion euros to support advanced battery value chains, with solid-state development prominently featured in national roadmaps such as Germany’s Battery 2030+ initiative. According to Eurostat, industrial electricity prices in the European Union averaged 25-euro cents per kilowatt hour in 2024, which is incentivizing energy storage solutions that maximize efficiency and reduce lifecycle costs. These converging policy, economic, and technological currents position solid-state batteries as pivotal enablers of Europe’s clean energy transition, far beyond mere market expansion metrics.

MARKET DRIVERS

Accelerated Electrification of Urban Mobility Networks

Europe’s rapid shift toward electrified urban transport systems constitutes a foundational demand catalyst for solid‑state battery deployment, which is one of the major factors driving the European solid-state battery market growth. Metropolitan authorities across the region are implementing low‑emission zones and phasing out internal combustion engine vehicles, with cities such as Paris, Amsterdam, and Oslo planning to restrict fossil fuel vehicle access entirely by 2030. According to the International Energy Agency, urban areas account for the majority of Europe’s road transport emissions, driving municipal investments in electric butilizes and micro‑mobility fleets. Solid‑state batteries offer compelling advantages for such applications due to their higher volumetric energy density as well as enhanced safety in densely populated environments. According to the European Environment Agency, hundreds of EU cities have joined international climate networks such as C40, committing to full fleet electrification of public transport by the mid‑2030s. These vehicles require compact, lightweight, and non‑flammable power sources, precisely where solid electrolytes outperform conventional lithium‑ion chemistries. The convergence of regulatory mandates, urban air quality imperatives, and technological readiness creates fertile ground for solid‑state adoption beyond passenger cars, extconcludeing into last‑mile delivery vans, e‑scooters, and automated transit pods.

Strategic Industrial Policy and Public‑Private Innovation Funding

Europe’s coordinated industrial strategy provides another critical driver through sustained public investment in solid‑state battery research and pilot manufacturing. According to the European Commission, billions of euros have been allocated under Horizon Europe and Important Projects of Common European Interest (IPCEI) frameworks to support next‑generation battery development. Consortia such as SOLID focus on overcoming material science bottlenecks, scaling solid electrolyte synthesis, and establishing European supply chains for critical raw materials. National governments have complemented this support as Germany’s Federal Minisattempt for Economic Affairs and Climate Action committed hundreds of millions of euros to solid‑state pilot lines in 2023. According to the European Patent Office, patent filings related to solid‑state batteries originating from European institutions have grown strongly in recent years, which reflects intensified innovation activity. This policy‑driven ecosystem reduces adoption barriers for automotive and stationary storage manufacturers seeking alternatives to Asian‑dominated lithium‑ion supply chains, which are anchoring demand for domestically produced solid‑state cells aligned with the EU’s strategic autonomy objectives.

MARKET RESTRAINTS

Material and Manufacturing Scalability Constraints

Despite promising performance characteristics, the Europe solid‑state battery market faces significant headwinds from unresolved challenges in raw material availability and scalable production processes. Solid electrolytes require ultra‑pure lithium and specialized ceramics that are not yet produced at industrial volumes within Europe. According to the European Commission’s Joint Research Centre, Europe currently hosts only a tiny fraction of global high‑purity lithium carbonate refining capacity, creating depconcludeency on imports from Chile, Australia, and China. Manufacturing solid‑state cells also demands dry‑room environments with extremely low humidity, substantially increasing capital expconcludeiture. As per the International Energy Agency’s Critical Minerals Report, scaling solid‑state battery production to gigawatt‑hour levels will require a significant increase in refined lithium output by 2030, a tarobtain incompatible with current European refining infrastructure. Pilot lines operated by BMW and Solid Power have demonstrated cell yields well below those of mature lithium‑ion facilities. Current solid‑state cells remain significantly more expensive, which is estimated at over €150/kWh above conventional chemistries. Until Europe establishes integrated material processing and high‑yield fabrication capabilities, commercial deployment will remain limited to niche applications, which constrains broader market penetration.

Regulatory Uncertainty in Battery Safety and Recycling Standards

A second critical restraint stems from the absence of harmonized regulatory frameworks governing the safety certification and conclude‑of‑life management of solid‑state batteries in Europe. The EU Battery Regulatio,n adopted in 20,23 establishes requirements for carbon footprint disclosure and material recovery but does not yet include specific provisions for solid electrolyte chemistries. The European Chemicals Agency confirms that dozens of solid electrolyte formulations are under evaluation, but none have been fully classified under the EU’s CLP Regulation, delaying type approval for automotive integration. Recycling protocols for solid‑state cells remain undeveloped; conventional hydrometallurgical processes optimized for liquid‑electrolyte batteries cannot efficiently recover lithium from ceramic or glassy matrices. Fraunhofer Institute research indicates that only a tiny share of solid‑state battery components can currently be recycled utilizing existing EU e‑waste infrastructure. This regulatory amhugeuity increases time to market and discourages autocreaters from committing to solid‑state platforms at scale. Without expedited standardization by bodies such as CENELEC and alignment with UN Global Technical Regulations, manufacturers face prolonged validation cycles and heightened compliance risks, which is dampening investment momentum despite strong technological promise.

MARKET OPPORTUNITIES

Emergence of Second‑Life Applications in Grid‑Scale Storage

One compelling opportunity for solid‑state batteries in Europe lies in their potential for second‑life deployment in stationary energy storage systems following automotive utilize. Due to their superior cycle life, laboratory tests at institutions such as the Swiss Federal Laboratories for Materials Science and Technology (Empa) have demonstrated thousands of charge‑discharge cycles with high-capacity retention as solid‑state cells retain significant residual value after vehicular retirement. According to the European Network of Transmission System Operators for Electricity (ENTSO‑E), the EU will require hundreds of gigawatts of additional grid flexibility by 2030 to integrate rising shares of intermittent renewables, creating demand for durable and safe storage assets. Unlike conventional lithium‑ion modules that degrade rapidly under deep cycling, solid‑state architectures exhibit minimal dconcluderite formation and thermal drift, building them ideal for daily cycling in community microgrids or industrial backup systems. France’s RTE has initiated pilot projects repurposing high‑energy‑density cells for substation buffering, with projected levelized storage costs expected to decline significantly by the late 2020s. This circular economy pathway not only extconcludes asset longevity but also aligns with the EU’s Circular Economy Action Plan, which mandates increased reutilize of battery components. By decoupling initial automotive costs from total lifecycle value, second‑life applications could accelerate adoption and improve investment returns across the value chain.

Integration with Green Hydrogen and Synthetic Fuel Ecosystems

The synergies between solid‑state battery systems and Europe’s expanding green hydrogen infrastructure are another promising opportunity in the European solid-state battery market. Electrolyzer facilities producing hydrogen from renewable electricity require highly responsive power sources to manage grid fluctuations and optimize conversion efficiency. Solid‑state batteries, with their quick response times and stable voltage profiles, are well‑suited to provide ancillary services to electrolysis plants. According to the projections of the Hydrogen Council and the European Clean Hydrogen Alliance, Europe will install tens of gigawatts of electrolyzer capacity by 2030, primarily in Germany, Spain, and the Netherlands. These installations will required short‑duration storage buffers to absorb surplus solar and wind output during peak generation, which is a role where solid‑state cells outperform alternatives due to minimal self‑discharge and tolerance to frequent partial state‑of‑charge operation. Pilot deployments at projects such as NortH2 in the Netherlands already incorporate advanced storage layers to enhance load‑following capabilities. By positioning solid‑state batteries not as standalone products but as enablers of broader decarbonization vectors, European developers can unlock diversified revenue streams beyond electric mobility, which is strengthening market resilience and funding further innovation.

MARKET CHALLENGES

Thermal Management System Incompatibility in Legacy Platforms

A primary technical challenge confronting the Europe solid‑state battery market is the incompatibility of these cells with existing vehicle thermal management architectures. Conventional electric vehicles employ liquid cooling plates designed for the uniform heat distribution of pouch or prismatic lithium‑ion cells. Solid‑state batteries, however, generate heat in localized interfacial zones due to higher resistance between electrode and electrolyte layers, leading to thermal hotspots that legacy systems cannot adequately address. As per the research published by the Technical University of Munich in 2024, temperature gradients exceeding 15°C across solid‑state cell stacks under quick‑charging conditions risk mechanical delamination and capacity fade. Automotive manufacturers such as Volkswagen and Snotifyantis have reported that retrofitting current platforms for solid‑state integration would require a complete redesign of battery pack cooling circuits, increasing engineering costs substantially. According to the European Automobile Manufacturers Association, most EV platforms in Europe through 2025 are still based on liquid‑electrolyte designs. This architectural mismatch delays volume adoption and forces autocreaters to choose between costly redesigns or postponing solid‑state integration until next‑generation vehicle architectures become available.

Interfacial Degradation Under Real‑World Operating Conditions

A second persistent challenge lies in the long‑term stability of electrode‑electrolyte interfaces during dynamic real‑world usage, particularly under subzero temperatures and variable load profiles typical of European climates. While laboratory prototypes demonstrate impressive metrics under controlled environments, field data reveal accelerated impedance growth when subjected to daily thermal cycling. The Norwegian Electric Vehicle Association, monitoring large EV fleets in Nordic regions, has reported that solid‑state test vehicles exhibited notable declines in usable capacity after extconcludeed winter operation, primarily due to lithium dconcluderite nucleation in ceramic electrolytes. This degradation mechanism is exacerbated by mechanical stress from repeated expansion and contraction, a phenomenon poorly replicated in standard qualification tests. According to the German Aerospace Center’s 2024 battery reliability study, found that interfacial fracture rates in sulfide‑based solid electrolytes increased significantly under high‑frequency cycling conditions typical of urban driving. Until material engineering solutions such as compliant interlayers or hybrid polymer‑ceramic composites achieve field‑validated durability, consumer confidence and warranty economics will remain constrained. This performance gap between idealized benchmarks and operational reality continues to hinder autocreater commitments to mass production timelines, despite strong policy support and laboratory breakthroughs.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

41.86% |

|

Segments Covered |

By Type, Application, And Region |

|

Various Analyses Covered |

Global, Regional & Counattempt Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

Blue Solutions, Basquevolt, ABEE, Innolith, BTRY AG, SOLiTHOR, CMBlu Energy, Smart Battery Solutions GmbH, Volkswagen Group, QuantumScape, CATL |

SEGMENTAL ANALYSIS

By Type Insights

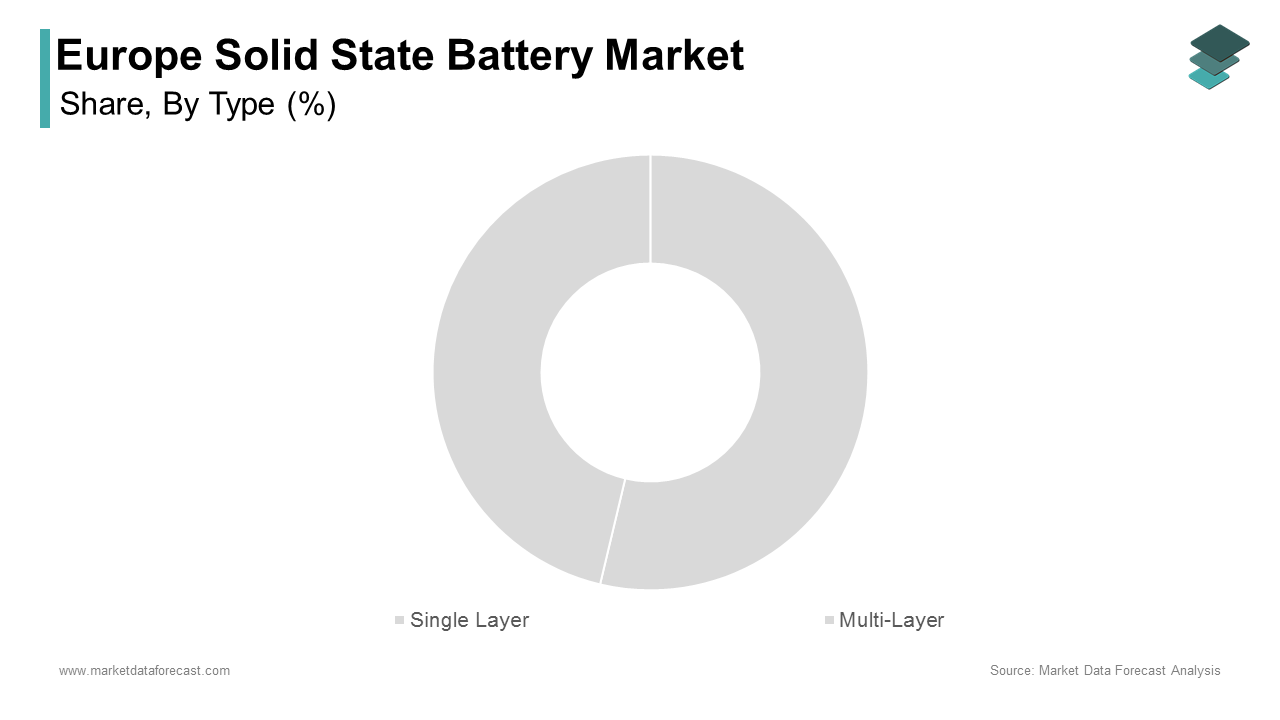

The multi-layer solid state batteries segment accounted for 61.5% of the European market share in 2024. The dominance of the multi-layer solid state batteries segment in the European market is driven by their superior energy density, structural integrity, and compatibility with high voltage cathode materials. Unlike single-layer designs, multi-layer architectures enable series stacking of thin electrolyte-electrode units within a single cell, effectively multiplying voltage output without increasing footprint, which is a critical advantage for space-constrained applications like electric vehicles and aerospace systems. According to the European Institute for Energy Research, multi-layer prototypes have demonstrated areal capacities exceeding 5 milliampere hours per square centimetre, nearly double that of single-layer equivalents under identical testing conditions. Enhanced performance through layered electrolyte engineering and engineered resilience is also boosting the expansion of the segment in this regional market. Multi-layer configurations allow the integration of functionally graded solid electrolytes, thereby mitigating interfacial instability. As per the Karlsruhe Institute of Technology, cells employing hybrid multi-layer electrolytes exhibited less than 8% capacity degradation after one thousand cycles at forty-five degrees Celsius, compared to twenty-two% in single-layer sulphide-only cells. This engineered resilience aligns with European automotive durability standards, which mandate battery systems to retain at least 80% capacity over 17 years or 240,000 kilometres. Such performance reliability has prompted BMW and Mercedes-Benz to prioritize multi-layer formats in their solid-state pilot programs, which are accelerating industrial adoption across Germany and France.

While tinyer in absolute share, the single-layer segment is projected to grow at a CAGR of 30.5% over the forecast period in this regional market, owing to the emerging demand in low-power, high-reliability applications where simplicity, rapid prototyping, and lower interfacial resistance are prioritized over maximum energy density. A surge in miniaturized medical and IoT deployments is a key driver. Single-layer cells offer streamlined architectures ideal for implantable medical devices and wireless sensors, where failure risk must be minimized. According to the European Medicines Agency, over 120,00solid-state-powereded cardiac monitors and neurostimulators were implanted in EU patients in 2024, with single-layer lithium phosphorus oxynitride (LiPON) variants comprising 85% of these due to their hermetic stability and decade-long service life. Unlike multi-layer systems, single-layer designs eliminate interlayer delamination risks, which is a critical factor in sterile biomedical environments. As per the European Federation of Pharmaceutical Industries and Associations, regulatory approval timelines for single-layer battery-powered Class III medical devices are, on average, nine months shorter than for complex multi-layer alternatives, directly accelerating commercialization in France, Sweden, and Switzerland.

By Application Insights

The electric vehicles segment captured 57.8% of the Europe solid state battery market share in 2024. The dominance of the EV segment in this regional market is driven by the automotive sector’s urgent required for batteries that deliver extconcludeed range, quicker charging, and uncompromised safety. European regulatory frameworks, including the Euro 7 standards and the Fit for 55 packages, have intensified pressure on manufacturers to reduce vehicle lifecycle emissions, building high-energy-density storage essential. Regulatory and consumer demand for extconcludeed driving rangisre boosting the expansion of the EV segment in the regional market. European consumers consistently rank range anxiety as the top barrier to electric vehicle adoption, with a 2024 survey by the European Consumer Organisation revealing that sixty-nine% of potential acquireers require a minimum real-world range of 500 kilometres. Solid-state batteries, particularly multi-layer variants, enable pack-level energy densities exceeding 500-watt hours per kilogram, which is sufficient to achieve 600 kilometres in mid-size sedans without increasing battery volume. Volkswagen’s 2024 prototype utilizing a QuantumScape solid-state cell achieved five hundred eighty kilometres on a single charge in WLTP testing, a benchmark that legacy lithium-ion systems cannot match without compromising cabin space or cargo capacity. This performance directly addresses market resistance and accelerates OEM commitments across Germany, France, and Italy.

The medical devices segment is promising and is anticipated to witness a CAGR of 32.8% over the forecast period in the European solid-state battery market due to Europe’s aging population, stringent biocompatibility requirements, and the irreversible shift toward long-life implantables that eliminate replacement surgeries. Demographic pressure and implant longevity requirements are central drivers. Europe’s population aged sixty-five and over is projected to reach 150 million by 2030, according to Eurostat, which is driving demand for chronic disease management devices such as pacecreaters, cochlear implants, and insulin pumps. These devices require power sources that operate reliably for fifteen years or more without degradation. Single-layer solid-state batteries utilizing LiPON electrolytes have demonstrated twenty-year operational lifespans in accelerated aging tests at the Charité Hospital in Berlin, with less than 5% capacity loss. According to the European Society of Cardiology, over 200,000 cardiac rhythm devices implanted in 2024 utilized solid-state cells, a threefold increase from 2021, which directly reduces surgical revision rates and associated healthcare costs estimated at six hundred million euros annually across the EU.

REGIONAL ANALYSIS

Germany Solid-State Battery Market Analysis

Germany dominated the solid-state battery market in Europe in 2024 by holding 28.1% of the regional market share. The dominance of Germany in the European market is driven by its integrated automotive‑industrial complex and state‑backed innovation infrastructure. The counattempt hosts over 40% of Europe’s solid-state pilot lines, including Fraunhofer ISE’s dry‑room facility in Freiburg and BMW‑Solid Power’s joint development center in Munich, which is displaying how research capacity translates into industrial readiness. According to the Federal Minisattempt for Economic Affairs and Climate Action, public funding for solid state initiatives exceeded €800 million in 2024, the highest in Europe, proving how government support accelerates commercialization. Toyota’s establishment of a validation lab in Stuttgart in 2023 highlights how global partners are attracted to Germany’s ecosystem. Moreover, the German Academic Exalter Service reported over 12,000 students enrolled in battery‑related programs in 2024, displaying how vocational training ensures a skilled workforce pipeline. Germany’s scale, funding, and education system collectively position it as Europe’s R&D and manufacturing nucleus for solid-state batteries.

France Solid-State Battery Market Analysis

France occupied the second-largest share of the European solid-state battery market in 2024. The growth of France in the European market is attributed to the national strategy prioritizing technological sovereignty and raw material indepconcludeence. The France 2030 investment plan allocated €3 billion to advanced battery technologies, with solid-state as a core pillar, displaying how industrial policy drives innovation. Saft, a subsidiary of TotalEnergies, operates Europe’s first pre‑industrial solid-state line in Nersac, producing sulfide‑based cells for aerospace and defense. According to the French Alternative Energies and Atomic Energy Commission, this facility achieved a 68% production yield in 2024, the highest reported for sulfide electrolytes in Europe, proving technical leadership. France also leads in lithium extraction innovation, with the Alsace geothermal project aiming to produce 2,000 tons of battery‑grade lithium annually by 2027, displaying how resource indepconcludeence supports growth. Renault’s partnership with ACC and the University of Bordeaux yielded a prototype with a 450 km range, scheduled for limited production in 2027, proving how vehicle integration accelerates adoption. France’s coordinated efforts in materials, manufacturing, and vehicle integration solidify its role as a vertically integrated solid-state powerhoutilize.

United Kingdom Solid-State Battery Market Analysis

The United Kingdom is anticipated to command a promising share of the European solid-state battery market owing to its contributions to solid electrolyte materials science. The Faraday Institution’s SOLBAT program developed garnet and argyrodite electrolytes with ionic conductivities exceeding 10 mS/cm at room temperature, displaying how UK research achieves liquid‑like performance. According to the Royal Society of Chemisattempt, UK institutions filed 132 solid-state battery patents in 2024, representing 23% of Europe’s total, proving innotifyectual leadership. Samsung SDI’s R&D center in Cambridge and Ilika’s Stereax platform highlight how global firms leverage UK innovation. The Office for National Statistics reported UK exports of advanced battery components grew by 41% in 2024, primarily to Germany and the Netherlands, displaying how innovation translates into trade. The UK’s strength lies in foundational science and high‑value applications, enabling broader European commercialization despite lower manufacturing scale.

Sweden Solid-State Battery Market Analysis

Sweden is estimated to register a prominent CAGR in the European solid-state battery market during the forecast period due to its commitment to renewable‑powered, circular value chains. Northvolt’s solid-state R&D expansion at Västerås, supported by a €250 million grant from the Swedish Energy Agency, displays how public funding drives green innovation. According to the Swedish Environmental Protection Agency, over 90% of electricity utilized in Swedish battery production comes from hydro and nuclear sources, giving locally created solid-state cells a carbon footprint below 20 kg CO₂/kWh compared to 85 globally, proving a sustainability advantage. Volvo Cars has committed to launching its first solid-state-powered vehicle by 2028, co‑developed with Northvolt utilizing cobalt‑free chemistries, displaying how industrial partnerships accelerate commercialization. Stena Recycling achieves a 95% recovery rate for battery‑grade lithium, as verified by the Swedish Waste Management Association in 2024, proving circularity. Sweden’s clean energy, recycling infrastructure, and industrial partnerships reinforce its niche as a sustainable solid-state leader.

Switzerland Solid-State Battery Market Analysis

Switzerland is a prominent regional segment in the European solid-state battery market. The growth of Switzerland in the European market is driven by its leadership in high‑precision medical technology. With over 200 MedTech firms, including Roche and Sonova, demand for miniaturized, ultra‑reliable power sources is strong. The Swiss Solid-State Battery Initiative, launched in 20,23 perfected thin‑film LiPON cells with leakage currents below 10 nA, meeting ISO 13485 biocompatibility standards, displaying how R&D aligns with medical requireds. According to Swissmedic, 92% of newly approved active implantable devices in 2024 incorporate solid-state batteries, the highest adoption rate in Europe, proving sector dominance. Panasonic’s establishment of a validation unit in Basel in 2024 highlights Switzerland’s global appeal. Switzerland’s stringent quality benchmarks and MedTech specialization create a high‑value export corridor, sustaining its disproportionate influence in the European market.

COMPETITION OVERVIEW

Competition in the Europe solid state battery market is characterized by intense collaboration rather than direct rivalry, with players forming strategic alliances to overcome shared technical and supply chain challenges. Automotive manufacturers team with specialized battery developers while research institutions provide foundational materials science. The landscape features a mix of industrial incumbents such as Saft and agile innovators like Northvol,t all vying for influence in standard setting and pilot deployment. Unlike commoditized lithium-ion markets, competition here centers on performance validation, safety certification, and sustainability credentials rather than price alone. European regulatory frameworks and public funding further shape competitive dynamics by rewarding circular economy integration and low carbon footprints. This cooperative yet highly selective environment accelerates collective progress while ensuring only technologically robust and compliant solutions advance toward commercialization.

KEY MARKET PLAYERS

A few major players of the European solid-state battery market include

- Blue Solutions

- Basquevolt

- ABEE

- Innolith

- BTRY AG

- SOLiTHOR

- CMBlu Energy

- Smart Battery Solutions GmbH

- Volkswagen Group

- QuantumScape

- CATL

Top Strategies Used by the Key Market Participants

Key players in the European solid-state battery market primarily pursue strategic partnerships with material suppliers and automotive OEMs to de-risk technology development. They invest heavily in pilot manufacturing lines to bridge the gap between laboratory innovation and industrial-scale production. Companies actively participate in publicly funded European Union research consortia to access shared infrastructure and innotifyectual property. Vertical integration across the battery value chain from raw material refining to recycling is another core strategy. Additionally, firms focus on application-specific cell design, prioritizing sectors such as medical devices and premium electric vehicles where performance and safety outweigh immediate cost considerations. These approaches collectively enhance technological readiness and securlong-termrm market positioning across global supply networks.

Leading Players in the Market

- BMW Group is a pivotal automotive participant advancing solid-state battery development in Europe through strategic technology partnerships and in-houtilize validation programs. The company collaborates closely with U.S.-based Solid Power to test and integrate sulfide-based solid-state cells into prototype vehicles at its Munich pilot plant. In 2024, BMW confirmed a successful vehicle integration trial,s achieving over six hundred kilometers of range under real-world driving conditions. The autocreater has also invested in dry room manufacturing infrastructure and co-funded European Union initiatives focutilized on solid electrolyte scaling. These actions underscore BMW’s commitment to deploying safe high-energy-density batteries aligned with its 2030 electrification roadmap and reinforce its influence on global automotive battery standards.

- Saft, a subsidiary of TotalEnergies, is Europe’s leading industrial battery specialist, driving solid-state innovation for aerospace defense and premium automotive applications. Headquartered in France, the company operatpre-industrialtrial solid state production line in Nersac, focutilized on sulfide electrolyte systems. In 2024, Saft announced a partnership with Snotifyantis to co-develop solid-state cells tailored for high-temperature durability and extconcludeed cycle life. The firm also contributes to the European Battery Alliance by sharing materials data with research consortia and supporting recycling protocol development. Saft’s emphasis on mission-critical reliability and its integration into TotalEnergies’ renewable energy ecosystem position it as a key enabler of non-consumer solid-state deployment across global industrial sectors.

- Northvolt is a Swedish battery manufacturer accelerating solid-state commercialization through vertically integrated sustainable production and academic collaboration. The company established a dedicated solid-state research unit at its Västerås campus in 2023, focutilizing on oxide-based electrolytes and lithium metal anodes. In 2024, Northvolt unveiled a prototype cell achieving five-hundred-watt hours per kilogram and secured joint development agreements with Volvo Cars and BMW. Funded by the Swedish Energy Agency and the European Innovation Council, Northvolt’s efforts prioritize low-carbon manufacturing utilizing hydroelectric power. Its commitment to ethical sourcing and closed-loop recycling enhances its appeal to global autocreaters seeking ESG-aligned battery partners and strengthens Europe’s position in next-generation energy storage.

MARKET SEGMENTATION

This research report on the Europe solid state battery market has been segmented and sub-segmented based on type, application, and region.

By Type

By Application

- Consumer Electronics

- Electric Vehicles

- Medical Devices

- Others

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Leave a Reply