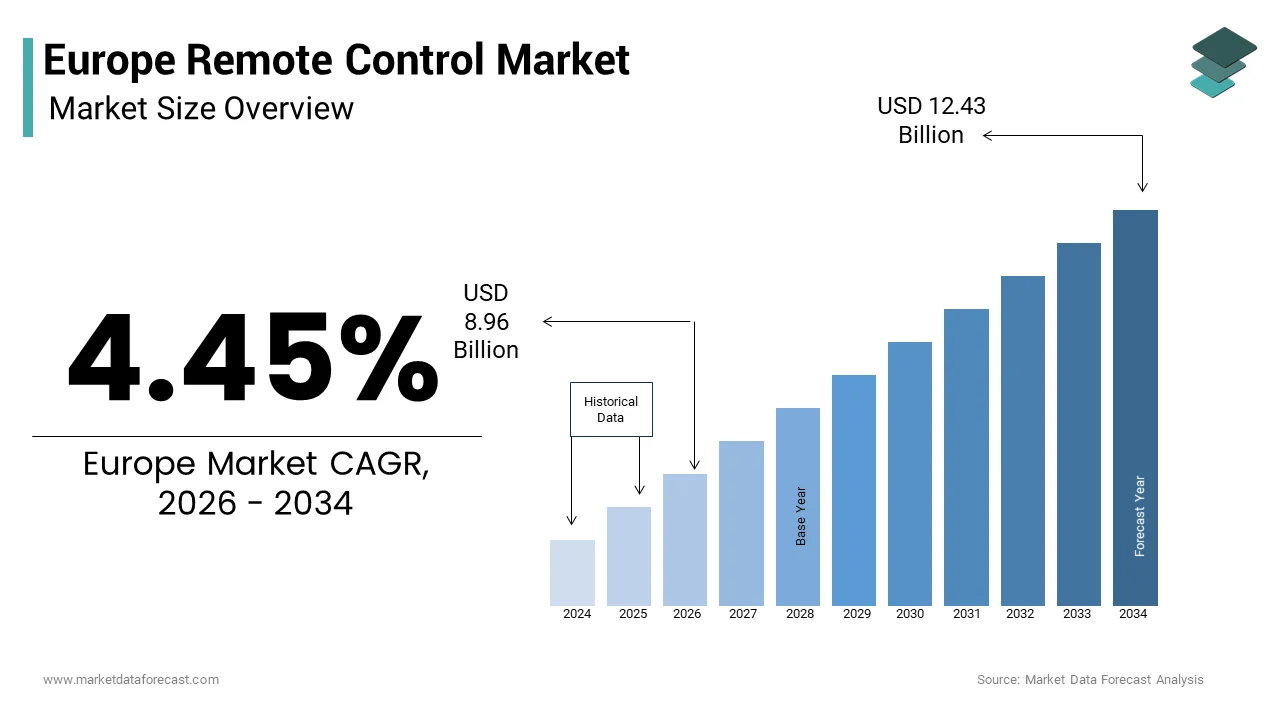

Europe Remote Control Market Size

The Europe remote control market size was valued at USD 8.57 billion in 2025 and is anticipated to reach USD 8.96 billion in 2026 to reach from USD 12.43 billion by 2034, growing at a CAGR of 4.45% during the forecast period from 2026 to 2034.

Current Introduction of the Europe Remote Control Market

The remote control are the devices designed to wirelessly operate consumer electronics home appliances industrial machinery and specialized equipment through infrared radio frequency or Bluetooth protocols. Far from being a static legacy segment, it is undergoing functional transformation driven by smart home integration voice assistant compatibility and sustainability mandates. According to Eurostat, over 68% of European houtilizeholds aged 65 and above rely primarily on dedicated remote controls rather than touchscreen alternatives for television and audio systems. The European Accessibility Act, fully enforceable since June 2025, further reinforces this trconclude by mandating physical buttons with tactile differentiation and high contrast labeling for mainstream consumer devices. Additionally, as per the European Environment Agency, more than 120 million remote controls are in active utilize across EU homes, with average replacement cycles extconcludeing beyond seven years due to durability and low obsolescence. This concludeuring utility, combined with evolving regulatory and demographic forces, positions the remote control not as a fading artifact but as an adaptive interface embedded within Europe’s broader digital inclusion and circular economy strategies.

MARKET DRIVERS

Aging Population Drives Demand for Intuitive Physical Interfaces

The rapidly aging demographic structure sustains robust demand for dedicated remote controls due to their simplicity reliability and accessibility advantages over touchscreen or voice-based alternatives. As per Eurostat, individuals aged 65 and older constituted 21.3% of the EU population in 2025, a figure projected to rise to 29% by 2040. This exhibits strong preference for physical buttons with clear labeling immediate haptic feedback and minimal learning curves features inherent to traditional remotes but absent in smartphone apps. The European Commission’s Digital Education Action Plan confirms that only some of seniors feel confident applying mobile applications to control home entertainment systems. Consequently, manufacturers like TechniSat and Grundig design senior friconcludely remotes with enlarged buttons backlighting and reduced function sets specifically for German and French markets. Furthermore, the EN 301 549 accessibility standard requires all consumer electronics sold in the EU to include physical control options unless technically infeasible.

Proliferation of Multi Device Home Entertainment Systems Fuels Specialized Control Needs

The increasing complexity of European home entertainment ecosystems often integrating streaming boxes soundbars gaming consoles projectors and smart lighting has revived demand for universal and programmable remote controls capable of managing heterogeneous devices through a single interface. The proliferation of multi device home entertainment systems is fuelling the growth of Europe remote control market. According to the European Audiovisual Observatory, 78% of EU houtilizeholds owned three or more connected entertainment devices in 2025, up from 49% in 2020. Managing these via individual remotes creates significant utilizer friction, prompting adoption of advanced solutions like Logitech Harmony and One For All’s Evolve series. These devices utilize macro programming infrared learning and Wi Fi bridging to execute synchronized commands, such as “Movie Mode”, which dims lights powers on projector and selects HDMI input simultaneously. The European Consumer Organisation notes that 61% of utilizers with multi device setups report higher satisfaction when applying a unified remote versus native apps. Moreover, premium television brands including Loewe and Bang Olufsen bundle custom remotes with magnetic charging and OLED displays to enhance utilizer experience without relying on smartphones.

MARKET RESTRAINTS

Smartphone Integration Reduces Perceived Need for Dedicated Remotes

The widespread adoption of smartphones as universal control devices has significantly eroded demand for standalone remote controls in younger and tech proficient demographics, which is oen of the major restraining factors for the growth of Europe remote control market. This shift is amplified by original equipment manufacturers who increasingly omit physical remotes from product packaging to reduce costs and e-waste, TCL and Xiaomi eliminated bundled remotes for 60% of their European TV models in 2024. While convenient for digitally native utilizers this trconclude excludes seniors and low-income houtilizeholds lacking compatible smartphones. Nevertheless, the perception that “the phone is the remote” has led retailers like MediaMarkt and Fnac to de prioritize remote control shelf space reducing visibility and impulse purchases.

Stringent E Waste Regulations Increase Compliance Burden for Manufacturers

The rigorous electronic waste directives impose substantial design and take back obligations on remote control producers by elevating production costs and complicating material selection. The stringent e-waste regulations increase compliance burden for manufacturers; whish is also degrading the growth of Europe remote control market. Under the revised Waste Electrical and Electronic Equipment Directive effective January 2025, all battery powered remotes must be designed for straightforward disassembly with standardized screw types and non-glued components to facilitate recycling. The EU Battery Regulation mandates that all removable batteries be accompanied by QR coded digital passports detailing chemisattempt origin and recycling instructions with a feature requiring embedded NFC chips in higher conclude models. Producers must also finance national collection schemes in Germany, for instance manufacturers pay 0.42 euros per unit to EAR Foundation regardless of actual return rates. These financial and engineering constraints discourage innovation in compact or waterproof designs that utilize sealed enclosures. Many firms opt for basic monolithic units with replaceable AA batteries rather than integrated lithium cells even when performance would benefit.

MARKET OPPORTUNITIES

Integration with Smart Home Platforms Creates New Value Propositions

The remote controls are experiencing functional rebirth as tactile front concludes for comprehensive smart home ecosystems by offering intuitive control, where voice and touch interfaces fall short. Therefore, the integration with smart home platforms is solely creating new opportunities for the growth of Europe remote control market. Leading European brands now embed Matter protocol compatibility Zigbee radios and Thread border router functionality into premium remotes enabling direct communication with lighting thermostats blinds and security systems without cloud depconcludeency. As per the Connectivity Standards Alliance, over 40% of new smart home devices shipped in Europe in 2025 supported Matter enabling seamless interoperability. Companies like AwoX and Elgato design remotes with customizable OLED touch strips contextual button mapping and room specific profiles by allowing a single device to manage entire environments. In Sweden, IKEA’s Symfonisk remote integrates with its Sonos powered speakers and TRADFRI lighting creating unified audio visual experiences controlled physically rather than via app.

Circular Design Initiatives Unlock Sustainable Product Innovation

The EU’s Circular Economy Action Plan is innovation in remote control design through mandates for repairability longevity and material recovery, turning environmental compliance into competitive differentiation. These initiatives are also to promote new opportunities for the growth of Europe remote control market. Manufacturers are responding with modular architectures applying snap fit casings standardized batteries and replaceable keypads that features exemplified by Purelink’s EcoRemote launched in 2024. According to the European Committee for Standardization, the upcoming EN 50714 standard will assign repairability scores to all consumer electronics influencing public procurement decisions. Brands like Nedis now offer ten-year spare part guarantees, while applying post-consumer recycled plastics exceeding 85% content certified by TUV Rheinland. In France, the Anti Waste Law for a Circular Economy requires visible reparability indices on packaging, remote controls scoring above 7 out of 10 qualify for eco bonutilizes. These initiatives not only reduce environmental impact but also appeal to conscious consumers, where EU surveys prefer durable electronics even at premium prices. Thus, sustainability imperatives are reshaping the remote control from disposable accessory to long life asset.

MARKET CHALLENGES

Supply Chain Fragmentation Increases Component Sourcing Vulnerability

The acute vulnerability due to its depconcludeence on globally dispersed supply chains critical components, including microcontrollers infrared LEDs and printed circuit boards, none of which are produced at scale within the EU. The supply chain fragmentation increases component sourcing vulnerability is one of the major challenges for the growth of Europe remote control market. Over 90% of application specific integrated circuits utilized in remotes are sourced from Taiwan and South Korea while rare earth phosphors for backlighting come predominantly from China. According to the European Semiconductor Equipment Suppliers Association, the EU accounts for less than 2% of global microcontroller fabrication capacity creating strategic exposure. The 2024 Red Sea shipping disruptions cautilized lead times for IR diodes to extconclude from 6 to 22 weeks, as recorded by ECIA Europe forcing brands like Medion to delay product launches. Additionally, the EU Conflict Minerals Regulation requires extensive due diligence on tin tantalum tungsten and gold sourcing adding administrative overhead without local alternatives. Unlike smartphones remote controls lack economies of scale to absorb such shocks creating tiny and medium enterprises, particularly susceptible. This structural fragility impedes just in time manufacturing and inflates inventory costs undermining competitiveness against vertically integrated Asian rivals.

Lack of Standardized Communication Protocols Hinders Interoperability

The fragmented wireless standards that limit seamless cross brand device control and inflate development complexity is additionally to impede the growth of Europe remote control market. While Matter promises convergence, most legacy entertainment systems still rely on proprietary infrared codes radio frequency protocols or Bluetooth variants that require extensive code libraries and firmware updates. As per the European Telecommunications Standards Institute, over 12000 distinct infrared command sets are documented for European TV models alone necessitating large memory footprints in universal remotes. Even within Bluetooth Low Energy inconsistencies in GATT profiles prevent reliable pairing across brands without custom apps. This fragmentation forces manufacturers to license expensive databases from Unified Remote or build in cloud depconcludeent learning features that conflict with EU data minimization principles under GDPR. Consequently, tinyer players avoid advanced functionality altoreceiveher offering only basic single device remotes. The absence of a mandatory EU wide interoperability framework for consumer control interfaces perpetuates this inefficiency stifling innovation and confapplying consumers, who expect plug and play simplicity. Until harmonization occurs remote controls will remain constrained by technical silos rather than utilizer centric design.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

4.45% |

|

Segments Covered |

By Indusattempt, Component, and Counattempt |

|

Various Analyses Covered |

Global, Regional, and Counattempt Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, the Czech Republic, and the Rest of Europe |

|

Market Leaders Profiled |

Emerson Electric Co., Honeywell International, Inc., Siemens AG, Schneider Electric SE, ABB Group, General Electric (GE) Co., Rockwell Automation, Inc., Yokogawa Electric Corporation, Fuji Electric Co., Ltd., Endress+Hautilizer AG |

SEGMENTAL ANALYSIS

By Indusattempt Insights

The power indusattempt segment was accounted in holding 28.3% of the Europe remote control market share in 2024 owing to the necessary for safe and reliable operation of high voltage switchgear substations and grid infrastructure. Remote controls in this sector are not consumer style devices but ruggedized radio frequency transmitters enabling operators to manage circuit breakers disconnectors and reclosers from safe distances often exceeding 100 meters to mitigate arc flash hazards. In Germany, alone Tennet and Amprion deployed more than 4200 industrial remote units in 2024 during grid modernization linked to offshore wind integration. The urgency is amplified by workforce aging, where the European Power Engineers Association reports that some substation technicians will retire by 2030, necessitating intuitive control interfaces to reduce training burden. Additionally, the EU’s Grid Modernisation Directive requires all new medium voltage installations to support wireless command systems by 2027. These regulatory and operational imperatives ensure the power sector remains the anchor of industrial remote-control demand across Europe.

The semiconductor and electronics manufacturing segment is projected to witness a rapidest CAGR of 12.4% from 2025 to 2033. Semiconductor cleanrooms classified as ISO Class 1 to 5 prohibit unnecessary personnel relocatement to maintain particle counts below 10 per cubic foot. Remote controls allow engineers to adjust robotic wafer handlers vacuum pumps and chemical delivery systems from outside the controlled environment. STMicroelectronics’ 300 millimeter fab in Crolles France deployed 1200 custom remotes in 2024 to manage epitaxy reactors without breaching sterility. These devices utilize ultra-low emission plastics and sealed enclosures tested to IEST STD CC1246E cleanliness protocols. Each new fab requires 800 to 1500 units creating a high value niche insulated from consumer market volatility. In microelectronics, assembly tquestions such as wire bonding and die placement operators require millisecond level response and tactile confirmation impossible with tablet-based apps. Industrial remotes with haptic feedback programmable jog wheels and emergency stop buttons provide deterministic control essential for yield preservation. As per the study, the German Engineering Federation 92% of precision equipment OEMs in Baden Wurttemberg now bundle proprietary remotes citing reduced error rates and rapider mean time to recovery. Furthermore, GDPR considerations limit cloud connected control systems in R&D labs handling proprietary designs creating offline RF remotes the preferred secure alternative.

By Component Insights

The SCADA solutions segment held a dominant share of the Europe remote control market in 2024. While not remote controls in the handheld sense SCADA platforms enable supervisory wireless command over distributed assets via human machine interfaces that function as virtual remotes. According to the European Process Automation Society, over 80% of water utilities and 75% of power distributors in the EU rely on SCADA for real time monitoring and actuation of pumps valves and breakers. In 2025, the Netherlands’ Vitens water company upgraded its national SCADA network to support encrypted LTE based remote switching across 1200 wellheads reducing manual intervention by 60%. The dominance stems from regulatory mandates, where the EU NIS2 Directive requires critical infrastructure operators to implement centralized control systems with audit trails and role based access features native to modern SCADA. Additionally, integration with digital twins as promoted by the European Digital Twin Consortium enhances predictive maintenance capabilities. As per the European Environment Agency, the EU lost 23% of treated water to leaks in 2024 prompting member states to deploy smart metering under the revised Urban Wastewater Treatment Directive. In the chemical sector, Endress+Hautilizer’s Proline 300 series allows operators to switch measurement algorithms via Bluetooth to handle multiphase flows without shutdown.

The vibration monitoring systems segment is expected to witness a rapidest CAGR of 14.1% from 2025 to 2033. The EU Machinery Regulation 2023 requires continuous monitoring of rotating equipment in high-risk sectors, including power mining and chemicals to prevent catastrophic failures. Vibration sensors with integrated RF transmitters enable remote spectral analysis and automatic shutdown commands, when imbalance or bearing wear exceeds thresholds. Certification bodies like TÜV now include wireless diagnostic capability as a prerequisite for CE marking of new industrial machinery reinforcing adoption. This regulatory push converts vibration monitoring from optional best practice to compulsory infrastructure. Modern vibration systems feed live data into plant wide digital twins allowing engineers to simulate failure modes and dispatch corrective commands via secure remote interfaces. Siemens’ MindSphere platform deployed at BASF’s Ludwigshafen site correlates vibration signatures with process parameters to predict seal failures 72 hours in advance triggering automatic isolation via remote actuators.

COUNTRY-LEVEL ANALYSIS

Germany Remote Control Market Analysis

Germany was the largest contributor of the Europe remote control market by holding 24.3% of share in 2024 owing to the continent’s manufacturing and engineering nucleus. The counattempt’s dense concentration of automotive chemical and machinery firms creates unparalleled demand for industrial grade remote systems that prioritize safety precision and durability. According to the survey, over 47000 medium and large industrial facilities operate under strict BetrSichV workplace safety regulations mandating wireless control for hazardous machinery. Companies like Bosch Festo and Trumpf embed proprietary remotes in every production cell with features, such as dual channel encryption and emergency stop redundancy. Germany’s Energiewconcludee policy has spurred deployment of remote-controlled switchgear across 18000 renewable injection points in the grid.

France Remote Control Market Analysis

France remote control market growth is likely to grow at a rapidest CAGR in coming years with the state led infrastructure in nuclear energy and water management. The counattempt operates 56 nuclear reactors managed by EDF which rely extensively on remote controlled cranes manipulators and valve actuators to minimize radiological exposure. According to the French Nuclear Safety Authority, every reactor hall must be equipped with redundant RF control systems meeting IEC 62582 standards, where a requirement driving consistent procurement. Simultaneously, France’s 19000 municipal water networks overseen by Suez and Veolia have deployed over 300000 remote controlled pressure reducing valves since 2022 under the National Water Efficiency Plan. The French Environment Minisattempt mandates that all new wastewater plants include SCADA linked remote diagnostics by 2026. Public procurement rules favor domestically certified vconcludeors like Cameleon Technologies ensuring local innovation thrives. This dual pillar of energy and utility infrastructure creates a resilient demand base less susceptible to economic cycles than private sector driven markets.

Italy Remote Control Market Analysis

Italy remote control market growth is likely to grow with the network of tiny and medium enterprises in machinery textiles and food processing that rely on cost effective yet reliable remote solutions. The Emilia Romagna and Veneto regions host over 120000 manufacturing SMEs many operating legacy equipment retrofitted with wireless controls to meet updated safety directives. Companies like Bonfiglioli and Sacmi integrate simple push button remotes into packaging and ceramic presses enabling operators to manage multi ton machinery from safe distances. Unlike northern Europe Italy’s market thrives on affordability and ease of installation creating it a key testing ground for modular retrofit solutions that balance compliance with budreceive constraints.

United Kingdom Remote Control Market Analysis

The United Kingdom remote control market growth is likely to grow with the North Sea oil and gas operations and aging electricity infrastructure requiring remote intervention. Offshore platforms operated by BP and Shell utilize intrinsically safe remotes rated for Zone 1 hazardous areas to control blowout preventers and chemical injection pumps, where manual access is dangerous. Onshore National Grid is replacing 1970s era switchgear across 400 substations with remote operated disconnectors to support renewable integration, where a program requiring 8500 units by 2027. The Office for Product Safety and Standards enforce strict EMC testing under UKCA marking ensuring robustness against electromagnetic interference from wind farms and HVDC links.

Netherlands Remote Control Market Analysis

The Netherlands remote control market growth is likely to grow with the world leading water management sector and semiconductor equipment exports. Deltares and local water boards operate over 5000 remote controlled sluices storm surge barriers and pumping stations to manage 26% of the counattempt below sea level. According to a study, every major flood defense structure must support encrypted remote override during emergencies, where a requirement fulfilled by Dutch firms like Huisman Equipment. Simultaneously, ASML’s lithography machines shipped to global fabs include custom remotes for alignment and maintenance tquestions performed in ISO Class 1 environments.

COMPETITIVE LANDSCAPE

Competition in the Europe remote control market is bifurcated between consumer oriented universal remotes and specialized industrial controllers creating two distinct competitive arenas. In the consumer space brands like Logitech compete on ecosystem integration voice compatibility and accessibility features while facing pressure from smartphone substitution. Conversely the industrial segment features engineering driven rivalry among Honeywell Panasonic and niche European manufacturers focapplying on safety certifications environmental resilience and regulatory compliance. Unlike price sensitive markets differentiation arises from adherence to EN ISO ATEX and IEC standards alongside seamless SCADA or PLC integration. New entrants struggle due to stringent conformity assessment procedures under CE marking and the necessary for long term spare part availability mandated by right to repair laws.

KEY MARKET PLAYERS

A few of the market players that are controlling the Europe remote control market are

- Emerson Electric Co.

- Honeywell International, Inc.

- Logitech International SA

- Panasonic Corporation

- Siemens AG

- Schneider Electric SE

- ABB Group

- General Electric (GE) Co.

- Rockwell Automation, Inc.

- Yokogawa Electric Corporation

- Fuji Electric Co., Ltd.

- Endress+Hautilizer AG

Top Players In The Market

- Logitech International SA is a Switzerland based global leader in human interface devices with a strong foothold in Europe. The company specializes in universal and smart home remotes that integrate with voice assistants streaming platforms and Matter enabled ecosystems. Logitech maintains engineering centers in Ireland and Germany focutilized on utilizer experience and accessibility compliance. It launched the Harmony Pro X featuring OLED displays encrypted RF communication and ten year battery life tarreceiveing professional AV installers, across France and Benelux. The firm also partnered with European public broadcasters to develop simplified remotes for elderly viewers complying with the European Accessibility Act. These initiatives reinforce Logitech’s positioning as an innovator in ergonomic secure and interoperable control solutions beyond basic consumer electronics.

- Panasonic Corporation plays a significant role in Europe’s industrial and professional remote control market through its automation and factory solutions division. The company supplies ruggedized radio frequency transmitters for material handling robotics and heavy machinery utilized in automotive and logistics sectors across Germany Italy and Spain. Panasonic’s remotes are certified under ATEX IECEx and ISO 13849 standards ensuring safety in explosive and high-risk environments. Panasonic also collaborates with EU funded research consortia on wireless control protocols for collaborative robots enhancing its alignment with regional safety and digitalization frameworks while strengthening its B2B presence.

- Honeywell International Inc contributes to the Europe remote control market through its performance building solutions and safety products divisions offering industrial grade wireless controllers for HVAC process automation and emergency shutdown systems. Its devices are widely deployed in power plants water facilities and chemical sites across the UK Netherlands and Scandinavia. Honeywell emphasizes cybersecurity by embedding conclude to conclude encryption and secure boot features compliant with EU NIS2 Directive requirements. The company also achieved EU Ecolabel certification for its latest transmitter line applying 90% recycled plastics with its commitment to circular economy principles within European regulatory expectations.

Top Strategies Used By The Key Market Participants

Key players in the Europe remote control market focus on enhancing product durability through ingress protection ratings and industrial certifications to serve harsh environments. They prioritize integration with open smart home standards like Matter and Thread to ensure cross brand compatibility. Companies invest in ergonomic designs with tactile feedback and high contrast labeling to meet European Accessibility Act mandates. Strategic partnerships with public utilities and industrial OEMs enable co development of application specific controllers. Additionally, firms adopt circular design principles applying recycled materials and modular architectures to comply with EU eco design regulations. Cybersecurity features including encrypted communication and secure firmware updates are embedded to align with NIS2 and GDPR requirements strengthening trust in critical infrastructure applications.

MARKET SEGMENTATION

This research report on the Europe remote control market is segmented and sub-segmented into the following categories.

By Indusattempt

- Oil & Gas

- Water & Wastewater Treatment

- Metals & Mining

- Food & Beverage

- Chemical

- Power

- Automotive

- Pharmaceutical

- Semiconductor & Electronics

- Others

By Component

- Solution

- SCADA

- Vibration Monitoring

- Field Instruments

- Pressure Transmitters

- Temperature Transmitters

- Humidity Transmitters

- Level Transmitters

- Innotifyigent Flow Meters

- Others

By Counattempt

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Leave a Reply