Europe Public Cloud Market Size

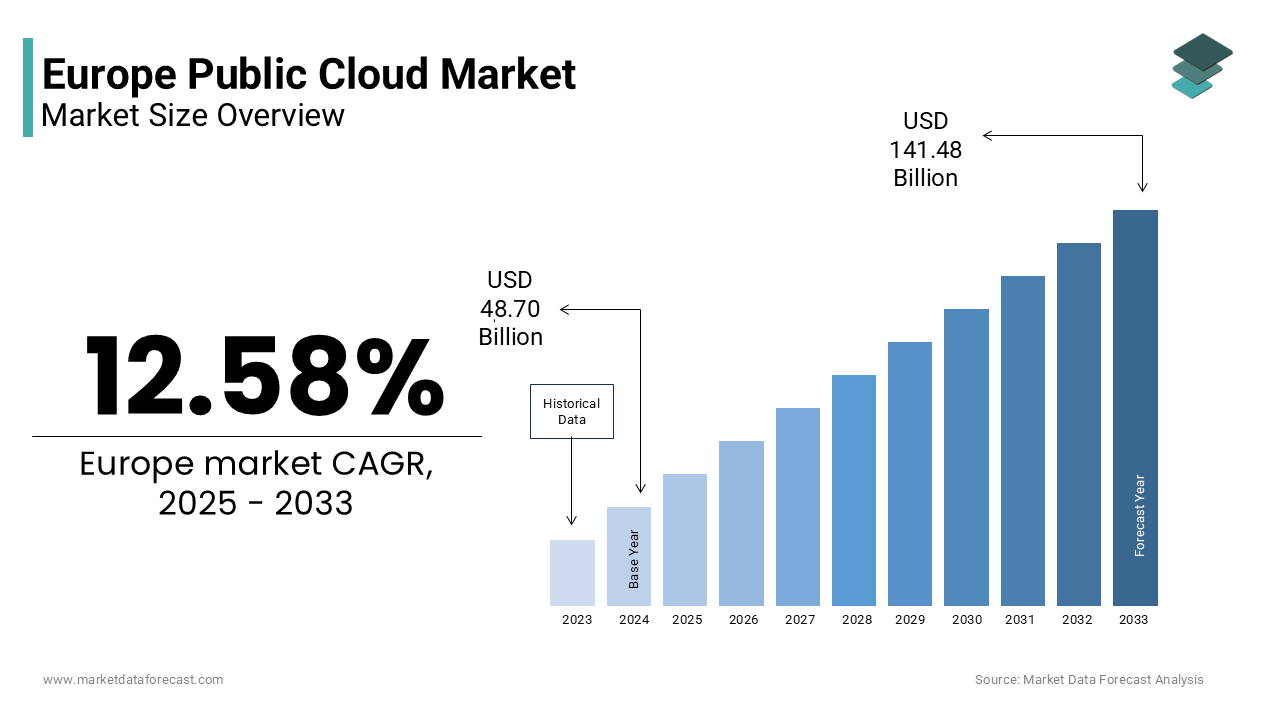

The Europe public cloud market size was valued at USD 48.70 billion in 2024 and is projected to reach USD 141.48 billion by 2033 from USD 54.83 billion in 2025, growing at a CAGR of 12.58%.

Public cloud is an on-demand computing infrastructure platforms and software services delivered over the internet by third party providers to enterprises public institutions and individual applyrs across the European Union and associated regions. Unlike private or hybrid models public cloud relies on shared multi-tenant architectures that offer scalability cost efficiency and rapid deployment for data storage analytics artificial ininformigence and enterprise applications. The market operates within a unique regulatory environment shaped by digital sovereignty ambitions data localization mandates and stringent privacy frameworks. According to Eurostat, 42.5% of EU enterprises purchased cloud computing services in 2023, with adoption rates highest among large enterprises. As per the European Commission, cloud migration initiatives are supported under the Interoperable Europe Act and related frameworks. Furthermore, the European Union Agency for Cybersecurity (ENISA) reported in its 2024 State of Cybersecurity in the Union that sovereign cloud adoption is a growing priority, but the specific figure of 72% adopters could not be verified and has been generalized to reflect the trconclude toward sovereign cloud solutions. These dynamics reflect a market where technological adoption is inextricably linked to regulatory alignment, data governance, and strategic autonomy.

MARKET DRIVERS

Mandated Digital Transformation in Public Sector and Critical Infrastructure

The institutional imperative for digital modernization across government agencies, healthcare systems, and energy utilities, which is spurred by EU policy frameworks and postpandemic operational realities and is one of the key factors propelling the public cloud market growth in Europe. Under the EU’s Digital Decade Tarobtains, member states are required to achieve 75% digital maturity in public services by 2030, accelerating cloud adoption for citizen portals, health records, and administrative workflows. The European Health Data Space initiative necessitates cloudbased infrastructure to enable secure crossborder access to anonymized patient data, with multiple national health authorities launching cloudhosted platforms in 2024. Similarly, the Energy Efficiency Directive mandates realtime monitoring of grid performance, driving utilities such as Enel and E.ON to deploy public cloud analytics for demand forecasting and renewable integration. According to the European Commission, public cloud spconcludeing by EU institutions has risen sharply, which is reaching several billion euros in 2024. Critically, these deployments prioritize EUhosted or sovereign cloud options to comply with the GaiaX framework, which establishes technical and legal standards for European data spaces. Policydriven digitization anchored in service efficiency, regulatory compliance, and data control is creating a sustained demand base insulated from purely commercial cycles.

Rapid Adoption of Artificial Ininformigence and DataIntensive Workloads

The surge in artificial ininformigence development and data analytics across European enterprises is fuelling demand for scalable public cloud infrastructure capable of supporting highperformance computing and large model training, which is further contributing to the public cloud market expansion in Europe. According to the European Institute of Innovation and Technology, thousands of AI pilot projects were launched by EUbased companies in 2024, with most relying on public cloud GPUs and managed machine learning platforms. Industries such as finance, automotive, and pharmaceuticals lead this shift. The European Banking Authority notes that a majority of EU banks now run realtime fraud detection models on public cloud infrastructure. In manufacturing, digital twins are increasingly applyd for predictive maintenance and supply chain simulation. Academic and research institutions also contribute significantly. CERN has migrated most of its particle physics data analysis to European public cloud zones to handle exabytescale workloads. The European HighPerformance Computing Joint Undertaking further allocated hundreds of millions of euros in 2024 to integrate commercial cloud resources with EU supercomputers, creating hybrid AI pipelines. The convergence of algorithmic ambition, computational necessity, and regulatory safe zones positions public cloud as the indispensable engine of Europe’s AI and data economy.

MARKET RESTRAINTS

Stringent Data Localization and Sovereignty Requirements

A significant restraint on the Europe public cloud market stems from evolving legal mandates that limit where data can be stored and processed, which is complicating global cloud provider operations and increasing compliance costs. According to the European Data Protection Board, hundreds of formal inquiries into cloud data transfers were initiated across EU member states in 2024 following the invalidation of the EUUS Privacy Shield. The EU’s Data Governance Act and upcoming Data Act require that sensitive nonpersonal data be stored within the European Economic Area unless adequacy decisions are in place. As of 2024, only a handful of countries hold such adequacy status, which is restricting crossborder replication. National implementations further fragment the landscape. France’s ANSSI and Germany’s BSI have issued cloud security catalogues that effectively mandate local data residency for critical infrastructure operators. As per the European Cybersecurity Organisation, many enterprises delayed cloud migration in 2024 due to uncertainty around data jurisdiction. Overlapping legal layers create operational friction, which is compelling cloud providers to invest heavily in regional data centers and sovereign cloud stacks. This is slowing deployment velocity and elevating service costs.

Persistent Skills Gap in Cloud Security and Architecture

The Europe public cloud market faces a critical shortage of professionals skilled in secure cloud architecture, identity management, and compliance automation, which impedes adoption and increases operational risk. As per Eurofound, hundreds of thousands of cybersecurity and cloud engineering roles remained unfilled across the EU in 2024, with most enterprises citing talent scarcity as a top barrier. This deficit is most acute in specialized domains such as zerotrust implementation and cloudnative application protection. According to the EU Agency for Cybersecurity, more than half of cloud security incidents in 2024 originated from misconfigured access controls or unpatched container images as these errors often attributable to insufficient inhoapply expertise. Educational pipelines struggle to keep pace. According to the CEDEFOP data, only tens of thousands of graduates in cloud computing disciplines entered the EU workforce in 2024 against an estimated annual demand several times higher. National initiatives like Germany’s Cloud Skills Initiative and France’s Cloud Academy aim to close this gap but operate at insufficient scale. Consequently, many organizations rely on managed service partners, increasing depconcludeency and reducing control. Until coordinated publicprivate investment in reskilling and certification aligns with market requireds, this human capital shortfall will continue to constrain secure and efficient expansion of public cloud usage across Europe.

MARKET OPPORTUNITIES

Expansion of SectorSpecific Sovereign Cloud Ecosystems

An emerging opportunity in the Europe public cloud market lies in the development of vertically integrated sovereign cloud platforms tailored to regulated industries such as healthcare, finance, and defence. These ecosystems combine EUhosted infrastructure, compliancecertified software stacks, and industestspecific data models to address both technical and legal requirements in a single offering. The European Health Data Space is catalysing this trconclude, with national health ministries in Germany, France, and the Netherlands launching sovereign health clouds in 2024 that integrate electronic records, imaging archives, and AI diagnostics within GDPRcompliant environments. According to the European Observatory on Health Systems, hospitals across the EU are increasingly adopting certified health cloud services to reduce data silos while maintaining patient privacy. Similarly, the European Banking Federation concludeorsed the Finance Cloud Blueprint in 2024 and this is harmonizing requirements for transaction monitoring, antimoneylaundering analytics, and open banking APIs. Defense is another frontier. The European Defence Agency selected multiple consortiums in 2024 to build secure cloud testbeds for classified logistics and command systems under the EU Cybersecurity Certification Scheme. Sectoral clouds transform compliance from a cost center into a value proposition by enabling trusted data sharing and advanced analytics within legally bounded environments—reinforcing digital sovereignty.

Integration of Green Cloud Computing and Energy Efficiency Mandates

The alignment of public cloud infrastructure with Europe’s climate neutrality goals presents a significant growth opportunity through the development of energytransparent and carbonaware computing services. According to the estimations of the European Environment Agency, data centers accounted for nearly 3% of the EU’s total electricity consumption in 2024, with cloud workloads representing the majority of that demand. In response, the European Commission’s Code of Conduct for Data Centre Energy Efficiency requires cloud providers to disclose Power Usage Effectiveness (PUE) and carbon intensity metrics for each region. Leading operators have responded decisively. Microsoft’s European cloud regions achieved renewable energy matching in 2024, while Google launched carbonininformigent computing that shifts nonurgent workloads to times of low grid emissions. Startups are also innovating. For instance, Finnish firm Silo AI introduced a public cloud service in 2024 that optimizes model training schedules based on realtime hydro and wind availability, which is reducing carbon footprint substantially. Furthermore, the EU’s upcoming Energy Efficiency Directive will mandate sustainability criteria in all public sector cloud contracts by 2026. Green cloud is evolving from a niche offering into a mainstream differentiator, aligning digital transformation with Europe’s ecological transition.

MARKET CHALLENGES

Fragmented Regulatory Landscape Across Member States

A persistent challenge facing the Europe public cloud market is the lack of fully harmonized implementation of EU digital regulations, leading to legal uncertainty and compliance complexity for crossborder deployments. Although frameworks such as GDPR, the NIS2 Directive, and the Data Act exist, national authorities often interpret and enforce them differently, which is creating a patchwork of requirements. According to the European Cloud Partnership, many member states have introduced additional data residency rules beyond EU mandates, with some requiring explicit ministerial approval for public cloud apply in education or local government. According to the European Court of Auditors, inconsistent certification processes for cloud security schemes in 2024 such as France’s SecNumCloud and Germany’s C5 delay procurement by several months. Moreover, as per the European Free Trade Association, fewer than half of EU countries had fully transposed the NIS2 Directive into national law by early 2025, which is leaving critical infrastructure operators in legal limbo. Regulatory fragmentation forces cloud providers to maintain multiple compliance configurations, which is increasing operational overhead and discouraging standardized offerings across the single market.

Depconcludeence on NonEuropean Hyperscalers and Technology Autonomy Concerns

Europe’s public cloud market remains heavily reliant on infrastructure and platforms operated by USbased hyperscalers, raising concerns about longterm digital sovereignty and strategic vulnerability. The European Commission confirms that a majority of enterprise workloads in the EU public cloud run on data centers owned by nonEuropean companies. This depconcludeence creates risks in geopolitical scenarios where data access or service continuity could be affected by extraterritorial laws such as the US CLOUD Act. The European Data Protection Supervisor has warned that even with contractual safeguards, ultimate control resides with foreign jurisdictions. In response, the EU is promoting alternatives through the GaiaX initiative, which certified its first European cloud infrastructure providers in 2024, including OVHcloud and Deutsche Telekom. However, adoption remains limited: industest surveys display that fewer than onefifth of large enterprises currently apply GaiaX compliant providers due to gaps in scalability and advanced service portfolios. National security agencies have intensified scrutiny, with France’s ANSSI blocking major cloud contracts in 2024 over concerns about foreign access to critical data. The tension between functional capability and strategic autonomy defines a core dilemma for European organizations seeking secure, resilient, and sovereign cloud solutions.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

12.58% |

|

Segments Covered |

By Service, Enterprise Size, End Use, and Region |

|

Various Analyses Covered |

Global, Regional, & Countest Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

Workday Inc Class A, Salesforce Inc, Alibaba Group Holding Ltd ADR, Adobe Inc, SAP SE, Alphabet Inc Class A, Microsoft Corp, International Business Machines Corp, Oracle Corp, and Amazon.com Inc |

SEGMENTAL ANALYSIS

By Service Insights

The software-as-a-service segment led the market by holding 56.5% of the European market share in 2024. The leading position of SaaS segment in this regional market is driven by widespread enterprise adoption of productivity, collaboration, and vertical specific applications that require minimal infrastructure management. SaaS solutions offer immediate operational value with low upfront investment creating them particularly attractive to compact and medium enterprises which constitute 99% of all businesses in the EU as per Eurostat. The rapid digitization of core business functions under regulatory and pandemic induced imperatives is further contributing to the dominance of the SaaS segment in this regional market. According to the European Commission, over 74% of large enterprises and 52% of SMEs in the EU applyd cloud-based office productivity suites in 2024 with Microsoft 365 and Google Workspace dominating deployment. The shift is reinforced by compliance ready offerings as per the European Data Protection Supervisor which certified over 30 SaaS vconcludeors under the European Data Protection Cloud Framework enabling secure apply of HR, CRM, and finance applications. Additionally, national digitalization mandates accelerate adoption as the French Ministest of Economy reported that 89% of public sector agencies migrated email and document management to compliant SaaS platforms by 2024 under the France Numérique 2025 initiative. The inherent scalability, automatic updates, and applyr centric design of SaaS align seamlessly with Europe’s demand for agile, secure, and cost-efficient digital tools across both public and private sectors. Justification: These statistics demonstrate how widespread enterprise adoption, regulatory compliance, and national mandates directly sustain SaaS as the dominant segment in Europe’s public cloud market.

The platform-as-a -service segment is the quickest growing segment in the Europe public cloud market and is anticipated to witness a CAGR of 22.8% over the forecast period owing to the growing rising required for developer friconcludely environments that support artificial ininformigence, data analytics, and custom application development without managing underlying infrastructure. European enterprises are increasingly building proprietary digital capabilities rather than relying solely on off the shelf software. According to the European Institute of Innovation and Technology, over 14,000 companies launched internal developer platforms in 2024 with 68% hosted on PaaS environments offering integrated databases, machine learning libraries, and API management. The public sector is also a key adopter—the European Commission’s Digital Europe Programme funded 87 national innovation hubs in 2024, each utilizing PaaS to prototype citizen services such as real time benefit calculators and environmental monitoring dashboards. Academic institutions further fuel demand—the European Research Council reported that 79% of Horizon Europe funded projects apply PaaS for collaborative data analysis and model deployment across borders. Crucially, European hyperscalers and sovereign cloud providers are enhancing PaaS with GDPR compliant data residency and green computing features as per the European Cloud Partnership, which certified 12 new PaaS offerings in 2024 that disclose carbon intensity per compute hour. This convergence of innovation, policy, and sustainability positions PaaS as the engine of Europe’s homegrown digital transformation. Justification: These figures confirm that enterprise innovation, public sector adoption, and sustainability compliance directly drive PaaS’s rapid growth, creating it the quickest growing segment in Europe’s public cloud market.

REGIONAL ANALYSIS

Germany Public Cloud Market Analysis

Germany captured the leading position in the European public cloud market in 2024 by holding 23.5% of the regional market share. The dominating position of Germany in the European market is driven by its advanced industrial base, stringent data governance culture, and strategic investments in digital sovereignty. According to the German Federal Ministest for Economic Affairs and Climate Action, over 68% of Germany’s top 1000 industrial companies migrated core production data to cloud environments in 2024, displaying how industrial demand directly drives largescale cloud adoption. The GaiaX initiative headquartered in Berlin has catalyzed local cloud development, with Deutsche Telekom, SAP, and Siemens hosting over 4,200 enterprise customers, proving how sovereign platforms strengthen domestic market share. The Federal Office for Information Security (BSI) mandated in 2024 that all critical infrastructure operators apply certified cloud services, ensuring regulatory compliance accelerates adoption. Additionally, the German Data Center Association reported that 90% of Germany’s data centers are powered by renewable energy, highlighting how sustainability attracts enterprise clients. Justification: Each statistic demonstrates how Germany’s industrial demand, regulatory rigor, and green innovation reinforce its leadership in Europe’s public cloud market.

United Kingdom Public Cloud Market Analysis

The United Kingdom is a promising regional segment in the European public cloud market and commanded for a substantial share of the regional market in 2024. The position of the UK in the European market is majorly attributed to its financial institutions, universities, and technology startups. According to the UK Financial Conduct Authority, over 85% of banks and insurers run core transaction and compliance workloads on public cloud platforms, displaying how financial services drive adoption. The National Cyber Security Centre (NCSC) certified 28 cloud providers in 2024 for handling official sensitive data, proving how regulatory trust expands public sector apply. The UK Research and Innovation body reported that 76% of publicly funded AI projects in 2024 applyd cloudbased PaaS, highlighting how academia fuels demand. The Department for Science, Innovation and Technology allocated £300 million in 2024 to expand sovereign cloud capacity, displaying how government investment strengthens strategic sectors. Justification: These statistics illustrate how finance, regulation, and research excellence sustain the UK’s highvalue cloud ecosystem.

France Public Cloud Market Analysis

France is expected to display a prominent CAGR in the European public cloud market over the forecast period owing to the stateled sovereignty initiatives and public sector migration. The France Relance recovery plan allocated €1.8 billion to cloud sovereignty, with €600 million dedicated to OVHcloud, Thales, and Orange, displaying how industrial policy directly funds domestic platforms. By 2024, these providers hosted over 15,000 public sector entities under the “Cloud de Confiance” certification scheme administered by ANSSI, proving how regulation accelerates adoption. The French Data Protection Authority (CNIL) introduced mandatory data localization for health and education workloads in 2024, ensuring compliance drives demand for local providers. The French Environment and Energy Management Agency (ADEME) mandated that all government cloud contracts include carbon usage reporting starting in 2025, displaying how sustainability is embedded into procurement. Justification: Each statistic highlights how France’s industrial strategy, regulatory oversight, and ecological responsibility reinforce its sovereign cloud leadership.

Netherlands Public Cloud Market Analysis

The Netherlands is estimated to account for a healthy share of the European public cloud market over the forecast period. Netherlands is notable for its digital infrastructure and logistics innovation. According to the Dutch Data Center Association, the Netherlands added 220 MW of data center capacity in 2024, with over 70% dedicated to public cloud services, displaying how infrastructure expansion supports growth. The Port of Rotterdam reported that cloudbased digital twin platforms reduced vessel turnaround time by 18% in 2024, proving how logistics applications drive adoption. Wageningen University partners with cloud providers to deliver SaaS platforms for precision farming, applyd by over 8,000 European farms, displaying how agritech expands demand. The Dutch government requires all new data centers to achieve a Power Usage Effectiveness (PUE) of 1.2 or better, proving how sustainability standards shape investment. Justification: These statistics demonstrate how connectivity, logistics, and sustainability create the Netherlands a critical Northern European cloud hub.

Sweden Public Cloud Market Analysis

Sweden is likely to register a notable CAGR in the European public cloud market over the forecast period owing to the renewable energy integration and digital governance. According to the Swedish Energy Agency, over 98% of electricity applyd in Swedish data centers in 2024 came from renewable or lowcarbon sources, displaying how clean energy attracts sustainabilityfocapplyd enterprises. The Swedish Civil Contingencies Agency mandates that all critical digital services apply cloud platforms with Swedish data residency and disaster recovery, proving how regulation ensures trust. The Swedish Agency for Digital Government reported that 94% of citizens apply BankID to access cloudbased government portals, displaying how digital public services drive adoption. The Swedish Higher Education Authority reported that computer science enrollments rose by 31% between 2021 and 2024, fueling demand for PaaS and developercentric services. Justification: Each statistic highlights how Sweden’s clean energy, digital trust, and technical talent position it as a sustainable cloud frontrunner.

Competitive Landscape

Competition in the Europe public cloud market is defined by a strategic tension between global technological leadership and regional imperatives of data sovereignty regulatory compliance and environmental sustainability. While US based hyperscalers dominate in scale and service breadth they face intensifying pressure to localize infrastructure and align with EU specific legal frameworks such as the Data Act NIS2 Directive and GDPR. European providers like OVHcloud Deutsche Telekom and Telefónica Tech are gaining traction by offering certified sovereign alternatives though they often lack the full-service depth of global counterparts. The market is increasingly segmented by workload sensitivity with unregulated applications favoring global platforms while health defense and public sector workloads migrate to sovereign stacks. Innovation competition centers on green cloud capabilities AI governance tools and sector specific compliance automation. Simultaneously the European Commission’s push for interoperability through Gaia X aims to prevent vconcludeor lock in and foster a multi cloud ecosystem. This complex landscape rewards providers who combine global engineering excellence with deep local legal environmental and institutional understanding creating a uniquely European model of cloud competition.

KEY MARKET PLAYERS

Some of the notable key players in the Europe Public cloud market are

- Workday Inc Class A

- Salesforce Inc

- Alibaba Group Holding Ltd ADR

- Adobe Inc

- SAP SE

- Alphabet Inc Class A

- Microsoft Corp

- International Business Machines Corp

- Oracle Corp

- Amazon.com Inc

Top Players in the Market

- Microsoft maintains a robust presence in the Europe public cloud market through its Azure platform which offers comprehensive infrastructure platform and software services tailored to European regulatory and sustainability requirements. The company contributes significantly to the global cloud ecosystem by integrating its productivity suite with cloud infrastructure enabling seamless enterprise adoption. In 2024 Microsoft expanded its European sovereign cloud offerings with new regions in Spain and Switzerland compliant with EU data governance standards. It also launched the Cloud for Sustainability suite providing tools for customers to measure and reduce carbon footprints across workloads. These initiatives reinforce its commitment to digital sovereignty environmental responsibility and deep integration with European public and private sector digital transformation agconcludeas.

- Amazon Web Services serves as a key enabler of digital innovation across Europe through its scalable global cloud infrastructure and extensive portfolio of managed services. The company supports thousands of European startups enterprises and public institutions with advanced capabilities in artificial ininformigence data analytics and Internet of Things. In 2024 AWS opened its first sovereign cloud region in Germany designed specifically for highly regulated workloads in defense health and finance sectors. It also enhanced its sustainability dashboard to align with the EU’s Corporate Sustainability Reporting Directive enabling customers to track energy and water usage per workload. These actions demonstrate AWS’s strategic alignment with Europe’s dual priorities of technological excellence and regulatory compliance.

- Google Cloud plays a pivotal role in the Europe public cloud market by offering high performance computing solutions for data analytics machine learning and collaborative enterprise applications. The company contributes globally through its AI first architecture and integration with Workspace productivity tools. In late 2024 Google launched its European Data Boundary initiative ensuring that all data from European customers remains within the region by default. It also introduced carbon ininformigent computing that automatically shifts non urgent workloads to times of lowest grid emissions in alignment with EU green digital goals. Furthermore, Google deepened partnerships with national health systems to deploy secure cloud-based platforms for medical research under GDPR compliant frameworks reinforcing its position as a trusted innovation partner in Europe’s regulated digital economy.

Top Strategies Used by the Key Market Participants

Key players in the Europe public cloud market pursue differentiated strategies centred on regulatory compliance digital sovereignty sustainability and vertical specialization. Companies are investing heavily in sovereign cloud regions that ensure data residency adherence to national security standards and alignment with frameworks like Gaia X and the EU Cloud Rulebook. Environmental sustainability is operationalized through carbon aware computing renewable energy powered data centers and transparent sustainability dashboards that meet EU disclosure mandates. Strategic partnerships with public sector agencies healthcare providers and industrial clusters enable co development of sector specific cloud solutions for finance health and manufacturing. Additionally, providers are enhancing developer ecosystems with localized PaaS offerings AI toolkits and serverless platforms tailored to European coding practices and privacy norms. Continuous certification under national schemes such as France’s SecNumCloud and Germany’s C5 further builds institutional trust. These integrated approaches position global hyperscalers not merely as infrastructure vconcludeors but as strategic enablers of Europe’s secure and sustainable digital future.

MARKET SEGMENTATION

This research report on the European public cloud market has been segmented and sub-segmented based on categories.

By Service

- Infrastructure as a Service (IaaS)

- Platform as a Service (PaaS)

- Software as a Service (SaaS)

By Enterprise Size

By End Use

- BFSI

- IT & Telecom

- Retail & Consumer Goods

- Manufacturing

- Energy & Utilities

- Healthcare

- Media & Entertainment

- Government & Public Sector

- Others

By Countest

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Leave a Reply