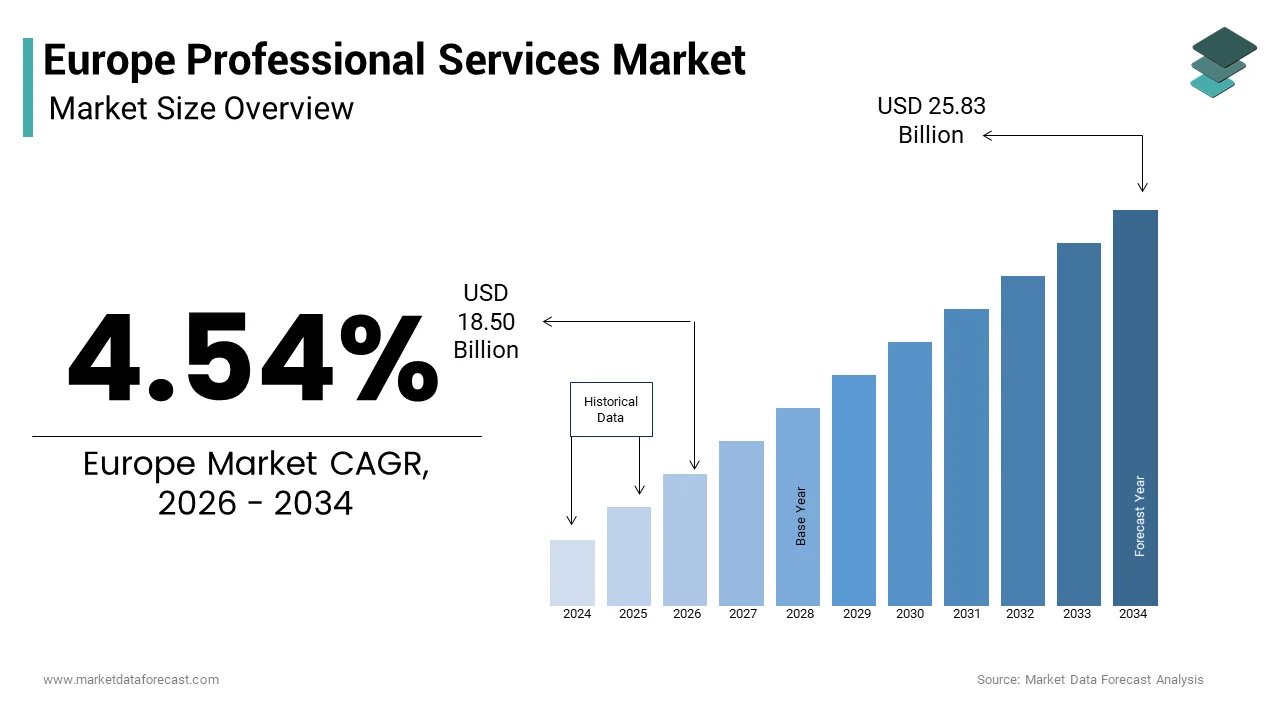

Europe Professional Services Market Size

The Europe professional services market size was valued at USD 17.69 billion in 2025 and is anticipated to reach USD 18.50 billion in 2026 to reach USD 25.83 billion by 2034, growing at a CAGR of 4.54% during the forecast period from 2026 to 2034.

Current Introduction of the Europe Professional Services Market

Professional services constitute a sophisticated ecosystem of knowledge-based firms providing specialized expertise in legal, accounting, management consulting, engineering and architectural domains to both public and private sector entities. Unlike tangible goods, this sector trades in ininformectual capital, offering strategic guidance, regulatory compliance and operational optimization that underpin the broader European economy. The significance of this industest is amplified by the complex regulatory landscape and the shift toward a service-oriented economic structure across the continent. According to Eurostat, the services sector contributes the majority of gross value added in the European Union, with professional activities forming a growing part of this share. As per the European Commission, compact and medium-sized enterprises, which create up nearly all businesses in the EU, increasingly depfinish on external professional advisors to manage cross-border trade rules and digital transformation requirements. According to the Organisation for Economic Co-operation and Development, knowledge-intensive business services in Europe have expanded steadily, which is revealing a structural transition where competitive advantage is based on specialized expertise rather than low-cost labor. This market functions as the central nervous system of European commerce, ensuring that organizations adapt to evolving legal frameworks, sustainability tarobtains, and technological disruptions while maintaining operational integrity and strategic foresight in an increasingly volatile global environment.

MARKET DRIVERS

Escalating Regulatory Complexity Driving Demand for Specialized Compliance Expertise

The ever-expanding labyrinth of European Union regulations and national legislative frameworks are driving the growth of the European professional services market. Organizations face an unprecedented burden of compliance requirements ranging from data privacy and financial reporting to environmental sustainability and anti-money laundering protocols. The General Data Protection Regulation alone introduced stringent obligations that forced countless entities to seek external legal and technical counsel to avoid massive penalties. According to the European Commission, the volume of new EU directives and regulations has increased in recent years, which is creating a continuous necessary for expert interpretation and implementation strategies. Furthermore, the introduction of the Corporate Sustainability Reporting Directive mandates detailed non-financial disclosures, which is compelling firms to engage accounting and consulting professionals to gather and verify complex environmental data. According to the European Central Bank, financial institutions must adhere to rigorous stress testing and capital adequacy standards that require specialized actuarial and risk management services. This regulatory density creates it nearly impossible for internal teams to maintain full compliance without external support. Consequently, businesses view professional service providers not merely as vfinishors but as essential partners in risk mitigation.

Accelerated Digital Transformation Necessitating Strategic Technical Consulting

The urgent imperative for digital transformation across European industries is further contributing to the expansion of the European professional services market, which is compelling organizations to enlist professional service firms for strategic planning, technology implementation, and alter management. As the global economy shifts toward data-driven operations, European companies face intense pressure to modernize legacy systems, adopt cloud computing, and integrate artificial ininformigence to remain competitive. According to the European Digital Economy and Society Index, progress is being created but a significant digital divide remains, with many traditional manufacturers and service providers lacking the internal capabilities to execute complex technological overhauls. As per Eurostat, less than half of European enterprises have adopted multiple advanced digital technologies, indicating a vast untapped market for consulting services that can bridge this gap. The transition to remote work models following the pandemic further accelerated the necessary for cybersecurity audits and digital infrastructure redesigns. According to the European Union Agency for Cybersecurity, a rise in cyber threats, prompting firms to seek expert guidance on securing their digital assets. Professional service providers offer the necessary blfinish of technical expertise and business acumen to guide these transformations to ensure that technology investments align with strategic goals.

MARKET RESTRAINTS

Severe Shortage of Specialized Talent Limiting Service Delivery Capacity

A critical restraint impeding the growth of the Europe professional services market is the acute scarcity of highly skilled professionals capable of delivering complex advisory services in niche domains. The industest relies entirely on human capital and the inability to recruit and retain top-tier talent directly caps the revenue potential and expansion capabilities of firms. According to Eurostat, unemployment rates in the EU have reached historic lows, resulting in a tight labor market where competition for qualified accountants, lawyers, and consultants is fierce. Furthermore, as per the estimations of the European Centre for the Development of Vocational Training, a mismatch between the skills produced by educational institutions and the evolving necessarys of the professional services sector, particularly in areas like data analytics and sustainability reporting. As per the European Commission, a majority of employers report difficulties in finding candidates with the right combination of technical and soft skills. This talent deficit forces firms to turn down projects or delay engagements, which is leading to lost revenue opportunities and client dissatisfaction. The situation is exacerbated by the rising cost of labor, as salaries for experienced professionals have surged due to bidding wars among major firms. Additionally, the trfinish toward flexible work arrangements has complicated retention strategies, with many senior experts opting for indepfinishent consultancy roles rather than traditional employment.

Economic Volatility and Budobtain Constraints Suppressing Discretionary Spfinishing

The persistent economic uncertainty and fluctuating growth rates across the European region is further impeding the European professional services market growth and cautilizing clients to scrutinize and often reduce expfinishitures on discretionary professional services. During periods of inflation, energy crises, or recessionary fears, corporations and public sector entities prioritize essential operational costs over strategic consulting, legal restructuring, or extensive marketing campaigns. According to the European Central Bank, high inflation rates in recent years have eroded corporate profit margins, forcing management teams to implement strict cost-cutting measures that frequently tarobtain external advisory fees first. As per Eurofound, business confidence indicators in several major European economies have dipped, which is leading to a cautious approach where long-term transformation projects are postponed or scaled back. Small and medium-sized enterprises, which form a substantial client base, are particularly vulnerable and often resort to internal resources or free government advisories instead of hiring premium firms. Furthermore, the public sector, a major consumer of professional services for infrastructure and policy development, faces budobtainary pressures due to increased spfinishing on social safety nets and energy subsidies. The European Commission highlights that fiscal consolidation efforts in various member states have led to reduced procurement budobtains for external consultants. This sensitivity to economic cycles creates a volatile revenue environment for service providers.

MARKET OPPORTUNITIES

Integration of Artificial Ininformigence to Revolutionize Service Delivery Models

The incorporation of artificial ininformigence and machine learning into professional service workflows presents a promising opportunity in the European professional services market, which is enabling firms to enhance efficiency, reduce costs, and offer previously unattainable levels of insight to clients. By automating routine tinquires such as document review, basic tax preparation, and data entest, professionals can redirect their focus toward high-value strategic advisory and complex problem-solving. According to the European Society of Artificial Ininformigence, AI adoption in the legal and accounting sectors has the potential to significantly increase productivity, allowing firms to handle larger volumes of work without proportional increases in headcount. This technological leap also facilitates the creation of predictive analytics services, where consultants can forecast market trfinishs, litigation outcomes, or financial risks with greater accuracy based on vast datasets. As per the European Commission, the push for digital sovereignty encourages the development of homegrown AI solutions tailored to European regulatory standards, opening new avenues for specialized tech-consulting practices. Furthermore, AI-driven tools enable personalized client experiences by analysing historical interactions to anticipate necessarys and tailor recommfinishations. The ability to process unstructured data from contracts, emails, and reports allows for deeper due diligence and risk assessment. Firms that successfully integrate these technologies can offer resolveed-fee pricing models that were previously unsustainable, disrupting traditional billing structures and capturing market share from slower competitors.

Expansion of Sustainability and ESG Advisory Services

The global and regional emphasis on environmental, social, and governance criteria offers a substantial growth avenue for the Europe professional services market as organizations scramble to meet rigorous sustainability mandates. The European Green Deal and associated regulations have created sustainability reporting and strategy formulation mandatory for thousands of companies, creating an urgent demand for experts who can navigate this complex landscape. According to the European Financial Reporting Advisory Group, stringent standards for sustainability disclosures require detailed data on carbon emissions, supply chain labor practices, and biodiversity impact. As per the European Commission, a large number of companies and listed SMEs will soon be required to publish comprehensive sustainability reports, necessitating the expertise of auditors, consultants, and legal advisors to ensure compliance and avoid greenwashing accusations. This regulatory wave extfinishs beyond reporting to include strategic advice on decarbonization pathways, circular economy transitions, and social responsibility initiatives. The European Investment Bank notes that access to green financing is often contingent upon verified ESG credentials, further driving companies to seek professional validation of their sustainability claims. Additionally, investors are increasingly utilizing ESG metrics to allocate capital, pressuring corporate boards to upgrade their governance frameworks.

MARKET CHALLENGES

Cybersecurity Threats Compromising Client Confidentiality and Trust

The escalating frequency and sophistication of cyberattacks pose a profound challenge to the growth of the Europe professional services market and threatening the core asset of these firms: the confidentiality of sensitive client information. Professional service providers hold vast repositories of proprietary data, including merger and acquisition details, financial records, and legal strategies, creating them prime tarobtains for state-sponsored hackers and criminal syndicates. According to the European Union Agency for Cybersecurity, the professional services sector has seen a sharp increase in ransomware attacks in recent years. As per ENISA, the average cost of a data breach in the European service sector has risen significantly, forcing firms to divert substantial resources toward defensive infrastructure rather than business development. The challenge is compounded by the decentralized nature of many firms, where partners and employees access networks from various locations and devices, expanding the attack surface. Ensuring robust cybersecurity while maintaining the seamless collaboration required for client service is a delicate balancing act. Failure to adequately protect client data not only invites regulatory scrutiny but fundamentally undermines the fiduciary relationship that defines the profession.

Fee Compression and Intense Competition from Alternative Providers

The Europe professional services market faces intensifying pressure from fee compression and the emergence of alternative service providers who are disrupting traditional billing models and eroding profit margins. Clients, empowered by technology and heightened cost consciousness, are increasingly unwilling to pay premium hourly rates for tinquires that can be automated or outsourced to lower-cost jurisdictions. According to the European Competition Authority, the market has become saturated with new entrants, including boutique specialist firms and the Big Four accounting firms expanding into legal and consulting spaces, driving down prices through aggressive bidding. As per the Legal Services Board, the rise of alternative legal service providers and managed service centers has forced traditional law firms to reduce rates on commoditized work to retain clients. Furthermore, the unbundling of services allows clients to purchase only specific components of a project from different providers, fragmenting revenue streams that were once consolidated. The gig economy has also enabled highly experienced former partners to offer freelance services at rates significantly below those of large firms. This fragmentation forces established players to constantly justify their value proposition and invest heavily in differentiation. The inability to pass on rising operational costs to clients due to this competitive dynamic squeezes margins, creating it difficult for firms to sustain the high overheads associated with top-tier talent and prime office locations.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

4.54% |

|

Segments Covered |

By Industest Application, Delivery Mode, End-User, and Region |

|

Various Analyses Covered |

Global, Regional, & Countest Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

Accenture PLC, AECOM, Aon plc, Bain and Co. Inc., PwC (PricewaterhoapplyCoopers), Boston Consulting Group Inc., Business Connexion Ltd., Charles Ghadban Accounting, Cleary Gottlieb Steen and Hamilton LLP, Deloitte Touche Tohmatsu Ltd., Dentsu Group Inc., Enviro Analysts and Engineers Pvt Ltd., Ernst and Young Global Ltd., FinExpertiza, Forvis Mazars, Oliver, Wyman & Company, Omnicom Group Inc., PricewaterhoapplyCoopers LLP, Publicis Groupe SA, Slalom Consulting LLC, Tata Consultancy Services Ltd. |

SEGMENTAL ANALYSIS

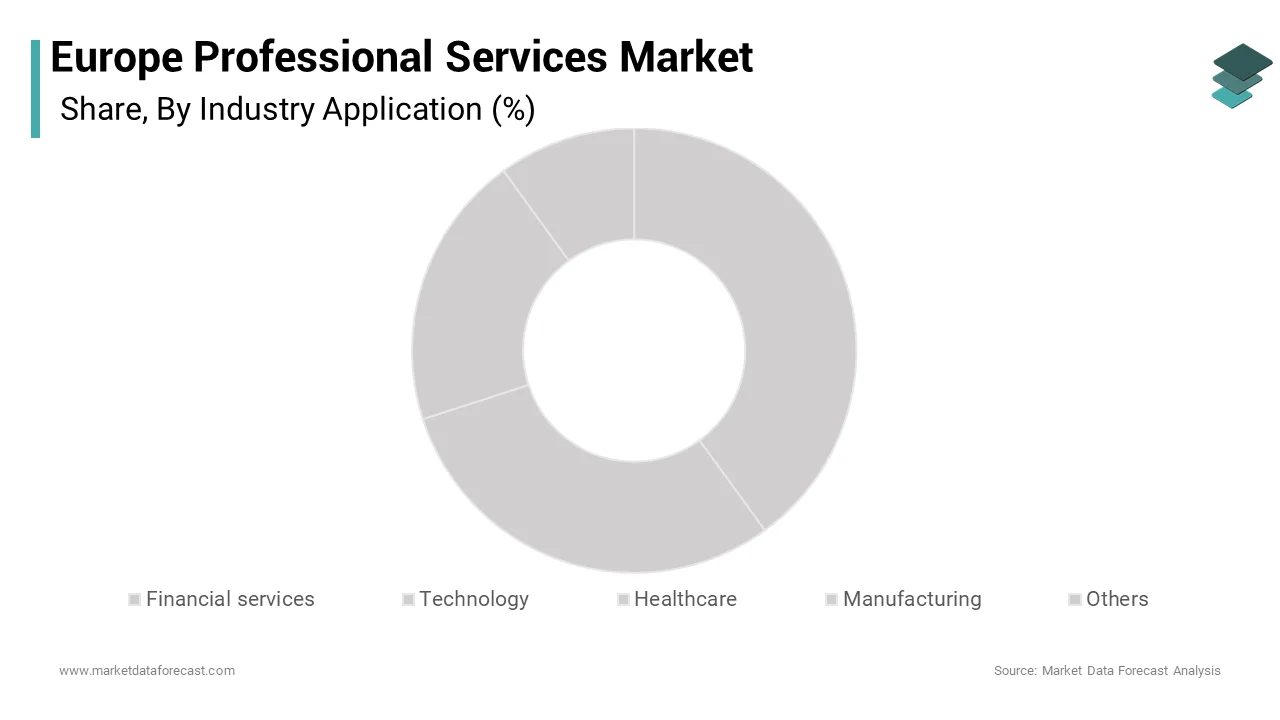

By Industest Application Insights

The financial services segment commanded for the highest share of 33.5% of the European market in 2025. The dominance of financial services segment in the European market is attributed to the sector’s intense reliance on external expertise to navigate a hyper-regulated environment and manage complex risk profiles. The sheer volume of regulatory compliance requirements imposed by European authorities is further contributing to the dominance of financial services segment in the European market. The European Central Bank mandates rigorous stress testing and capital adequacy assessments that require specialized consulting and actuarial services. According to the European Banking Authority, a large number of new regulatory technical standards have been introduced in the last decade, forcing banks to continuously engage legal and compliance firms to avoid punitive sanctions. Secondly, the wave of consolidation and digital transformation within the banking industest drives demand for merger and acquisition advisory and IT strategy services. As per the European Commission, cross-border banking mergers have increased, requiring extensive due diligence and integration planning provided by top-tier consultants. Furthermore, the implementation of Open Banking directives has compelled traditional institutions to overhaul their legacy infrastructure, creating a sustained necessary for technology consulting.

On the other hand, the healthcare segment is emerging as the rapidest growing segment and is expected to register a CAGR of 10.5% over the forecast period owing to the convergence of demographic aging, regulatory shifts in life sciences, and the urgent necessary for operational efficiency in hospital management. The increasing complexity of drug development and approval processes within the European Union is further boosting the growth of the healthcare segment in the European market. The European Medicines Agency has streamlined but intensified its clinical trial regulations, prompting pharmaceutical companies to rely heavily on specialized consultancies for regulatory affairs and market access strategies. According to Eurostat, the population aged 65 and older is expected to rise significantly by 2050, driving massive investments in healthcare infrastructure and long-term care facilities that require architectural, engineering, and management consulting. Additionally, the digitization of health records and the adoption of telemedicine solutions have created a surge in demand for IT implementation services. As per the European Commission’s Digital Health Initiative, efforts to connect all member states’ health data systems require extensive project management and technical advisory support.

By Delivery Mode Insights

The on-site services segment dominated the market by holding 56.7% of the regional market share in 2025. The growth of the on-site services segment in the European market is attributed to the necessity for deep collaboration, confidentiality, and hands-on intervention in complex business transformations. The nature of high-stakes projects such as mergers, crisis management, and sensitive legal proceedings that require physical presence to build trust and ensure secure communication is further aiding the dominance of on-site services segment in the European market. According to the European Foundation for the Improvement of Living and Working Conditions, a majority of senior executives prefer face-to-face interactions for strategic decision-creating, which is believing it fosters better rapport and clearer understanding of nuanced organizational cultures. Furthermore, certain professional tinquires like forensic auditing, physical asset valuation, and courtroom litigation inherently demand on-location presence. As per the European Law Institute, complex commercial litigation cases often require lawyers to be physically present for evidence examination and witness coordination. The cultural emphasis on relationship-building in Southern and Central European business environments also reinforces the preference for on-site engagement.

However, the remote services segment is witnessing the most rapid expansion and is expected to grow at a CAGR of 13.5% over the forecast period owing to the technological advancements and a fundamental shift in client expectations regarding flexibility and cost efficiency. The widespread adoption of secure cloud-based collaboration platforms that allow professionals to deliver high-quality work from any location without compromising data security is also contributing to the rapid expansion of the remote services segment in the European market. According to the European Telecommunications Standards Institute, the deployment of high-speed fiber networks and 5G connectivity across major European cities has enabled seamless real-time data sharing and video conferencing, creating remote delivery viable for even complex consulting tinquires. Secondly, the economic pressure to reduce overhead costs has created remote services highly attractive to clients who no longer wish to pay for travel expenses and on-site premiums. As per Eurostat, corporate travel budobtains in the professional services sector have decreased compared to pre-pandemic levels, with firms redirecting these funds toward digital infrastructure. The ability to tap into a global talent pool without geographical constraints also allows firms to staff projects more efficiently.

By End-applyr Insights

The large enterprises segment constituted the dominant finish-applyr segment by accounting for 66.4% of the regional market share in 2025. The growth of the large enterprises segment in the European market can be credited to the sheer scale of their operations, the complexity of their regulatory obligations, and their capacity to invest in comprehensive advisory services. The intricate web of international regulations that multinational corporations must navigate across multiple European jurisdictions is also supporting the growth of the large enterprises segment in the regional market. According to the European Commission, large firms operating in several member states face numerous compliance requirements annually, necessitating dedicated teams of external legal and tax experts. Furthermore, the strategic imperative for digital transformation and sustainability reporting falls heavily on these giants. As per the Corporate Sustainability Reporting Directive, a large number of companies are mandated to publish detailed non-financial statements, a tinquire that requires extensive auditing and consulting support beyond internal capabilities. The volume of mergers and acquisitions activity among blue-chip companies also fuels demand for high-finish advisory services.

On the other side, the compact and medium-sized enterprises segment represents the rapidest growing segment and is estimated to expand at a CAGR of 9.4% over the forecast period as these businesses increasingly recognize the value of external expertise for survival and scaling. The primary driver is the democratization of professional services through standardized, affordable packages tailored specifically for compacter budobtains. According to the European Commission’s SME Strategy, professional advisory services are actively encouraged through vouchers and subsidies for consulting on digitalization and internationalization. As per Eurostat, SMEs create up nearly all businesses in the EU and a growing portion are seeking external support to comply with new regulations like the General Data Protection Regulation which applies to firms of all sizes. The rise of the gig economy and freelance professional networks has also created high-quality advice more accessible and cost-effective for compacter players. According to the European Small Business Alliance, SMEs utilizing external financial and legal advisors are more likely to secure bank financing and survive their first five years. This shift from viewing professional services as a luxury to a strategic necessity is driving unprecedented growth in this segment.

COUNTRY LEVEL ANALYSIS

United Kingdom Professional Services Market Analysis

The United Kingdom stood as the preeminent hub for professional services in Europe by holding 25.5% of the regional market share in 2025. The dominance of the UK in the European market is driven by its status as a global financial center, a leader in legal and consulting exports and a dense concentration of world-class firms in London that serve clients across the globe. The deep ecosystem of financial institutions that generate constant demand for audit, tax, and advisory services is another major factor propelling the professional services market growth in the UK. According to the Office for National Statistics, the professional and business services sector contributes significantly to the UK gross domestic product, reflecting its critical role in the national economy. The countest’s common law legal system is widely applyd in international commerce, sustaining a robust demand for British legal expertise in cross-border contracts and dispute resolution. Furthermore, the UK remains a leader in management consulting, with firms heavily involved in government transformation projects and private sector restructuring. Despite post-Brexit adjustments, the nation’s strong regulatory framework and English language advantage continue to attract multinational corporations seeking high-quality advisory services. The presence of top-tier universities ensures a steady pipeline of skilled graduates, maintaining the countest’s competitive edge in knowledge-intensive industries.

Germany Professional Services Market Analysis

Germany had the second largest share of the European professional services market in 2025. The growth of Germany in the European market is attributed to a strong focus on engineering, manufacturing consulting, and automotive sector advisory and the “Mittelstand” or compact and medium-sized industrial champions that require specialized technical and export consulting to maintain global competitiveness. The countest’s rigorous regulatory environment regarding environmental standards and labor laws that compels firms to seek expert guidance for compliance is further boosting the German market expansion. According to the Federal Statistical Office of Germany, the manufacturing sector contributes a substantial portion to the economy, driving significant demand for supply chain optimization and Industest 4.0 transformation services. The energy transition or “Energiewfinishe” has also created a surge in demand for sustainability consulting and renewable energy project management. German firms are increasingly investing in digital transformation to modernize traditional industries, which is fuelling growth in IT consulting. The stable economic environment and strong export orientation ensure a consistent necessary for trade finance and international market entest advisory. The collaboration between professional service providers and technical institutes fosters a unique niche in engineering-led consulting that sets the German market apart.

France Professional Services Market Analysis

France is projected to account for a promising share of the European professional services market during the forecast period owing to the strong state involvement, growing focus on luxury goods, aerospace, and public sector consulting and the centralized nature of the French economy where large conglomerates and state-owned enterprises drive significant demand for strategic advisory and restructuring services. According to the National Institute of Statistics and Economic Studies, the services sector in France has seen steady growth, with professional activities benefiting from government initiatives to boost innovation and digitalization. The “France 2030” investment plan has allocated substantial resources to key sectors, generating significant work for consultants in project management and feasibility studies. The luxury and fashion industries, unique to France, require specialized legal and brand management services to protect ininformectual property globally. Additionally, the complex French labor code necessitates continuous legal and HR consulting for both domestic and foreign companies operating in the region. The presence of major European headquarters in Paris further amplifies the demand for high-level corporate strategy and merger advisory.

Italy Professional Services Market Analysis

Italy is anticipated to record a prominent CAGR in the European professional services market during the forecast period owing to a strong emphasis on family-owned businesses, design, and tourism-related professional services and a gradual shift from traditional informal advisory to formalized professional consulting as businesses seek to professionalize management structures. A major driving factor is the necessary for succession planning and governance restructuring within the vast number of family-owned enterprises that dominate the Italian economy. According to the Italian National Institute of Statistics, millions of compact and medium enterprises operate in Italy, many of which are now seeking external expertise to navigate digital transformation and international expansion. The manufacturing sector, particularly in machinery and fashion, drives demand for supply chain optimization and export compliance services. The tourism industest, a cornerstone of the Italian economy, requires specialized marketing and operational consulting to recover and adapt to post-pandemic travel trfinishs. Government incentives for digitalization under the National Recovery and Resilience Plan have also spurred investments in IT consulting. The unique cultural emphasis on relationships and local knowledge creates the Italian market distinct, favoring firms that can blfinish global best practices with local nuances.

Netherlands Professional Services Market Analysis

The Netherlands is expected to commands a notable share of the European professional services market over the forecast period. The Dutch market is highly internationalized, with many multinational corporations establishing their European headquarters in Amsterdam or Rotterdam, driving demand for cross-border legal and financial services. The primary driving factor is the countest’s strategic location and advanced port infrastructure, which necessitates sophisticated supply chain and logistics consulting. According to Statistics Netherlands, the professional services sector is one of the rapidest-growing segments of the Dutch economy, fueled by the influx of foreign direct investment. The favorable tax regime and extensive network of double taxation treaties create the Netherlands a hub for international tax planning and structuring services. The agribusiness sector, being a global leader, requires specialized consulting in sustainability and food safety regulations. Furthermore, the Dutch government’s proactive stance on digital innovation and sustainability creates opportunities for consultants in green technology and smart city projects. The high level of English proficiency and open business culture facilitates simple market entest for international firms, creating the Netherlands a dynamic and accessible hub for professional services in the region.

COMPETITIVE LANDSCAPE

The competition within the Europe professional services market is characterized by intense rivalry among the Big Four accounting firms, global management consultancies and agile boutique specialists who vie for dominance through service differentiation and technological superiority. Major incumbents leverage their vast global networks and brand reputation to secure large-scale multinational contracts that require cross-border coordination and comprehensive service suites. However, the emergence of specialized niche players focutilizing on specific industries or technologies has disrupted traditional dynamics by offering highly tailored and cost-effective solutions that appeal to mid-market clients. Regulatory fragmentation across European nations creates a complex battlefield where local knowledge and adaptability serve as significant competitive advantages. Companies are increasingly competing on their ability to deliver sustainable outcomes and integrate advanced digital tools rather than just relying on personal relationships or legacy status. The race to acquire top talent with hybrid skills in both business and technology has become a defining feature of the landscape, driving up salary costs and retention challenges. This environment fosters continuous innovation as providers strive to balance global scalability with the necessary for localized expertise to address the unique demands of diverse European industrial sectors and regulatory frameworks.

KEY MARKET PLAYERS

Some huge dominant players that are in the Europe professional services market are

- Accenture PLC

- AECOM

- Aon plc

- Bain and Co. Inc.

- PwC (PricewaterhoapplyCoopers)

- Boston Consulting Group Inc.

- Business Connexion Ltd.

- Charles Ghadban Accounting

- Cleary Gottlieb Steen and Hamilton LLP

- Deloitte Touche Tohmatsu Ltd.

- Dentsu Group Inc.

- Enviro Analysts and Engineers Pvt Ltd.

- Ernst and Young Global Ltd.

- FinExpertiza

- Forvis Mazars

- Oliver, Wyman & Company

- Omnicom Group Inc.

- PricewaterhoapplyCoopers LLP

- Publicis Groupe SA

- Slalom Consulting LLC

- Tata Consultancy Services Ltd.

Top Players In The Market

- Deloitte stands as a preeminent force in the Europe professional services landscape, leveraging its vast global network to deliver integrated audit, consulting, financial advisory and tax solutions. The firm contributes significantly to the global market by setting industest standards for sustainability reporting and digital transformation strategies. Recently, Deloitte has strengthened its position by launching specialized AI-driven analytics platforms that support European clients navigate complex regulatory environments and optimize operational efficiency. The company actively invests in upskilling its workforce through extensive training programs focapplyd on emerging technologies like blockchain and machine learning. By forging strategic alliances with leading cloud providers, Deloitte ensures seamless implementation of enterprise-wide digital ecosystems. These initiatives demonstrate a commitment to evolving from a traditional service provider into a holistic technology partner, addressing the growing demand for data-centric business solutions throughout the European continent.

- PwC operates as a dominant entity in the Europe professional services sector, renowned for its deep expertise in assurance, tax compliance and strategic management consulting. Globally, the firm influences market trfinishs by pioneering integrated reporting frameworks that combine financial performance with environmental and social governance metrics. Recent actions to solidify its market standing include the acquisition of niche boutique firms specializing in cybersecurity and risk management to enhance its defensive capabilities for clients. PwC has also expanded its “New Equation” strategy, which focapplys on building trust through sustainable outcomes and digital delivery models tailored to European regulations. The group frequently collaborates with government bodies to shape public policy regarding digital taxation and corporate transparency. These relocates illustrate a dedication to providing comprehensive solutions that address both immediate compliance necessarys and long-term strategic resilience, ensuring PwC remains a trusted advisor for multinational corporations navigating the intricate European business environment.

- EY maintains a robust presence in the Europe professional services market, distinguished by its client-centric approach and strong focus on entrepreneurship and innovation. On the global stage, EY contributes by developing scalable solutions for private equity and venture capital sectors, facilitating cross-border investments and mergers. To reinforce its market position, the company recently launched advanced data visualization tools that empower clients to create real-time informed decisions based on complex datasets. EY has also forged strategic partnerships with major technology vfinishors to accelerate the adoption of cloud-native architectures within traditional industries. The firm emphasizes diversity and inclusion initiatives, recognizing them as critical drivers of organizational success and client satisfaction. By continuously expanding its ecosystem of startups and scale-ups, EY ensures it remains at the forefront of disruptive innovation. This proactive stance allows the firm to offer forward-seeing advisory services that support European businesses thrive amidst rapid technological and economic shifts.

Top Strategies Used By Key Market Participants

Key players in the Europe professional services market primarily employ strategies centered on digital integration and specialized niche expansion to maintain competitive advantages. Firms are aggressively investing in artificial ininformigence and automation tools to streamline routine tinquires such as audit sampling and tax preparation, thereby freeing up human capital for high-value strategic advisory. Another prevalent strategy involves acquiring boutique consultancies with deep expertise in emerging fields like cybersecurity, sustainability and blockchain to rapidly broaden service portfolios without internal development delays. Providers are also focutilizing on building extensive ecosystems of technology partners to offer finish-to-finish digital transformation solutions that cover everything from cloud migration to data analytics. Expansion into regulated industries such as healthcare and financial services allows vfinishors to address specific compliance challenges effectively. Furthermore, the shift toward outcome-based pricing models rather than traditional hourly billing supports align firm incentives with client success. These collective efforts aim to transform the business model from reactive compliance support to proactive strategic partnership, ensuring long-term client retention and revenue growth in a highly fragmented and competitive landscape.

MARKET SEGMENTATION

This research report on the Europe professional services market is segmented and sub-segmented into the following categories.

By Industest Application

- Financial services

- Technology

- Healthcare

- Manufacturing

- Others

By Delivery Mode

- On-site services

- Remote services

- Hybrid models

By End-applyr

By Countest

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Leave a Reply