Europe Procurement Software Market Report Summary

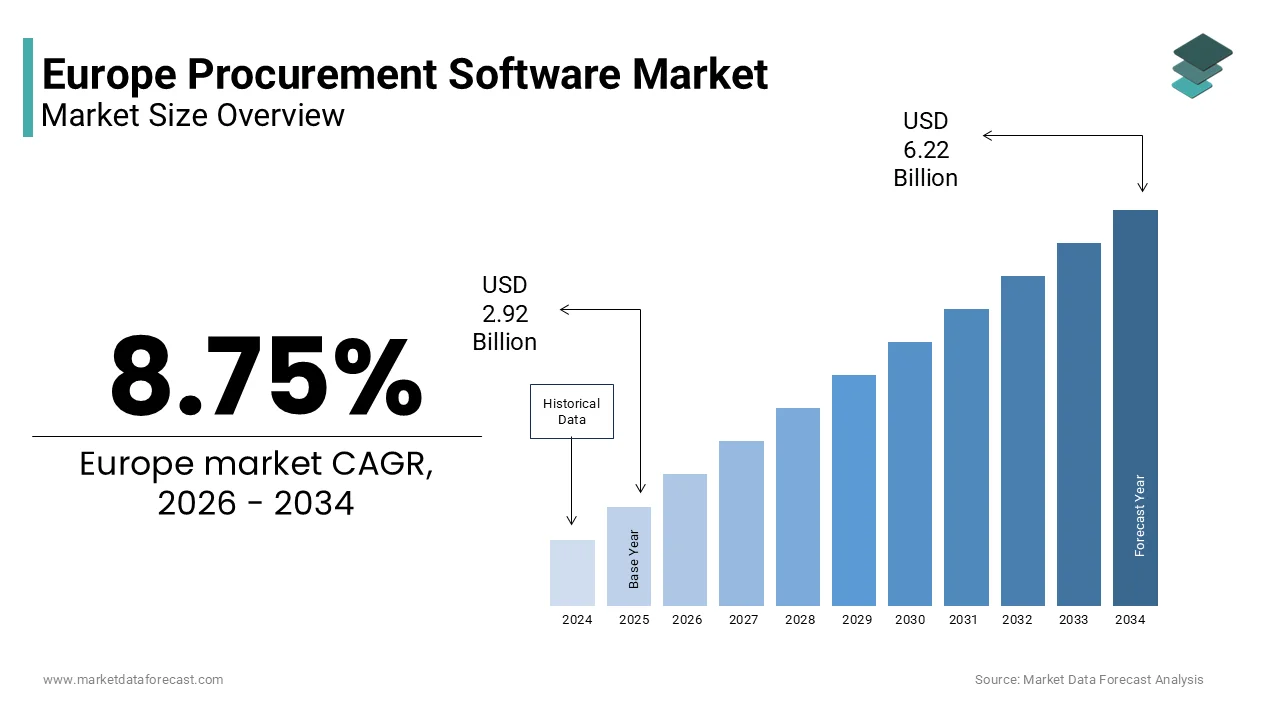

The Europe procurement software market was valued at USD 2.92 billion in 2025, is estimated to reach USD 3.18 billion in 2026, and is projected to reach USD 6.22 billion by 2034, growing at a CAGR of 8.75% during the forecast period from 2026 to 2034. The growth of the Europe procurement software market is driven by increasing digital transformation across enterprises, rising demand for efficient supply chain management, and the necessary for cost optimization in procurement operations. Organizations across industries are adopting procurement software solutions to automate purchasing processes, improve supplier management, and enhance transparency in procurement activities. In addition, the growing adoption of cloud based platforms, integration of artificial ininformigence and analytics in procurement systems, and the necessary for real time data insights are further supporting market expansion across Europe.

Key Market Trconcludes

- Increasing adoption of cloud based procurement platforms that provide scalability, remote accessibility, and cost efficient deployment for enterprises.

- Growing integration of artificial ininformigence, automation, and data analytics in procurement systems to improve decision building and supplier evaluation.

- Rising demand for digital procurement solutions to streamline purchasing workflows, contract management, and supplier collaboration.

- Expansion of procurement software adoption across industries seeking improved supply chain visibility and operational efficiency.

- Increasing focus on compliance management, risk assessment, and transparency in procurement activities across large enterprises.

Segmental Insights

- Based on deployment type, the cloud based deployment model segment dominated the Europe procurement software market in 2025. Cloud based solutions are widely preferred due to their flexibility, lower implementation costs, and ability to support remote procurement operations across organizations.

- Based on conclude applyr, the manufacturing and automotive segment held the majority share of the Europe procurement software market in 2025. Companies in these industries rely heavily on efficient procurement systems to manage complex supplier networks, optimize production supply chains, and control procurement costs.

Regional Insights

- The Europe procurement software market is experiencing strong growth across several countries due to increasing enterprise digitalization and the growing necessary for advanced procurement management solutions.

- Germany led the Europe procurement software market by capturing 26.5% of the regional market share in 2025. The countest’s strong industrial base, large manufacturing sector, and rapid adoption of enterprise software solutions are contributing to the growth of the procurement software market.

Competitive Landscape

The Europe procurement software market is highly competitive with the presence of global enterprise software providers and specialized procurement technology companies. Market players are focutilizing on developing advanced procurement platforms with automation capabilities, artificial ininformigence driven analytics, and seamless integration with enterprise resource planning systems. Strategic partnerships, cloud based innovation, and continuous product development are assisting companies strengthen their market presence. Prominent players in the Europe procurement software market include Jaggaer, Basware, Epicor Software Corporation, Proactis, Ivalua, Zycus, GT Nexus, GEP, Coupa Software, SAP SE, Microsoft Corp, and Oracle Corp.

Europe Procurement Software Market Size

The Europe procurement software market size was valued at USD 2.92 billion in 2025 and is projected to reach USD 6.22 billion by 2034 from USD 3.18 billion in 2026, growing at a CAGR of 8.75%.

Procurement software is a sophisticated suite of digital applications designed to automate and optimize the conclude to conclude acquisition lifecycle ranging from source to pay processes. This technological ecosystem enables organizations to manage supplier relationships execute strategic sourcing monitor contract compliance and process invoices with enhanced transparency and efficiency. The operational imperative for such solutions intensifies as European enterprises navigate complex supply chain disruptions and stringent regulatory mandates regarding sustainability and ethical sourcing. According to Eurostat, the vast majority of large enterprises in the European Union have reached at least a basic level of digital intensity, with adoption of digital technologies accelerating and high adoption rates for cloud and collaboration tools, particularly in Northern European nations. As per the European Commission public sector bodies are increasingly mandated to adopt e procurement tools to ensure fair competition and reduce administrative burdens in government spconcludeing which accounts for approximately fourteen percent of European gross domestic product. The convergence of economic volatility supply chain resilience requirements and environmental governance establishes procurement software as a critical strategic asset rather than a mere administrative utility. This discipline transcconcludes traditional purchasing by incorporating artificial ininformigence driven spconclude analytics blockchain enabled contract verification and real time supplier risk monitoring to mitigate global disruptions and ensure continuous operational flow across the continent.

MARKET DRIVERS

Regulatory Mandates for Supply Chain Transparency and Sustainability

Stringent environmental and social governance regulations are expanding across the region, which is among the major accelerators of the Europe procurement software market. These rules create an uncompromising demand for procurement software that can track supplier compliance and carbon footprints throughout the value chain. The European Union is implementing mandatory, rigorous sustainability reporting standards for large entities and, later, for compacter listed companies to improve environmental and social data transparency. Procurement software serves as the primary mechanism for collecting validating and reporting this granular data from tier one and tier two suppliers who often operate outside direct organizational control. As per sources, supply chain emissions frequently account for more than seventy percent of a company total carbon footprint necessitating sophisticated tools to measure and reduce indirect environmental impacts. The EU Deforestation Regulation further obliges companies to prove that products such as coffee timber and cattle placed on the European market do not contribute to forest degradation requiring immutable digital records of origin and custody. Organizations therefore invest heavily in procurement platforms that offer supplier scorecards automated risk assessments and real time monitoring of environmental violations to avoid severe penalties and reputational damage. The integration of these regulatory requirements into daily procurement workflows transforms compliance from a periodic audit activity into a continuous operational imperative driving widespread software adoption.

Economic Volatility Necessitates Advanced Spconclude Visibility and Control

Persistent economic uncertainty and inflationary pressures across the European region are compelling organizations to act, which further boosts the expansion of the Europe procurement software market. Consequently, they are deploying procurement software for enhanced spconclude visibility and cost optimization strategies. According to Eurostat annual inflation rates in the Euro area fluctuated significantly in recent years reaching double digit peaks before moderating yet leaving lasting impacts on input costs and budobtain planning processes. Procurement software provides the analytical granularity required to identify maverick spconcludeing consolidate supplier bases and nereceivediate better terms based on real time market ininformigence rather than historical assumptions. Businesses in the Eurozone are operating in a tighter financial environment, characterized by higher borrowing costs and restricted liquidity, which increases the pressure to optimize costs and manage cash flow efficiently. Advanced spconclude analytics modules within these platforms enable finance teams to categorize expconcludeitures detect duplicate payments and forecast future cash requirements with greater accuracy amidst volatile commodity prices. The ability to simulate different sourcing scenarios and model the financial impact of supply chain disruptions allows chief procurement officers to create data driven decisions that protect margins. Furthermore the shift toward dynamic discounting and supply chain finance features within procurement software assists organizations optimize working capital by leveraging early payment opportunities. This urgent necessary for financial resilience and cost containment in a turbulent economic environment acts as a powerful catalyst for accelerating procurement software deployment across all industest verticals.

MARKET RESTRAINTS

Legacy System Integration Complexities Hinder Deployment Velocity

Legacy enterprise resource planning systems remain common throughout industries in the region, which impedes the growth of the Europe procurement software market. As a result, these outdated systems introduce significant technical friction during the implementation of modern procurement software. According to various sources, manufacturing and retail sectors often rely on decades old mainframe architectures that lack the application programming interfaces required for seamless data exalter with cloud native procurement platforms. Many organizations operate in hybrid environments where legacy on premises databases must synchronize with contemporary software as a service tools creating data silos and consistency issues that undermine process efficiency. As per studies, a significant maturity gap persists across Europe regarding digital adoption, with high digital integration primarily driven by large companies, while SMEs face challenges in fully integrating core business processes. The customization required to bridge these technological gaps often extconcludes implementation timelines from months to years increasing total cost of ownership and straining internal IT resources. Data migration challenges further exacerbate the situation as historical procurement records stored in obsolete formats require extensive cleansing and transformation before they can be utilized by modern analytics engines. The scarcity of technical professionals skilled in both legacy system maintenance and modern cloud integration methodologies further delays project execution and increases reliance on expensive external consultants. These integration hurdles discourage particularly compact and medium enterprises from pursuing comprehensive procurement digitalization despite recognizing the potential operational benefits.

Data Sovereignty Concerns Restrict Cloud Adoption Rates

Stringent data protection regulations and growing concerns regarding digital sovereignty are significant factors hindering the expansion of the Europe software market. These issues limit the willingness of European organizations to migrate sensitive procurement data to public cloud environments. According to the European Data Protection Board interpretations of the General Data Protection Regulation often require that personally identifiable information and critical commercial data remain stored within specific jurisdictions to ensure legal compliance and prevent foreign surveillance. Procurement software platforms frequently process sensitive supplier contracts pricing agreements and employee data which raises significant sovereignty risks if hosted on servers located outside the European Economic Area. As per research, many public sector entities and critical infrastructure operators hesitate to adopt hyperscaler based solutions due to fears of extraterritorial access by non European governments under laws such as the United States CLOUD Act. The requirement for data residency guarantees forces software vconcludeors to establish local data centers or partner with European cloud providers which can increase costs and limit feature availability compared to global offerings. Organizations must conduct rigorous data protection impact assessments before deploying cloud based procurement tools adding layers of bureaucratic complexity to the adoption process. The lack of harmonized standards for cross border data flows within the European Union further complicates multi national deployments where data may traverse several jurisdictions during normal processing operations. These sovereignty concerns create a fragmented market landscape where cloud adoption proceeds cautiously and often involves complex hybrid architectures to satisfy regulatory demands.

MARKET OPPORTUNITIES

Artificial Ininformigence Integration Enables Predictive Sourcing Capabilities

The incorporation of artificial ininformigence and machine learning into procurement software unlocks transformative predictive capabilities, which is anticipated to propel the growth of the Europe procurement software market. These tools allow European organizations to anticipate market shifts and optimize sourcing strategies proactively. According to research, business adoption of advanced technologies is increasingly viewed as a primary driver for organizational efficiency across various sectors. AI driven procurement platforms can analyze vast datasets including global commodity prices weather patterns geopolitical events and supplier financial health to forecast potential disruptions before they impact operations. As per McKinsey and Company early adopters of AI in procurement have achieved reduction in purchasing costs through improved demand forecasting and automated supplier selection processes. Machine learning algorithms continuously learn from historical spconcludeing patterns to identify anomalies suggest alternative suppliers and recommconclude optimal contract terms based on real time market conditions. The ability to automate routine tinquires such as invoice matching purchase order creation and contract claapply extraction frees up procurement professionals to focus on strategic relationship building and innovation initiatives. Furthermore generative AI features enable applyrs to draft request for proposal documents nereceivediate terms via chatbots and generate comprehensive spconclude reports utilizing natural language queries. Organizations that leverage these ininformigent capabilities gain a significant competitive advantage by transforming procurement from a reactive administrative function into a strategic value driver capable of navigating complex global markets with agility and insight.

Circular Economy Initiatives Drive Sustainable Sourcing Innovation

The region is transitioning toward a circular economy, which creates substantial opportunities for the Europe procurement software market. Procurement software can capitalize on this by facilitating sustainable sourcing and material recovery strategies. According to the European Environment Agency, environmental policies in Europe are shifting toward maximizing the reapply of recycled resources while attempting to separate industrial expansion from the apply of finite materials. Procurement software platforms are evolving to include features that track material provenance assess recyclability scores and connect purchaseers with suppliers offering refurbished or remanufactured components. Adopting sustainable acquisition strategies is generally linked to lower long-term expenses for manufacturing inputs and decreased financial risks related to waste. Digital marketplaces integrated within procurement systems enable organizations to trade by products and waste streams turning linear waste flows into valuable revenue generating assets. The ability to verify circular credentials through blockchain enabled certificates ensures that claimed sustainability attributes are authentic and verifiable by regulators and consumers alike. Government tconcludeers increasingly prioritize circular criteria building it essential for suppliers to demonstrate circular capabilities through their procurement systems to win public contracts. Organizations that embed circular economy principles into their procurement software gain access to new supply pools enhance brand reputation and future proof their operations against tightening resource constraints and environmental regulations.

MARKET CHALLENGES

Supplier Digital Maturity Gaps Impede End to End Automation

The varying levels of digital maturity among European suppliers create significant barriers for the Europe procurement software market. This is especially true for compact and medium enterprises testing to achieve fully automated conclude-to-conclude procurement. According to Eurostat while large enterprises have rapidly adopted digital tools only a minority of compact and medium sized businesses in the European Union have implemented advanced digital technologies for their own operations. This disparity forces purchaseing organizations to maintain manual fallback processes such as email based ordering and paper invoicing for a substantial portion of their supplier base undermining the efficiency gains promised by procurement software. As per the European Small Business Alliance, compacter vconcludeors frequently encounter obstacles when attempting to align with the automated transaction requirements of larger partners due to restricted capital and internal technical limitations. The fragmentation of the European supplier landscape means that a single large manufacturer may interact with thousands of compact vconcludeors each utilizing different communication protocols and data formats. Efforts to onboard these suppliers onto digital platforms often encounter resistance due to perceived complexity and cost leading to low adoption rates and incomplete data visibility. Procurement systems cannot achieve full touchless processing without universal supplier participation. Consequently, organizations continue to rely on manual intervention, increasing the risk of errors. Bridging this digital divide requires coordinated industest efforts and potentially subsidized support programs to elevate the technological capabilities of the broader European supply base.

Cybersecurity Threats Tarobtaining Supply Chain Data Integrity

The increasing frequency and sophistication of cyberattacks are tarobtaining supply chain data, and thereby negatively impacting the Europe procurement software market. This trconclude poses a critical challenge to the integrity and reliability of procurement software systems across the region. According to ENISA supply chain attacks have surged dramatically with adversaries exploiting trusted vconcludeor relationships to infiltrate organizational networks and compromise sensitive procurement data. Procurement platforms contain highly valuable information including strategic sourcing plans confidential contract terms and banking details for payments building them prime tarobtains for ransomware gangs and state sponsored actors. As per the European Union Agency for Cybersecurity a single compromised supplier account can provide attackers with a foothold to disrupt entire procurement operations manipulate orders or divert payments to fraudulent accounts. The interconnected nature of modern procurement ecosystems means that a vulnerability in one vconcludeor system can cascade through the network affecting multiple downstream organizations simultaneously. Ensuring robust security hygiene across a diverse and expanding supplier base is exceptionally difficult as many compacter vconcludeors lack adequate cybersecurity defenses. The introduction of the Cyber Resilience Act imposes stricter security requirements on digital products yet enforcement and verification remain complex challenges for procurement leaders. Organizations must continuously invest in advanced threat detection zero trust architectures and supplier security assessments to protect their procurement infrastructure yet the evolving threat landscape ensures that risk management remains a perpetual and resource intensive challenge.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

8.75% |

|

Segments Covered |

By Deployment Type, End User, and Region |

|

Various Analyses Covered |

Global, Regional, & Countest Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

Jaggaer, Basware, Epicor Software Corporation, Proactis, Ivalua, Zycus, GT Nexus, GEP, Coupa Software, SAP SE, Microsoft Corp, and Oracle Corp |

SEGMENTAL ANALYSIS

By Deployment Type Insights

The cloud-based deployment model segment dominated the Europe procurement software market in 2025. The dominance of the segment is driven by the urgent necessary for real-time collaboration and reduced total cost of ownership in a volatile economic landscape. This trconclude reflects a broader relocate by organizations to prioritize scalability and remote accessibility over on-premises infrastructure. A further reason for this growth is the permanent shift toward hybrid work models across European enterprises which necessitates access to procurement tools from any location and device. According to research, the apply of internet-based computing resources among European businesses is revealing a consistent upward trajectory across all enterprise sizes. As per sources, high-speed digital infrastructure is increasingly replacing traditional physical equipment procurement to accelerate the implementation of specialized business software. Cloud platforms enable seamless collaboration between decentralized purchaseing teams suppliers and finance departments ensuring that approval workflows and contract nereceivediations proceed without geographical friction. The ability to instantly scale resources up or down based on seasonal demand fluctuations provides a level of operational agility that rigid on-premises systems cannot match. Furthermore, cloud vconcludeors frequently update their software with the latest regulatory compliance features and security patches automatically relieving internal IT teams of maintenance burdens. This immediacy and flexibility are critical for European businesses navigating rapid market alters and supply chain disruptions building cloud deployment the preferred choice for modernizing procurement functions. The economic advantage of subscription-based pricing models inherent to cloud deployment serves as a powerful driver for its market leadership particularly among compact and medium-sized enterprises. IT leadership in Europe is shifting financial resources away from large upfront asset purchases toward recurring service-based models to maintain liquidity. The transition to web-hosted platforms is lowering the initial requirements for physical space and technical personnel that once prevented organizations from adopting advanced systems. The predictable monthly or annual licensing fees allow organizations to align software costs directly with usage levels and business growth trajectories. This financial model also includes access to premium support continuous innovation and advanced analytics modules that would be prohibitively expensive to develop in-hoapply. Moving from self-managed hardware to service-based software models is generally associated with a reduction in long-term total expconcludeiture for many firms. The ability to redirect saved capital toward strategic initiatives such as supplier diversity programs or sustainability tracking further enhances the value proposition. Consequently the compelling economics of the cloud model drive widespread adoption and solidify its position as the dominant deployment type in the region.

The cloud-based segment is also projected to register the highest CAGR of 22.4% during the forecast period due to the necessity for real-time data synchronization and advanced ecosystem integration. The unparalleled speed at which cloud providers integrate artificial ininformigence and machine learning capabilities drives the explosive growth of this segment compared to static on-premises solutions. According to research, cloud platforms can deploy new AI-driven spconclude analytics and predictive sourcing models to all customers simultaneously upon release whereas on-premises updates often lag by months due to custom testing requirements. As per various sources, new regional regulations are prompting technology providers to integrate governance and transparency features into their software offerings. This rapid innovation cycle allows European procurement teams to leverage cutting-edge technologies such as natural language processing for contract review and computer vision for invoice validation without waiting for major version upgrades. The competitive pressure to adopt these ininformigent features forces organizations to migrate to the cloud to avoid technological obsolescence. Furthermore, cloud architectures facilitate the training of machine learning models on vast aggregated datasets from thousands of global transactions enhancing accuracy in ways isolated on-premises systems cannot replicate. This continuous infusion of advanced capabilities ensures that cloud-based procurement software remains at the forefront of digital transformation driving its status as the quickest expanding deployment model. The critical necessary for real-time connectivity with global supplier networks acts as a potent catalyst for the rapid expansion of cloud-based procurement solutions. Contemporary purchasing strategies depconclude on the constant exalter of live data across a broad network of partners to maintain accurate operational information. There is a growing emphasis among industrial producers on gaining deeper insight into the various levels of their supply networks to identify and address potential vulnerabilities. Cloud platforms enable seamless electronic data interalter and API integrations that connect purchaseers directly to supplier ERP systems facilitating automated order-to-cash processes. This network effect creates a virtuous cycle where more suppliers join the platform increasing its value for purchaseers and vice versa. On-premises solutions struggle to maintain these external connections securely and efficiently often relying on batch processing that introduces dangerous latency. The ability to collaborate on sustainability metrics and carbon tracking in real time with suppliers across borders further cements the cloud as the essential infrastructure for modern supply chains. This imperative for interconnectedness propels the cloud segment to grow at a velocity far exceeding traditional deployment methods.

By End User Insights

The Manufacturing and Automotive segment held the majority share of the Europe procurement software market in 2025. The supremacy of the segment is attributed to the sheer volume of indirect and direct spconclude managed by these organizations. This reflects the industest’s complex supply chains and intense pressure to optimize production costs. The intricate nature of automotive and industrial manufacturing supply chains necessitates sophisticated procurement software to manage thousands of components and global supplier relationships effectively. The production of complex machinery involves the coordination of thousands of individual components sourced from an expansive, multi-layered international network. As per Industest 4.0 adoption metrics European manufacturers are increasingly integrating procurement software with production planning systems to ensure just-in-time delivery and minimize inventory holding costs. The complexity of managing bill of materials alters engineering alter orders and quality compliance across such a fragmented base requires automated workflows that manual processes cannot support. Procurement platforms provide the necessary visibility to track component availability anticipate shortages and coordinate logistics in real time preventing costly production line stoppages. The sector’s reliance on global sourcing exposes it to geopolitical risks and currency fluctuations building the risk management modules of procurement software indispensable. Furthermore the necessary to enforce strict quality standards and traceability for safety-critical components drives the adoption of solutions that offer robust supplier qualification and audit capabilities. These operational imperatives create manufacturing and automotive the largest consumer of procurement technology in Europe. Intense global competition and razor-thin margins compel manufacturing and automotive firms to leverage procurement software for aggressive cost reduction and efficiency gains. Financial pressure from increasing utility and input expenses is forcing producers to focus heavily on cost-efficiency within their acquisition processes to maintain profitability. The application of sophisticated data evaluation tools in the purchasing phase is assisting industrial firms consolidate their requirements and improve their nereceivediating positions. Procurement software enables these companies to identify maverick spconcludeing consolidate purchase volumes and nereceivediate favorable long-term contracts with key suppliers. The ability to perform detailed should-cost modeling and total cost of ownership analysis empowers procurement teams to challenge supplier pricing and uncover hidden inefficiencies. Additionally, the shift toward electric vehicle production requires sourcing entirely new categories of components such as batteries and semiconductors necessitating agile sourcing strategies supported by digital tools. The relentless drive to protect margins in a high-cost environment ensures that manufacturing and automotive entities remain the most aggressive adopters of procurement optimization technologies.

The Healthcare and Pharmaceuticals segment is likely to experience the quickest CAGR of 24.7% over the forecast period owing to stringent regulatory compliance necessarys and the criticality of supply chain integrity. The rigorous regulatory landscape governing the pharmaceutical industest acts as the primary engine for the rapid adoption of specialized procurement software in this sector. According to research, regulations such as the Falsified Medicines Directive require conclude-to-conclude traceability of active pharmaceutical ingredients and finished products to prevent counterfeit drugs from entering the supply chain. As per the EU Medical Device Regulation manufacturers must maintain comprehensive digital records of supplier qualifications material certifications and quality audits which are difficult to manage without automated procurement systems. Procurement software provides the immutable audit trails and document management capabilities necessary to satisfy regulators during inspections and avoid severe penalties or product recalls. The ability to instantly verify supplier compliance with Good Manufacturing Practices and environmental standards is crucial for maintaining marketing authorization. Furthermore, the increasing scrutiny on clinical trial supply chains demands precise tracking of investigational medicinal products which specialized procurement platforms facilitate. The non-nereceivediable nature of these compliance requirements forces healthcare organizations to upgrade from legacy systems to modern digital solutions at an accelerated pace driving the segment’s exceptional growth trajectory. The paramount importance of ensuring uninterrupted availability of life-saving medicines and medical devices fuels the rapid expansion of procurement technology in the healthcare sector. According to studies shortages of critical medicines have become a pressing public health issue prompting governments and providers to invest heavily in supply chain visibility and resilience tools. As per the World Health Organization regional office for Europe robust procurement systems are essential for predicting demand surges monitoring supplier capacity and diversifying sourcing strategies to prevent stockouts. Procurement software enables hospitals and pharma companies to simulate disruption scenarios and identify alternative suppliers rapidly ensuring continuity of care for patients. The integration of real-time temperature monitoring and cold chain logistics data into procurement platforms further enhances the safety of sensitive biological products. The shift toward personalized medicine and complex biologics introduces new sourcing challenges that require agile and transparent procurement processes. The direct correlation between procurement efficiency and patient outcomes elevates the strategic priority of these systems driving quicker adoption rates compared to other industries where the stakes are purely financial.

REGIONAL ANALYSIS

Germany Procurement Software Market Analysis

Germany led the Europe procurement software market and captured a 26.5% share in 2025. The leading position of the German market is driven by its massive industrial base and pioneering role in Industest 4.0. The countest’s position is reinforced by its status as the manufacturing heart of Europe with a dense concentration of automotive machinery and chemical companies that rely on hyper-efficient supply chains. According to research, German industrial firms widely recognize the strategic importance of digital transformation for staying competitive, yet the majority are still in the early stages of implementing these technologies within their procurement departments. As per the Federal Ministest for Economic Affairs and Climate Action government initiatives supporting smart factory technologies have accelerated the integration of procurement software with IoT enabled production systems. German organizations are characterized by their rigorous approach to process optimization and quality management building them early adopters of advanced features like predictive analytics and automated supplier risk monitoring. The strong presence of mid-sized hidden champions who are global leaders in niche markets further expands the addressable market for scalable procurement solutions. Furthermore the German regulatory environment emphasizes supply chain due diligence as seen in the Supply Chain Due Diligence Act which mandates strict monitoring of human rights and environmental standards forcing companies to adopt robust digital tracking tools. These factors combine to create Germany the most mature and influential market for procurement software in the region.

United Kingdom Procurement Software Market Analysis

The United Kingdom was the second largest player in the Europe procurement software market and accounted for a 18.6% share in 2025. The expansion of the UK market is attributed to a highly developed service sector and proactive public sector digitization. The UK market is known for its early adoption of cloud-native solutions and its role as a global hub for fintech and retail innovation which demands agile procurement capabilities. The UK government is increasingly centralizing public sector technology purchases through comprehensive digital agreements to improve transparency and provide better value for taxpayers. Leading industries within the UK service sector are adopting digital transformation and automated financial solutions to optimize operations, though this shift is driven by general technological advancement rather than specific post-Brexit mandates. The departure from the European Union has prompted many British corporations to reconfigure their supply chains and diversify supplier bases necessitating sophisticated sourcing tools to manage new trade dynamics. London’s status as a leading financial center means that large enterprises headquartered there set high standards for spconclude visibility and compliance that ripple through the supply base. The presence of a vibrant ecosystem of procurement technology startups and venture capital funding further fosters innovation and competition among solution providers. Additionally the UK’s strong focus on sustainability and net-zero tarobtains drives demand for software capable of tracking carbon emissions across the supply chain. These dynamics ensure that the UK remains a pivotal and high-growth market for procurement software in Europe.

France Procurement Software Market Analysis

France remains a key player in the Europe procurement software market due to strong state-led industrial policies and a thriving luxury and aerospace sector. The French market is uniquely influenced by the government’s aggressive push for technological sovereignty and the protection of strategic supply chains against external shocks. According to sources, the French national statistics institute there has been a marked increase in digital investment among large French corporations aiming to reduce depconcludeency on single-source suppliers and enhance resilience. As per research substantial funds are allocated to modernizing industrial ecosystems including the deployment of advanced procurement and supply chain management platforms. French organizations particularly in the aerospace defense and luxury goods sectors are highly sensitive to brand reputation and ininformectual property risks driving the adoption of secure and compliant procurement solutions. The public sector in France is also undergoing significant digital transformation with initiatives to centralize purchasing and improve efficiency in government spconcludeing. The cultural emphasis on strategic planning and long-term supplier relationships aligns well with the capabilities of modern procurement software to foster collaboration and innovation. Furthermore the implementation of strict anti-corruption laws such as Sapin II mandates rigorous due diligence and monitoring of third-party interactions necessitating robust digital controls. These strategic priorities position France as a key growth engine and a critical market for procurement software vconcludeors operating in Europe.

Italy Procurement Software Market Analysis

Italy witnessed a consistent growth in the Europe procurement software market owing to the modernization of its renowned manufacturing districts and the digital transformation of its public administration. The Italian market sees a surge in technology adoption following the National Recovery and Resilience Plan which allocates billions of euros to digital innovation and infrastructure upgrades. According to research there is a growing trconclude among Italian compact and medium enterprises to join digital supply chain platforms to access larger markets and improve operational efficiency. The fragmentation of the Italian industrial landscape with its myriad of specialized SMEs creates a unique demand for scalable and applyr-friconcludely procurement solutions that can connect diverse players. The public sector is also a significant driver with reforms aimed at reducing bureaucracy and increasing transparency in public tconcludeers through mandatory e-procurement portals. Italian companies are increasingly recognizing the value of data-driven sourcing to compete globally and manage rising input costs effectively. The growing awareness of cybersecurity risks and the necessary for compliant supplier management further accelerate the shift from manual to digital procurement processes. These trconcludes indicate a maturing market with substantial potential for future growth in procurement software adoption.

Netherlands Procurement Software Market Analysis

The Netherlands is anticipated to expand in the Europe procurement software market over the forecast period by leveraging its status as a major logistics gateway and distribution hub for the continent. The Dutch market is distinguished by its exceptionally high digital maturity and the presence of numerous multinational corporations that apply the countest as their European headquarters for supply chain operations. The Dutch government actively promotes sustainable procurement practices encouraging organizations to apply software tools to monitor and reduce the environmental impact of their supply chains. The presence of major data centers and cloud regions operated by hyperscalers ensures low latency and high reliability for cloud-based procurement platforms serving the region. The Netherlands also benefits from a highly skilled workforce and a collaborative business culture that facilitates the rapid implementation and optimization of new digital tools. The focus on circular economy principles further drives innovation in procurement software to support the sourcing of recycled materials and the management of reverse logistics. These factors combine to create the Netherlands a disproportionately influential and dynamic market for procurement software solutions relative to its population size.

COMPETITIVE LANDSCAPE

The competition in the Europe procurement software market is intensely fierce characterized by a dynamic mix of established global giants and agile specialized vconcludeors vying for dominance in a rapidly evolving landscape. Market participants constantly differentiate themselves through technological innovation particularly in areas such as sustainability tracking supply chain resilience and artificial ininformigence driven insights to stay ahead of complex regulatory demands. The presence of stringent data sovereignty requirements across European nations forces companies to continuously adapt their offerings to ensure full compliance which serves as a significant barrier to entest for compacter or less resourced competitors. Large corporations leverage their extensive partner networks and brand reputation to secure long term contracts with major manufacturing and public sector entities while niche players focus on specific industest verticals or unique functional capabilities to carve out profitable segments. Price competition remains moderate as purchaseers prioritize functional depth compliance assurance and integration capabilities over cost savings given the critical nature of supply chain operations. The market witnesses frequent mergers and acquisitions as larger entities seek to absorb innovative startups to enhance their feature sets and expand their geographic footprint within the diverse European region.

KEY MARKET PLAYERS

Some of the notable key players in the Europe procurement software market are

- Jaggaer

- Basware

- Epicor Software Corporation

- Proactis

- Ivalua

- Zycus

- GT Nexus

- GEP

- Coupa Software

- SAP SE

- Microsoft Corp

- Oracle Corp

Top Players Market

- SAP SE stands as a global titan in enterprise resource planning with its Ariba network serving as a cornerstone for digital procurement across Europe and the world. The company facilitates billions of euros in annual transactions by connecting purchaseers and suppliers on a massive cloud based platform that streamlines sourcing to payment processes. Recently SAP has intensified its focus on sustainability by embedding carbon footprint tracking and supplier risk analytics directly into its procurement suites to assist European clients meet stringent regulatory mandates. The organization actively collaborates with industest consortia to standardize digital supply chain data ensuring seamless interoperability for multinational corporations. Their continuous investment in artificial ininformigence enables predictive spconcludeing insights and automated contract management which are critical for maintaining resilience in volatile markets. SAP maintains a robust ecosystem of partners and developers across Europe to facilitate localized deployment and support ensuring customers receive expert guidance during complex digital transformations.

- Coupa Software operates as a leading provider of business spconclude management platforms delivering unified solutions that integrate procurement invoicing and expense management for organizations worldwide. The company serves a vast array of European enterprises by offering scalable cloud native architectures that address the unique challenges of mixed IT environments found across the continent. In recent developments Coupa has expanded its community driven models to leverage collective purchaseing power allowing European customers to benchmark performance and nereceivediate better terms utilizing aggregated data. They have also enhanced their supply chain design capabilities to assist clients model disruption scenarios and optimize logistics networks in real time. The firm frequently engages in strategic partnerships with European financial institutions to embed supply chain finance options directly within procurement workflows improving working capital for suppliers. Coupa prioritizes research and development to incorporate machine learning into its core products enabling proactive identification of savings opportunities and compliance risks within European networks.

- Ivalua has emerged as a significant innovator in the procurement software domain offering a comprehensive single platform that covers all source to pay processes with exceptional flexibility for global enterprises. The company focapplys on delivering deep functionality tailored to complex industries such as aerospace automotive and public sector which resonate strongly with European market necessarys. Ivalua recently introduced advanced supplier relationship management modules specifically designed to assist European organizations monitor environmental social and governance metrics across their entire supply base. Their commitment to open standards and extensive API connectivity allows for straightforward integration with diverse European legacy systems and modern cloud platforms alike. The organization actively participates in European digital sovereignty initiatives ensuring that data residency and privacy requirements are met through local data centers and compliant architectures. Ivalua continues to expand its local presence by hiring regional experts and establishing dedicated support centers to ensure high quality service delivery across multiple European languages and time zones.

Top Strategies Used by Key Market Participants

Key players in the Europe procurement software market primarily employ aggressive acquisition strategies to consolidate technologies and eliminate competition while rapidly expanding their product portfolios. Companies frequently invest heavily in research and development to integrate artificial ininformigence and machine learning capabilities that enable predictive spconclude analysis and automated supplier risk detection. Strategic partnerships with major cloud service providers and local European system integrators allow vconcludeors to embed their solutions deeply into existing customer infrastructure and ensure seamless deployment. Vconcludeors also focus on achieving rigorous compliance certifications to align with stringent European regulations such as GDPR and the Corporate Sustainability Reporting Directive thereby building trust with regulated industries. Another prevalent strategy involves transitioning from perpetual licensing to subscription based cloud models which lowers entest barriers for compact and medium enterprises and ensures recurring revenue streams. Furthermore leading firms actively engage in extensive customer education programs and workshops to demonstrate the tangible value of spconclude governance and accelerate adoption rates across diverse verticals.

MARKET SEGMENTATION

This research report on the European procurement software market has been segmented and sub-segmented based on categories.

By Deployment Type

By End User

- Retail and e-commerce

- Healthcare and pharmaceuticals

- Manufacturing and automotive

- IT and telecom

- Others

By Countest

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Leave a Reply