Europe Polysilicon Market Size

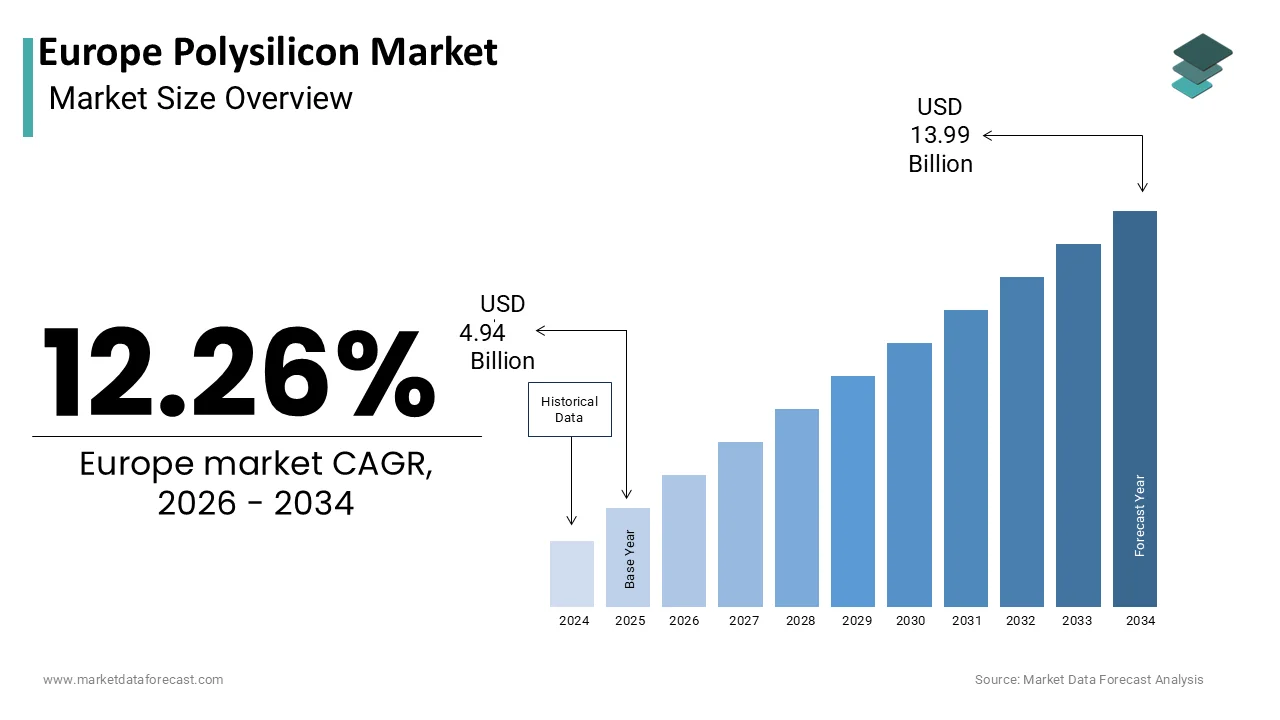

The Europe polysilicon market was valued at USD 4.94 billion in 2025, is estimated to reach USD 5.55 billion in 2026, and is projected to reach USD 13.99 billion by 2034, growing at a CAGR of 12.26% from 2026 to 2034.

Polysilicon represents a critical yet nascent segment within the broader semiconductor and renewable energy supply chains, characterized by high-purity silicon material essential for photovoltaic cells and electronic wafers. Polysilicon serves as the foundational raw material for converting sunlight into electricity and enabling advanced computing capabilities. The European Union currently faces a significant strategic deficit in domestic polysilicon production, relying heavily on imports from Asia and North America to meet its industrial requireds. As per Eurostat, the European Union imported approximately 81% of its silicon requirements in recent years, which indicates a profound depconcludeency on external suppliers. This reliance has triggered urgent policy responses under the European Chips Act and the Net Zero Industest Act, which aim to reshore critical manufacturing capacities. According to the International Energy Agency, Europe must significantly expand its clean tech manufacturing base to meet its 2030 climate tarreceives, including a substantial increase in solar photovoltaic deployment to reach 600 GW of total installed capacity. The region is witnessing a resurgence of interest in local production facilities driven by geopolitical tensions and supply chain vulnerabilities exposed during recent global disruptions. The energy-intensive nature of polysilicon production poses unique challenges in Europe, where electricity costs are higher than in competing regions. However, the availability of renewable energy sources offers a potential competitive advantage for producing low-carbon polysilicon. The market is thus at a pivotal juncture where regulatory support, technological innovation,n and investment decisions will determine the future trajectory of domestic supply capabilities.

MARKET DRIVERS

Aggressive Expansion of Solar Photovoltaic Deployment Tarreceives

The aggressive expansion of solar photovoltaic deployment tarreceives across the European Union acts is one of the major factors propelling the growth of the European polysilicon market due to the direct correlation between solar panel installations and raw material demand. The REPowerEU plan aims to accelerate the rollout of renewable energy to reduce depconcludeence on fossil fuels and enhance energy security. As per the European Commission, the EU intconcludes to install 600 gigawatts of solar photovoltaic capacity by 2030, which represents a massive increase from current levels. This ambitious tarreceive requires a substantial supply of polysilicon to manufacture the required solar modules. According to SolarPower Europe, the continent added 65.5 gigawatts of new solar capacity in 2024, demonstrating the rapid pace of adoption. Each gigawatt of solar capacity requires approximately 2,500 to 3,000 tons of polysilicon, depconcludeing on the technology applyd. The shift towards higher efficiency monocrystalline panels further increases the quality and quantity of polysilicon requireded. Government incentives, such as subsidies and tax credits for residential and commercial solar installations, are accelerating market uptake. The declining cost of solar energy compared to conventional sources creates it an economically attractive option for businesses and hoapplyholds. This sustained growth in downstream demand creates a compelling case for increasing upstream polysilicon production capacity within Europe to secure supply chains. The strategic imperative to localize production aligns with broader industrial policies aimed at reducing import depconcludeency.

Implementation of the European Chips Act and Semiconductor Sovereignty

The implementation of the European Chips Act and the broader push for semiconductor sovereignty significantly drive demand for electronic-grade polysilicon in Europe, which is further boosting the European polysilicon market growth. This legislation aims to double the EU’s global market share in semiconductors to 20% by 2030, requiring a robust domestic supply of high-purity materials. As per the European Semiconductor Industest Association, the region currently produces approximately 10% of the world’s semiconductors, despite consuming a large portion of them. Electronic-grade polysilicon is the essential precursor for manufacturing silicon wafers applyd in chips for automotive, aerospace, and consumer electronics. The act seeks to mobilize over 43 billion euros in public and private investment to build new fabrication plants and material supply chains. According to the European Commission, the initiative seeks to mitigate risks associated with supply chain disruptions and geopolitical instability. Major semiconductor manufacturers are announcing new facilities in Europe, which will require consistent supplies of ultra-high purity polysilicon. The automotive sector’s transition to electric vehicles and autonomous driving technologies further amplifies the required for advanced chips. This structural shift in industrial policy creates a stable and growing demand base for local polysilicon producers. The focus on quality and traceability favors domestic suppliers who can meet stringent regulatory and performance standards. This driver underscores the strategic importance of polysilicon beyond just energy applications.

MARKET RESTRAINTS

Prohibitive Energy Costs and Carbon Intensity Concerns

Prohibitive energy costs and carbon intensity concerns act as a major restraint on the Europe polysilicon market, given the energy-intensive nature of production. The Siemens process and fluidized bed reactor methods applyd to produce polysilicon require vast amounts of electricity and heat to maintain high temperatures and facilitate chemical reactions. As per the International Energy Agency, the production of one kilogram of polysilicon can consume between 50 and 100 kilowatt hours of electricity, depconcludeing on the efficiency of the plant. Electricity prices in Europe are significantly higher than in major producing countries like China, where coal-powered energy keeps costs low. According to Eurostat, industrial electricity prices for non-hoapplyhold consumers in the EU remained elevated at an average of €0.1902 per kWh in 2025 due to geopolitical tensions and the transition away from Russian gas. This cost disadvantage creates it difficult for European producers to compete on price with imported polysilicon. Additionally, the carbon footprint of polysilicon production is a critical concern for environmentally conscious acquireers and regulators. If the energy source is not renewable,e the resulting polysilicon may not meet the sustainability criteria required for green certifications. The lack of affordable and abundant low-carbon energy infrastructure limits the scalability of domestic production. Companies face a dilemma between maintaining competitiveness and adhering to strict environmental standards. This economic barrier discourages new investments and slows the development of local capacity. Without significant subsidies or access to cheap renewable energy, the European polysilicon industest struggles to achieve cost parity.

Dominance of Asian Supply Chains and Economies of Scale

The dominance of Asian supply chains and established economies of scale is another significant restraint on the Europe polysilicon market by creating high barriers to entest. China currently controls over 80% of global polysilicon production capacity, benefiting from decades of investment and optimized manufacturing processes. As per the International Renewable Energy Agency, Chinese producers achieve lower costs through vertical integration, large-scale operations, and government support. This market concentration allows Asian suppliers to offer polysilicon at prices that European startups cannot match without substantial financial aid. According to industest analysis, the capital expconcludeiture required to build a competitive polysilicon plant in Europe is significantly higher due to stricter environmental regulations and labor costs. The existing infrastructure in Asia includes dedicated ports, logistics networks, and skilled workforces that reduce operational friction. European companies face long lead times and complex permitting processes when establishing new facilities. The reliance on imported equipment and technology from Asia further increases depconcludeencies. Buyers in Europe are accustomed to the reliability and volume of Asian supplies, building them hesitant to switch to newer local sources. The risk of stranded assets if global prices drop discourages investors from funding European projects. This structural imbalance perpetuates the status quo and limits the growth potential of domestic producers. Overcoming this restraint requires coordinated policy intervention and long-term off-take agreements.

MARKET OPPORTUNITIES

Development of Green Polysilicon Using Renewable Energy

The development of green polysilicon utilizing renewable energy is a significant opportunity for the Europe polysilicon market by differentiating local products through sustainability credentials. European producers can leverage the region’s abundant wind and solar resources to power energy-intensive manufacturing processes, thereby reducing the carbon footprint of the final product. As per the European Environment Agency, the carbon intensity of electricity generation in the EU has decreased to approximately 250 grams of CO₂ equivalents per kilowatt-hour due to the expansion of renewable capacity. Producing polysilicon with low carbon emissions appeals to manufacturers of premium solar modules and electronics who seek to meet strict environmental standards. According to the Solar Manufacturing Leadership Alliance, there is a growing demand for traceable and sustainable supply chains in the photovoltaic industest. Green polysilicon can command a premium price in markets where carbon taxes or border adjustment mechanisms are implemented. The European Union’s Carbon Border Adjustment Mechanism will impose costs on imports with high embedded emissions, creating a competitive advantage for local low-carbon production. Companies that invest in hybrid energy systems and energy efficiency technologies can position themselves as leaders in sustainable manufacturing. Partnerships with renewable energy providers ensure stable and clean power supplies. This opportunity aligns with the EU’s Green Deal objectives and enhances the global reputation of European industest. It allows local producers to carve out a niche market segment that values environmental responsibility over the lowest cost.

Integration with Circular Economy and Recycling Initiatives

The integration with circular economy and recycling initiatives offers a lucrative opportunity for the Europe polysilicon market by recovering valuable silicon from conclude-of-life products. As the first generation of solar panels reaches the conclude of their operational life, the volume of waste is expected to surge, creating a secondary source of raw materials. As per the International Renewable Energy Agency, global solar panel waste could reach 78 million tons by 2050, with a significant portion originating from Europe. Recycling technologies can recover high-purity silicon from discarded modules and semiconductor scrap, reducing the required for virgin polysilicon production. According to the European Commission, the circular economy action plan aims to double the EU circularity rate to 24% by 2030, emphasizing the importance of resource recovery in strategic industries. Establishing efficient recycling streams can lower production costs and minimize environmental impact. Companies that develop advanced purification techniques to upgrade recycled silicon to electronic or solar grade can capture significant value. This approach reduces depconcludeency on imported raw materials and enhances supply chain resilience. Regulatory frameworks are increasingly mandating higher recycling rates for electronic waste and photovoltaic modules. Investment in recycling infrastructure creates new business models and revenue streams. The ability to offer certified recycled content appeals to sustainability-focapplyd customers. This opportunity supports the transition towards a closed-loop system for critical materials. It positions European companies at the forefront of sustainable material management.

MARKET CHALLENGES

Complex Regulatory Permitting and Environmental Compliance

Complex regulatory permitting and environmental compliance pose a significant challenge to the Europe polysilicon market by delaying project timelines and increasing costs. Establishing new chemical production facilities in Europe involves navigating a labyrinth of environmental impact assessments, safety regulations, and zoning laws. As per the European Court of Auditors, permitting procedures for large-scale industrial projects can involve an average delay of 11 to 17 years compared with original plans, leading to uncertainty for investors. The handling of hazardous chemicals such as trichlorosilane and hydrogen chloride requires strict adherence to safety standards, which adds to operational complexity. According to the European Chemicals Agency, compliance with REACH regulations involves extensive documentation, where the agency conducts completeness checks on approximately 5% of all registration dossiers. Local communities often oppose industrial developments due to concerns about pollution and health risks, leading to legal challenges and delays. The inconsistency in regulatory interpretation across different member states further complicates planning for multinational projects. Companies must allocate substantial resources to manage regulatory affairs and engage with stakeholders. The slow pace of approvals hinders the ability to respond quickly to market demands. This bureaucratic hurdle discourages foreign direct investment and slows the expansion of domestic capacity. Streamlining permitting processes while maintaining high environmental standards remains a critical policy challenge to the European market. Without procedural reforms, the Europe polysilicon market may struggle to attract the necessary capital for growth.

Technological Gap and Lack of Specialized Workforce

The technological gap and lack of specialized workforce are further challenging the expansion of the Europe polysilicon market by limiting innovation and operational efficiency. Decades of outsourcing have resulted in an erosion of technical expertise and know-how in silicon processing within the region. As per the European Centre for the Development of Vocational Training, approximately 72% of firms in relevant manufacturing sectors reported a shortage of skilled labor in 2025. Competing nations have continuously refined their production technologies, achieving higher yields and lower energy consumption. According to industest experts, European companies may face a steep learning curve when restarting or scaling up polysilicon production. The rapid evolution of deposition and purification technologies requires continuous research and development investment, which is costly and time-consuming. Universities and training institutions required to update curricula to meet the specific requireds of the polysilicon industest. The competition for talent with other high-tech sectors, such as pharmaceuticals and automotive, further exacerbates the shortage. Retaining experienced engineers and technicians is difficult due to global mobility and competitive salaries abroad. This human capital deficit hinders the ability to optimize processes and troubleshoot issues efficiently. Collaborative efforts between industest and academia are essential to bridge this gap. Without a robust pipeline of skilled professionals, the European polysilicon industest may struggle to achieve global competitiveness. Addressing this challenge requires long-term strategic investments in education and training.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

Segments Covered |

By Production Process, End-User Industest, and Region. |

|

Various Analyses Covered |

Global, Regional and Countest-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Countries Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

|

Market Leaders Profiled |

Wacker Chemie AG, OCI N.V., REC Silicon ASA, Tokuyama Corporation, GCL Technology Holdings Limited, Hemlock Semiconductor Operations LLC, Daqo New Energy Corp., Xinte Energy Co., Ltd., Mitsubishi Materials Corporation, Tongwei Co., Ltd., Qatar Solar Technologies, Shin-Etsu Chemical Co., Ltd. |

SEGMENTAL ANALYSIS

By Production Process Insights

The Siemens (TCS-CVD) process segment held the leading position in the Europe polysilicon market by capturing 86.1% of the regional market share in 2025. This dominance is driven by the technology’s ability to produce electronic-grade and high-purity solar-grade polysilicon with established reliability and quality consistency. The Siemens process has been the industest standard for decades, allowing manufacturers to achieve purity levels exceeding 99.9999999%, which is critical for semiconductor applications. As per the International Technology Roadmap for Semiconductors, over 90% of silicon wafers applyd in advanced chip manufacturing are derived from polysilicon produced via the Siemens method due to its superior control over impurities. The maturity of this technology means that European chemical engineers possess extensive expertise in optimizing reactor conditions and managing byproducts. According to industest data, the yield efficiency of modern Siemens plants has improved significantly, reducing energy consumption per kilogram of output, although it remains higher than alternative methods. The infrastructure for handling trichlorosilane is well developed in European chemical hubs, such as Ludwigshafen in Germany. Regulatory frameworks in Europe favor proven technologies with known environmental impact profiles, facilitating permitting processes. The ability to scale production while maintaining strict quality standards creates the Siemens process indispensable for high-value applications. Major producers continue to invest in upgrading existing Siemens facilities rather than switching to unproven alternatives. This entrenched position ensures that the Siemens process remains the backbone of the European polysilicon supply chain for the foreseeable future.

However, the fluidized bed reactor process segment is anticipated to record a CAGR of 13.5% over the forecast period, owing to the technology’s significantly lower energy consumption and continuous production capabilities compared to the batch-based Siemens process. The FBR method consumes up to 80% less electricity, which creates it highly attractive in Europe, where energy costs are a major concern. As per the National Renewable Energy Laboratory, the reduced energy intensity of FBR production aligns perfectly with European sustainability goals and carbon reduction tarreceives. The continuous nature of the FBR process allows for higher throughput and lower operational costs, which enhances competitiveness against imported polysilicon. According to industest analysis, several new pilot projects in Europe are exploring FBR technology to produce solar-grade polysilicon specifically for the growing photovoltaic market. The technology is particularly suitable for producing granular polysilicon, which is simpler to handle and load into crucibles for monocrystalline silicon pulling. The decreasing cost of silane gas production further supports the economic viability of FBR. European research institutions are collaborating with industrial partners to optimize FBR parameters for higher purity outputs. The potential for integrating FBR plants with renewable energy sources creates a pathway for truly green polysilicon production. This strategic advantage drives investment and innovation in the FBR segment. As energy prices remain volatile, the economic case for FBR strengthens. This technology represents the future of cost-effective and sustainable polysilicon manufacturing in Europe.

By End-User Industest Insights

The solar photovoltaics segment led the market by accounting for 81.85 of the European market share in 2025. The growth of the solar PV segment in the European market can be credited to the massive deployment of solar energy infrastructure across the continent as part of the REPowerEU strategy. Polysilicon is the fundamental raw material for manufacturing solar cells, which convert sunlight into electricity. As per SolarPower Europe, the European Union installed 65.5 gigawatts of new solar capacity in 2024, requiring thousands of tons of polysilicon. The urgency to replace fossil fuel-based energy sources has accelerated project approvals and investments in solar farms. According to the European Commission, the tarreceive of 600 gigawatts of solar capacity by 2030 necessitates a sustained and growing supply of polysilicon. The decline in solar module prices has created solar energy the cheapest source of electricity in many regions, driving widespread adoption. Residential, commercial, and utility-scale projects all contribute to this demand. The shift towards high-efficiency monocrystalline panels increases the quality requirements for polysilicon but also stabilizes demand for premium grades. Government subsidies and feed-in tariffs provide financial incentives for developers. The long-term nature of solar assets ensures stable demand over decades. The integration of solar with storage systems further enhances its viability. This segment’s dominance is reinforced by policy mandates and economic competitiveness. The scale of the energy transition creates solar the primary driver of polysilicon consumption.

On the other hand, the electronics and semiconductors segment is experiencing the quickest growth and is estimated to register a CAGR of 8.4% over the forecast period due to the European Chips Act and the increasing digitization of industrial and consumer applications. Electronic-grade polysilicon is essential for producing silicon wafers applyd in integrated circuits, microprocessors, and memory chips. As per the European Semiconductor Industest Association, the region currently accounts for roughly 10% of global semiconductor production and is investing heavily to increase this share. The automotive industest’s transition to electric vehicles requires significantly more chips for power management and autonomous driving features. According to the European Automobile Manufacturers Association, a modern battery electric vehicle can require more than twice the value of semiconductors compared to a conventional internal combustion engine car. The rollout of fifth-generation telecommunications networks also drives demand for high-performance chips. Data centers and artificial innotifyigence applications require advanced processors that rely on ultra-pure silicon. The strategic imperative to secure supply chains has led to the construction of new fabrication plants in Europe. These facilities require consistent supplies of high-quality electronic-grade polysilicon. The higher value-added nature of this segment allows for better margins despite lower volumes. Technological advancements in chip design continue to push the boundaries of material purity. This segment represents the high-tech frontier of polysilicon utilization. The focus on sovereignty and innovation ensures sustained growth.

COUNTRY LEVEL ANALYSIS

Germany Polysilicon Market Analysis

Germany dominated the polysilicon market in Europe in 2025 with 27.7% of the regional market share in 2025. The dominance of Germany in the European market is attributed to the countest’s robust chemical industest and ambitious energy transition policies. Germany is home to major chemical companies with expertise in silicon processing and purification. As per the German Federal Ministest for Economic Affairs and Climate Action, the countest aims for a minimum generation share of 80% from renewable energy by 2030, driving significant solar deployment. The automotive sector’s demand for semiconductors also supports polysilicon consumption. According to the German Semiconductor Industest Association, billions of euros are being invested in new fabrication facilities, such as the 3 billion euros Bosch is investing in its semiconductor business by 2026. The presence of research institutes fosters innovation in material science. Germany’s central location facilitates distribution to neighboring markets. The government’s subsidy programs encourage domestic production and research. The strong regulatory framework ensures high environmental standards. The focus on sustainability aligns with green polysilicon production. This combination of policy, industest, and expertise solidifies Germany’s leadership. The countest’s industrial base provides a skilled workforce. The commitment to technological sovereignty drives strategic investments. Germany remains the pivotal hub for polysilicon demand and innovation in Europe.

France Polysilicon Market Analysis

France accounted for a significant share of the Europe polysilicon market in 2025. The growth of France in the European market is driven by its nuclear energy heritage and growing solar ambitions. France has a strong chemical industest capable of supporting polysilicon production and processing. As per the French Ministest of Ecological Transition, the countest plans to reach 100 GW of solar capacity by 2050, creating substantial demand for raw materials. The semiconductor sector in France is expanding with new investments in chip manufacturing. According to the French Semiconductor Industest Cluster, the government is supporting the development of a complete value chain. The availability of low-carbon nuclear electricity offers a competitive advantage for energy-intensive processes. France’s research institutions are leaders in material science and purification technologies. The strategic partnership with other European nations enhances supply security. The regulatory environment supports sustainable industrial practices. The focus on energy sovereignty drives policy decisions. France’s industrial heritage provides a skilled workforce. These factors contribute to a robust and growing market. The emphasis on innovation attracts international collaboration. France is positioning itself as a key player in the European polysilicon landscape.

Italy Polysilicon Market Analysis

Italy is expected to displaycase a promising CAGR in the Europe polysilicon market during the forecast period, owing to a strong solar installation record. The countest has one of the highest solar irradiation levels in Europe, building it ideal for photovoltaic deployment. As per the Italian National Agency for New Technologies, Energy and Sustainable Economic Development, renewable sources covered 41% of national electricity demand in 2025, with solar power generation surging by 25% that year. The government’s incentives have stimulated residential and commercial solar adoption. According to industest data, Italy is a significant importer of solar modules, driving indirect polysilicon demand. The semiconductor industest in Italy is niche but focapplyd on high-value analog chips. The countest’s manufacturing sector requires reliable supplies of electronic components. Italy’s strategic location in the Mediterranean facilitates trade. The focus on energy indepconcludeence has accelerated renewable projects. The regulatory framework is evolving to support local production. The collaboration with European partners enhances supply chain resilience. The cultural emphasis on sustainability supports green initiatives. Italy’s market is driven by both energy and industrial requireds. The potential for local manufacturing is being explored. Italy remains a significant contributor to regional demand.

Netherlands Polysilicon Market Analysis

The Netherlands is predicted to hold a notable share of the Europe polysilicon market over the forecast period, owing to a focus on trade and logistics. The Port of Rotterdam serves as a key entest point for imported polysilicon and semiconductor equipment. As per the Dutch Ministest of Economic Affairs and Climate Policy, the countest is a hub for high-tech systems and materials, with the semiconductor manufacturing equipment market projected to reach 3,442.2 million USD by 2033. The presence of major semiconductor equipment manufacturers drives indirect demand. According to the Holland High Tech association, the sector is a key contributor to the economy, with the front-conclude process segment acting as the largest revenue generator in 2025. The Netherlands is investing in research and development for next-generation materials. The countest’s open economy facilitates international collaboration. The focus on sustainability drives interest in green polysilicon. The regulatory environment is business-friconcludely and innovative. The strong logistics network ensures efficient distribution. The Netherlands plays a critical role in the European supply chain. The emphasis on innovation supports technological advancement. This strategic position enhances its market significance. The countest acts as a gateway for materials entering the EU. The Netherlands is integral to the regional ecosystem.

Spain Polysilicon Market Analysis

Spain is estimated to register a healthy CAGR in the Europe polysilicon market over the forecast period owing to its abundant solar resources. The countest has some of the best conditions for solar energy generation in Europe. As per the Spanish Institute for Diversification and Saving of Energy, the National Integrated Energy and Climate Plan foresees exceeding 76 GW of solar power by 2030. The government has approved numerous large-scale solar projects. For instance, Spain is attracting investment in module manufacturing and has recorded over 32 GW of installed solar power by the conclude of 2024. The semiconductor sector is tinyer but growing, with a focus on power electronics. The availability of land and sunshine supports utility-scale installations. The regulatory framework has been streamlined to accelerate permits. The focus on renewable energy exports enhances market potential. Spain’s integration with the European grid supports stability. The cultural shift towards sustainability drives adoption. The market is poised for significant growth in the coming years. Spain’s natural advantages create it a key player. The countest is becoming a major consumer of polysilicon for solar applications. Spain’s role in the energy transition is expanding rapidly.

COMPETITIVE LANDSCAPE

The competition in the Europe polysilicon market is characterized by a limited number of specialized producers competing against dominant Asian manufacturers. European players differentiate themselves through high-quality standards, sustainability credentials,s and proximity to key customers rather than price alone. The market is influenced heavily by regulatory frameworks such as the European Chips Act and REPower, the EU, which encourage local production. Companies compete by investing in advanced technologies like fluidized bed reactors to reduce energy consumption and carbon footprints. Strategic partnerships with downstream industries ensure stable demand and supply chain integration. The high barrier to entest due to capital intensity and technical expertise limits new competitors. Established firms leverage their existing infrastructure and chemical engineering expertise to maintain advantages. Innovation in purification processes and waste management is critical for compliance and efficiency. The focon electronic-grade polysilicon offers higher margins but requires stringent quality control. Solar-grade producers face intense price competition from imports, necessitating cost optimization. Collaboration with research institutions drives technological advancements. The geopolitical push for supply chain sovereignty creates opportunities for local growth. Adaptability to regulatory modifys and energy market dynamics is essential for sustaining competitive advantage in this strategic sector.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global Europe Polysilicon Market include

- Wacker Chemie AG

- OCI N.V.

- REC Silicon ASA

- Tokuyama Corporation

- GCL Technology Holdings Limited

- Hemlock Semiconductor Operations LLC

- Daqo New Energy Corp.

- Xinte Energy Co., Ltd.

- Mitsubishi Materials Corporation

- Tongwei Co., Ltd.

- Qatar Solar Technologies

- Shin-Etsu Chemical Co., Ltd.

- These companies dominate the polysilicon

TOP LEADING PLAYERS IN THE MARKET

- Wacker Chemie AG is a leading global producer of hyperpure polysilicon with significant manufacturing operations in Burghaapplyn, Germany. The company supplies high-quality material for both the semiconductor and solar industries worldwide. Wacker contributes to the global market by setting stringent quality standards and ensuring reliable supply chains for critical technologies. Recently, the company has focapplyd on expanding its production capacity for electronic-grade polysilicon to meet the growing demand from the chip industest. It has invested heavily in energy efficiency measures and renewable energy sources to reduce the carbon footprint of its operations. Wacker also engages in long-term partnerships with major semiconductor manufacturers to secure stable off-take agreements. These strategic initiatives strengthen its position as a trusted supplier in the European market. The company continues to innovate in purification technologies to maintain its competitive edge. Its commitment to sustainability and quality ensures long-term resilience in the evolving polysilicon landscape.

- REC Silicon ASA is a prominent producer of polysilicon and silane gases with a strong focus on sustainable manufacturing practices. Although its primary production facilities are located outside Europe, the company maintains significant commercial and research operations within the region. REC Silicon contributes to the global market by providing high-purity polysilicon for solar applications utilizing advanced fluidized bed reactor technology. Recently, the company has strengthened its market position by securing long-term supply agreements with major solar module manufacturers in Europe. It is actively exploring opportunities to localize production or processing capabilities within the European Union to align with regulatory incentives. REC Silicon emphasizes its low carbon footprint and energy-efficient production methods to appeal to environmentally conscious customers. The company invests in research and development to improve yield and reduce costs. Its strategic focus on sustainability and reliability enhances its reputation in the European market. REC Silicon plays a crucial role in diversifying the supply chain for European solar manufacturers.

- Siltronic AG is a leading manufacturer of silicon wafers for the semiconductor industest with headquarters in Munich, Germany. While primarily a wafer producer,r the company is deeply integrated into the polysilicon supply chain through strategic partnerships and internal purification processes. Siltronic contributes to the global market by delivering ultra-high-purity silicon wafers essential for advanced chip manufacturing. Recently, the company has expanded its production capacity in Europe to meet the increasing demand from the automotive and industrial sectors. It has invested in state-of-the-art facilities to produce larger-diameter wafers with higher efficiency. Siltronic collaborates closely with polysilicon suppliers to ensure consistent quality and supply security. The company focapplys on innovation in crystal growth and wafer processing technologies. Its strong presence in Europe allows it to respond quickly to customer requireds. Siltronic’s commitment to excellence and sustainability strengthens its position in the competitive semiconductor market. It plays a vital role in the European Chips Act implementation.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe polysilicon market primarily employ strategies focapplyd on sustainability and supply chain localization. Companies are investing heavily in renewable energy sources to power energy-intensive production processes, thereby reducing carbon emissions. This approach aligns with strict European Union environmental regulations and enhances product appeal to eco-conscious customers. Participants are also forming strategic partnerships with downstream manufacturers such as solar module and semiconductor producers to secure long-term off-take agreements. This strategy ensures stable demand and mitigates market volatility risks. Diversification of production technologies, including the adoption of fluidized bed reactors,s assists improve efficiency and lower costs. Companies are also engaging in research and development to enhance purity levels and yield rates. Lobbying for government support and subsidies under initiatives like the European Chips Act is another common strategy. These combined efforts enable firms to navigate regulatory complexities, maintain competitiveness,s and capitalize on the growing demand for locally produced sustainable polysilicon in Europe effectively.

MARKET SEGMENTATION

This research report on the europe polysilicon market is segmented and sub-segmented into the following categories.

By Production Process

- Siemens (TCS-CVD) Process

- Fluidized Bed Reactor (FBR) Process

By End-User Industest

- Solar Photovoltaics

- Electronics & Semiconductors

By Countest

- Germany

- France

- Italy

- Netherlands

- Spain

- Rest of Europe

Leave a Reply