Europe Phenolic Resins Market Summary

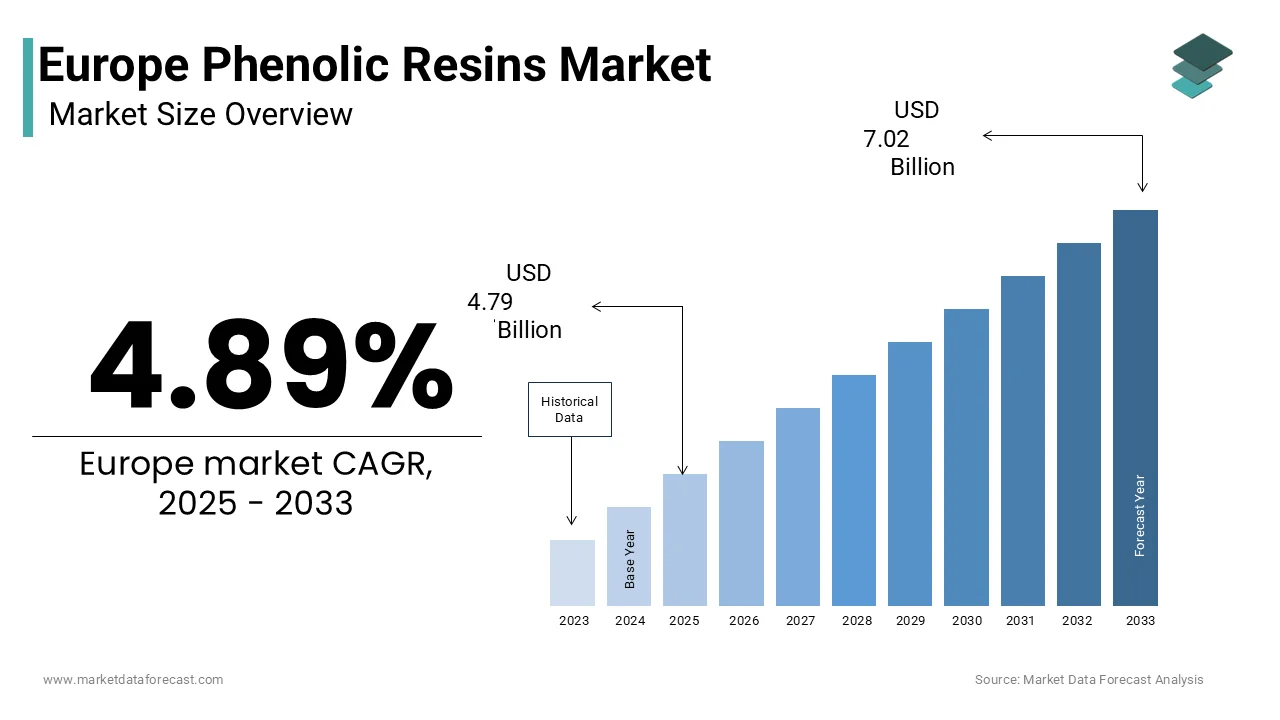

Europe’s phenolic resins market was valued at USD 4.57B in 2024, is estimated at USD 4.79B in 2025, and is forecast to reach USD 7.02B by 2033 (CAGR 4.89%, 2025–2033), driven by construction fire-safety mandates, EV-friction demand, and bio-based phenolic innovation.

Market snapshot

- 2024 value: USD 4.57B

- 2025 (est): USD 4.79B

- 2033 (forecast): USD 7.02B

- CAGR (2025–2033): 4.89%

Quick growth drivers

- EU fire-safety and building-performance rules (EN 13501-1, RE2020, Energy Performance Directive) are boosting phenolic insulation demand.

- Automotive electrification — sustained demand for high-temperature novolac friction/molding compounds in EV brakes and power modules.

- Industrial & foundry demand for phenolic no-bake binders (dimensional accuracy, lower emissions).

- Green finance and building renovation programs are increasing the specification of high-R-value phenolic systems.

Principal restraints

- Tightening formaldehyde rules and REACH compliance → higher CAPEX for low-free-formaldehyde processes.

- Feedstock price volatility (phenol/formaldehyde) and exposure to petrochemical market swings; CBAM/energy costs pressure margins.

- Thermoset recyclability limits and conclude-of-life waste classification under EU circular policies.

High-value opportunities

- Bio-based phenolics (lignin-derived phenol replacements, agricultural waste routes) to cut carbon footprint and win green procurement.

- High-performance insulation for deep retrofit (thin profile, low λ) and cold-chain/industrial refrigeration.

- Novolac in EV & power electronics — high-voltage, high-temperature molding compounds and arc-resistant grades.

- Chemical-recycling pilots and hybrid formulations (thermoset/thermoplastic blconcludes) to address circularity demands.

Principal challenges

- Developing economically viable large-scale bio-phenol routes and meeting identical performance to fossil phenol.

- Achieving meaningful conclude-of-life recycling for crosslinked materials — pilot chem-recycling remains costly.

- Competition from PIR, epoxy, and thermoplastics in mid-performance segments where phenolic’s unique properties are not essential.

Fastest-growing segments (short list)

- Novolac (molding compounds/friction): ~8.12% CAGR — EVs, power electronics, high-temp electrical.

- Molding compounds (application): ~8.44% CAGR — electrification & renewable energy infrastructure.

- Bio-based phenolic technologies (R&D/commercialisation): accelerated uptake in green public procurement (rapid growth potential).

Regional leadership & dynamics

- Germany: market leader (~27.5%) — integrated chemical Verbund, strong automotive and construction demand, active R&D.

- France: strong in insulation and aerospace ablatives; public funding for bio-phenol routes.

- Italy / UK / Spain: sizable demand from wood panels, construction retrofits, and specialized industrial applications; Italy is notable in wood panel resin utilize.

- Nordics / Netherlands: R&D and pilot bio-feedstock initiatives; adoption driven by circularity policies.

What wins commercially (competitive edge)

- Low-free-formaldehyde, certified Ecolabel/REACH-aligned formulations with documented emissions and occupational safety data.

- Backward integration or secure phenol sourcing to stabilise pricing and margins.

- Co-development partnerships with insulation panel buildrs, EV OEMs, and friction compound specialists to lock in specs and long-term supply.

- Early relocater advantage in scalable lignin-based phenolics and demonstrable lifecycle GHG reductions.

Top strategic question for execs

Prioritise a dual-track strategy: (1) secure feedstock resilience (vertical integration / long-term phenol contracts) and (2) accelerate commercialization of lignin/bio-phenol routes plus pilot chemical-recycling partnerships — pair product launches with verified EPDs and tarreceive green public tconcludeers and renovation-wave projects to capture premium pricing.

Some of the companies that are playing a dominating role in the European phenolic resins market include

Hexion Inc. · Sumitomo Bakelite · SI Group · Georgia-Pacific Chemicals · BASF SE · Indspec Chemical · Arizona Chemical · DIC · Kolon · Allnex

Europe Phenolic Resins Market Size

The europe phenolic resins market was valued at USD 4.57 billion in 2024, is expected to reach USD 4.79 billion in 2025, and is projected to reach USD 7.02 billion by 2033, growing at a CAGR of 4.89% from 2025 to 2033.

Phenolic resins are thermosetting polymers derived from the reaction of phenol and formaldehyde, widely utilized as binding and matrix agents in composites, abrasives, friction materials, insulation, and foundry applications. Valued for their exceptional thermal stability, flame resistance, and mechanical strength, these resins serve as critical performance enablers in sectors where safety and durability are non-neobtainediable. According to the European Phenolic Resins Association, phenol is a critical feedstock for resin synthesis in Europe, with Germany, France, and Italy being among the largest consumers. As per IAL Consultants, phenolic insulation materials represent a significant share of the European thermal insulation market, particularly in non‑residential construction, where demand is driven by EU energy performance regulations. The European foundry sector widely employs phenolic no‑bake binder systems for core and mold production, valued for their dimensional accuracy and reduced emissions profile. Furthermore, under the EU’s Ecodesign for Sustainable Products Regulation, phenolic‑based insulation materials are permitted in high‑rise construction due to their compliance with stringent fire safety standards, including Class A1 ratings certified by the European Committee for Standardization. These industrial and regulatory roles affirm phenolic resins as indispensable high‑performance intermediates in Europe’s manufacturing and sustainability infrastructure.

MARKET DRIVERS

Stringent Fire Safety Regulations in Construction and Transportation

Fire safety mandates across Europe are a primary driver for phenolic resin demand due to their unmatched flame resistance and low smoke toxicity, which is one of the major factors propelling the phenolic resins market growth in Europe. According to the European Committee for Standardization, phenolic resins are among the few organic polymer systems capable of achieving Class A1 non‑combustible classification under EN 13501‑1 without the addition of flame retardants. In the construction sector, the EU Energy Performance of Buildings Directive requires all new public buildings to meet near‑zero energy standards, which has significantly increased the adoption of phenolic foam insulation in walls and roofs. As per France’s RE2020 regulation, building materials must demonstrate both low carbon impact and high fire safety and leading to the growing utilize of phenolic panels in high‑rise projects across Paris. Similarly, the European Union Agency for Railways updated its Technical Specification for Interoperability in 2022, requiring interior train components to emit minimal smoke during combustion, which is a benchmark met by phenolic‑based composites. According to Germany’s Federal Railway Authority, phenolic resin‑bonded flooring and ceiling panels are widely utilized in new Deutsche Bahn intercity trains, underscoring their compliance with stringent safety standards. These regulatory frameworks collectively transform phenolic resins from optional materials into compliance necessities across critical infrastructure domains.

Growth in Automotive Lightweighting and Brake Friction Applications

The automotive industest’s pursuit of lightweight, durable components continues to fuel demand for phenolic resins in brake pads, clutch facings, and under-hood composites, which is another notable factor contributing to the European phenolic resins market expansion. According to the European Automobile Manufacturers Association, phenolic resin‑based friction materials are widely utilized in passenger vehicles across Europe, primarily in disc pads and drum linings. With over 13 million cars produced in the EU in 2023 and this represents a substantial annual demand for phenolic resins in braking systems. The shift toward electric vehicles has not diminished this requirement, as EVs demand high‑performance brakes to offset the weight of their battery packs. Major autobuildrs such as BMW and Volkswagen have confirmed that their EV platforms employ phenolic‑bonded pads engineered for low noise and high torque performance. Additionally, phenolic resins serve as binders in lightweight phenolic glass fiber composites utilized in engine covers and transmission houtilizings, offering thermal stability up to 200 degrees Celsius. As per the German Automotive Industest Association, a growing share of German OEMs now specify halogen‑free phenolic formulations to comply with conclude‑of‑life vehicle recycling directives. This deep integration into safety‑critical automotive systems ensures sustained industrial demand for phenolic resins despite ongoing mobility transitions.

MARKET RESTRAINTS

Regulatory Pressure on Formaldehyde Emissions and REACH Compliance

Stringent European regulations on formaldehyde emissions are a significant restraint on the European phenolic resins market. According to the European Chemicals Agency, formaldehyde is classified as a substance of very great concern under REACH due to its carcinogenic properties. As per EU Directive 2019/983, binding occupational exposure limits were set at 0.3 ppm (0.37 mg/m³) over eight hours, underscoring strict workplace safety requirements. This has compelled resin manufacturers to invest in low‑free formaldehyde technologies, which are widely reported to increase production costs, though exact percentages vary depconcludeing on process and scale. In the construction sector, the EU Ecolabel criteria restrict the utilize of binders that release excessive formaldehyde emissions, thereby limiting traditional phenolic formulations. Formaldehyde emission testing under UNI EN 717‑1 standards remains a critical compliance requirement for wood adhesives and insulation products. Regulatory hurdles such as these not only raise compliance costs but also delay product approvals and limit formulation flexibility, particularly for compact and medium‑sized compounders lacking advanced emission control infrastructure.

Volatility in Feedstock Prices and Petrochemical Depconcludeency

The cost instability due to their reliance on phenol and formaldehyde, both derived from fossil-based petrochemical feedstocks subject to global market fluctuations, is also hindering the phenolic resins market growth in Europe. According to the International Energy Agency, European phenol prices experienced sharp volatility in 2023, driven by benzene supply chain disruptions linked to refinery outages in the North Sea. As phenol typically accounts for around 60–65% of raw material costs in standard resole resins, such price swings directly affect resin pricing and margins. As per the European Petrochemical Association, more than 90% of EU phenol capacity is integrated with cumene production, building it highly sensitive to fluctuations in propylene and benzene markets. Furthermore, the EU’s Carbon Border Adjustment Mechanism, introduced in 2023, imposes indirect costs on energy‑intensive chemical production, raising operational expenses for resin plants. According to the industest reports from Germany’s VCI Chemical Industest Association, compacter resin producers often face reduced gross margins when unable to pass through sudden feedstock cost spikes. This petrochemical depconcludeency creates financial unpredictability that discourages long‑term investment in resin capacity and formulation innovation.

MARKET OPPORTUNITIES

Expansion of Bio-Based and Circular Phenolic Resin Technologies

The development of sustainable phenolic resins utilizing bio-derived phenol and recycled content presents a major growth opportunity for the European phenolic resins market. According to the European Institute of Innovation and Technology, companies such as Hexion and Arclin have advanced commercialization of lignin‑based phenolic resins, where a significant share of phenol can be replaced by pulping byproducts from the Nordic forest industest. In 2023, Dutch company Avantium partnered with a German insulation manufacturer to introduce a phenolic foam board containing bio‑based phenol, which is achieving a certified reduction in carbon footprint as verified by TÜV Rheinland. As per the EU’s Horizon Europe program, €18 million was allocated in 2023 to the “BioPhenol” consortium, which is developing scalable routes to produce phenol from agricultural waste. Additionally, Saint‑Gobain’s ISOVER division now offers phenolic insulation panels with post‑consumer recycled content, aligning with the EU’s Level(s) sustainability framework. These innovations not only reduce reliance on fossil feedstocks but also enable compliance with upcoming Ecodesign and Construction Products Regulation requirements mandating environmental product declarations. This transition positions phenolic resins not as legacy chemicals but as evolving enablers of circular construction and sustainable manufacturing.

Growing Demand for High-Performance Insulation in Renovation and Industrial Applications

The EU’s ambitious building renovation wave is creating substantial new demand for phenolic foam insulation in both residential retrofits and industrial cold chain infrastructure, which is another promising opportunity for the European phenolic resins market. According to the European Commission, the Renovation Wave Strategy aims to at least double annual energy renovation rates by 2030 and tarreceives a significant share of the EU building stock and requiring hundreds of millions of square meters of high‑performance insulation. Phenolic foams, with thermal conductivity values reported as low as 0.018 W/(m·K), are uniquely suited for space‑constrained retrofits where maximizing R‑value per millimeter is critical. As per France’s Agency for Ecological Transition, phenolic insulation has gained notable adoption in deep renovation projects for multi‑family buildings due to its thin profile and fire safety performance. In industrial applications, as per the European Cold Chain Federation, refrigerated warehoutilizes must maintain temperatures below –25 °C, which is driving demand for phenolic panels with integrated vapor barriers. Germany has expanded its cold storage footprint substantially, with industest reports noting that phenolic systems are widely specified in new facilities. This dual push from EU energy policy and logistics modernization unlocks sustained volume growth for advanced phenolic resin formulations.

MARKET CHALLENGES

Technical Limitations in Recyclability and End-of-Life Management

The thermoset nature of phenolic resins presents a fundamental challenge to circularity, as cross-linked networks cannot be melted or reprocessed like thermoplastics. According to the European Environment Agency, recycling rates for phenolic composite waste remain very low, with the majority of materials currently landfilled or incinerated due to the absence of viable large‑scale mechanical or chemical recycling pathways. In the automotive sector, the European End‑of‑Life Vehicles Directive mandates 95% recyclability by weight, yet phenolic‑bonded friction materials and under‑hood components are often excluded from recovery streams becautilize of contamination and separation challenges. As per studies from Nordic environmental institutes, brake dust from phenolic pads contributes to persistent micro‑particulate pollution in urban runoff, with remediation protocols still under development. Similarly, demolition waste containing phenolic insulation is classified as non‑inert under the EU Waste Framework Directive, which is complicating disposal and compliance. Although chemical recycling methods such as glycolysis and pyrolysis are being piloted by companies including Röchling and Solvay, these approaches remain energy‑intensive and economically unfeasible at scale. Until scalable closed‑loop solutions are established, phenolic resins will continue to face scrutiny under Europe’s circular economy action plan.

Competition from Alternative Thermoset and Thermoplastic Systems

Phenolic resins face intensifying substitution pressure from competing polymer systems offering clearer processing or perceived environmental advantages, which is another significant challenge to the regional market growth. According to the European Composites Industest Association, unsaturated polyester and epoxy resins have captured a significant share of the composite binder market in wind turbine blades and automotive parts, largely due to their lower cure temperatures and superior fiber wetting properties. As per the European Insulation Manufacturers Association, polyisocyanurate foams now match phenolic thermal performance in many applications while offering higher dimensional stability, building them strong competitors in the insulation sector. Furthermore, bio‑based thermoplastics such as polylactic acid reinforced with natural fibers are gaining traction in non‑structural applications, supported by compostability claims and circular economy initiatives. For instance, phenolic utilize in consumer electronics houtilizings has declined in recent years, as manufacturers increasingly shift to halogen‑free polycarbonates to comply with eco‑design labeling requirements. While phenolics retain dominance in high‑heat and fire‑critical applications, this encroachment in mid‑performance segments erodes both volume and pricing power. Without continuous innovation in processing, sustainability, and hybrid formulations, phenolic resins risk further marginalization in applications where extreme performance is not mandated.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

Segments Covered |

By Product, Application, and Region. |

|

Various Analyses Covered |

Global, Regional, and Countest-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Countries Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

|

Market Leaders Profiled |

Hexion Inc., Sumitomo Bakelite Co., Ltd., SI Group, Inc., Georgia-Pacific Chemicals LLC, BASF SE, Indspec Chemical Corporation, Arizona Chemical Company LLC, DIC Corporation, Kolon Industries, Inc., Allnex Belgium SA/NV, Mitsui Chemicals, Inc., Prefere Resins Holding GmbH, Lerg S.A., Bakelite Synthetics, United Resin Corp., Shengquan Group, ASK Chemicals GmbH, Georgia-Pacific LLC, Fenolit d.d., Jinan Shengquan Group Co., Ltd. |

SEGMENTAL ANALYSIS

By Product Insights

The resol segment led the market and held 3.1% of the European phenolic resins market share in 2024. The dominance of the resol segment in the European market is primarily driven by its single-component, self-curing chemistest that enables rapid processing without added hardeners, which is ideal for continuous industrial applications. In insulation manufacturing, resol-based phenolic foams are the only organic insulation material consistently achieving Euroclass A2 fire performance without halogenated additives, which is a critical requirement under the EU Construction Products Regulation. According to the European Committee for Standardization, phenolic insulation boards sold in the EU predominantly rely on resol chemistest due to its superior dimensional stability and closed‑cell structure that minimizes moisture uptake. Additionally, according to the European Wood Panel Association, exterior‑grade plywood and oriented strand board produced in Northern Europe frequently utilize resol binders for their resistance to boiling water and long‑term durability. As per REACH regulations, modern low‑free formaldehyde formulations are designed to comply with workplace exposure limits of 0.3 ppm (0.37 mg/m³) mandated under EU occupational safety directives. These combined technical and compliance advantages reinforce Resol Chemistest as the backbone of high‑volume industrial resin consumption across Europe.

The novolac segment is the quickest-growing product segment in the European phenolic resins market and is likely to expand at a CAGR of 8.12% over the forecast period, owing to the surging demand in high-temperature electrical and friction applications where thermal char retention and mechanical integrity under stress are paramount. Tier 1 suppliers such as Bosch and ZF have expanded the utilize of novolac‑based molding compounds in high‑voltage electric vehicle power modules, which is citing their arc resistance and low ionic impurity levels as critical performance advantages. As per the European Friction Material Standards Association, novolac binders remain the dominant choice in European brake lining formulations and are loved for their ability to maintain structural cohesion at elevated temperatures, which is an essential property for regenerative braking systems in heavier EVs. Furthermore, innovations in hexamine‑free curing technologies have been revealn to significantly reduce ammonia emissions during compression molding, with reductions of up to 80% reported in recent environmental assessments. These advances position novolac resins as aligned with both the demanding performance requirements of electric mobility and the tightening industrial emission standards across Europe, and fueling their accelerated adoption.

By Application Insights

The insulation segment captured 36.3% of the regional market share in 2024. The leading position of the insulation segment in this regional market can be credited to the stringent EU energy performance directives that prioritize materials with ultra-low thermal conductivity and non-combustible characteristics. According to the European Committee for Standardization, phenolic foam achieves thermal conductivity values as low as 0.017–0.019 W/(m·K), building it one of the lowest among organic insulation materials under EN 13166 certification. As per France’s RE2020 regulation, combustible insulation is restricted in multi‑story residential buildings, which has driven strong adoption of phenolic panels in high‑rise projects due to their fire safety and thin profile advantages. According to the Federal Ministest for Houtilizing, phenolic insulation is frequently specified in public‑funded deep energy retrofits in Germany, particularly where heritage façade constraints require minimal thickness. Moreover, the EU Taxonomy for Sustainable Activities explicitly recognizes high‑performance insulation as a climate mitigation activity, unlocking access to green financing for phenolic‑based projects. These combined regulatory and performance‑driven factors reinforce insulation as the primary consumption channel for phenolic resins across Europe.

The molding compounds segment is anticipated to witness a CAGR of 8.44% over the forecast period in this European market, owing to the electrification of mobility and renewable energy infrastructure, which require electrically insulating, heat-resistant components. Phenolic molding compounds are essential in electric vehicles for components such as battery cell separators, futilize boxes, and DC‑DC converter houtilizings, where continuous operation at 150–180 °C without deformation is required. As per Volkswagen Group disclosures, its Scalable Systems Platform incorporates phenolic molding compounds in EV architectures, which reflects increased material demand compared to internal combustion models. According to the European Power Electronics Roadmap, grid‑scale battery storage installations rely heavily on phenolic compounds for busbar insulators and module frames, which indicates their role in high‑voltage applications. Regulatory support also contributes to the expansion of the molding compounds segment in this regional market as the EU’s RoHS Directive maintains exemptions for phenolic resins in high‑reliability electrical systems due to the absence of technically viable halogen‑free alternatives. Furthermore, the ongoing development of mineral‑filled and glass‑reinforced novolac grades has enhanced arc resistance and tracking performance, which is securing phenolic resins as indispensable materials in next‑generation energy infrastructure.

COUNTRY LEVEL ANALYSIS

Germany Phenolic Resins Market Analysis

Germany led the European phenolic resins market with a 27.5% of the European market share in 2024. The dominance of Germany in the European market is attributed to its integrated chemical manufacturing base, strong automotive demand, and strict building energy codes. As per the German Association of the Automotive Industest (VDA), the automotive sector consumed over 19,000 tonnes of phenolic resins in 2023, primarily for brake pads and clutch facings. In construction, the updated Building Energy Act (GEG 2024) mandates U-values below 0.15 W/m²K for new non-residential buildings, typically achievable with phenolic or mineral wool insulation. Additionally, Germany’s High-Temperature Materials Research Center has advanced low-emission novolac formulations for semiconductor packaging, aligning with the EU Chips Act. Germany is expected to retain its central role in the European phenolic value chain in the coming years.

France Phenolic Resins Market Analysis

France is a promising regional segment in the European phenolic resins market. The building decarbonization policies and aerospace innovation are fuelling the phenolic resins market growth in France. According to Saint-Gobain ISOVER, sales of phenolic insulation boards grew by 38% year-on-year in 2023, supported by public houtilizing projects in Marseille and Bordeaux. Safran applies phenolic-based ablative composites in Ariane 6 rocket nozzles, requiring high char yields under extreme temperatures. France also invests in sustainable innovation, with the France 2030 plan allocating €150 million in 2023 to develop bio-based phenol routes from lignin. France is likely to strengthen its position through policy support and advanced industrial applications.

Italy Phenolic Resins Market Analysis

Italy accounts for a notable share of the European phenolic resins market during the forecast period due to the increasing demand for phenolic resins in wood panel manufacturing and premium automotive applications. As per ASSILEGNO, Italy operates over 1,300 mills producing exterior-grade plywood, consuming around 10,200 tonnes of resol resins annually. Automotive leaders such as Brembo and Marelli utilize novolac-based friction materials in high-performance braking systems for Ferrari and Lamborghini, requiring thermal stability above 400°C. The government’s “Ecobonus” scheme incentivizes thin-profile insulation, boosting phenolic foam adoption in historic city centers. Italy is expected to maintain steady growth, supported by manufacturing excellence and modernization policies.

United Kingdom Phenolic Resins Market Analysis

The United Kingdom is expected to exhibit a healthy CAGR in the European phenolic resins market during the forecast period. The growth of the UK in the European market is driven by construction regulations and specialized industrial applications. As per the UK Insulation Manufacturers Association, phenolic products accounted for 33% of non-residential insulation by value in 2023, particularly in hospitals and data centers. TT Electronics employs phenolic molding compounds for high-voltage insulators in rail and defense systems, while Rolls-Royce consumes over 1,200 tonnes annually in phenolic-bonded composites for aircraft brakes. With the Future Homes Standard set to reduce carbon emissions by 75–80% from 2025, the UK is positioned for stable demand in high-value applications.

Spain Phenolic Resins Market Analysis

Spain is anticipated to account for a noteworthy share of the European phenolic resins market during the forecast period due to the EU-backed construction programs and renewable energy expansion. Spain’s national renovation plan allocates €6.2 billion through 2026 for energy upgrades, which favors phenolic insulation in dense urban retrofits. As per the Spanish Green Building Council, over 135,000 homes underwent deep energy retrofits in 2023, with phenolic capturing 30% of the high-performance insulation segment. The wood panel industest in Galicia and Catalonia consumes more than 5,500 tonnes of resol resins annually, while Iberdrola’s renewable projects integrate phenolic-molded houtilizings in transformers and inverters. Spain is expected to see continued growth, supported by construction demand and clean energy initiatives.

COMPETITIVE LANDSCAPE

Competition in the European phenolic resins market is characterized by a concentrated landscape of multinational chemical giants and specialized regional producers vying for dominance in high-performance applications. The market is not driven by price but by technical differentiation, regulatory certification, and supply chain reliability. Leaders such as Hexion, BAS, F, and SI Group compete through formulation purity, emission control, and thermal stability tailored to exacting conclude-utilize requirements in insulation electronics and friction materials. Barriers to entest remain high due to capital intensity, feedstock integration necessarys, and complex compliance with EU chemical and construction regulations. Regional players focus on niche segments like wood adhesives or abrasives but face pressure from global suppliers offering integrated sustainability solutions. Differentiation increasingly hinges on the ability to deliver bio-based circular and low-carbon resins without compromising performance. This environment fosters continuous innovation but favors incumbents with deep R and D infrastructure, regulatory expertise, and long-standing industrial partnerships across automotive construction and energy sectors.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the European phenolic resins market include

- Hexion Inc.

- Sumitomo Bakelite Co., Ltd.

- SI Group, Inc.

- Georgia-Pacific Chemicals LLC

- BASF SE

- Indspec Chemical Corporation

- Arizona Chemical Company LLC

- DIC Corporation

- Kolon Industries, Inc.

- Allnex Belgium SA/NV

- Mitsui Chemicals, Inc.

- Prefere Resins Holding GmbH

- Lerg S.A.

- Bakelite Synthetics

- United Resin Corp.

- Shengquan Group

- ASK Chemicals GmbH

- Georgia-Pacific LLC

- Fenolit d.d.

- Jinan Shengquan Group Co., Ltd.

TOP LEADING PLAYERS IN THE MARKET

- Hexion Inc. is a global leader in thermosetting resins with a significant presence across Europe, supplying high-performance phenolic resins for insulationmoldinggg, and abrasive applications. The company contributes to the global market through its extensive portfolio of resol and novolac formulations engineered for low emissions and high thermal stability. Recently, Hexion expanded its production capacity for bio-based phenolic resins at its Bergen op Zoom facility in the Netherlands to meet EU sustainability mandates. It also launched its AEROPHEN insulation resin line certified under the EU Ecolabel for ultra-low formaldehyde emissions. These initiatives reinforce Hexion’s commitment to regulatory compliance and circular innovation while strengthening its integration with European construction and automotive supply chains.

- BASF SE is a premier European chemical producer with a strategic focus on advanced phenolic resins for high-value industrial applications, including electronics and friction materials. The company leverages its integrated Verbund site in Ludwigshafen, Germany, to ensure a secure phenol and formaldehyde feedstock supply for resin synthesis. In 2023, BASF introduced a halogen-free novolac molding compound tailored for 800-volt electric vehicle power modules meeting stringent IEC 60112 tracking resistance standards. It also partnered with the Fraunhofer Institute to develop chemical recycling pathways for phenolic composite waste. These actions highlight BASF’s dual emphasis on electrification readiness and conclude-of-life sustainability, positioning it at the forefront of next-generation phenolic technology.

- SI Group is a specialty chemical company with deep expertise in performance phenolic resins serving aerospace, automotive, and industrial markets across Europe. The company is globally recognized for high-purity novolac resins utilized in brake pads, clutch facing,,s and semiconductor encapsulants. To strengthen its European footprint, SI Group upgraded its production line in Sch OpaGe Germa,nyy in 2023 to produce lo,w odor low smoke phenolic resins compliant with EU REACH and rail fire safety standards. It also launched its VALOX FR portfoflame-retardanttardant resins for battery components in collaboration with major EV suppliers. These strategic enhancements underscore SI Group’s focus on safety-critical applications and regulatory alignment in high-growth sectors.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the European phenolic resins market employ several core strategies to maintain competitiveness and drive sustainable growth. They prioritize regulatory compliance by developing low-free formaldehyde and halogen-free formulations aligned with REACH and Ecolabel requirements. Companies invest in backward integration to secure a stable phenol and formaldehyde feedstock supply and mitigate price volatility. Strategic capacity expansions in Western and Central Europe address rising demand from the construction and electrification sectors. Innovation in bio-based phenolics utilizing lignin or waste-derived phenol supports circular economy objectives under EU Green Deal policies. Additionally, firms deepen application engineering partnerships with insulation panel buildrs,sbrakemanufacturersrs and EV components suppliers to co-develop customized resin solutions that enhance performance and processing efficiency.

MARKET SEGMENTATION

This research report on the europe phenolic resins market is segmented and sub-segmented into the following categories.

By Product

By Application

- Insulation

- Molding Compounds

By Countest

- Germany

- France

- Italy

- United Kingdom

- Spain

- Rest of Europe

Leave a Reply