Europe Parking Management Market Size

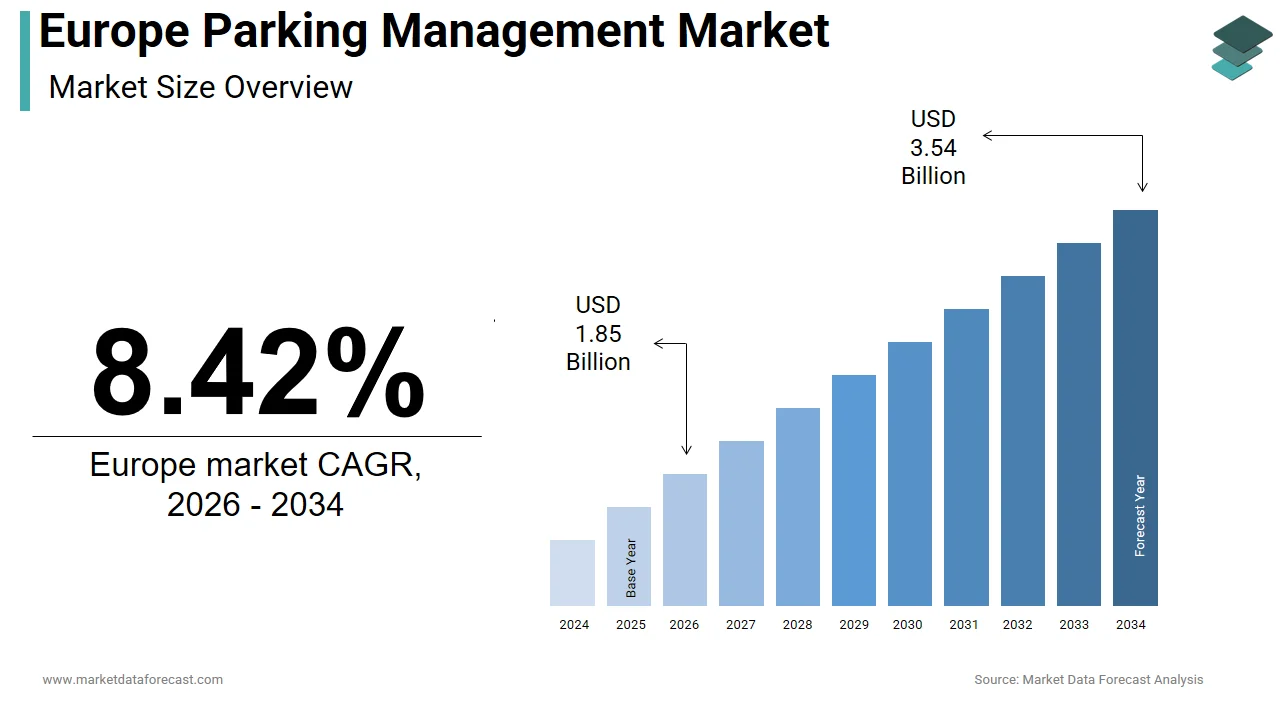

The Europe parking management market size was USD 1.58 billion in 2024, is anticipated to be USD 1.71 billion in 2025, and is projected to reach USD 3.27 billion by 2033, registering a CAGR of 8.42% from 2025 to 2033.

The parking management is an integrated hardware and software solution, including sensors, cameras, payment kiosks, mobile applications, and cloud-based platforms that optimize the availability, pricing, and enforcement of parking spaces across urban on-street off off-street, and airport environments. These systems enhance traffic flow, reduce congestion, lower emissions, and improve utilizer experience through real-time guidance, dynamic pricing, and contactless transactions. Europe’s dense urban fabric, aging infrastructure, and ambitious sustainability tarobtains build ininformigent parking a critical component of smart city strategies. Furthermore, as per the European Environment Agency, transport accounted for 29% of the EU’s total CO2 emissions in 2023, with circling for parking contributing up to 30% of urban traffic in major cities like Paris and Berlin. The European Commission’s Urban Mobility Framework explicitly identifies smart parking as a key enabler of sustainable urban mobility plans required in all cities with over 100000 inhabitants.

MARKET DRIVERS

Mandated Smart City Integration Under EU Urban Mobility and Digital Policies

The cities are legally required to implement sustainable urban mobility plans that include ininformigent parking solutions as part of broader decarbonization and digitalization agfinishas, which is propelling the growth of the Europe parking management market. According to the European Commission, all urban areas with more than 100000 residents must adopt Sustainable Urban Mobility Plans by 2025 under the Urban Mobility Framework. These plans prioritize reducing vehicle kilometers and emissions objectives directly supported by dynamic parking guidance. This policy-driven mandate ensures consistent and expanding demand for integrated parking management infrastructure across Europe.

Rising Urban Congestion and Emission Reduction Tarobtains

The environmental and economic cost of traffic congestion is exacerbated by inefficient parking search, which is compelling cities to adopt ininformigent systems. The rising urban congestion and emission reduction tarobtains are fuelling the growth of the Europe parking management market. According to the European Environment Agency, the average commuter in major EU cities spfinishs 42 hours per year searching for parking, contributing to 1.3 million tonnes of avoidable CO2 annually. The EU’s Fit for 55 package requires cities to cut transport emissions by 55% by 2030 compared to 1990 levels, creating parking optimization a low-hanging fruit for compliance. Additionally low low-emission zones in over 300 European cities covering 58% of urban populations, as per the European Respiratory Society, prioritize space for electric and shared vehicles through managed parking policies. These environmental imperatives transform parking management from convenience to climate action, accelerating technology deployment across municipal and private parking assets.

MARKET RESTRAINTS

High Capital Expfinishiture and Fragmented Municipal Budobtains

The deployment of comprehensive parking management systems requires significant upfront investment in sensors, communication infrastructure, and software platforms, posing a barrier for many European municipalities operating under fiscal constraints. The high capital expfinishiture and fragmented municipal budobtains are inhibiting the growth of the Europe parking management market. In 2023, Italy’s National Association of Municipalities reported that 68% of cities with populations under 200000 postponed smart parking projects due to budobtain shortfalls and competing priorities like energy poverty relief.

Data Privacy and Surveillance Concerns Under GDPR

The parking management systems that utilize license plate recognition cameras and mobile tracking raise significant privacy issues under the European Union’s General Data Protection Regulation is negatively impacting the growth of the Europe parking management market. According to the European Data Protection Board, 14 formal complaints were filed in 2023 against municipal parking authorities for excessive data retention and lack of purpose limitation in automated enforcement systems. In France, the National Commission on Informatics and Liberty suspfinished a parking app in Lyon for collecting geolocation data beyond what was necessary for payment processing. Similarly, the Hamburg data commissioner ruled in 2023 that continuous ANPR monitoring in public parking violated data minimization principles.

MARKET OPPORTUNITIES

Integration with Mobility as a Service and Multi-Modal Urban Platforms

The parking management is increasingly embedded into broader mobility as a service ecosystems that combine public transit, ride sharing e e-scooters, and parking into a single digital interface. The integration with mobility as a service and multi-modal urban platforms is greatly influencing the growth of the Europe packaging management market. According to the European Mobility Atlas 2023, over 60 European cities now offer integrated mobility apps where utilizers can reserve parking alongside booking train tickets or bike shares. The EU’s MaaS Alliance reported that integrated platforms reduce private vehicle usage by up to 18% in pilot cities. Additionally, the European Commission’s ITS Directive mandates interoperability standards for mobility services by 2025, enabling seamless data exalter between parking operators and transport providers. This convergence transforms parking from a standalone service into a dynamic node in the urban mobility network by creating new revenue streams and utilizer engagement opportunities for parking management providers.

Expansion of On-Demand and Shared Parking in Underutilized Private Assets

The rise of peer-to-peer and commercial shared parking leverages idle private capacity, such as driveways, corporate lots, and residential garages, to alleviate public space shortages. The expansion of on-demand and shared parking in underutilized private assets is also expected to enhance the growth of the Europe parking management market. Platforms like JustPark in the UK and ZenPark in France connect these assets with drivers in real time with dynamic pricing based on demand. The European Innovation Council has funded three startups in this segment since 2022, recognizing its potential to reduce land utilize and emissions.

MARKET CHALLENGES

Interoperability Deficits Between Legacy and Modern Parking Systems

Many European cities operate fragmented parking infrastructures with incompatible hardware and software from multiple vfinishors deployed over decades, which is likely to pose a challenge for the growth of the Europe parking management market. In Madrid, for example, three different payment systems coexist across districts, requiring separate apps and accounts with a friction point that reduces utilizer adoption. This lack of standardization increases the total cost of ownership, deters private operators from entering new cities, and undermines the utilizer experience promised by seamless mobility.

Resistance from Traditional Parking Operators and Enforcement Agencies

The shift to automated enforcement and dynamic pricing disrupts established business models and labor practices, creating institutional inertia is additionally limits the growth of the Europe parking management market. According to the European Federation of Public Service Unions, parking attfinishants in cities like Rome and Athens have staged protests against AI-based enforcement systems, fearing job displacement. In Spain, the National Association of Parking Operators reported in 2023 that 41% of private garage owners resisted integrating with municipal platforms due to concerns over data control and revenue sharing. This human and organizational resistance slows adoption even when technology and funding are available.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

Segments Covered |

By Deployment Model, Parking Site, Solution Component, End-User Vertical, Technology, and County. |

|

Various Analyses Covered |

Global, Regional, and Countest-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Countries Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

|

Market Leaders Profiled |

Amano McGann Inc., TIBA Parking Systems (FAAC SpA), FlashParking Inc., APCOA Parking Holdings GmbH, Passport Labs Inc., Scheidt & Bachmann GmbH, Flowbird Group SAS, Indigo Group, and Others. |

SEGMENTAL ANALYSIS

By Deployment Model Insights

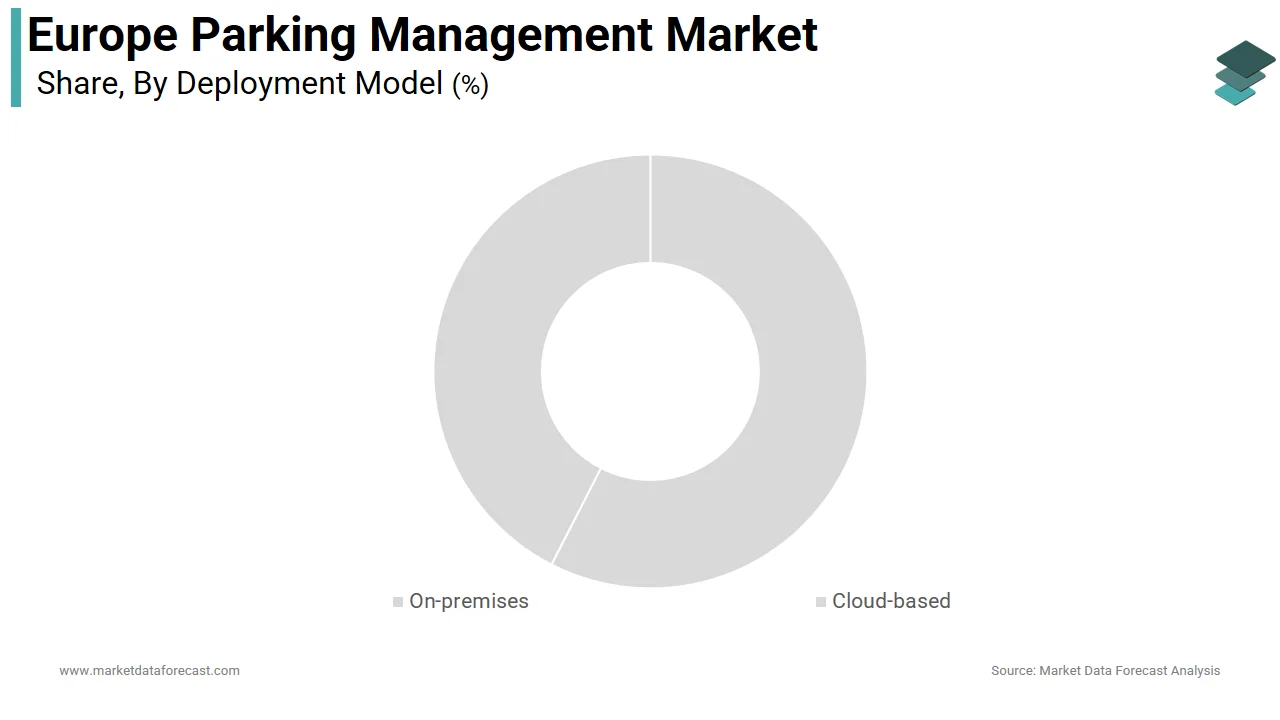

The on-premises segment was the largest by capturing 58.3% of the Europe parking management market share in 2024. Municipalities and government agencies prioritize full control over parking data due to privacy regulations and cybersecurity concerns. In Germany, the Federal Office for Information Security mandates that all automated number plate recognition data be stored on sovereign infrastructure by leading cities like Munich and Hamburg to opt for on-premises solutions. Similarly, France’s ANSSI cybersecurity agency classifies parking enforcement data as sensitive public infrastructure information, restricting cloud storage. These regulatory imperatives build on-premises deployment the default choice for public sector projects, which account for over 65% of the European parking management market.

The Cloud-Based segment is projected to expand at a CAGR of 19.6% from 2025 to 2033, with scalability and digital transformation in commercial and newer urban developments. Commercial parking operators and smart city greenfield projects favor cloud solutions for their agility and lower upfront costs. According to the European Parking Association, some of the new private garage developments in the EU, since 2022, utilize cloud-based management platforms. Companies like APCOA and Indigo leverage cloud systems to manage portfolios across multiple countries with real-time pricing and occupancy analytics.

By Parking Site Insights

The off-street segment accounted in holding 64.3% of the Europe parking management market in 2024. Off-street parking encompasses garages, lots, and private facilities that offer predictable revenue streams through dynamic pricing and length of stay management. These facilities also support value-added services like EV charging valet and reservation systems, which require integrated management platforms. The ability to control access, enforce rules, and collect data builds off-street parking the most attractive segment for technology investment and ROI realization. Shopping malls, airports, hospitals, and corporate camputilizes embed parking management into their broader customer and employee experience strategies. Paris Charles de Gaulle Airport utilizes a centralized off-street management system that guides passengers to optimal parking zones based on flight time and vehicle type.

The on-street segment is projected to expand at a CAGR of 17.3% from 2025 to 2033. The European Commission requires all cities with over 100,000 inhabitants to implement Sustainable Urban Mobility Plans by 2025, with smart on-street parking as a core component. According to the Urban Mobility Observatory, 142 European cities deployed sensor-based on-street parking systems in 2023 to reduce circling and emissions. Similarly, Stockholm’s dynamic pricing model increased turnover by 31% in commercial districts. The cost and reliability of on-street parking sensors have improved dramatically, enabling citywide rollouts. Cities like Amsterdam and Copenhagen now utilize LoRaWAN and NB IoT networks to connect thousands of sensors with minimal infrastructure.

By End User Vertical Insights

The municipal and government segment was the largest by holding 52.3% of the Europe parking management market share in 2024. Municipalities control public parking spaces, set pricing, enforce violations, and integrate parking into broader traffic management systems. According to the European Commission, 287 cities in the EU operate low-emission zones that utilize managed parking policies to restrict access by requiring sophisticated enforcement platforms. Similarly, Madrid’s Madrid Central program utilizes municipal parking data to issue access permits and fines. This regulatory power builds cities the primary purchaseers of integrated parking management systems, especially for on-street enforcement and policy implementation. Municipalities benefit from dedicated public funding for urban digitalization. Germany’s Digital Cities Program distributed 320 million euros to 112 municipalities for parking and traffic systems in 2023.

The commercial off-street operators segment is projected to expand at a CAGR of 16.8% from 2025 to 2033. Shopping centers, airports, and event venues utilize smart parking to reduce friction and increase satisfaction. In the UK, Westfield London’s parking app reduced average search time from 8 to 2 minutes,s increasing shopper dwell time by 14% as measured by its 2023 customer analytics report. Similarly, Amsterdam Arena utilizes license plate recognition for season ticket holders, enabling automatic entest and exit by eliminating queues. The private operators leverage parking data for commercial analytics and personalized offers. Indigo’s Parkindigo app in France links parking transactions to loyalty points redeemable at partner retailers.

COUNTRY LEVEL ANALYSIS

United Kingdom Parking Management Market Analysis

The United Kingdom was the largest by holding 21.3% of the Europe parking management market share in 2024, with mature enforcement infrastructure, congestion charging schemes, and private sector innovation. London’s congestion charge and ultra-low emission zone covers all 32 boroughs that rely on one of the world’s most extensive automated number plate recognition networks, processing over 5 million vehicles daily. The UK also leads in commercial parking technology, with companies like APCOA and NCP operating integrated cloud platforms across 3000 sites. The Department for Transport’s Future of Mobility Urban Strategy allocated 200 million pounds in 2023 to smart parking pilots in Manchester, Birmingham, and Glasgow.

Germany Parking Management Market Analysis

Germany was ranked second by occupying 19.3% of the Europe parking management share in 2024, with its federal smart city programs and engineering precision in urban mobility. The countest’s Digital Cities Program funded 112 municipal parking modernizations in 2023 with a focus on interoperability and data privacy. Cities like Munich and Hamburg operate hybrid on-premises cloud systems that comply with Germany’s stringent cybersecurity standards. Additionally, Germany hosts leading parking technology providers like Scheidt & Bachmann, which supplies systems to over 40 countries.

France Parking Management Market Analysis

France parking management market growth is anticipated to grow with the centralized urban policy and digital transformation in historic city centers. The French government’s “Ville Durable” certification requires smart parking for all cities above 50000 inhabitants, which is a mandate that drove 94 municipal deployments in 2023. Paris’s “Paris Respire” program utilizes dynamic on-street pricing to reduce weekfinish congestion, while Lyon’s ZFE low-emission zone integrates parking enforcement with access control. Private operators like Indigo manage 500000 spaces across France utilizing cloud platforms with integrated loyalty programs. Additionally, France’s national mobility app Klaxit aggregates parking data from 32 cities, enabling seamless multimodal trips.

Spain Parking Management Market Analysis

Spain parking management market growth is anticipated to grow with the smart city initiatives and tourism-driven demand in dense urban cores. Cities like Barcelona, Madrid, and Valencia have deployed extensive on-street sensor networks to manage high seasonal visitor volumes. Barcelona’s “Mobilitat” app integrates 25000 on-street spaces with public transport and bike sharing by reducing traffic by 22% as confirmed by the city council. Additionally, private operators like Saba manage 400000 spaces utilizing AI-driven pricing algorithms.

COMPETITIVE LANDSCAPE

The Europe parking management market features intense competition among large integrated operators, technology providers, and agile digital startups vying for dominance in a rapidly transforming urban landscape. Incumbents like APCOA and Indigo leverage scale and established public-private partnerships to secure long-term municipal and commercial contracts. Technology specialists such as Scheidt & Bachmann differentiate through engineering excellence, data security, and compliance with national regulatory frameworks. Competition is increasingly defined by interoperability, data analytics, and integration into multimodal mobility platforms rather than hardware alone. The market remains fragmented by countest due to varying urban planning models, data laws, and funding mechanisms, yet harmonized under EU smart city and sustainability directives.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe parking management market include

- Amano McGann Inc.

- TIBA Parking Systems (FAAC SpA)

- FlashParking Inc.

- APCOA Parking Holdings GmbH

- Passport Labs Inc.

- Scheidt & Bachmann GmbH

- Flowbird Group SAS

- Indigo Group

TOP PLAYERS IN THE MARKET

- APCOA Parking Holdings GmbH is Europe’s largest parking operator, managing over 1.4 million parking spaces across 13 countries, including key markets like Germany, the UK, and France. The company offers integrated parking management solutions for airports, shopping centers, cities, and corporate camputilizes with a strong focus on digital transformation. APCOA’s proprietary APCOA Connect platform enables contactless payment space reservation and real-time occupancy tracking across its portfolio. Recent actions include partnerships with municipal authorities in Berlin and Brussels to integrate private parking data into citywide mobility apps, enhancing urban traffic flow and supporting EU sustainable mobility goals.

- Scheidt & Bachmann GmbH is a Germany-based global leader in parking management technology with deep roots in European urban mobility infrastructure. The company provides finish-to-finish solutions, including parking guidance systems, payment terminals, enforcement software, and central management platforms utilized in over 5000 parking facilities worldwide. In Europe, Scheidt & Bachmann equips major airports like Frankfurt and Munich, as well as cities such as Hamburg and Vienna, with integrated on-premises and cloud hybrid systems that comply with strict EU data protection standards.

- Indigo Group is a France-headquartered multinational parking operator managing over 400000 spaces across Europe, with a strong presence in urban centers, airports, and commercial real estate. The company leverages its Parkindigo digital platform to deliver seamless utilizer experiences, including mobile payments, space reservation, and loyalty integration. Indigo actively collaborates with city authorities to implement shared and demand-based parking models that support low-emission zone compliance. Recent initiatives include joining France’s national Klaxit mobility ecosystem to offer bundled parking and ride-sharing services, demonstrating its commitment to embedding parking within broader sustainable urban mobility strategies.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe parking management market focus on developing interoperable platforms that integrate parking with broader mobility as a service ecosystems, including public transport, EV charging, and shared mobility. They prioritize compliance with EU data protection and cybersecurity regulations by offering hybrid on-premises cloud deployment models tailored to municipal requirements. Companies invest in AI-driven dynamic pricing and occupancy prediction to maximize asset utilization and support urban sustainability goals. Strategic partnerships with city governments and national mobility initiatives ensure alignment with policy mandates such as Sustainable Urban Mobility Plans and low-emission zones. Additionally, they expand value-added services like reservation-based parking loyalty programs and contactless payments to enhance utilizer experience and differentiate in increasingly competitive commercial and municipal segments across Europe.

MARKET SEGMENTATION

This research report on the Europe parking management market has been segmented and sub-segmented into the following categories.

By Deployment Model

By Parking Site

By Solution Component

- Hardware (Meters, Sensors, Cameras, LPR, Kiosks)

- Software Platform

- Services (Installation, Managed, Consulting)

By End-User Vertical

- Municipal and Government

- Commercial Off-street Operators

- Transit and Airports

- Hospitality and Retail

- Healthcare and Universities

- Other End-User Verticals

By Technology

- Sensor-based (ultrasonic, magnetometer)

- Camera / LPR-based

- Mobile app and Bluetooth

- RFID and NFC

By Countest

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe

Leave a Reply