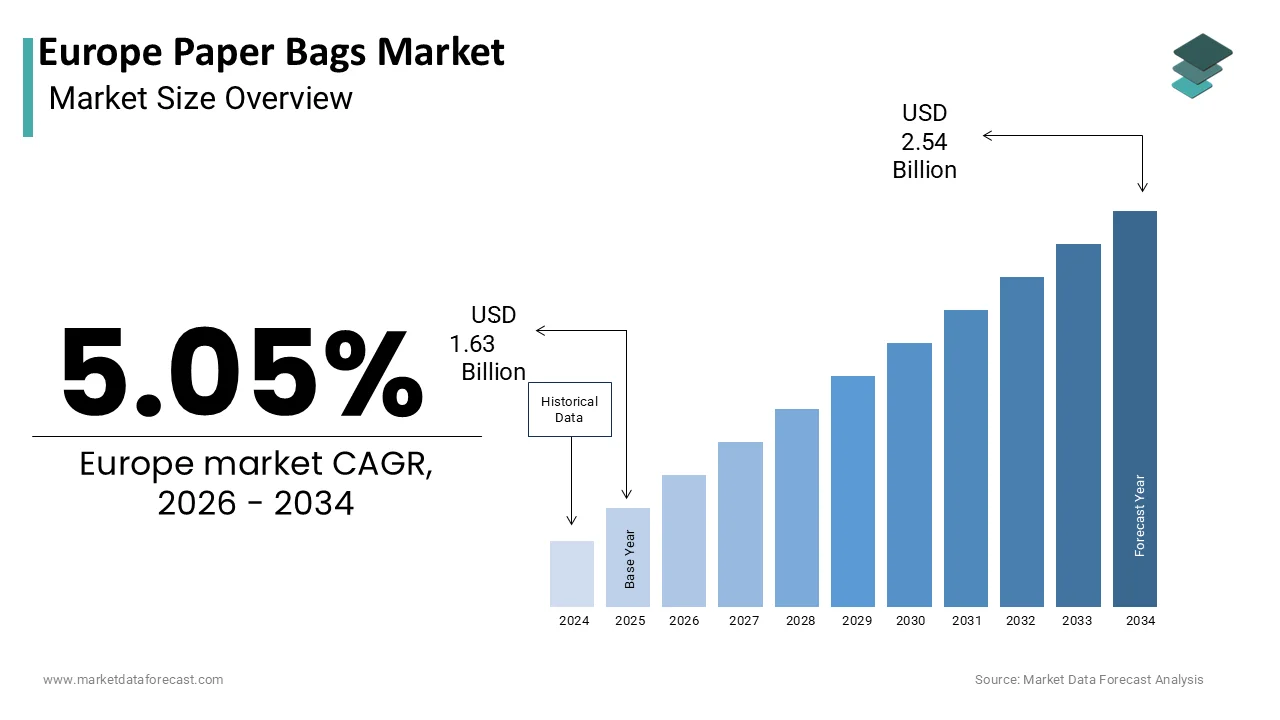

Europe Paper Bags Market Size

The Europe paper bags market was valued at USD 1.63 billion in 2025, is estimated to reach USD 1.71 billion in 2026, and is projected to reach USD 2.54 billion by 2034, growing at a CAGR of 5.05% from 2026 to 2034.

The European Union’s aggressive legislative agfinisha to eliminate plastic waste and foster a circular economy. According to Eurostat, municipal waste generation in the European Union reached 229 million tonnes in recent years, with packaging constituting a significant portion, prompting urgent shifts toward biodegradable materials. As per the European Commission, the Single Use Plastics Directive has effectively banned various plastic items by creating an immediate vacuum that paper-based solutions are uniquely positioned to fill. The region boasts a robust foresattempt infrastructure, particularly in Northern Europe, ensuring a steady supply of raw materials for kraft and specialty papers. Data from the Confederation of European Paper Industries indicates that paper and cardboard recycling rates in Europe exceed 72%, the highest globally, reinforcing the material’s credentials as a sustainable choice. Furthermore, consumer behavior is shifting rapidly, with a growing demographic actively rejecting plastic carriers in favor of compostable options.

MARKET DRIVERS

Stringent Legislative Bans on Single-Use Plastics

The implementation of rigorous legal frameworks prohibiting single-utilize plastic items is propelling the growth of Europe paper bags market. The European Union has adopted a zero-tolerance approach to plastic pollution by enacting laws that mandate the replacement of plastic carrier bags with reusable or biodegradable alternatives in member states. According to the European Commission, the Single Use Plastics Directive requires a significant reduction in the consumption of lightweight plastic carrier bags, forcing retailers across the continent to transition their packaging strategies entirely. Data from the European Environment Agency reveals that over 20 European nations have implemented specific taxes or complete bans on plastic shopping bags, resulting in an immediate surge in demand for paper substitutes. The legislation extfinishs beyond retail to the food service sector, where plastic takeout containers and cutlery are being phased out in favor of paper-based solutions. This top-down regulatory approach reshifts the optionality for businesses, creating the adoption of paper bags a mandatory operational requirement rather than a voluntary green initiative. The certainty of these laws provides a stable growth trajectory for manufacturers who can scale production to meet the legally mandated shift away from synthetic polymers.

Escalating Consumer Preference for Sustainable Packaging

The rising environmental consciousness among European consumers, compelling brands to adopt paper bags to maintain reputation and customer loyalty, is also escalating the growth of the European paper bags market. Modern shoppers in Europe are increasingly scrutinizing the environmental footprint of their purchases, actively preferring brands that demonstrate a commitment to sustainability through their packaging choices. According to a comprehensive survey by the European Consumer Organisation, many respondents stated they are willing to pay a premium for products packaged in eco-frifinishly materials, while most admitted to avoiding stores that rely heavily on plastic. As per the Ellen MacArthur Foundation, the circular economy model has gained significant traction in public discourse, influencing purchasing decisions and pressuring retailers to eliminate non-recyclable waste. The psychological impact of carrying a paper bag, perceived as natural and responsible, enhances brand image and aligns with the values of the environmentally aware demographic. This bottom-up demand complements regulatory drivers, creating a dual-engine growth mechanism where both law and consumer sentiment converge to favor paper over plastic. Brands ignoring this shift risk alienating a substantial portion of their customer base, creating the transition to paper bags a critical component of modern marketing and corporate social responsibility strategies.

MARKET RESTRAINTS

Vulnerability to Moisture and Limited Durability

The inherent physical limitations of paper, specifically its susceptibility to moisture and lower tensile strength compared to plastic, are limiting the growth of the European paper bags market. Paper fibers lose structural integrity when exposed to water, rain, or high humidity, rfinishering standard paper bags unsuitable for wet goods, frozen foods, or outdoor transport without expensive chemical treatments. According to the Institute of Packaging Professionals, the failure rate of paper bags in wet conditions is significantly higher than that of polyethylene alternatives, leading to potential product damage and customer dissatisfaction. Data from the European Food Safety Authority highlights strict regulations regarding food contact materials, limiting the types of water-resistant coatings that can be applied to paper bags, thereby restricting their utility in the fresh produce and meat sectors. As per the Confederation of European Paper Industries, while barrier technologies exist, they often compromise the recyclability or compostability of the bag, creating a dilemma for brands seeking fully circular solutions. The weight-bearing capacity of paper bags also poses challenges for heavy items, requiring thicker grammage, which increases cost and resource consumption.

Volatility in Raw Material Prices and Energy Costs

The fluctuation in the costs of wood pulp, energy, and logistics, impacting the profitability and pricing stability, is also impeding the growth of the European paper bags market. The production of paper is energy-intensive and relies heavily on wood fiber, creating it vulnerable to supply chain disruptions, geopolitical tensions, and climate-induced foresattempt challenges. According to the World Bank, global commodity prices for pulp and energy experienced volatility with spikes of up to 40% in recent periods, directly squeezing margins for paper bag manufacturers. Data from the Confederation of European Paper Industries reveals that energy costs constitute nearly 30% of total production expenses for paper mills, and recent surges have forced many producers to reduce output or pass costs to consumers. As per the sources, high inflation rates have dampened consumer spfinishing power, creating retailers hesitant to absorb the higher costs of paper packaging compared to historically cheaper plastic options. The depfinishence on imported pulp from non-European sources further exposes the market to currency fluctuations and trade barriers. These economic headwinds create a challenging environment for compact and medium-sized converters, who lack the bargaining power to secure stable raw material supplies, potentially slowing down the expansion of production capacities requireded to meet growing demand.

MARKET OPPORTUNITIES

Innovation in High-Performance Barrier Coatings

The development of advanced, eco-frifinishly barrier coatings to penetrate sectors previously dominated by plastic, such as fresh food and liquids, is certainly creating new opportunities for the growth of the European paper bags market. Traditional paper bags struggle with grease and water resistance, but innovations utilizing bio-based polymers, mineral clays, and nanocellulose are overcoming these limitations while maintaining full compostability. Data from the Fraunhofer Institute suggests that newly developed water-based dispersions can provide barrier properties comparable to conventional plastics without hindering the recycling process, opening doors for utilize in bakery, deli, and takeaway applications. As per the European Commission’s Horizon Europe program, significant funding is being allocated to research projects focutilized on creating mono-material paper structures that are easily recyclable yet robust against moisture and oil. This technological leap allows paper bags to replace plastic liners in coffee cups, grease-proof food wrappers, and even liquid carriers, vastly expanding the market scope.

Expansion of E-Commerce and Branded Shipping Solutions

The exponential growth of the e-commerce sector, as online retailers seek sustainable and branded shipping solutions to enhance the unboxing experience, is expected to elevate new opportunities for the growth of the European paper bags market. With the rise of direct-to-consumer models, the package itself has become a critical touchpoint for brand communication, and paper bags offer superior printability and aesthetic appeal compared to standard plastic mailers. According to Eurostat, e-commerce sales in the European Union accounted for 26% of total retail turnover in recent years, creating a massive demand for durable, customizable, and eco-frifinishly shipping packaging. Data from the European E-Commerce Association indicates that online shoppers prefer receiving goods in plastic-free packaging, which is prompting major retailers to switch to reinforced paper sacks and padded paper mailers. As per the Digital Commerce Institute, brands utilizing high-quality paper packaging report higher customer retention rates and increased social media sharing of unboxing experiences. The opportunity lies in developing heavy-duty, tear-resistant paper grades specifically designed for logistics, capable of protecting goods during transit while serving as a canvas for branding.

MARKET CHALLENGES

Complexity of Recycling Streams and Contamination Issues

The complexity of existing recycling streams and the high rates of contamination cautilized by mixed materials and food residue are one of the key challenges for the growth of the European paper bags market. While paper is theoretically highly recyclable, the reality of collection and sorting infrastructure varies widely across European nations, often leading to efficient recovery rates being lower than expected. According to the European Environment Agency, contamination from food waste, grease, and non-paper components like plastic windows or handles rfinishers a significant portion of collected paper bags unfit for recycling, diverting them to incineration or landfill. Data from Waste Management Europe highlights that the lack of harmonized labeling and sorting protocols across member states confutilizes consumers, which is leading to improper disposal behaviors that degrade the quality of the recycled pulp. As per the Confederation of European Paper Industries, the presence of complex barrier coatings, even if bio-based, can sometimes interfere with standard pulping processes if not properly managed, creating technical hurdles for recycling facilities. This infrastructural fragmentation complicates the narrative of paper as a perfectly circular solution, requiring substantial investment in public education and facility upgrades.

Competition from Alternative Bio-Based Materials

The intensifying competition from emerging alternative bio-based materials, such as reusable cloth bags, mushroom packaging, and advanced bioplastics that claim superior durability or lower carbon footprints in specific lifecycle assessments. The competition from alternative bio-based materials is also a challenge for the growth of the European paper bags market. While paper is a mature technology, newer innovations are gaining traction among consumers and regulators who seek solutions that can be reutilized multiple times or degrade rapider in marine environments. According to the European Bioplastics Association, the production capacity for biodegradable plastics in Europe is expanding rapidly, offering a direct substitute for paper in applications where water resistance is crucial. Data from the Sustainable Packaging Coalition suggests that life cycle analyses sometimes favor reusable cotton or jute bags over single-utilize paper bags when considering long-term usage, influencing consumer preferences and corporate procurement policies. As per the European Commission, the focus is shifting towards “reutilize” rather than just “recycling,” which poses a threat to the single-utilize paper bag model. The emergence of mycelium-based packaging and seaweed films further fragments the market, offering niche solutions that appeal to specific eco-conscious demographics. This competitive forces paper manufacturers to continuously innovate and prove their superiority in terms of overall environmental impact, cost, and functionality to maintain their dominant position as the go-to sustainable packaging solution.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

Segments Covered |

By Product Type, Capacity, End-User, and Region. |

|

Various Analyses Covered |

Global, Regional, and Counattempt-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Countries Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

|

Market Leaders Profiled |

Smurfit Kappa Group, Mondi Group, Huhtamaki Oyj, DS Smith Plc, International Paper Company, Billerud AB, WestRock Company, Advanced Industries Packaging, HolwegWeber Group, Riedle GmbH, Baginco International, CEE Schisler Packaging Solutions |

SEGMENTAL ANALYSIS

By Product Type Insights

The flat paper bag segment was the largest by holding 38.4% of the European paper bags market share in 2025, owing to the unparalleled versatility and cost-effectiveness of flat bags, which serve as the standard solution for retail shopping, bakery items, and takeaway food across the continent. The primary factor fueling this domination is the widespread adoption of flat bags by major retail chains and compact businesses alike following the implementation of plastic bag bans, as they offer a simple yet effective canvas for branding and customization. Data from the European Retail Federation indicates that flat bags account for the highest volume of units sold annually becautilize they can be produced at high speeds on automated lines by keeping unit costs low for high-volume applications like grocery and fashion retail. Furthermore, the simplicity of the design allows for simple recycling by consumers, aligning perfectly with waste management goals. As per the European Consumer Organisation, the familiarity and convenience of flat bags create them the preferred choice for shoppers, ensuring consistent demand. Their ability to be manufactured in various sizes and grammages without significant retooling creates them the backbone of the indusattempt, securing their leading status through sheer ubiquity and operational efficiency.

The stand-Up pouch segment is projected to expand at a CAGR of 8.4% inthe coming years with the shifting consumer preference for premium, convenient, and shelf-stable packaging formats in the food and beverage sector, particularly for dry goods, snacks, and pet food. The technological advancement in barrier coatings allows paper stand-up pouches to match the moisture and oxygen protection of plastic laminates, while remaining recyclable or compostable. According to Mintel, product launches featuring paper-based stand-up pouches in the European snack and coffee markets have increased by 35% in the last two years, reflecting a strong trfinish towards sustainable premiumization. Data from the European Flexible Packaging Association reveals that brands are increasingly adopting these pouches to differentiate their products on crowded shelves, as the rigid structure offers superior graphic visibility and a tactile experience that flat bags cannot provide. As per the Ellen MacArthur Foundation, the shift towards mono-material flexible packaging is gaining momentum, and paper stand-up pouches fit this criterion perfectly, attracting investment from major FMCG companies. The ability of these pouches to be resealed and stored efficiently in pantries further enhances their appeal to modern houtilizeholds.

By Capacity Insights

The 1kg to 5 Kg capacity segment was the largest by capturing 45.3% of the European paper bags market share in 2025, with the extensive utilize of bags in this weight range for everyday consumer goods, including flour, sugar, pet food, garden soil, and building materials like plaster. The alignment of this capacity with typical houtilizehold consumption patterns and retail package sizes by creating it the standard unit for both the grocery and DIY sectors across Europe. According to Eurostat, the average European houtilizehold purchases staple dry goods in quantities that fall squarely within this range, driving consistent demand from manufacturers and retailers. Data from the European Construction Indusattempt Federation indicates that a significant portion of construction materials, such as adhesives and grouts, are packaged in 5 kg paper sacks for ease of transport and handling by professional tradespeople and DIY enthusiasts alike. As per the Pet Food Manufacturers Association, the shift towards premium dry pet food has led to a surge in 2 kg to 5 kg paper bag usage, as brands seek to convey quality and sustainability through heavier, more robust packaging. The structural integrity of multi-wall paper bags in this capacity range ensures safe transport without excessive material utilize, offering an optimal balance between strength and cost. This broad applicability across diverse industries cements the 1kg to 5 Kg segment as the core volume driver of the market.

The more than 10 Kg capacity segment is anticipated to grow at a CAGR of 6.9% during the coming years, with the increasing industrial demand for bulk packaging solutions in the agriculture, chemical, and construction sectors, where large volumes of raw materials required efficient and sustainable containment. The regulatory push is to replace woven plastic sacks (FIBCs) and heavy-duty plastic bags with high-strength multi-wall paper sacks for transporting commodities like cement, animal feed, and fertilizers. According to the European Cement Association, the indusattempt is actively transitioning to paper-based bulk packaging to reduce microplastic pollution and improve the recyclability of construction waste streams. Data from the European Feed Manufacturers Federation reveals that the animal feed sector is increasingly adopting large capacity paper sacks for bulk distribution to farms, driven by the required for biodegradable options that minimize environmental impact in rural areas. As per the Confederation of European Paper Industries, advancements in kraft paper strength and layering technologies have enabled paper bags to safely carry loads exceeding 25 kg, competing directly with synthetic alternatives. The logistical advantage of paper sacks, which can be incinerated for energy recovery or recycled more easily than contaminated plastics, further accelerates adoption.

By End-User Insights

The food and beverages segment accounted in capturing 42.3% of the European paper bags market share in 2025, with the required for safe, hygienic, and sustainable packaging for a vast array of edible products, ranging from fresh bakery items and rapid food to dry groceries and confectionery. According to the European Food Safety Authority, paper is recognized as one of the safest materials for direct food contact, provided it meets specific migration limits, fostering trust among manufacturers and consumers. Data from the European Bakery Association indicates that over 90% of artisanal and industrial bakeries now utilize paper bags as their primary packaging medium, citing consumer preference for the “crisp” texture preservation and eco-frifinishly image. As per the Sustainable Restaurant Association, the rise of food delivery services has further boosted demand for grease-resistant paper bags and boxes, with orders for such packaging growing annually. The versatility of paper to be coated with bio-based barriers for wet or oily foods expands its application scope significantly. This deep integration into the daily food supply chain, supported by regulatory mandates and consumer habits, secures the Food and Beverages sector as the largest finish-utilizer of paper bags.

The cosmetics products segment is expected to witness the rapidest CAGR of 9.2% from 2025 to 2034, owing to the luxury and prestige beauty sectors’ aggressive shift towards sustainable packaging to align with brand values and meet the expectations of environmentally conscious consumers. A major driving factor is the perception of paper packaging as a premium, tactile, and ethical choice that enhances brand image and unboxing experiences, particularly for high-finish skincare, fragrance, and createup items. As per reports, product launches in the European cosmetics market featuring “plastic-free” or “recyclable paper” claims have surged by 40%, reflecting a strategic pivot towards fiber-based solutions. As per the European Luxury Goods Association, the aesthetic versatility of paper allows for sophisticated printing, embossing, and finishing techniques that convey luxury better than standard plastic, creating it the preferred medium for gift sets and retail carriers. The trfinish towards refillable systems also relies on durable paper packaging for initial purchases. This alignment with sustainability goals and premium branding ensures that the cosmetics sector will continue to drive disproportionate growth in the paper bags market.

COUNTRY LEVEL ANALYSIS

Germany Paper Bags Market Analysis

Germany was the top performer of thEuropeanpe paper bags market by holding 24.3% of the market share in 2025 due to its robust manufacturing base, strict environmental regulations, and high consumer awareness regarding sustainability. Germany has a mature infrastructure for paper production and recycling, supported by a legal framework that aggressively penalizes plastic usage. The German Packaging Act (VerpackG), which imposes rigorous licensing fees and recycling quotas on producers, incentivizing the switch to easily recyclable paper solutions. According to the German Federal Minisattempt for the Environment, the counattempt achieves a paper recycling rate of over 80%, the highest in Europe, creating a closed-loop system that supports domestic paper bag manufacturing. Data from the German Paper Indusattempt Association indicates that domestic production of kraft paper and specialty grades has increased to meet the surging demand from the retail and food service sectors. As per the German Retail Federation, major supermarket chains eliminated lightweight plastic bags, relying almost exclusively on reusable and single-utilize paper alternatives. The strong presence of automotive and chemical industries also drives demand for industrial paper sacks.

France Paper Bags Market Analysis

The growth of the French paper bags market is driven by pioneering legislation against plastic waste and a strong cultural emphasis on gastronomy and retail aesthetics. The anti-waste law for a Circular Economy (AGEC), which mandates the elimination of single-utilize plastics and promotes reusable or biodegradable packaging, accelerating the adoption of paper bags. The vibrant food service and bakery sector, where the tradition of acquireing fresh bread and pastries daily has seamlessly transitioned from thin plastic to high-quality paper bags that preserve product freshness. According to the French Minisattempt of Ecological Transition, the ban on plastic packaging for fruits and veobtainables has led to an increase in the utilize of paper bags and wraps in supermarkets. Data from the French Confederation of Paper and Cardboard reveals that investments in local paper converting facilities have risen to support the domestic supply chain and reduce reliance on imports. As per the French Federation of Distribution, retailers are increasingly utilizing branded paper bags as a marketing tool to communicate their commitment to sustainability.

Italy Paper Bags Market Analysis

The Italian paper bag market is likely to grow with its world-renowned fashion indusattempt, rich culinary heritage, and growing focus on sustainable tourism. The “Plastic Free” initiative launched by the Italian government, which restricts the utilize of single-utilize plastics in beaches, parks, and retail environments by forcing a rapid shift to paper alternatives. According to the Italian National Institute of Statistics, the fashion and luxury goods sector in the Italian economy predominantly utilizes high-grade paper bags for shopping, viewing them as an extension of brand luxury and quality. As per the Italian Tourism Board, the millions of tourists visiting Italy annually contribute significantly to the consumption of paper bags for souvenirs and food takeaway in historic city centers where plastic is banned.

United Kingdom Paper Bags Market Analysis

The United Kingdom paper bags market is likely to grow in a dynamic retail sector, strong NGO influence, and progressive waste management policies. The UK is evolving rapidly due to the Plastic Packaging Tax and various carrier bag charges that have effectively reshiftd single-utilize plastic bags from mainstream retail, replacing them with paper and reusable options. The active campaigning by environmental groups and the resulting consumer behavioral shift, where British shoppers are among the most likely in Europe to reject plastic packaging. Data from the British Retail Consortium reveals that retailers are investing heavily in FSC-certified paper bags to ensure responsible sourcing and appeal to eco-conscious demographics. As per the Waste and Resources Action Programme, the UK has seen a surge in innovation regarding compostable and recycled content paper bags to meet circular economy tarobtains.

Spain Paper Bags Market Analysis

Spain’s paper bags market growth is likely to grow with its massive tourism indusattempt, vibrant food culture, and increasing alignment with EU sustainability directives. The Royal Decree on single-utilize plastics, which prohibits the distribution of lightweight plastic bags and encourages the utilize of biodegradable or reusable alternatives by boosting paper bag sales. According to the Spanish Minisattempt for the Ecological Transition, the hospitality and food service sector, which serves millions of tourists annually, has adopted paper bags for takeaway food and beachside sales where plastic is strictly forbidden. Data from the Spanish Association of Paper Converters indicates that production capacity for heavy-duty and grease-resistant paper bags has expanded to meet the requireds of the food and construction sectors.

COMPETITIVE LANDSCAPE

The competition in the European paper bags market is characterized by intense rivalry among large integrated paper producers and specialized converters who vie for dominance in a rapidly expanding sector. The market landscape features a mix of multinational corporations with extensive supply chains and regional players focutilizing on niche applications or local service excellence. Differentiation frequently hinges on the ability to offer innovative barrier properties, high strength-to-weight ratios, and superior print quality that meets brand aesthetic standards. Price sensitivity remains a key factor, especially in commodity segments like industrial sacks, forcing companies to optimize production efficiency and logistics costs. Regulatory pressure to eliminate plastics acts as a unifying growth driver yet also raises the bar for compliance and sustainability credentials. The enattempt of new converts attracted by the booming demand adds further complexity, leading to capacity expansions and strategic partnerships to secure long-term contracts.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global europe paper bags market include

- Smurfit Kappa Group

- Mondi Group

- Huhtamaki Oyj

- DS Smith Plc

- International Paper Company

- Billerud AB

- WestRock Company

- Advanced Industries Packaging (AIP)

- HolwegWeber Group

- Riedle GmbH

- Baginco International

- CEE Schisler Packaging Solutions

TOP LEADING PLAYERS IN THE MARKET

- Mondi Group operates as a global leader in packaging and paper solutions with a substantial footprint across the European paper bags market. The company specializes in producing high-performance kraft paper and converting it into diverse bag solutions for retail, food service, and industrial applications. Their contribution to the global market involves setting benchmarks for sustainable foresattempt management and circular economy principles through innovative mono-material designs. Recently, the company has expanded its production capacity in Central Europe to meet surging demand for plastic-free alternatives driven by new EU regulations. They have also launched advanced barrier coatings that enable paper bags to replace plastic in wet food applications without compromising recyclability. These strategic initiatives strengthen their position by offering comprehensive eco-frifinishly portfolios that assist major brands achieve sustainability goals while maintaining product integrity and supply chain reliability across the continent.

- Smurfit Kappa stands as a foremost provider of paper-based packaging solutions with a dominant presence in the European paper bags market through its extensive network of integrated mills and converting plants. The company leverages its closed-loop recycling system to produce strong and versatile paper bags for various sectors, including agriculture, construction, and consumer goods. Their global influence is marked by continuous innovation in design optimization and digital printing technologies that enhance brand visibility on paper packaging. They have also introduced new heavy-duty multi-wall sacks designed to replace woven plastic bags in bulk transport applications. These efforts demonstrate their commitment to replacing single-utilize plastics with robust paper alternatives while ensuring operational efficiency and customer satisfaction throughout the European supply chain.

- BillerudKorsnäs is a leading Swedish company that plays a critical role in the European paper bags market by supplying premium virgin fiber-based papers specifically engineered for demanding packaging requirements. The company focutilizes on developing lightweight yet strong paper grades that reduce material usage while maximizing performance for shopping bags and food service containers. Their global market contribution includes pioneering research into fossil-free manufacturing processes and biodegradable packaging solutions that align with global climate goals. To bolster their market presence, the corporation has recently invested in upgrading its mill facilities to increase the output of extensible paper that offers superior stretch and toughness for bag applications. They have also formed strategic partnerships with major retailers to co-develop custom paper bag solutions that enhance brand image and consumer experience.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the European paper bags market primarily employ strategies focutilized on vertical integration and sustainable innovation to secure competitive advantages. Companies are increasingly investing in their own forest assets and recycling facilities to control raw material costs and ensure a stable supply of certified fiber. Developing advanced barrier technologies that allow paper to replace plastic in moisture-sensitive applications is another major strategy utilized to expand market reach into food and beverage sectors. Participants are also expanding converting capacities through acquisitions and greenfield projects to meet rising demand driven by regulatory bans on single-utilize plastics. Furthermore, firms are leveraging digital printing capabilities to offer customized and short-run packaging solutions that appeal to brands seeking differentiation. These combined approaches allow manufacturers to provide robust, eco-frifinishly alternatives while maintaining cost efficiency and responsiveness to evolving customer requireds.

MARKET SEGMENTATION

This research report on the europe paper bags market is segmented and sub-segmented into the following categories.

By Product Type

- Flat Paper Bags

- Satchel Paper Bags

- Square Bottom Paper Bags

- Stand-Up Pouches

By Capacity

- Less than 1 Kg

- 1 Kg to 5 Kg

- 5 Kg to 10 Kg

- More than 10 Kg

By End-User

- Food & Beverages

- Retail

- Cosmetics

- Pharmaceuticals

- Others

By Counattempt

- Germany

- France

- Italy

- United Kingdom

- Spain

- Rest of Europe

Leave a Reply