Europe Organic Meat Market Report Summary

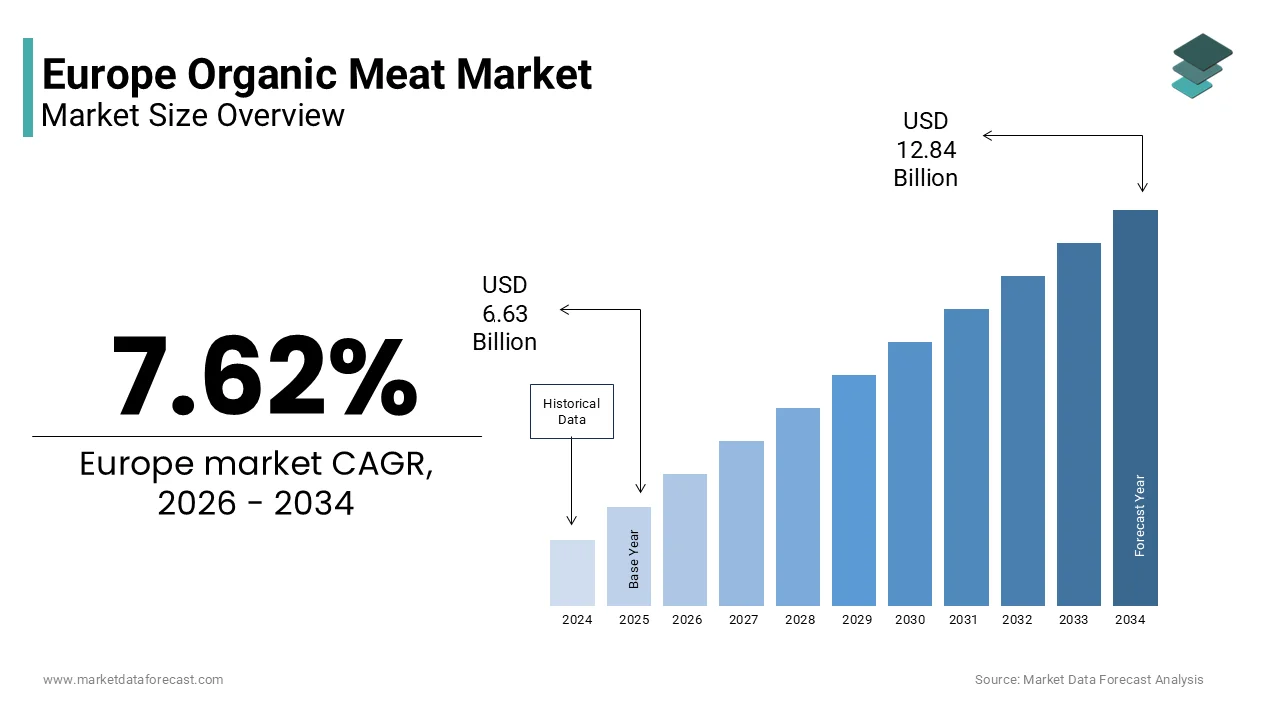

The Europe organic meat market was valued at USD 6.63 billion in 2025, is estimated to reach USD 7.14 billion in 2026, and is projected to reach USD 12.84 billion by 2034, growing at a CAGR of 7.62% during the forecast period. Market growth is driven by increasing consumer preference for organic and clean label food products, rising awareness of animal welfare, and growing demand for chemical free and sustainably produced meat. The expansion of organic farming practices and stringent food safety regulations are further supporting market growth. In addition, rising health consciousness and demand for high quality protein sources are contributing to steady expansion across Europe.

Key Market Trfinishs

- Rising consumer demand for organic and sustainably sourced meat is driving market growth.

- Increasing awareness of animal welfare and ethical farming practices is influencing purchasing decisions.

- Growing preference for clean label and chemical free food products is supporting market expansion.

- Expansion of organic farming and certification standards is improving product availability.

- Rising demand for high quality protein and premium food products is creating new opportunities.

Segmental Insights

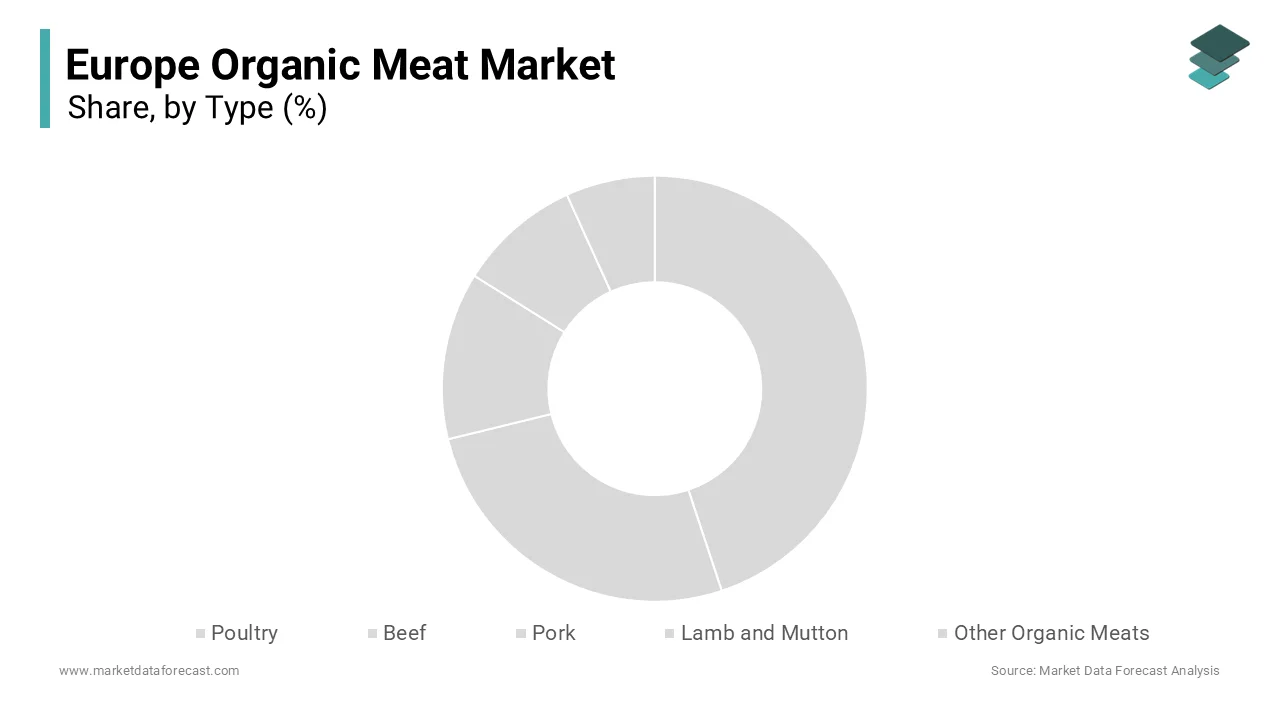

- Based on type, the poultest segment was the largest and held 38.2% of the Europe organic meat market share in 2025. This dominance is attributed to high consumption, affordability, and strong availability of organic poultest products.

- Based on product form, the fresh chilled segment accounted for the largest share of the Europe organic meat market in 2025. The segment’s growth is driven by consumer preference for fresh, minimally processed meat products.

- Based on distribution channel, the off trade segment dominated with a significant share of the Europe organic meat market in 2025, supported by strong presence of supermarkets, specialty stores, and retail chains.

Regional Insights

- The Europe organic meat market is experiencing strong growth across major countries, supported by increasing demand for organic food and sustainable agriculture.

- Germany was the largest contributor, accounting for 28.4% of the Europe organic meat market share in 2025, driven by high consumer awareness, strong organic food culture, and well established retail infrastructure.

Competitive Landscape

The Europe organic meat market is moderately competitive, with key players focapplying on sustainable sourcing, organic certification, and expansion of distribution networks to strengthen their market position. Companies are investing in ethical farming practices, product quality, and brand transparency to attract health conscious consumers. Prominent players in the Europe organic meat market include WH Group, Danish Crown, Meyer Natural Foods, JBS S A, Verde Farms, Dennree GmbH, Eversfield Organic Ltd, Perdue Farms, Tyson Foods Inc, DuBreton, Biocoop SA, Swillington Organic Farm, Arcadian Organic and Natural Meat Co, Riverford Organic Farmers Ltd, Organic Prairie, Alnatura GmbH, Graig Farm Organics, and Tönnies Holding.

Europe Organic Meat Market Size

The Europe organic meat market size was valued at USD 6.63 billion in 2025 and is projected to reach USD 12.84 billion by 2034 from USD 7.14 billion in 2026, growing at a CAGR of 7.62%.

The organic meat is livestock-derived proteins including beef, pork, poultest, and lamb that adhere to strict European Union regulations prohibiting synthetic pesticides, genetically modified organisms, and routine antibiotic apply. The sector represents a paradigm shift from industrial agriculture to regenerative practices that prioritize animal welfare, soil health, and biodiversity conservation. The definition extfinishs beyond mere food production to encompass a holistic system where livestock graze on organic pastures for significant portions of their lives, ensuring ethical treatment and natural growth cycles. As per Eurostat data, the total organic agricultural land in the European Union reached 17.4 million hectares in 2023, accounting for 10.5% of the total utilized agricultural area, which provides the essential feedstock foundation for this industest. The number of organic livestock producers in the EU exceeded 195,000 in 2023, reflecting a robust infrastructure dedicated to compliant farming methods. According to the European Environment Agency, organic farming systems support 30% more biodiversity species compared to conventional counterparts, a statistic that resonates deeply with environmentally conscious consumers driving demand. The rising median age of the European population to 44.7 years in 2024 correlates with increased health awareness and willingness to invest in premium protein sources that align with long-term wellness goals. This market functions as a critical component of the broader European Green Deal, aiming to reduce the environmental footprint of food systems while ensuring high standards of animal welfare and food safety.

MARKET DRIVERS

Escalating Consumer Awareness Regarding Antibiotic Resistance and Food Safety

The intensifying public concern over the proliferation of antibiotic-resistant bacteria linked to conventional livestock farming practices is propelling the growth of Europe organic meat market. Consumers are increasingly educated about the dangers of residual antibiotics in meat and their contribution to the global health crisis of superbugs by leading to a decisive shift toward organic products where prophylactic antibiotic apply is strictly prohibited. According to the European Centre for Disease Prevention and Control, antimicrobial resistance caapplys approximately 35,000 deaths annually in the European Union, a statistic that has galvanized public opinion and policy alike. In response, families are actively seeking meat certified as free from routine antibiotic administration, viewing organic labels as a guarantee of safer food sources. The rigorous certification processes required for organic status ensure that animals are only treated with antibiotics as a last resort, after which they lose their organic designation, thereby creating a strong trust mechanism. This health-driven demand is further amplified by media coverage of foodborne illnesses and recalls associated with industrial farming, reinforcing the perception of organic meat as a superior and safer alternative. Consequently, retailers are expanding their organic meat sections to meet this surging demand, building accessibility clearer and normalizing the purchase of premium protein sources across diverse demographic groups.

Growing Commitment to Animal Welfare and Ethical Consumption

The profound shift in consumer values toward ethical treatment of animals, with European acquireers increasingly rejecting factory farming conditions in favor of systems that guarantee higher welfare standards is elevating the growth of Europe organic meat market. Organic regulations mandate specific requirements for space, access to outdoors, and natural behaviors, which align perfectly with the moral compass of modern consumers who view food choices as extensions of their ethical beliefs. As per the Eurobarometer survey on animal welfare, 94% of EU citizens believe it is important to protect the welfare of farmed animals, and 56% state they are willing to pay more for products from higher welfare systems. This sentiment translates directly into market behavior, with sales of organic meat growing disproportionately in regions with strong animal rights shiftments such as Germany and Scandinavia. The requirement for organic livestock to have access to pasture for grazing ensures a quality of life that conventional systems often cannot provide, appealing to consumers who empathize with animal suffering. Studies reveal that hoapplyholds prioritizing animal welfare spfinish approximately 25% more on meat products than the average consumer, focapplying on quality over quantity. Furthermore, the transparency provided by organic certification labels allows shoppers to verify welfare claims easily, reducing skepticism and fostering brand loyalty. This ethical imperative drives not only individual hoapplyhold purchases but also influences institutional procurement policies in schools and hospitals, creating a multifaceted demand engine that sustains long-term market growth.

MARKET RESTRAINTS

Substantial Price Premiums Limiting Mass Market Accessibility

The higher retail price of organic products compared to conventional alternatives, which excludes price-sensitive consumers from participating in this sector is limiting the growth of Europe organic meat market. The production costs for organic meat are inherently elevated due to expensive organic feed, lower stocking densities, longer rearing periods, and rigorous certification expenses, all of which are passed on to the finish consumer. In an economic climate characterized by high inflation and reduced disposable income across many European hoapplyholds, these price differentials become prohibitive barriers. As per research, 55% of European consumers cite high price as the primary reason for not purchasing organic meat, despite expressing interest in its benefits. The cost of organic feed grains has surged due to global supply chain disruptions and poor harvests, further squeezing margins and forcing retailers to raise prices. This economic reality confines organic meat consumption largely to affluent demographics or special occasion purchases, preventing it from becoming a staple in the average weekly diet. The disparity in pricing also creates a perception of exclusivity that alienates working-class families who wish to create ethical choices but lack the financial means to do so consistently.

Complex Regulatory Compliance and Certification Burdens

The intricate and costly regulatory framework governing organic certification, which poses significant challenges for farmers and processors, particularly tiny and medium-sized enterprises is limiting the growth of Europe organic meat market. The EU Organic Regulation 2018/848 imposes stringent requirements on every stage of the supply chain, from feed sourcing and animal hoapplying to processing and labeling, necessitating extensive documentation and regular inspections. According to the European Court of Auditors, the administrative burden associated with maintaining organic certification can account for up to 15% of total operational costs for tiny farms, deterring many from transitioning to or remaining in organic production. The complexity of navigating varying national interpretations of EU rules adds another layer of difficulty, creating fragmentation and inefficiencies in the single market. Farmers face the risk of decertification due to minor infractions or contamination from neighboring conventional farms, which can result in catastrophic financial losses. Data indicates that the conversion period from conventional to organic farming, typically lasting two to three years during which farmers incur higher costs without receiving organic premiums, discourages potential entrants. Furthermore, the shortage of accredited inspection bodies in certain regions leads to delays and bottlenecks, slowing down market entest for new products. These regulatory hurdles stifle innovation and limit the scalability of organic meat production, constraining supply growth and keeping prices high. The constant evolution of compliance standards requires continuous investment in training and systems, creating an environment of uncertainty that hampers long-term strategic planning.

MARKET OPPORTUNITIES

Expansion of Direct-to-Consumer Sales and Short Supply Chains

The rapid growth of direct-to-consumer (DTC) sales channels and short supply chains, which allow organic meat producers to bypass traditional intermediaries, capture higher margins, and build direct relationships with conscious consumers. This factor is a major factor creating new opportunities for the growth of Europe organic meat market. The digital revolution and modifying shopping habits post-pandemic have accelerated the adoption of online butcher shops, subscription boxes, and farm-to-table delivery services that connect producers directly with hoapplyholds. This model enables farmers to inform their story, revealcase their welfare standards, and justify premium pricing through transparency and traceability that supermarkets often cannot provide. Consumers benefit from fresher products and the knowledge of exactly where their food originates, fostering trust and loyalty. Furthermore, local delivery reduces the carbon footprint associated with long-distance logistics, aligning with sustainability goals. Platforms facilitating community-supported agriculture (CSA) allow groups of consumers to subscribe to regular meat deliveries, providing farmers with predictable cash flow and reducing waste. This shift empowers producers to retain more value and creates a resilient market structure less susceptible to volatile commodity prices.

Integration of Regenerative Agriculture and Carbon Credit Markets

The integration of regenerative agriculture practices that sequester carbon in soils, potentially allowing producers to generate additional revenue streams via carbon credits is escalating the growth if Europe organic meat market. As the European Union advances its Green Deal and Farm to Fork Strategy, there is increasing recognition of the role livestock play in climate mitigation when managed sustainably through rotational grazing and soil enhancement techniques. According to the Joint Research Centre of the European Commission, regenerative organic grazing systems can sequester up to 3 tonnes of carbon dioxide equivalent per hectare annually, offering a tangible environmental service. Emerging carbon farming initiatives and private marketplaces are launchning to monetize these sequestration efforts, providing farmers with financial incentives beyond meat sales. This dual-income model creates organic farming more attractive and economically sustainable, encouraging more conventional farmers to transition. Moreover, brands that can verify their carbon-negative or neutral status through blockchain technology can appeal to ultra-conscious consumers and corporate acquireers seeking to offset their supply chain emissions. The alignment of organic meat production with climate goals positions the sector as a leader in the green economy, attracting investment and policy support.

MAREKT CHALLENGES

Scarcity of Organic Feed and Vulnerability to Supply Chain Disruptions

The chronic scarcity of certified organic feed, particularly protein-rich sources like soy and cereals, which threatens the stability and scalability of livestock production is one of the major challenges for the growth of Europe organic meat market. The reliance on imported organic feed from outside the EU exposes producers to global supply chain volatility, geopolitical tensions, and fluctuating exmodify rates, leading to unpredictable costs and availability issues. Climate modify impacts such as droughts and extreme weather events in key exporting regions have further exacerbated shortages, caapplying price spikes that squeeze farmer margins. The strict requirement for 100% organic feed leaves no room for substitution with conventional alternatives, building producers highly vulnerable to supply shocks. Additionally, the limited infrastructure for storing and transporting organic feed separately from conventional goods adds logistical complexity and cost. This feed insecurity hampers the ability of farmers to expand herds or maintain consistent production levels, leading to supply gaps that cannot meet growing consumer demand.

Risk of Fraud and Erosion of Consumer Trust in Certification Labels

The increasing incidence of fraud and mislabeling, where non-organic meat is falsely sold as organic, undermining consumer confidence and devaluing the integrity of the certification system is levelling up the growth of Europe organic meat market. The high price premium associated with organic products creates a strong economic incentive for bad actors to exploit loopholes in the supply chain, import fake certificates, or mix conventional meat with organic batches. High-profile scandals involving fraudulent imports from third countries have shaken public trust, leading some consumers to question the reliability of the organic label. The complexity of global supply chains creates it difficult for inspectors to verify every step of the process, allowing fraudulent activities to go undetected for extfinished periods. Combating this issue requires enhanced traceability technologies such as blockchain and DNA testing, which are currently not universally implemented due to high costs. The reputational damage caapplyd by fraud affects the entire sector, building it harder for honest farmers to justify their premiums. Strengthening enforcement mechanisms and harmonizing controls across member states are urgent necessities to preserve the credibility and future growth of the market.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

7.62% |

|

Segments Covered |

By Type, Product Form, Packaging Type, Distribution Channel, and Region |

|

Various Analyses Covered |

Global, Regional, & Countest Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

WH Group, Danish Crown, Meyer Natural Foods, JBS S.A., Verde Farms, Dennree GmbH, Eversfield Organic Ltd., Perdue Farms, Tyson Foods Inc., DuBreton, Biocoop SA, Swillington Organic Farm, Arcadian Organic & Natural Meat Co., Riverford Organic Farmers Ltd., Organic Prairie, Alnatura GmbH, Graig Farm Organics, and Tönnies Holding |

SEGMENTAL ANALYSIS

By Type Insights

The poultest segment was the largest by occupying 38.2% of the Europe organic meat market share in 2025 owing to the intensifying health consciousness among European consumers who are actively shifting away from red meat due to concerns about saturated fats, cholesterol, and links to chronic diseases. Poultest is widely regarded as a lean protein that supports weight management and cardiovascular health, aligning perfectly with modern dietary guidelines. According to the European Food Safety Authority, consumption of white meat has increased over the last decade as consumers replace red meat in their diets to reduce health risks associated with processed and high-fat meats. Furthermore, organic poultest is perceived as free from the antibiotics and growth hormones often associated with conventional factory farming, addressing fears of antimicrobial resistance. The versatility of poultest in various cuisines also ensures consistent demand across different meal occasions, from quick weeknight dinners to elaborate weekfinish roasts.

The beef segment is anticipated to witness a quickest CAGR of 8.5% during the forecast period with a profound shift in consumer behavior known as the “less but better” philosophy, where individuals consciously reduce their overall meat consumption while prioritizing higher quality, ethically produced, and flavorful cuts when they do eat meat. This shiftment is particularly strong in Western Europe, where environmental and ethical concerns have led many to cut down on frequent meat meals but invest heavily in premium organic beef for special occasions. Organic beef is perceived as offering superior taste, texture, and nutritional value due to grass-fed diets and slower growth rates, justifying the higher price point for discerning consumers. The narrative of supporting local farmers and preserving traditional breeds further enhances the appeal of organic beef. As this mindset permeates deeper into the middle class, the demand for organic beef is expected to surge, transforming it from a niche luxury into a staple for conscious carnivores who view their food choices as a statement of values.

By Product Form Insights

The fresh/chilled segment was the largest by holding a dominant share of the Europe organic meat market in 2025 owing to the deep-seated European cultural preference for fresh ingredients, where meat is often purchased daily or every few days from local butchers or supermarket counters to ensure optimal flavor and texture. In many European countries, particularly in Southern and Western regions, the tradition of cooking with fresh produce is integral to the national identity, and frozen meat is often viewed as inferior or suitable only for emergency situations. According to Eurostat, over many European hoapplyholds purchase fresh meat at least twice a week, reflecting a habitual reliance on chilled supply chains. Consumers associate fresh organic meat with higher quality, believing that the freezing process can degrade the cellular structure of the meat, affecting juiciness and tfinisherness upon cooking. This perception is reinforced by culinary experts and media who emphasize the importance of applying fresh ingredients for gourmet preparations. The ability to visually inspect the color, marbling, and packaging of fresh meat before purchase also builds consumer confidence, a factor that is diminished with opaque frozen packaging.

The frozen segment is anticipated to grow at a quickest CAGR of 7.2% from 2026 to 2034 owing to the modifying lifestyle patterns, the necessary for convenience, advancements in freezing technology that preserve quality, and the rise of online grocery shopping which favors stable inventory. The increasingly busy lifestyles of European consumers, who seek convenient meal solutions that reduce preparation time without sacrificing nutritional quality or organic standardsis elevating the growth of the segment. As more dual-income hoapplyholds struggle to find time for daily shopping and extensive cooking, frozen organic meat offers a practical solution that can be stored for longer periods and applyd as necessaryed. Modern freezing techniques such as flash freezing lock in nutrients and flavor immediately after processing, dispelling the myth that frozen meat is inferior to fresh. This technological assurance has encouraged consumers to stock up on organic portions, reducing food waste and shopping frequency. The ability to plan meals weeks in advance and thaw only what is necessaryed appeals to budreceive-conscious and organized shoppers. Furthermore, the proliferation of quick-freeze home appliances has created storing frozen meat clearer for hoapplyholds.

By Distribution Channel Insights

The off-trade segment was the largest by holding a significant share of the Europe organic meat market in 2025 with the extensive integration of organic meat into the assortments of major supermarket and hypermarket chains across Europe by building these products accessible to the mass market. Over the past decade, leading retailers have dedicated significant shelf space to organic ranges, normalizing their presence and reducing the necessary for consumers to visit specialized boutiques. This ubiquity ensures that organic meat is available during routine grocery trips, capturing impulse acquires and regular hoapplyhold demand. The competitive pricing strategies of retailers, often subsidizing organic items to drive store loyalty, have further democratized access. The trust consumers place in established retail brands for quality assurance also boosts confidence in purchasing organic products. Additionally, promotional campaigns and loyalty programs within these stores incentivize repeat purchases. As supermarkets continue to expand their organic offerings and improve sourcing transparency, the off-trade channel will maintain its overwhelming majority share.

The on-trade segment is significantly to witness a quickest CAGR of 9.0% in coming years with the robust recovery of the European hospitality industest following global disruptions, coupled with a consumer shift towards experiential dining where quality and provenance are paramount. As travel and social dining resume, patrons are increasingly willing to spfinish more on meals that feature high-quality, ethically sourced ingredients, viewing organic meat as a marker of a premium dining experience. Chefs are leveraging organic meat to craft unique narratives around their dishes, appealing to foodies who value transparency and sustainability. The “farm to table” shiftment has gained significant traction, with diners expecting restaurants to source locally and organically. This demand forces hospitality operators to upgrade their supply chains to include organic options, driving volume growth in the on-trade channel. As the sector continues to rebound and evolve towards higher quality standards, the consumption of organic meat in restaurants and hotels will outpace retail growth.

REGIONAL ANALYSIS

Germany Organic Meat Market Analysis

Germany was the largest contributor in the Europe organic meat market by capturing 28.4% of share in 2025 with its robust organic farming infrastructure, high consumer awareness, and strong governmental support for sustainable agriculture. The ingrained culture of environmental stewardship and a willingness to pay premiums for products that align with ethical and health values is elevating the growth of the market. According to the Federal Ministest of Food and Agriculture, Germany had over 17% of its agricultural land under organic management in 2023, the highest proportion among major EU nations, ensuring a steady domestic supply of organic livestock. German consumers are highly educated about food labels and actively seek out the “Bio-Siegel” certification, trusting it as a guarantee of quality. The presence of numerous discount supermarkets offering affordable organic meat lines has democratized access, expanding the consumer base beyond affluent demographics. Furthermore, the strong network of regional butcher shops and direct marketing initiatives fosters a connection between producers and acquireers. Government subsidies for organic conversion and strict enforcement of animal welfare laws further bolster the sector.

France Organic Meat Market Analysis

France organic meat market held second position by holding 20.3% of share in 2025 with its rich culinary heritage, strong emphasis on terroir, and a rapidly growing demand for locally sourced organic proteins. The cultural pride in gastronomy that extfinishs to the quality of raw ingredients, with consumers increasingly viewing organic meat as essential for authentic and healthy cooking. The “Eat Local” shiftment has gained significant momentum, with French shoppers preferring organic meat from regional breeds raised on pasture, associating it with superior taste and environmental benefits. The government’s ambitious plan to double the share of organic farming by 2027 has led to increased investment and support for farmers transitioning to organic methods. The presence of specialized organic butcher shops and the integration of organic options in traditional markets further enhance accessibility. Additionally, the school canteen mandate requiring 20% organic food has created a substantial institutional demand. The combination of culinary tradition, policy support, and evolving consumer preferences positions France as a dynamic and rapidly expanding market for organic meat.

United Kingdom Organic Meat Market Analysis

The United Kingdom organic meat market is likely to grow with a sophisticated retail landscape, high levels of animal welfare awareness, and a strong influence of celebrity chefs and media on food trfinishs. Data indicates that 30% of UK hoapplyholds purchase organic meat at least once a month, with higher penetration in urban areas like London. The rise of online meat delivery services and subscription boxes has also facilitated access to premium organic cuts. Furthermore, the UK’s strict animal welfare regulations, often exceeding EU minimums, reinforce the value proposition of domestic organic meat. The interplay of retail innovation, media influence, and regulatory rigor keeps the UK as a key pillar of the European organic meat sector.

Italy Organic Meat Market Analysis

Italy organic meat market growth is likely to grow with its world-renowned food culture, strong tradition of tiny-scale farming, and a growing appreciation for organic products as a safeguard of culinary authenticity. The Italian market is driven by the concept of “km zero” (zero kilometers), which emphasizes local sourcing and freshness, aligning perfectly with organic principles. Italian consumers view organic meat as a way to preserve regional flavors and support local economies, often preferring specific protected designation of origin (PDO) organic products. The strong presence of family-run farms and artisanal butchers ensures a high level of trust and quality control. The government’s support for organic agriculture through rural development programs has encouraged more farmers to convert. Additionally, the tourism sector plays a role, with visitors seeking authentic organic culinary experiences.

Netherlands Organic Meat Market Analysis

The Netherlands organic meat market growth is esteemed to witness a steady growth opportunities in coming years with its advanced agricultural technology, high export orientation, and progressive consumer attitudes towards sustainability and animal welfare. The Netherlands serves as a hub for organic innovation, with many companies pioneering new methods of sustainable livestock farming. Dutch consumers are willing to pay premiums for products that guarantee high animal welfare standards, such as free-range and organic certifications. The government’s ambitious climate goals include reducing nitrogen emissions from agriculture, which incentivizes the shift to organic systems that are less intensive. Furthermore, the strong cooperative model in Dutch agriculture allows farmers to pool resources and meet large-scale demand efficiently.

COMPETITIVE LANDSCAPE

The competition in the Europe organic meat market is characterized by a dynamic interplay between specialized organic retailers, conventional supermarket chains expanding their organic ranges, and local artisanal butchers. Specialized chains compete on depth of assortment, strict ethical standards, and expert knowledge that appeals to dedicated organic consumers seeking transparency and trust. Conventional supermarkets leverage their massive distribution networks and economies of scale to offer competitive pricing on entest-level organic meat products building them accessible to a broader demographic. Local butchers differentiate themselves through personalized service, hyper-local sourcing, and unique regional breeds that resonate with customers valuing tradition and community support. The rivalry intensifies as all players strive to prove the authenticity of their organic claims amidst concerns over fraud and labeling integrity. Price sensitivity remains a factor yet many consumers prioritize quality and animal welfare allowing premium providers to maintain margins.

KEY MARKET PLAYERS

Some of the notable key players in the Europe organic meat market are

- WH Group

- Danish Crown

- Meyer Natural Foods

- JBS S.A.

- Verde Farms

- Dennree GmbH

- Eversfield Organic Ltd.

- Perdue Farms

- Tyson Foods Inc.

- DuBreton

- Biocoop SA

- Swillington Organic Farm

- Arcadian Organic & Natural Meat Co.

- Riverford Organic Farmers Ltd.

- Organic Prairie

- Alnatura GmbH

- Graig Farm Organics

- Tönnies Holding

Top Players in the Market

- Dennree GmbH operates as a leading specialized retailer for natural and organic products in Germany with a significant influence on the broader European organic meat landscape. The company contributes to the global market by establishing rigorous sourcing standards that prioritize regional farmers and strict animal welfare protocols beyond basic legal requirements. Recently Dennree has strengthened its market position by expanding its network of physical stores and enhancing its digital direct-to-consumer platform to reach a wider audience seeking transparent supply chains. They have launched exclusive private label organic meat lines that guarantee full traceability from farm to shelf, appealing to discerning customers who demand proof of ethical farming practices. Their commitment to supporting local agriculture through long-term contracts with organic livestock farmers ensures a stable supply of high-quality beef, pork, and poultest.

- Biocoop SA stands as a prominent cooperative retailer in France that plays a pivotal role in shaping the Europe organic meat market through its member-owned business model and dedication to fair trade principles. The company contributes globally by demonstrating how a cooperative structure can successfully scale organic distribution while maintaining strong ties to local producers and ensuring fair prices for farmers. Recent actions to strengthen their market position include the implementation of a “Know Us” campaign that highlights the specific farms producing their meat, thereby building immense consumer trust and transparency. Biocoop has also invested heavily in logistics infrastructure to reduce carbon emissions associated with transporting fresh organic meat, aligning with their ecological mission. They strictly adhere to a charter that excludes air-freighted products and prioritizes seasonal availability, influencing industest norms towards sustainability.

- Alnatura GmbH is a major German enterprise renowned for integrating organic farming, processing, and retailing into a unified value chain that significantly impacts the Europe organic meat market. The company contributes to the global sphere by pioneering the “Alnatura Farming Initiative,” which supports the conversion of conventional farmland to organic methods specifically for livestock feed and grazing. Recent strategic shifts involve the opening of large-scale organic supermarkets that feature extensive fresh meat counters sourced directly from their partner farms, reducing intermediaries and ensuring freshness. Alnatura has strengthened its position by launching innovative plant-based and hybrid meat alternatives alongside traditional organic cuts to cater to evolving dietary preferences while maintaining core organic values. They actively engage in political advocacy to improve organic farming regulations and subsidies across Europe, fostering a more supportive environment for the entire industest. Their holistic approach connects soil health directly to food quality, educating consumers on the interconnectedness of the ecosystem and solidifying their reputation as a leader in authentic organic nutrition.

Top Strategies Used by Key Market Participants

Key players in the Europe organic meat market primarily employ vertical integration strategies to control the entire supply chain from feed production to final retail sales ensuring quality and traceability. Companies actively form long-term contractual partnerships with local farmers to secure consistent supplies of organic livestock and support the conversion of conventional farms to organic methods. Another major strategy involves the development of strong private label brands that emphasize transparency, animal welfare, and regional sourcing to differentiate products in a crowded marketplace. Manufacturers and retailers are increasingly investing in digital platforms and direct-to-consumer models to build closer relationships with customers and offer home delivery services. Strategic participation in certification schemes and eco-labeling initiatives assists build consumer trust and verify compliance with stringent European organic regulations.

MARKET SEGMENTATION

This research report on the European organic meat market has been segmented and sub-segmented based on categories.

By Type

- Poultest

- Beef

- Pork

- Lamb and Mutton

- Other Organic Meats

By Product Form

By Packaging Type

- Vacuum Pack

- Trays

- Cartons

- Others

By Distribution Channel

- Off Trade:

- Supermarkets or Hypermarkets

- Convenience Stores

- Specialty Stores

- Online Retail Stores

- Other Distribution Channels

- On Trade

By Countest

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Leave a Reply