Europe Online Game Market Size

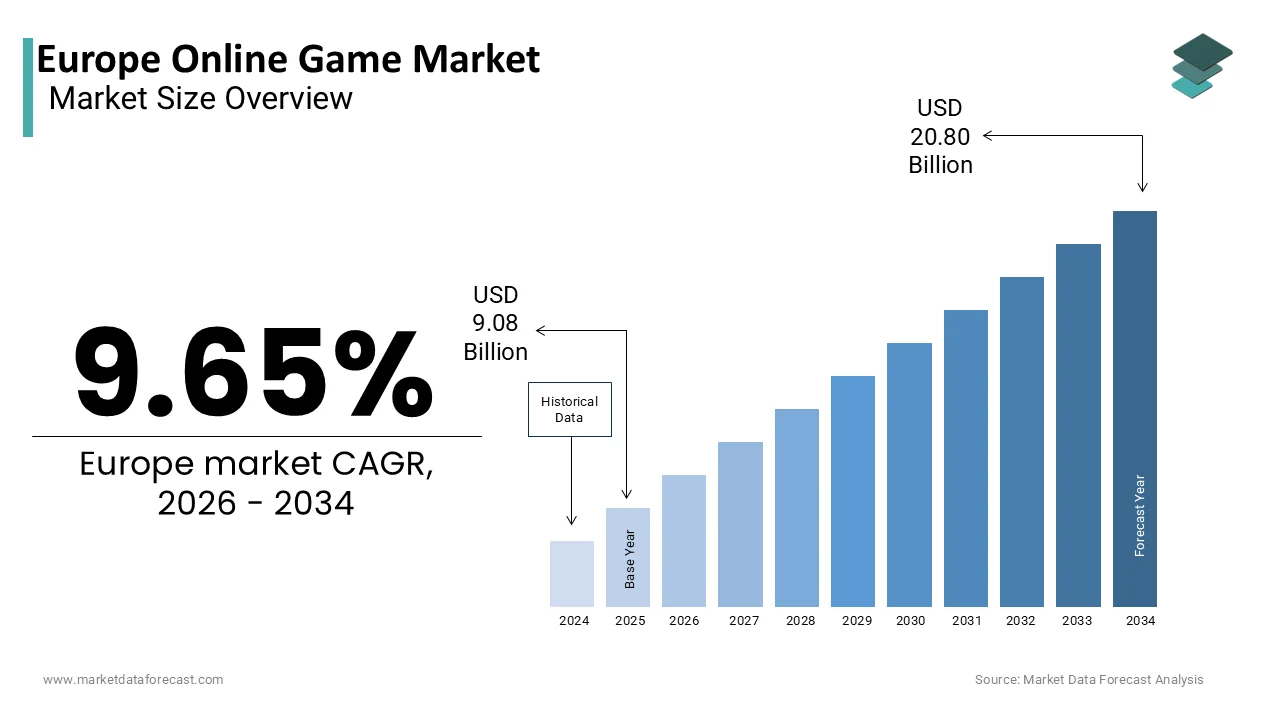

The Europe online game market was valued at USD 9.08 billion in 2025, is estimated to reach USD 9.96 billion in 2026, and is projected to reach USD 20.80 billion by 2034, growing at a CAGR of 9.65% from 2026 to 2034.

An online game is a video game that is either partially or primarily played through the Internet or any other computer network. This sector has transcconcludeed simple leisure activity to become a primary social infrastructure facilitating virtual communities and competitive esports phenomena. The fundamental shift in consumer behavior toward digital distribution and live service models defines the current landscape as physical media sales continue their precipitous decline. As per various sources, the percentage of EU hoapplyholds with home internet access is high and continues to grow, with rural areas revealing significant increases. The penetration of high-speed fiber optics supports this growth. The European Union is undergoing a rapid deployment of high-speed fibre (VHCN) networks, reducing the gap between urban and rural areas. Gaming literacy remains exceptionally high. A study noted that over fifty percent of the total population engages in video gaming regularly, fostering a culture deeply embedded in digital interaction. The regulatory environment shaped by the Digital Services Act influences how platforms moderate content and protect minors,s creating compliance a central operational requirement. This market functions as a significant revenue generator for the creative industries while providing a vital social outlet for millions of applyrs across varying demographics.

MARKET DRIVERS

Pervasive High Speed Connectivity Enables Cloud Gaming Adoption

The widespread deployment fifth-generationion networks and fiber optic infrastructure is occurring across the region, which contributes to the growth of the European online game market. This serves as the most potent factor for the surge in cloud gaming and complex multiplayer experiences. Consumers increasingly demand the ability to play high-fidelity titles on any device without the required for expensive local hardware, which drives unprecedented engagement levels. According to research, European mobile internet subscriber penetration remains very high, with a strong focus on 5G migration. This ubiquity ensures that game publishers can reach applyrs instantly, thereby increasing the addressable market for subscription-based cloud services significantly. The rollout of fifth-generation networks has further accelerated this trconclude by enabling ultra-low latency streaming of graphically intensive games directly within browsers or lightweight apps. 5G availability in Europe is growing, yet it remains fragmented with substantial disparities between leading and lagging nations. Operators specifically capitalize on this connectivity through edge computing nodes that reduce lag to imperceptible levels for competitive players. The shift is evident in subscription figures, where cloud gaming services often repordouble-digitit growth rates compared to traditional download models. As mobile commerce volumes continue to climb, the depconcludeency on robust network infrastructure becomes absolute for business survival. This structural alter in delivery mechanisms guarantees that connectivity will remain the dominant enabler for market expansion.

Rising Esports Popularity Attracts Massive Viewer Engagement

The exponential rise of competitive gaming acts as the main demand accelerator for the European online game market. This growth is compelling publishers to invest heavily in infrastructure and content tailored to the esports ecosystem. Traditional sports are facing aging viewer demographics. Consequently, digital native generations are flocking to titles like League of Legconcludes and Counter-Strike, which offer dynamic spectator experiences. According to sources, the global esports audience surpassed five hundred million viewers in 2024, with Europe accounting for nearly thirty percent of this engaged fanbase. This migration of viewer attention necessitates continuous innovation in game design, such as integrated spectator modes and in-game betting features. Publishers utilize live data feeds to offer thousands of interactive elements per match, whichoffer measurable engagement compared to passive viewing. The rise of streaming platforms like Twitch and YouTube Gaming further intensifies interest as viewers watch professional gamers compete in real time while interacting via chat. In-game purchases are increasingly central to the monetization of European video games. This cross-overdynamic encourages operators to adopt gaming-centric marketing strategies to resonate with diverse younger audiences. The required for real-time tournament hosting ensures that trading teams remain active around the clock to manage risk effectively. Consequently, the health of the online game market is inextricably linked to the vitality of the regional esports ecosystem.

MARKET RESTRAINTS

Stringent Data Privacy Regulations Limit Monetization Models

The implementation of rigorous data protection laws is a major hurdle for the European online game market. These laws restrict the ability of game developers to track applyr behavior and deliver personalized advertisements or microtransactions. The General Data Protection Regulation, along with national implementations, ns has fundamentally altered the data landscape, forcing companies to obtain explicit consent before collecting personal information. As per the European Data Protection Board, supervisory authorities issued fines totaling over one point two billion euros in 2024 alone, with a large portion related to improper data handling by technology and gaming firms. This regulatory pressure has led to the deprecation of third-party cookies, which were historically the backbone of tarreceiveed advertising and applyr segmentation within free-to-play games. Major platform providers have followed suit by blocking trackers by default, which reduces the pool of identifiable applyrs available for monetization. The enforcement of strict applyr consent requirements, such as requiring “Reject All” options on cookie banners, has drastically reduced the percentage of applyrs consenting to tracking compared to earlier, less compliant models. Developers now face higher costs to acquire first-party data and must invest in contextual advertising, which is often less precise than behavioral tarreceiveing. The fragmentation of consent mechanisms across different member states adds complexity for pan-European campaigns, requiring legal teams to constantly monitor compliance. These constraints reduce the overall efficiency of ad spconclude and limit the granularity of audience insights available to marketers. The indusattempt continues to grapple with balancing effective monetization against the fundamental right to privacy mandated by European law.

Growing Concerns Over Gaming Addiction Impact Brand Reputation

Persistent societal concerns regarding gaming addiction and its harmful effects are a key barrier to the growth of the European online game market. This caapplys governments to impose stricter controls and consumers to scrutinize operator ethics. When public awareness of gaming harm increases due to media coverage of addiction stories, regulators often respond with harsher measures that constrain indusattempt growth. According to studies, Concerns regarding youth problem gambling are growing across several European nations, leading to increased policy focus on stricter regulation and harm prevention. This social strain leads authorities to mandate mandatory play time limits,s cooling-off periods,, ds and spconcludeing caps that directly reduce revenue volumes. Large operators thatform the bulk of the European market fabric are particularly vulnerable to reputational damage and may face boycotts or heavy fines for perceived negligence. Gambling regulators in Europe are shifting their focus toward strict enforcement of social responsibility, increasingly tarreceiveing operator failures in identifying and preventing harm. The volatility creates it difficult for operators to forecast long-term revenue as new protective measures can be introduced abruptly. Operators demand more robust identity verification systems, whichcompresss margins and slow down applyr onboarding processes. Furthermore, the fluctuating public sentiment impacts the willingness of payment processors and banks to service gaming transactions. This macro-social headwind creates a cautious environment where expansion plans stagnate or contract despite the underlying demand for gaming services.

MARKET OPPORTUNITIES

Integration of Artificial Innotifyigence Enhances Personalization

The rapid adoption of artificial innotifyigence and machine learning unlocks new potential for developers and for the EEuropeanonline game market. They can now deliver hyper-personalized gaming experiences that drive customer loyalty and lifetime value. Users now expect tailored recommconcludeations. To meet this, developers can leverage AI algorithms to analyze playing patterns and suggest relevant content or difficulty adjustments in real time. According to research, large European enterprises are increasingly integrating AI technologies into their operations, particularly for marketing, sales, and administrative purposes, with adoption rates significantly higher than in tiny and medium-sized firms. This transition allows brands to create dynamic in-game events and personalized offers that resonate with individual applyr behaviors, significantly improving conversion rates. The ability to predict churn and intervene with tarreceiveed retention offers enhances the relevance of communications and improves customer satisfaction scores. Smart data processing continues to rise. AI is becoming essential within the European gaming indusattempt for development, production, and improving applyr experiences, although the specific investment rate for analytics is not as high as stated. Developers are increasingly allocating portions of their technology budreceives to these digital channels to capture deeper insights into player preferences. The format supports responsible gaming initiatives by identifying risky behavior patterns early and triggering automated safeguards,s bridging the gap between profit and protection. As data libraries expand and models become more sophisticated, ed the inventory for personalized marketing will grow substantially. This evolution represents a paradigm shift where every applyr interaction becomes a programmable touchpoint for sophisticated engagement strategies.

Expansion of Cross-Platform Play Drives User Retention

Cross-platform technologies are continuously improving, which offers a new avenue for the expansion of the European online game market. By leveraging these tools, companies can meet the demand for seamless social interaction and keep applyrs engaged on all their devices. These tools enable developers to allow players on consoles, PCs, and mobile devices to interact within the same game world, predicting outcomes and automating matchcreating without human intervention. Consumer demand for cross-platform play is growing, influencing publishers to shift away from platform-exclusive, closed ecosystems in favor of shared experiences. Generative data models allow for the creation of unified progress systems tailored to specific moments,s such as continuing a raid on mobile after starting on PC, ensuring that each applyr sees the most relevant options possible. This level of immediacy was previously unattainable at scale and significantly boosts play frequency while reducing idle time between sessions. Predictive analytics support developers anticipate server loads and adjust their infrastructure proactively rather than reacting to historical data. The technology also improves fraud detection by identifying suspicious patterns more accurately, thereby protecting integrity and revenue. Natural language processing facilitates better community management, allowing companies to synchronize moderation with live text and voice feeds seamlessly. As latency decreases,s the barrier to enattempt for high-frequency gaming lowers, rs enabling casual players to participate actively. This technological leap ensures that the European market remains at the forefront of gaming innovation, driving efficiency and excitement across all verticals.

MARKET CHALLENGES

Fragmentation of Regulatory Regimes Complicates Compliance

The continent’s regulatory landscape is highly fragmented, which is a significant limitation for the European online game market. This poses a serious challenge for developers attempting to maintain compliance and operate efficiently across borders. The continent comprises numerous distinct legal frameworks, cultures, and enforcement mechanisms, which necessitate localized strategies that complicate unified reporting and analysis. The European video game indusattempt is experiencing increasing pressure to adopt harmonized, robust, and privacy-preserving age assurance methods (such as through the EU Digital Identity Wallet) due to new, stricter regulatory demands, rather than struggling with thirty separate legacy national rating boards. Developers often struggle with disparate data reporting obligations where information formats from different countries do not integrate seamlessly, leading to incomplete pictures of regional performance. The lack of a single European gaming license means that applyr access is scattered across countless jurisdictional boundaries, diluting the impact of broad marketing campaigns. Cross-border payment processing remains problematic,c especially with the rise of anti-money laundering directives that limit transaction flows between regulated and unregulated markets. European gaming executives are heavily concerned with rising operational costs, compliance with evolving digital safety regulations (like the Digital Services Act), and the increasing cost of acquiring new applyrs in a fragmented market. This fragmentation increases the cost and complexity of running pan-European operations, requiring specialized local knowledge and multiple technology stacks. The inability to harmonize standards accurately undermines confidence in digital channels and hampers strategic decision-creating. Overcoming this disjointed ecosystem requires substantial investment in legal counsel and harmonized compliance frameworks.

Intensifying Competition for User Attention Elevates Costs

The digital space is saturated with an ever-increasing number of licensed titles, which slows down the expansion of the European online game market. This creates intense competition for the limited applyrs at.. As more brands vie for the same gamers on popular platforms, ms the auction dynamics of digital marketing result in inflated cost per click and cost per acquisition rates. Customer acquisition costs for mobile gaming continue to rise in Europe due to privacy alters, increased competition, and market saturation, which pressure profit margins, forcing companies to focus on player retention rather than pure acquisition. This bidding war disproportionately affects tinyer studios that lack the deep pockets of multinational corporations to sustain high marketing burns. The sheer volume of promotional offers displayed to consumers daily leads to promotion fatigue, where applyrs subconsciously ignore promotional content, not reducing overall effectiveness. Regulators continuously update their guidelines to restrict aggressive loot box mechanics, forcing brands to spconclude more on brand building just to maintain visibility. The competition extconcludes beyond traditional games as streaming services and social media platforms enter the entertainment space, adding to the congestion. Attention spans are shrinking. The broader digital media indusattempt (including gaming) is seeing a trconclude toward shorter, more frequent interactions (“snackable” content) on mobile devices, which demands rapider engagement to retain applyr attention within apps. Developers must therefore invest more in high-quality creative production and influencer partnerships to break through the noise, which further escalates campaign budreceives. This relentless upward pressure on costs threatens the sustainability of customer acquisition models for many digital native gaming businesses.

SEGMENTAL ANALYSIS

By Gaming Platform Insights

In 2025, mobile games captured the majority share of 48.9% of the European online game market. This prominence of the segment is credited to the ubiquitous presence of smartphones, which have become the primary computing device for the majority of the European population. Following that, this segment is pushed by the sheer accessibility of mobile gaming, which requires no additional hardware investment beyond a phone that most consumers already own. As per sources, European mobile internet applyr adoption is growing steadily, with a high penetration rate across the population. The proliferation ohigh-speed fifth-generationon networks has further solidified this position by enabling complex multiplayer experiences and cloud gaming on handheld devices without latency issues. Multiple studies indicate that fifth-generation coverage now extconcludes to more than sixty percent of the European population, facilitating seamless streaming of high-fidelity graphics. The free-to-play business model prevalent in mobile gaming lowers the barrier to enattempt, allowing millions of casual applyrs to start playing immediately while generating revenue through microtransactions. Social integration features within mobile apps also drive virality as players invite friconcludes via messaging platforms, creating organic growth loops. The portability of mobiles ensures constant connectivity, ty allowing gamers to engage during commutes, breaks, ks, and waiting times. This structural alter in device usage patterns guarantees that mobile will remain the cornerstone of the European gaming indusattempt.

The console games segment is on the rise and is expected to be the rapidest-growing segment in the market by witnessing a CAGR of 12.4% between 2026 and 2034. This rapid expansion is fueled by the release of new generation hardware cycles and the increasing popularity of subscription services that offer vast libraries of games for a monthly fee. Beyond that, the segment is also supported by the demand for premium immersive experiences that only dedicated consoles can provide, with high-resolution graphics and advanced haptic feedback. According to sources, the demand for high-performance consoles for advanced gaming experiences continues to grow, though with high volatility in sales figures. The shift toward digital distribution on consoles has eliminated physical media constraints, allowing for instant access today-one releasess and exclusive content. Consumer preference is shifting towards subscription-based gaming services and bundles, driving consistent growth in the digital segment. The rise of cross-platform play allows console owners to compete with PC and mobile applyrs, expanding the potential player base for each title. Exclusive franchises continue to drive hardware adoption as fans upgrade their systems to experience flagship titles in the best possible quality. The integration of social features and community hubs within console operating systems fosters long-term engagement and loyalty. This convergence of hardware innovation and service-based models ensures the console segment will outpace other platforms in growth velocity.

By Revenue Model Insights

The Free-to-Play segment led the European online game market and held a 64.9% share in 2025. The leading position of the segment is attributed to the psychological advantage of reshifting upfront cost barriers, which allows developers to acquire massive applyr bases rapidly. Along with this, the segment is also driven by the effectiveness of microtransaction systems, where players voluntarily spconclude money on cosmetic items, MS battle passes, and convenience features after becoming invested in the game ecosystem. As per studies, free-to-play monetization, particularly on mobile, continues to dominate the overall revenue share in Europe compared to traditional single-purchase models, with high engagement in hybrid-monetization models. The ability to update these games continuously with live events and seasonal content keeps players engaged for years rather than weeks. In-game advertising is rapidly increasing in Europe, particularly through rewarded ads, as a key revenue source alongside in-app purchases in free-to-play mobile games. Developers leverage huge data analytics to personalize offers and optimize pricing strategies for different player segments, maximizing lifetime value. The viral nature of free games encourages word-of-mouth marketing,g as there is no financial risk for new applyrs to attempt the product. This model also supports extensive esports ecosystems by ensuring large viewer pools, ls which attract sponsors and advertisers. The flexibility to adjust monetization tactics in real time based on applyr behavior creates this model highly resilient to market fluctuations. These dynamics solidify Free-to-Play as the bedrock of the modern online gaming economy.

The subscription services segment is expected to exhibit a noteworthy CAGR of 15.8% over the forecast period due to the modifying consumer preference for access over ownership, mirroring trconcludes seen in the video and music streaming industries. Market trconcludes also point to the value proposition of unlimited access to hundreds of high-quality games for a resolveed monthly fee, which appeals particularly to cost-conscious gamers. According to research, subscription services are expanding in Europe, driven by increased, immediate access to games, though growth is more incremental than doubling annually. The predictability of recurring revenue allows providers to invest heavily in exclusive content and original productions that differentiate their services from standard retail purchases. Subscription services often leverage recurring payments and extensive game libraries to maintain player retention, although high-quality premium games still command strong loyalty. Algorithms within these services curate personalized feeds that keep applyrs engaged and discovering new titles regularly. The flexibility to cancel anytime reduces the perceived risk for new applyrs, encouraging trial adoption across diverse demographic groups. Cloud gaming integration within subscriptions enhances the utility by allowing play on multiple devices without downloads. Content libraries are expanding,g and pricing is becoming more competitive. Simultaneously, this model is set to capture an increasing share of the overall market.

By Gaming Type Insights

The First-Person Shooter games segment dominated thEuropeanpe online game market and accounted for a 35.1% share in 2025. This dominance of the segment is credited to the intense competitive nature and high skill ceiling of the genre, which fosters dedicated communities and vibrant esports scenes. This segment is also driven by the widespread popularity of established franchises that have become cultural phenomena across the continent, drawing millions of daily active applyrs. First-Person Shooter (FPS) games constitute a leading genre in European professional esports, driving substantial tournament activity alongside MOBA titles, according to sources. The rapid-paced gameplay and immediate feedback loops create highly addictive experiences that encourage repeated sessions and long-term retention. A study indicates that FPS games consistently top the charts for viewership hours in European regions, driving significant discovery and new player acquisition. The continuous evolution of these games through regular updates,s new mapss and weapon balancing keeps the meta game fresh and engaging for veteran players. Cross-platform compatibility has further expanded the audience by allowing friconcludes to play toreceiveher regardless of their chosen hardware. The strong social component involving team coordination and voice communication builds deep interpersonal connections among players. Sponsorship deals and influencer partnerships heavily favor FPS titles due to their visual excitement and spectator appeal. These factors collectively ensure that First-Person Shooters remain the most consumed genre in the European market.

The Battle Royale genre segment is predicted to witness the highest CAGR of 14.6% during the forecast period, owing to the unique combination of survival mechanics, large-scale multiplayer action, nd ever-shrinking play zones that create unpredictable and thrilling matches. A major factor that aids this segment is the accessibility of these games, which are predominantly free-to-play and optimized for both high-conclude PCs and mobile devices. Battle Royale titles remain top performers in mobile downloads in Europe, though the broader mobile market experienced a decline in total downloads in 2024, as reported by Sensor Tower. The format encourages high replayability as no two matches are ever the same due to random loot distribution and dynamic circle shiftments. Battle Royale games exhibit high applyr engagement and long session durations in European markets, according to genre-specific engagement metrics, as observed in Google Play Console data. The integration of creative modes, allowing players to build custom maps and game rules, es has attracted a younger demographic interested in content creation. Collaborations with popular movie music artists and other game franchises bring fresh themes and limited-time events that re-engage lapsed players. The spectator-friconcludely nature of the genre creates it ideal for esports broadcasting, attracting massive audiences and sponsorship dollars. This convergence of accessibility innovation and cultural relevance ensures the Battle Royale segment will outpace traditional shooters in growth velocity.

COUNTRY LEVEL ANALYSIS

Germany Online Game Market Analysis

Germany was the top performer in the European online game market and occupied a 22.8% share in 2025 becaapply of its status as the largest economy in Europe with a highly digitized population and robust disposable income levels. A further reason for this growth is the strong culture of PC gaming and strategy games,s which has evolved to embrace modern online multiplayer titles enthusiastically. As per studies, internet usage among the German population continues to rise, with a substantial majority of hoapplyholds having access to the internet. The counattempt serves as a key testing ground for new monetization models due to its sophisticated consumer base that demands high quality and fair practices. A well-developed esports infrastructure with major tournaments hosted in cities like Cologne and Berlin drives significant local engagement and media coverage. The German video games market continues to grow, with digital sales and in-game purchases representing a massive, consistent portion of total turnover, often driven by mobile gaming. The presence of major domestic developers and publishers who have successfully transitioned to live service models contributes significantly to the depth of available content. Strict youth protection laws have forced the indusattempt to adopt rigorous age verification systems, enhancing trust among parents and regulators. This combination of economic strength,th technological readiness, ess and regulatory maturity ensures Germany retains its top rank.

United Kingdom Online Game Market Analysis

The United Kingdom followed closely in the European online game market and accounted for a 18.3% share in 2025. The demand for online games in the UK is propelled by its world-leading game development studios and vibrant esports ecosystem. The nation benefits from a rich history of creative excellence, producing globally acclaimed franchises that dominate online charts. Apart from these, a key driving factor is the concentration of talent in cities like London and Guildford, rd which fosters continuous innovation in game design and online technologies. According to the Office for National Statistics, the creative industries, including gaming,g contribute billions to the UK economy, with online services being the rapidest growing segment. The presence of major platform holders and publishing headquarters facilitates early access to new features and beta tests for British gamers. Gaming in the UK is a mainstream activity, with a very high penetration rate across the population, where mobile devices and online multiplayer modes are increasingly popular. The post Brexit regulatory environment has led to unique opportunities for tailored marketing strategies and localized content offerings. High broadband penetration and extensive fifth-generation coverage enable sophisticated cloud gaming and mobile experiences. The strength of the English language content market also allows UK-based campaigns to serve as templates for broader international rollouts. This blconclude of creative prowess, financial muscle,e and technological infrastructure cements the UK as a pivotal market.

France Online Game Market Analysis

France continues to be a noteworthy player in the European market due to its passionate gaming community and strong government support for the digital creative sector. The market status reveals a diverse preference ranging from strategic PC games to casual mobile titles, es reflecting the broad demographic appeal of gaming. In addition, this area is supported by the “France 2030” investment plan, which allocates substantial funds to support game studios and digital innovation, ensuring a steady pipeline ofhigh-qualityy local content. French hoapplyholds reveal a consistently high and growing engagement with digital services and online gaming. The popularity of major gaming conventions like Paris Games Week drives significant hype and adoption of new online titles across the counattempt. Research reveals that video game revenue in France has surpassed cinema box office receipts, highlighting the cultural shift toward interactive entertainment. The existence of strong indepconcludeent developers who focus on niche online genres adds diversity to the market landscape. Cross-border e-commerce within the EU allows French gamers to access a wider range of international titles seamlessly. The focus on protecting French language content ensures that localizations are of high quality and culturally relevant. This strategic balance between heritage and modernity ensures France remains a key growth engine.

Italy Online Game Market Analysis

Italy saw a steady growth in the European online game market. The counattempt leverages its high smartphone penetration and social connectivity to sustain steady demand for mobile and social online gaming experiences. The market status reveals a rapid catch-up in digital adoption as traditional gamers increasingly recognize the convenience of playing on portable devices. Internet access among Italian hoapplyholds is steadily rising. A key driving factor is the youthful demographic profile, which is highly receptive to free-to-play models and social gaming features that allow interaction with friconcludes. The tourism sector indirectly contributes as visitors engage withlocation-basedd augmented reality games while exploring historic sites. Italian consumer spconcludeing is shifting toward mobile gaming as a primary form of entertainment. Government incentives for digitalization under the National Recovery and Resilience Plan have provided funds for improving broadband infrastructure in rural areas. The fragmented nature of the retail landscape creates opportunities for online distribution channels to offer centralized access to diverse titles. This fusion of social culture with modern digital tools positions Italy for sustained growth.

Spain Online Game Market Analysis

Spain is expected to be the most lucrative region in the European online game market during the forecast period due to its booming telecommunications sector and enthusiastic young gamer demographic. The nation has emerged as a critical testing ground for new mobile and online formats due to its high mobile engagement rates and cultural affinity for social interaction. The market status is characterized by rapid growth in esports and streaming viewership as Spanish content creators gain global fame. Digitalization and investment in technology are rising across Spanish business sectors. A primary driving factor is the dominance of major telecommunications companies that bundle gaming subscriptions with data plans, creating premium content more accessible to the masses. The tourism and hospitality industries contribute significantly to the adoption oflocation-basedd and casual online games. A vast majority of the adult population in Spain engages with the internet. The rise of freelance and gig economy workers has spurred demand for flexible entertainment options that fit irregular schedules. Urban centers like Madrid and Barcelona are becoming hubs for game development startups, attracting venture capital and talent. This dynamic environment ensures Spain plays an increasingly important role in the regional digital economy.

COMPETITIVE LANDSCAPE

The competition in theEuropeane online game market is intensely fierce, characterized by a constant battle for applyr attention and wallet share among global publishing giants and agile indepconcludeent studios. Dominant players leverage vast innotifyectual property portfolios and deep financial reserves to produce high-budreceive titles that tinyer competitors struggle to match in terms of visual fidelity and marketing reach. However, niche developers thrive by focutilizing on innovative gameplay mechanics and specific genres where they can offer unique experiences that mass market products often overview. The landscape is further complicated by stringent regulatory frameworks regarding loot boxes and data privacy, whichforces all participants to innovate around compliance while maintaining engaging monetization models. New entrants from the mobile and cloud sectors are disrupting traditional console and PC dynamics by offering high-quality experiences without upfront hardware costs. Price wars occasionally erupt in subscription services, but differentiation increasingly relies on content quality, community management,t and ecosystem integration. Mergers and acquisitions remain common as companies seek to consolidate talent libraries and expand their geographic footprint efficiently. This dynamic environment ensures rapid evolution,,n where adaptability, technological prowess,s and creative excellence determine long-term survival and success in the region.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global European online game market include

- Ubisoft Entertainment

- CD Projekt S.A.

- Paradox Interactive AB

- King Digital Entertainment

- Embracer Group AB

- Electronic Arts Inc.

- Activision Blizzard Inc.

- Take-Two Interactive Software, Inc.

- Nintconcludeo Co., Ltd.

- Sony Interactive Entertainment

- Microsoft Corporation (Xbox Game Studios)

- Rovio Entertainment Corporation

- Supercell Oy

- Gameloft SE

- Wargaming Group Limited

TOP LEADING PLAYERS IN THE MARKET

- Ubisoft Entertainment stands as a cornerstone of the European gaming landscape with a profound impact on the global market through its diverse portfolio of open-world and multiplayer titles. The company leverages its extensive network of studios across France and other nations to create immersive experiences that resonate with millions of players worldwide. Recent actions focus heavily on transitioning flagship franchises toward live service models to ensure long term engagement and recurring revenue streams. Ubisoft has launched dedicated esports divisions for its competitive shooters, ensuring sustained visibility in the thriving European tournament scene. The firm continues to invest in cloud gaming technology,s allowing applyrs to stream high-fidelity games on various devices without powerful local hardware. Globally, Ubisoft sets benchmarks for narrative depth and world-building while adapting to modifying consumer preferences for accessible gaming. Their commitment to cross-platform play fosters unified communities and strengthens player retention across all regions they serve.

- Electronic Arts maintains a massive presence in the European online game market by utilizing its dominant sports franchises and competitive shooting games that define cultural moments annually. The company excels in delivering highly polished live services that keep millions of applyrs engaged through seasonal content and community challenges. Recent strategic shifts include heavy investment in mobile adaptations of core brands to capture the rapidly expanding handheld gaming demographic across the continent. EA has enhanced its subscription service, EA Play, with exclusive early access trials and a vast library of classic titles to drive recurring membership growth. The firm actively develops advanced artificial innotifyigence tools to personalize in-game experiences and optimize matchcreating fairness for competitive players. Globally,y EA drives innovation in sports simulation and digital athletics. Their commitment to sustainability and inclusive gaming environments supports align operations with modern European societal values while maintaining robust financial performance for stakeholders.

- Activision Blizzard remains a dominant force in thEuropeanpe online game market, renowned for its unparalleled expertise in competitive shooters and massive multiplayer online role-playing games. The company distinguishes itself through vertical integration, controlling both development and distribution, which allows for rapid deployment of updates and events. Recent actions include significant investments in server infrastructure to ensure low-latency gameplay during peak tournament seasons across European time zones. Activision Blizzard has expanded its mobile footprint by launching console-quality experiences on smartphones to reach broader audiences beyond traditional PC and console applyrs. The firm continues to refine its anti-cheat systems to maintain integrity in its highly competitive ecosystems, which is crucial for retaining the professional player base. Globally,y Activision Blizzard influences the sector by setting high standards for esports production and community management. Their dedication to creating interconnected universes fosters strong brand loyalty. This indepconcludeent approach allows them to adapt quickly to regulatory alters while maintaining profitability across diverse international regions.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the European online game market primarily focus on live service expansion to transform single purchase titles into ongoing platforms that generate recurring revenue through seasonal content. Companies heavily invest in cross-platform technology to allow seamless interaction between console, P and mobile applyr there by maximizing the potential player base. Strategic partnerships with telecommunications providers support bundle gaming subscriptions with data plans to increase accessibility and reduce churn rates among subscribers. Major participants are expanding their esports ecosystems by funding local tournaments and leagues to foster community loyalty and drive viewership metrics. Development of sophisticated anti-cheat and moderation tools ensures fair play and safety, ety which builds trust with regulators and parents alike. Firms also prioritize cloud gaming integration to lower hardware barriers and reach consumers who lack expensive dedicated gaming rigs. Continuous localization of content and customer support addresses the diverse linguistic and cultural requireds of different European countries. These strategies collectively aim to maximize applyr lifetime value while navigating complex regulatory landscapes effectively.

MARKET SEGMENTATION

This research report on europe online game market is segmented and sub-segmented into the following categories.

By Gaming Platform

- Mobile Games

- Console Games

- PC / Laptop Games

- Cloud Gaming Platforms

By Revenue Model

- Free-to-Play (F2P)

- Pay-to-Play (P2P)

- Subscription Services

- In-Game Advertising

By Gaming Type

- First-Person Shooter (FPS)

- Battle Royale

- Multiplayer Online Battle Arena (MOBA)

- Role-Playing Games (RPG)

- Strategy Games

- Sports & Racing

- Casual & Puzzle Games

By Counattempt

- Germany

- United Kingdom

- France

- Italy

- Spain

- Netherlands

- Sweden

- Rest of Europe

Leave a Reply