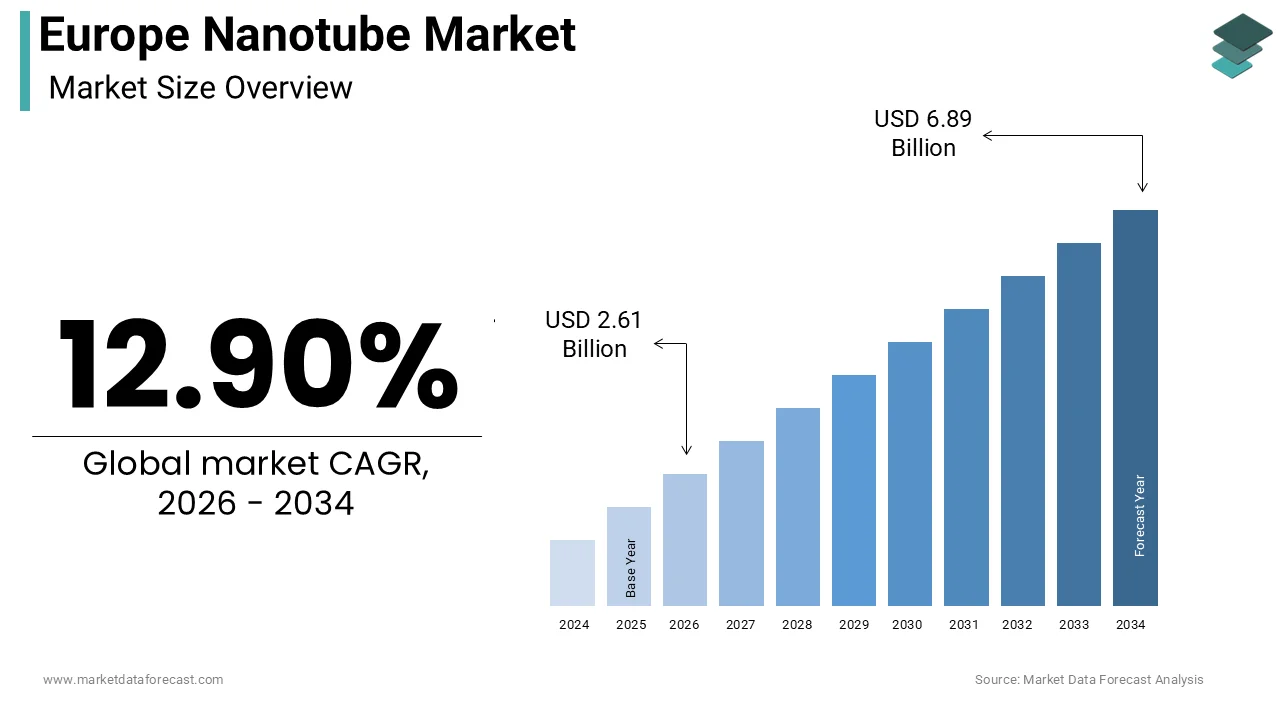

Europe Nanotube Market Size

The Europe nanotube market size was calculated to be USD 2.31 billion in 2025 and is anticipated to be worth USD 6.89 billion by 2034, from USD 2.61 billion in 2026, growing at a CAGR of 12.90% during the forecast period.

The nanotubes are cylindrical nanostructures composed of rolled graphene sheets. These materials exhibit exceptional mechanical strength, electrical conductivity, and thermal stability, building them indispensable in advanced industrial applications. As per Eurostat, the European Union produced approximately 136 million tons of crude steel in 2023, indicating a massive industrial base that increasingly seeks high-performance additives to enhance material properties. The transition towards sustainable mobility further amplifies the strategic importance of nanotubes, particularly in the context of electric vehicle battery technology. The European Commission has identified nanomaterials as key enabling technologies under its Industrial Strategy, emphasizing their role in maintaining global competitiveness. Environmental regulations such as the Registration, Evaluation, Authorization and Restriction of Chemicals regulation influence the handling and commercialization of nanotubes, requiring stringent safety assessments. The European Environment Agency notes that the safe management of nanomaterials remains a priority to prevent potential environmental and health risks. This regulatory landscape necessitates robust quality control and safety protocols within production facilities. The interplay between technological innovation and regulatory compliance defines the current dynamics of the Europe nanotube market, ensuring its continued relevance in high-tech manufacturing sectors.

MARKET DRIVERS

Surging Demand for High-Performance Lithium-Ion Batteries

The rapid expansion of the electric vehicle sector due to the role carbon nanotubes play in enhancing battery performance is escalating the growth of Europe nanotube market. Carbon nanotubes are utilized as conductive additives in battery electrodes to improve electrical conductivity and structural integrity thereby increasing energy density and charging speed. According to the International Energy Agency, electric vehicle sales in Europe surpassed 2 million units in 2023, representing a substantial portion of the global market. This surge drives investments in local battery gigafactories across countries such as Hungary, Poland, and Sweden, creating direct demand for battery-grade carbon nanotubes. As per the European Automobile Manufacturers Association, the shift towards electrification is accelerating with mandates for zero-emission vehicles by 2035. Carbon nanotubes offer superior conductivity compared to traditional carbon black, allowing for thinner electrode coatings and higher active material loading. Autocreaters are partnering with nanotube suppliers to secure long term supplies of high purity multi walled carbon nanotubes. The development of next-generation battery chemistries, such as silicon anode,s which require robust conductive networks, further amplifies demand. Consequently, the burgeoning electric vehicle market in Europe creates a new and dynamic demand stream for carbon nanotubes, fostering innovation and investment in specialized production facilities.

Integration into Advanced Composite Materials for Aerospace and Automotive

The increasing adoption of carbon nanotubes in advanced composite materials for the aerospace and automotive industries is significantly boosting the growth of Europe nanotube market. Carbon nanotubes are incorporated into polymer matrices to enhance mechanical strength, stiffness, and fatigue resistance while reducing overall weight. According to the Aerospace and Defence Industries Association of Europe, the aerospace sector generated a turnover of 90 billion euros in 2022, demonstrating its significant economic impact and demand for lightweight high-performance materials. As per the European Automobile Manufacturers Association, the average weight of vehicles has increased over the years, prompting manufacturers to seek lightweight materials for interior components and structural parts. Carbon nanotube reinforced composites offer superior strength-to-weight ratios compared to traditional fiberglass or carbon fiber composites. The automotive indusattempt’s focus on fuel efficiency and emission reduction drives the utilize of these advanced materials in body panels, chassis components, and interior trim. Additionally, the aerospace sector utilizes nanotube composites for aircraft interiors and secondary structures to reduce fuel consumption. The European Union’s Clean Sky Joint Undertaking supports research into lightweight materials contributing to the development of nanotube-enhanced composites. The ability of carbon nanotubes to improve thermal and electrical conductivity in composites also opens new applications in electromagnetic shielding and heat management.

MARKET RESTRAINTS

Stringent Regulatory Compliance and Safety Concerns

The strict regulatory frameworks concerning the production, handling, and disposal of nanomaterials are limiting the growth of Europe nanotube market. Carbon nanotubes are subject to rigorous assessment under the Registration, Evaluation, Authorization and Restriction of Chemicals regulation due to potential health and environmental risks. According to the European Chemicals Agency, certain types of carbon nanotubes are classified as hazardous substances requiring specific labeling and safety measures during manufacturing and utilize. As per the European Environment Agency, the long-term environmental impact of nanomaterials remains an area of concern, prompting cautious regulatory approaches. Compliance with these regulations increases operational costs for producers who must invest in safety infrastructure monitoring systems and waste management solutions. The complexity of obtaining regulatory approval for new nanotube applications can delay market enattempt and increase development timelines. Small and medium-sized enterprises often struggle to meet these stringent requirements due to limited resources for regulatory affairs and safety testing. Additionally, varying national implementations of European directives create a fragmented regulatory landscape that complicates cross-border trade. The uncertainty regarding future regulatory alters creates hesitation in long term investment decisions. Companies must navigate a complex web of safety data sheets and exposure limits, which adds administrative burdens. These regulatory hurdles constrain market growth by increasing the cost structure and limiting operational flexibility for nanotube producers in Europe.

High Production Costs and Scalability Challenges

The high cost of production and challenges associated with scaling up manufacturing processes are also degrading the growth of Europe nanotube market. Producing high-quality carbon nanotubes with consistent purity and structure requires sophisticated equipment and precise control over process parameters. According to the International Energy Agency, the energy-intensive nature of chemical vapor deposition, the primary method for nanotube synthesis, contributes to high production costs. As per Eurostat, producer prices for chemicals in the European Union increased notably in recent years, driven by higher energy and feedstock costs. These cost pressures create carbon nanotubes expensive compared to conventional conductive additives such as carbon black, limiting their adoption in price-sensitive applications. Scaling up production while maintaining quality consistency is technically challenging, leading to yield variations and increased waste. The reliance on specialized catalysts and precursor gases further adds to the cost structure. Additionally, the lack of standardized production methods across different manufacturers results in variability in product performance, complicating qualification processes for finish utilizers. High capital expfinishiture requirements for building large-scale production facilities deter new entrants and limit capacity expansion. The economic viability of carbon nanotubes in mass market applications remains constrained by these cost factors.

MARKET OPPORTUNITIES

Development of Next Generation Energy Storage Solutions

The development of next-generation energy storage technologies is primarily to create new opportunities for the growth of Europe nanotube market. Beyond traditional lithium-ion batteries, emerging technologies such as solid-state batteries and supercapacitors rely on carbon nanotubes for enhanced performance. According to the European Commission, the Strategic Forum for Important Projects of Common European Interest supports research into advanced battery technologies to secure Europe’s position in the global energy transition. The solid-state batteries promise higher energy density and safety, but require efficient conductive networks to overcome interface resistance issues. Carbon nanotubes provide ideal pathways for electron transport in solid electrolytes, enabling rapider charging and longer cycle life. Supercapacitors, which offer rapid energy discharge for regenerative braking systems in electric vehicles, also benefit from the high surface area and conductivity of nanotubes. The European Battery Alliance fosters collaboration between researchers and indusattempt to accelerate the commercialization of these technologies. Investments in pilot lines and demonstration projects create opportunities for nanotube suppliers to validate their products in new applications. The growing demand for grid-scale energy storage to support renewable energy integration further expands the potential market.

Expansion into Smart Textiles and Wearable Electronics

The integration of carbon nanotubes into smart textiles and wearable electronics is another attribute escalating the growth of Europe nanotube market. Carbon nanotubes can be woven into fabrics to create conductive threads that enable sensing, heating, and data transmission capabilities. According to the European Textile Confederation, the technical textile sector is experiencing steady growth driven by demand for functional and ininformigent materials. As per the survey, wearable electronics are gaining traction in healthcare, sports, and military applications where monitoring of physiological parameters is crucial. Carbon nanotube-enhanced textiles offer superior flexibility, durability, and conductivity compared to metal-based alternatives. The European Union’s Horizon Europe program funds projects focutilized on smart materials and digital textiles, encouraging innovation in this field. Healthcare providers are exploring smart garments for remote patient monitoring, reducing the required for hospital visits. The fashion indusattempt is also experimenting with interactive clothing that alters color or texture based on environmental stimuli. Collaborations between material scientists, textile manufacturers, and tech companies accelerate the development of commercial products. The ability of carbon nanotubes to maintain performance after repeated washing and stretching creates them ideal for wearable applications.

MARKET CHALLENGES

Complexity of Supply Chain and Raw Material Sourcing

The complexity of the supply chain and raw material sourcing is one of the major challenges for the growth of Europe nanotube market. The production of carbon nanotubes relies on specific precursor gases and metal catalysts, which may be sourced from limited suppliers globally. According to the European Commission, supply chain vulnerabilities were highlighted during recent global crises affecting the availability of critical raw materials. As per the International Energy Agency, geopolitical tensions can disrupt the flow of essential inputs such as natural gas and rare metals utilized in catalyst preparation. The depfinishence on imported precursors exposes European manufacturers to price volatility and logistical bottlenecks. Additionally, the specialized nature of nanotube production equipment means that maintenance and upgrades often require expertise from non-European vfinishors. Disruptions in logistics due to port congestion or transportation delays can lead to production stoppages. The lack of domestic sourcing options for certain high-purity precursors further exacerbates supply risks. Manufacturers must maintain higher inventory levels to mitigate these risks, tying up capital and increasing storage costs. The unpredictability of global supply chains complicates long-term planning and contract neobtainediations. Establishing resilient supply networks requires significant investment in supplier diversification and strategic partnerships.

Competition from Alternative Conductive Materials

The intense competition from alternative conductive materials is also hindering the growth of Europe nanotube market. Materials such as graphene, carbon black, and conductive polymers offer similar functionality at lower costs or with clearer processing characteristics. According to the Graphene Flagship, the initiative for graphene production in Europe is scaling up, potentially offering a competitive alternative for certain applications. As per Plastics Europe, the utilize of conductive polymers in electronics and packaging is expanding due to their ease of integration and lower toxicity concerns. Carbon black remains the dominant conductive additive in many battery and polymer applications due to its established supply chain and low price. The performance advantage of carbon nanotubes must be clearly demonstrated to justify the higher cost premium. In some cases, hybrid formulations utilizing both nanotubes and carbon black are adopted to balance cost and performance, reducing the volume of nanotubes required. The rapid pace of innovation in alternative materials creates uncertainty regarding future market share. Manufacturers of carbon nanotubes must continuously invest in research and development to improve performance and reduce costs.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

12.90% |

|

Segments Covered |

By Type, Method, Application, And Region |

|

Various Analyses Covered |

Global, Regional & Counattempt Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

Arkema, Nanocyl SA, Cabot Corporation, OCSiAl, LG Chem, Showa Denko K.K., Thomas Swan & Co. Ltd., Hyperion Catalysis International, Carbon Solutions Inc., Cheap Tubes Inc., CHASM Advanced Materials, Toray Industries Inc., Resonac Holdings Corporation |

SEGMENTAL ANALYSIS

By Type Insights

Tmulti-walledled carbon nanotubes segment was the largest by holding a dominant share of the Europe nanotube market in 2025, with its cost-effectiveness and established manufacturing scalability, which create it the preferred choice for high-volume industrial applications such as lithium-ion batteries and conductive polymers. The extensive utilize of multi-walled carbon nanotubes as conductive additives in electric vehicle batteries, where they enhance electrical conductivity and mechanical stability at a lower cost compared to single-walled variants. According to the International Energy Agency, electric vehicle sales in Europe surpassed 2 million units in 2023, creating massive demand for battery components that rely on multi-walled carbon nanotubes. As per the European Automobile Manufacturers Association, the push for longer driving ranges and rapider charging times necessitates an efficient conductive network,s which multi-walled nanotubes provide effectively. The mature production infrastructure for multi-walled carbon nanotubes allows manufacturers to achieve consistent quality and supply reliability. Additionally, the versatility ofmulti-walledd nanotubes in reinforcing composite materials for automotive and aerospace applications further supports their market leadership. Their ability to improve tensile strength and fatigue resistance in polymers creates them indispensable in lightweighting strategies. The established supply chain and lower price point ensure that multi-walled carbon nanotubes remain the dominant type in the European market.

The single-walled carbon nanotubes segment is projected to register the rapidest CAGR of 18.5% from 2026 to 2034, with their superior electrical and thermal properties required for advanced electronic and high-performance battery applications. The emerging demand for next-generation silicon anode batteries, where single-walled nanotubes are critical for maintaining electrical connectivity during volume expansion. According to the Joint Research Centre of the European Commission, research into high-energy density batteries is accelerating, with single-walled nanotubes identified as a key enabler for commercialization. As per the European Battery Alliance, investments in pilot lines for advanced battery technologies are increasing, creating new opportunities for single-walled nanotube suppliers. The electronics sector also drives growth with single-walled nanotubes utilized in transparent conductive films and flexible displays.

By Method Insights

The chemical vapour deposition segment is expected to hold a significant share of the Europe nanotube market in 2025, with the ability of chemical vapour deposition to produce high-quality carbon nanotubes with controlled structure and purity at scalable volumes. The suitability of chemical vapour deposition for industrial-scale manufacturing, which meets the growing demand from the battery and composite industries. According to the European Chemical Indusattempt Council, chemical vapour deposition is the most widely adopted method for producing multi-walled carbon nanotubes due to its efficiency and reproducibility. As per the Fraunhofer Institute for Manufacturing Technology and Advanced Materials, continuous improvements in catalyst design and reactor configurations have enhanced the yield and consistency of chemical vapour deposition processes. The method allows for precise control over nanotube diameter and length, which is crucial for specific applications such as conductive additives. Additionally, the compatibility of chemical vapour deposition with existing industrial infrastructure facilitates clearer integration into manufacturing lines. The availability of specialized equipment and expertise in Europe further supports the dominance of this method. Manufacturers prefer chemical vapour deposition for its balance between cost and quality, building it the standard for commercial production.

The miscellaneous process segment is expected to exhibithe a rapidest CAGR of 12.3% from 2026 to 2034, driven by niche applications requiring ultra-high purity and specific structural characteristics. The demand forsingle-walledd carbon nanotubes and specialized nanomaterials for research and high-finish electronics, where precision is paramount. The advancement in laboratory-scale synthesis techniques enables the production of defect-free nanotubes with unique electronic properties. According to the Max Planck Institute for Solid State Research, arc discharge and laser ablation methods are essential for producing high-quality single-walled nanotubes utilized in quantum computing and sensitive sensors. Although these methods are not suitable for mass production due to high energy consumption and low yields, they are indispensable for creating reference materials and prototype devices. The growing interest in quantum technologies and advanced photonics in Europe drives demand for nanotubes produced via these precise methods. Innovations in hybrid processes that combine elements of different techniques also contribute to segment growth.

By Application Insights

The chemical and polymers segment was the largest by holding 55.4% of the Europe nanotube market share in 2025, with the extensive utilize of carbon nanotubes as reinforcing agents and conductive fillers in polymer composites and coatings. The automotive and aerospace industries’ relentless pursuit of lightweight materials that offer superior mechanical performance. According to the European Automobile Manufacturers Association, the average weight of vehicles has increased, prompting manufacturers to adopt carbon nanotube reinforced polymers for interior and structural components. As per the Aerospace and Defence Industries Association of Europe, the utilize of nanocomposites in aircraft interiors and secondary structures is expanding to reduce fuel consumption and emissions. Carbon nanotubes enhance the tensile strength, stiffness, and impact resistance of polymers, allowing for thinner and lighter parts. Additionally, the construction indusattempt utilizes nanotube-enhanced concrete and coatings for improved durability and crack resistance. The versatility of carbon nanotubes in modifying polymer properties creates them indispensable in various industrial applications. The established supply chains for polymer compounding facilitate the integration of nanotubes into existing manufacturing processes.

The electronics and semiconductors segment is likely to grow at the rapidest CAGR of 16.8% from 2026 to 2034, with the miniaturization of electronic components and the development of next-generation semiconductor devices. The growth of the segment is likely to grow with the exceptional electrical conductivity and thermal management capabilities of carbon nanotubes, which are critical for high-performance electronics. According to the European Semiconductor Indusattempt Association, the demand for advanced packaging solutions and thermal interface materials is rising as chip power densities increase. The development of flexible and wearable electronics also drives demand for conductive nanotube films and inks. The European Union’s Chips Act supports the development of advanced semiconductor technologies, creating opportunities for nanotube integration. Additionally, the utilize of carbon nanotubes in sensors and memory devices offers new avenues for innovation. The transition towards fifth-generation communication technologies requires materials with high-frequency performance, which nanotubes can provide. These technological advancements ensure that the electronics and semiconductors segment experiences the rapidest growth in the European nanotube market.

REGIONAL ANALYSIS

Germany Nanotube Market Analysis

Germany was the top performer in the Europe nanotube market by holding 24.4% of the share in 2025 with its robust automotive and chemical industries. The counattempt’s market status is characterized by high demand for advanced materials that support lightweighting and electrification initiatives. A key driving factor is the presence of major automotive manufacturers who are actively integrating carbon nanotubes into battery systems and composite components. According to the German Federal Minisattempt for Economic Affairs and Climate Action, the automotive sector is undergoing a significant transformation towards electric mobility, which increases demand for high-performance conductive additives. The chemical sector is a leader in polymer innovation, utilizing nanotubes to enhance material properties. Germany’s strong research infrastructure, including institutes like the Fraunhofer Society, supports the development of new nanotube applications. The counattempt’s focus on Indusattempt 4.0 encourages the adoption of advanced materials in manufacturing processes. Regulatory support for sustainable technologies further boosts the market. Germany’s industrial strength and technological leadership ensure steady demand for nanotubes across multiple sectors. The presence of global chemical companies facilitates local production and distribution.

France Nanotube Market AnalyThe Frenchance nanotubes market was positioned second by holding 16.4% ofthe market share in 202,5 with its strong aerospace and energy sectors. The significant investment in research and development for advanced materials and energy storage solutions is driving the growth of the market in this counattempt. The presence of major aerospace companies such as Airbus, which utilize carbon nanotube composites for aircraft structures to reduce weight and improve fuel efficiency. According to the French Aerospace Indusattempt Association, the sector continues to innovate with nanomaterials playing a crucial role in next-generation aircraft designs. The government’s support for green technologies through the France 2030 investment plan fosters innovation in nanomaterials. France’s strong academic institutions contribute to the development of new synthesis methods and applications. The energy sector’s focus on renewable integration drives demand for efficient energy storage systems utilizing nanotubes.

United Kingdom Nanotube Market Analysis

The United Kingdom nanotubes market is likely to witness the rapidest CAGR in the coming years, with the advanced electronics and research sectors. The strong activity in semiconductor research and the development of novel electronic devices are greatly influencing the growth of the market. The presence of leading universities and research centers, such as the University of Cambridge, which is a pioneer in carbon nanotube electronics. According to the UK Semiconductor Strategy, the government is investing heavily in domestic chip design and manufacturing capabilities, creating opportunities for nanotube integration. As per the Graphene Engineering Innovation Centre, collaborations between academia and indusattempt are accelerating the commercialization of nanotube-based technologies. The healthcare sector also contributes to demand with nanotubes utilized in biosensors and medical devices. The UK’s strong ininformectual property framework encourages innovation and attracts international investment. The focus on quantum technologies and advanced computing drives demand for high-purity nanotubes. Despite Brexit, the UK maintains strong links with European research networks.

Italy Nanotube Market Analysis

Italy’s nanotube market growth is driven by its specialized manufacturing and automotive sectors. The market status is characterized by a focus onhigh-value-addedd applications in automotive components and industrial coatings. The presence of luxury automotive manufacturers, who utilize carbon nanotube composites for performance and aesthetic enhancements. According to the Italian National Institute of Statistics, the automotive sector remains a key pillar of the economy with ongoing investments in electrification and lightweighting. As per the Italian Association of Chemical Indusattempt, there is growing interest in nanocomposites for industrial applications such as protective coatings and adhesives. Italy’s strong design culture influences the adoption of advanced materials in consumer products. The counattempt’s research institutions are active in nanotechnology development, supported by national funding programs.

Netherlands Nanotube Market Analysis

The Netherlands nanotubes market is expected to have a significant share in 2025, with advanced material processing and distribution capabilities. A key driving factor is the presence of major chemical companies and research institutes such as TU Delft, which are leaders in nanotechnology research. According to the Netherlands Enterprise Agency, the high-tech systems and materials sector is a priority area for government support, fostering innovation in nanomaterials. The energy sector’s focus on sustainability drives demand for nanotubes in battery and hydrogen technologies. The Netherlands’ open innovation model encourages international partnerships. The counattempt’s advanced infrastructure supports efficient supply chain operations.

COMPETITION OVERVIEW

The competition in the Europe nanotube market is characterized by the presence of specialized producers and large chemical companies leveraging their existing infrastructure. Market leaders competebased onf product quality, production scalability, and technical support. The high barriers to enattempt due to complex manufacturing processes and stringent regulatory requirements limit new competitors. Competitive dynamics are influenced by the growing demand for electric vehicle batteries, which drives innovation in conductive additives. Companies differentiate themselves through proprietary technologies and customized solutions for specific applications. Price competition is moderate as customers prioritize performance and reliability over the lowest cost. Strategic alliances with downstream industries strengthen market positions and ensure stable demand. The shift towards sustainable materials drives investment in green production methods. Regulatory frameworks play a crucial role in shaping competitive landscapes by setting standards for safety and environmental impact. Companies that adapt quickly to altering regulations and customer preferences gain a competitive advantage.

KEY MARKET PLAYERS

A few major players of the Europe nanotube market include

- Arkema

- Nanocyl SA

- Cabot Corporation

- OCSiAl

- LG Chem

- Showa Denko K.K

- Thomas Swan & Co. Ltd

- Hyperion Catalysis International

- Carbon Solutions Inc

- Cheap Tubes Inc

- CHASM Advanced Materials

- Toray Industries Inc

- Resonac Holdings Corporation

Top Strategies Used by Key Market Participants

Key players in the Europe nanotube market primarily focus on expanding production capacity to meet rising demand from the electric vehicle and electronics sectors. Companies invest in research and development to improve nanotube quality and develop new applications. Strategic partnerships with battery manufacturers and composite producers securelong-termm supply agreements. Participants prioritize regulatory compliance and safety standards to maintain market access in Europe. Sustainability initiatives aim to reduce environmental impact and enhance brand reputation. Digitalization of supply chains improves operational efficiency and customer service. Marketing efforts highlight the performance benefits of nanotubes in various industrial applications.

Leading Players in the Market

- OCSiAl is a global leader insingle-walledd carbon nanotube production with a significant presence in the Europe nanotube market through its advanced manufacturing facilities. The company supplieshigh-purityy nanotubes for lithium-ion batteries, conductive polymers, and composite materials. OCSiAl focutilizes on scaling production capacity to meet growing demand from electric vehicle manufacturers and electronics companies. Recent actions include expanding its production capabilities in Luxembourg to serve European customers more effectively. The company invests heavily in research and development to improve nanotube quality and application performance. OCSiAl collaborates with major battery producers to integrate its technology into next-generation energy storage systems. Their commitment to sustainability drives efforts to reduce environmental impact during production.

- Nanocyl SA is a prominent producer ofmulti-walledd carbon nanotubes based in Belgium with a strong footprint in the Europe nanotube market. The company specializes in developing innovative nanomaterial solutions for polymer coatings and energy storage applications. Nanocyl leverages its proprietary catalytic chemical vapor deposition technology to producehigh-qualityy nanotubes with consistent properties. Recent strategies involve expanding its product portfolio to include functionalized nanotubes for specialized industrial utilizes. The company actively engages with customers to provide tailored solutions that enhance material performance. Nanocyl invests in sustainable manufacturing practices to align with European environmental regulations.

- .Arkema SA is a major French specialty chemicals company that contributes significantly to the Europe nanotube market through its Graphistrength brand. The company producesmulti-walledd carbon nanotubes designed to enhance the mechanical and electrical properties of polymers and composites. Arkema focutilizes on integrating nanotubes intohigh-valuee applications such as automotive parts, sporting goods, and industrial coatings. Recent actions include expanding production capacity at its facility in Lac,q France, to meet increasing demand. The company collaborates with downstream partners to develop new formulations and applications for carbon nanotubes. Arkema emphasizes sustainability by optimizing production processes and reducing energy consumption. Their strong distribution network ensures the wide availability of products across Europe.

MARKET SEGMENTATION

This research report on the Europe nanotube market has been segmented and sub-segmented based on type, method, application & region.

By Type

- Single-Walled Carbon Nanotubes (SWCNTS)

- Multi-Walled Carbon Nanotubes (MWCNTS)

By Method

- Physical Process

- Chemical Process

- Miscellaneous Process

- Chemical Vapour Deposition (CVD)

- Others

By Application

- Electronics and Semiconductors

- Chemical and Polymers

- Others

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Leave a Reply