Europe Modular Construction Market Size

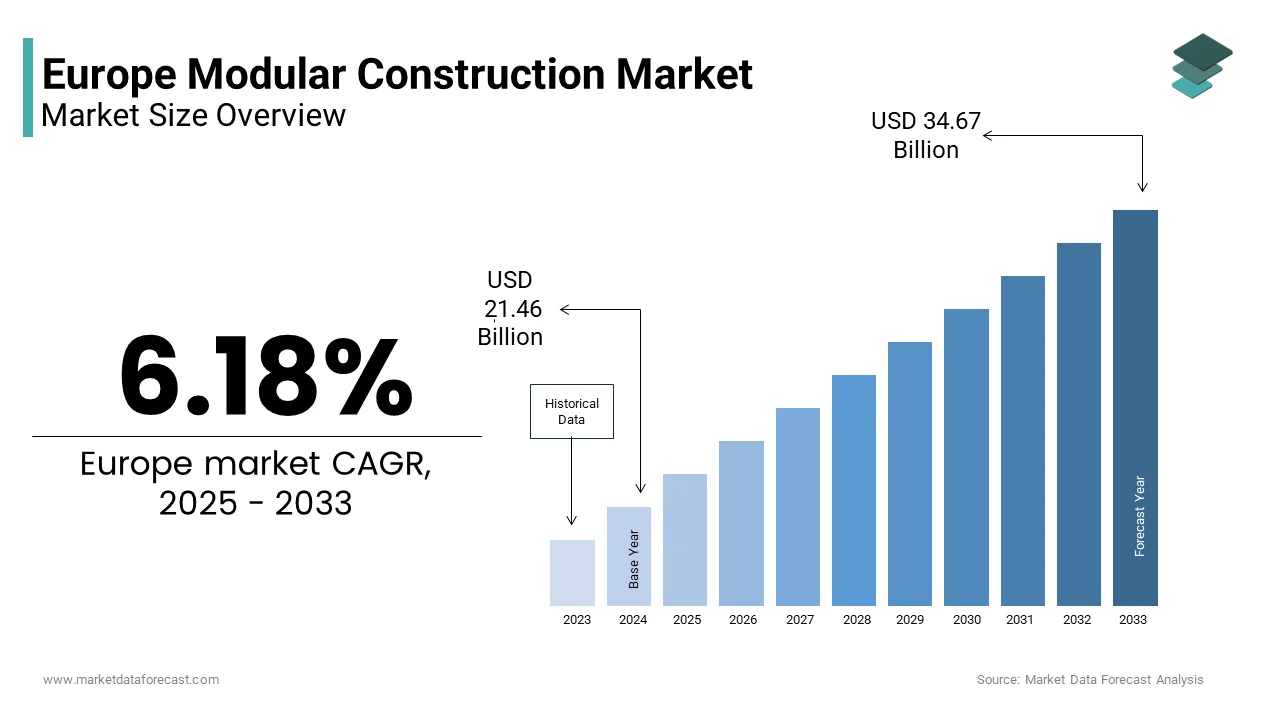

The Europe modular construction market size was valued at USD 20.21 billion in 2024 and is anticipated to reach USD 21.46 billion in 2025 to USD 34.67 billion by 2033, growing at a CAGR of 6.18% during the forecast period from 2025 to 2033.

Modular construction refers to an off-site building method wherein volumetric units or panels are fabricated in controlled factory environments and subsequently assembled on location to form complete structures. This approach diverges from conventional construction through its emphasis on precision engineering, reduced onsite labor, and accelerated project timelines. The practice aligns with Europe’s intensifying necessary for hoapplying, healthcare, and educational infrastructure amid chronic labor shortages and tightening environmental regulations. According to research, the European Union has experienced a significant and growing hoapplying gap in recent years, driven by various factors, with a particularly acute shortage of affordable hoapplying observed in Germany. Simultaneously, the built environment in the European Union is a major consumer of energy and a significant source of greenhoutilize gas emissions, highlighting a critical necessary for substantial improvements in sustainable and efficient building systems. Modular construction emerges not merely as a technique but as a strategic response to urban densification pressures, decarbonization mandates under the European Green Deal, and the imperative for resilient supply chains following recent geopolitical disruptions. Its integration into national infrastructure strategies reflects a paradigm shift in how Europe conceptualizes built environments in the twenty-first century.

MARKET DRIVERS

Accelerated Project Timelines Drive Adoption Across Public Infrastructure Sectors

The compression of construction schedules through modular methods has become a decisive driver in the Europe modular construction market. This is particularly true for schools, hospitals, and emergency hoapplying. Building practices following traditional methods usually take a significant amount of time for educational facilities of average size. The utilize of modular techniques in building design can significantly decrease how long it takes to complete a project. Many new school buildings now include elements of off-site construction as a common approach to meet the necessary for more space. Certain hospital construction projects utilizing modular methods have been able to become operational in a comparatively short timeframe, quicker than is typically possible with conventional building schedules. A key advantage in speed comes from running project tquestions simultaneously: the foundation can be worked on at the location while the individual parts are being created elsewhere. This approach avoids common delays that happen when bad weather interferes with on-site building work. Cities in some regions have adopted the regular utilize of modular construction provide social hoapplying quickly. This method is utilized to rapidly deploy thousands of hoapplying units to address immediate shelter necessarys. The ability to deliver habitable, code-compliant structures within weeks rather than years positions modular construction as an indispensable tool for responsive governance in Europe’s evolving urban landscape.

Stringent EU Green Building Regulations Reinforce Demand for Factory-Built Solutions

The region’s regulatory architecture, particularly the Energy Performance of Buildings Directive and the upcoming Carbon Border Adjustment Mechanism, exerts profound influence on construction methodologies, which further accelerates the Europe modular construction market. Modular construction inherently aligns with these frameworks through material optimization, waste reduction, and energy-efficient assembly protocols. Factories producing modular units generate less construction waste compared to on-site builds. Moreover, controlled environments enable precise insulation placement and airtightness control, directly contributing to the EU’s tarobtain of achieving net-zero operational emissions for all new buildings by 2030. Modular construction projects under building certification programs consistently reveal improved performance compared to conventional projects in whole-life carbon metrics. The revision of the Construction Products Regulation in 2024 further compels manufacturers to disclose environmental product declarations, a requirement that modular producers satisfy more readily due to standardized production logs. A majority of publicly funded modular hoapplying projects are achieving high-level eco-label certification tiers. This regulatory tailwind transforms compliance from a cost center into a competitive differentiator, embedding modular approaches within Europe’s decarbonization roadmap.

MARKET RESTRAINTS

Fragmented National Building Codes Impede Cross-Border Scalability

Persistent discrepancies in national building codes and certification protocols, despite the European Union’s harmonization efforts through the Construction Products Regulation, are major barriers to the Europe modular construction market. Each member state maintains distinct structural load requirements, fire safety classifications, and acoustic performance thresholds that complicate the replication of standardized modular designs across borders. For instance, seismic design categories mandated in Italy’s NTC 2018 differ materially from Germany’s DIN 1055 standards, necessitating costly redesigns for manufacturers seeking pan-European deployment. Operating modular construction firms in multiple countries can lead to higher average compliance costs compared to operating in only one counattempt. Different nations have unique thermal regulations for modular wall assemblies, requiring incompatible insulation specifications. Variations in national regulations and specifications can cautilize permitting approvals to be delayed. The absence of a unified digital permitting framework exacerbates delays, with modular projects requiring many separate authority validations in Spain versus those in Denmark. Mutual recognition of modular certifications is essential for realizing economies of scale, stimulating investment, and driving innovation within the sector.

Perception Gaps and Lack of Skilled Workforce Limit Mainstream Acceptance

Deep-seated misconceptions about modular construction’s durability, aesthetic flexibility, and long-term value persist among developers, architects, and conclude utilizers across the region, despite empirical evidence to the contrary, which ultimately inhibits the expansion of the Europe modular construction market. As per a study, a notable share of European property investors still associate modular buildings with temporary or low-quality structures, a legacy of postwar prefabrication. This perception gap translates into reduced demand from premium segments, where modular penetration remains less in luxury residential markets. Compounding this issue is a severe shortage of professionals trained in Design for Manufacture and Assembly principles. There is a noticeable skills gap concerning digital fabrication competencies within the construction sector. Training programs that focus specifically on modular construction techniques are currently limited in availability across several regions. The integration of modular construction topics into traditional vocational training programs remains infrequent. The absence of experts for complex modular integrations heightens the risk of project budobtain overruns and quality deviations, reinforcing negative perceptions. Modular construction’s market growth will remain limited by outdated perceptions and a lack of skilled professionals until the indusattempt and academia collaborate to promote it as a high-performance building solution, not just a low-cost option.

MARKET OPPORTUNITIES

Retrofitting Aging Infrastructure Through Modular Insertion Techniques Presents High Growth Potential

The continent’s vast stock of aging public buildings, particularly schools and healthcare facilities constructed between 1950 and 1980, offers a fertile ground for modular intervention via insertion or pod replacement strategies, which in turn provides new opportunities for the growth of the Europe modular construction market. Rather than full demolition, modular units can be slotted into existing structural grids to upgrade outdated interiors with minimal disruption. Across European regions, a large number of educational facilities necessary significant upgrades to meet modern standards for energy efficiency and accessibility. Initiatives are underway in some areas to improve school infrastructure, often incorporating modern construction techniques such as modular refurbishments. In specific Northern European countries, there is a push to update healthcare facilities, like nursing homes, with improved amenities for residents, utilizing methods that have revealn efficiencies in project timelines. These interventions leverage modular precision to enhance thermal performance, accessibility, and infection control without displacing occupants, a critical advantage in publicly funded assets where continuity of service is nonnereceivediable. This niche, though technically demanding, aligns with circular economy principles by extconcludeing building lifespans and avoiding embodied carbon from new construction.

Public-Private Partnership Frameworks Unlock Large-Scale Modular Deployment in Social Hoapplying

The acute hoapplying affordability crisis across European urban centers has cautilized innovative financing models wherein public entities provide land and regulatory quick tracking while private modular developers deliver turnkey units, which offer fresh prospects for the expansion of the Europe modular construction market. Such partnerships mitigate the capital intensity that historically deterred modular adoption. In the Netherlands, public initiatives and municipal land policies are increasingly promoting industrialized and modular construction methods to accelerate the delivery of much-necessaryed affordable hoapplying units. Spain’s national hoapplying plan encourages innovative building techniques and efficiency in construction through various funding streams, supporting the modernization and industrialization of the hoapplying sector. Indusattempt analyses and general reports suggest that modular hoapplying projects often demonstrate quicker project delivery compared to traditional construction, which supports in more rapidly addressing urgent hoapplying demands. Finnish hoapplying corporations utilize efficient, modern construction techniques, including modular systems, which contribute to cost management and enable the consistent supply of hoapplying within a stable market. These structured frameworks convert policy intent into scalable delivery, positioning modular construction as the operational engine of Europe’s social hoapplying revival.

MARKET CHALLENGES

Supply Chain Vulnerabilities Exacerbated by Geographic Concentration of Module Factories

Its vulnerability to supply chain disruptions due to the high geographic concentration of fabrication facilities hampers the growth of the Europe modular construction market. The modular construction sector in core Western European nations, notably Germany and the Netherlands, features a high concentration of advanced manufacturing facilities. Supply chain vulnerabilities, such as disruptions to major inland waterways like the Rhine River, pose significant risks to the timely transport and delivery of oversized modular components. Simultaneously, reliance on specialized components such as automated lifting systems and precision steel framing ties the sector to narrow supplier pools. The broader construction indusattempt experienced extconcludeed lead times and production challenges for various materials and equipment due to widespread supply chain volatility and material shortages in recent years. Unlike traditional construction, which can substitute local materials, modular production demands exact component conformity, leaving little room for improvisation. The war in Ukraine further exposed depconcludeencies on Eastern European suppliers for insulation and electrical subassemblies. Exports and production of various construction insulation materials, including phenolic foam, have experienced fluctuations in response to volatile petrochemical feedstock prices and evolving energy efficiency regulations. The market will remain vulnerable to logistics failures and sourcing issues until manufacturing diversifies and inventory buffers are utilized strategically.

Integration Complexities With Legacy Building Management Systems in Retrofit Projects

The seamless integration of prefabricated units with existing building management systems, especially in deep energy retrofits of midcentury structures, remains one of the major constraints to the Europe modular construction market. Many hospitals, universities, and government buildings upgraded with modular extensions rely on decades-old HVAC, fire alarm, and security networks that lack standardized communication protocols. Modular retrofit projects in the UK often encounter significant challenges with integrating existing operational technology systems, frequently necessitating the utilize of custom middleware solutions to bridge compatibility gaps. In Germany, as in other regions, modular construction projects can experience interoperability failures between different building automation and control architectures, such as KNX and BACnet. Issues stemming from the integration of diverse and sometimes incompatible control systems remain a notable barrier to the efficient implementation of modular building solutions. These technical mismatches not only inflate budobtains but also compromise energy performance, as smart sensors embedded in new modules cannot relay data to legacy dashboards, nullifying real-time optimization benefits. Modular additions will continue to operate as isolated components within larger physical ecosystems, reducing their overall lifecycle value proposition, until Europe implements mandatory open data standards for public building infrastructure.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

6.18% |

|

Segments Covered |

By Type, Material, Application & Region |

|

Various Analyses Covered |

Global, Regional & Counattempt Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe |

|

Market Leaders Profiled |

Laing O’Rourke, Skanska, Modulaire Group, KLEUSBERG, Berkeley Group, Bouygues Batiment International, Daiwa Houtilize Modular Europe Ltd., Modubuild, Elements Europe, Moelven Industrier ASA |

SEGMENTAL ANALYSIS

By Type Insights

In 2024, the Permanent Modular Construction (PMC) segment was the prominent segment in the Europe modular construction market and captured a substantial share. The prominence of the PMC segment is credited to its alignment with long-term infrastructure necessarys across hoapplying, education, and healthcare. Unlike temporary solutions, PMC units are engineered to meet the same durability, safety, and aesthetic standards as conventional buildings while retaining offsite efficiency benefits. An additional driver is institutional demand for code-compliant, scalable, and sustainable facilities. The German government, through the Federal Minisattempt of Hoapplying, Urban Development, and Building, actively promotes the utilize of serial and modular construction methods across publicly funded hoapplying projects as a key strategy to significantly accelerate project timelines, reduce costs, and address the national hoapplying deficit. NHS England has integrated the utilize of modern methods of construction (MMC), including modular techniques, into its capital investment strategies to streamline the development of healthcare infrastructure, such as new primary care centers and hospitals, amidst budobtain constraints and the necessary for rapid delivery of facilities. Crucially, PMC benefits from full integration into national building registries, enabling mortgage financing and long-term asset valuation, factors that relocatable units lack. This institutionalization, coupled with lifecycle cost advantages. PMC reduces operational expconcludeitures compared to traditional builds, solidifies its market leadership.

The relocatable modular construction segment is estimated to register the quickest CAGR of 9.4 % from 2025 to 2033 due to Europe’s escalating necessary for flexible, short-term spatial solutions in response to humanitarian, educational, and industrial contingencies. A different accelerator is the migrant crisis, which has prompted governments to adopt rapidly deployable shelter systems. French authorities are increasingly utilizing temporary and adaptable hoapplying solutions to manage the growing demand for accommodation for asylum seekers amid consistently high arrival numbers. In parallel, the education sector utilizes relocatable classrooms to manage enrollment surges without capital-intensive expansions. There is a growing interest in Sweden in the utilize of modular construction methods for educational facilities as a way to quickly address necessarys for increased school capacity and potentially expedite building timelines. Additionally, industrial firms leverage relocatable units for on-site offices and worker accommodations in remote energy or mining projects, particularly in Eastern Europe. This operational agility, combined with declining unit costs, positions relocatable construction as Europe’s most dynamically expanding segment.

By Material Insights

The steel segment held the leading share of 52.6% of the Europe modular construction market in 2024. The leading positioning of the steel segment is attributed to its structural versatility, rapid fabrication compatibility, and resilience in multistory applications, critical for urban infill projects. Steel’s high strength-to-weight ratio enables taller modular stacks, directly addressing density mandates in cities like Berlin and Amsterdam, where height restrictions favor vertical expansion over footprint growth. Moreover, steel’s compatibility with automated welding and robotic assembly lines in factories such as those operated by Laing O’Rourke in the UK enhances precision and throughput. The material also aligns with circular economy goals. Regulatory tailwinds further support adoption, as the revised Eurocode 3 now includes specific design protocols for modular steel systems, reducing certification amlargeuity that previously hindered uptake.

The wood segment is anticipated to witness the quickest CAGR of 11.2% from 2025 to 2033. The rapid expansion of the wood segment is fuelled by Europe’s aggressive embodied carbon reduction policies and advances in engineered timber technologies, suchas cross-laminated timber and dowel-laminated timber. Austria and Finland reveal a trconclude towards applying mass timber in new public modular school construction. The environmental imperative is clear. Wood-based modular buildings generally have a lower embodied carbon footprint compared to structures created of steel or concrete. Furthermore, wood’s biophilic properties enhance occupant well-being, a factor increasingly codified in building standards. Guidelines in Norway support the incorporation of timber interiors within publicly funded healthcare modular units. Digital fabrication has also resolved historical limitations. CNC routers now cut timber modules with millimeter precision, enabling complex geometries previously exclusive to steel. Policy and funding initiatives at the European level provide a supportive framework for the continued utilize and innovation of sustainable materials like wood in construction.

By Application Insights

The education and institutional segment dominated the Europe modular construction market by occupying a 31.2% share in 2024. The dominance of the education and institutional segment is becautilize of systemic underinvestment in public infrastructure, coupled with demographic pressures. Across the European Union, a substantial portion of existing school buildings requires significant renovation and modernization to comply with contemporary safety, energy efficiency, and accessibility requirements. Modular construction offers a turnkey solution that aligns with compressed academic calconcludears and stringent public procurement rules. In France, local authorities and municipalities are increasingly adopting modular construction solutions to rapidly accommodate student necessarys and address infrastructure challenges as part of broader educational facility investment plans. Danish public sector construction strategies encourage efficient and cost-effective building methods for new educational facilities, including the utilize of industrialized and modular construction approaches, to improve delivery times and manage budobtains effectively. These projects often integrate smart learning environments with prefabricated AV and HVAC systems, enhancing pedagogical quality without compromising speed. The segment’s institutional backing, recurring budobtain allocations, and low political risk ensure its sustained market leadership.

The healthcare segment is likely to experience the quickest CAGR of 12.7% from 2025 to 2033. The swift growth of the healthcare segment is driven by bypost-pandemicc healthcare infrastructure gaps, aging populations, and the rise of decentralized care models. Europe’s population aged 65 and over is experiencing a significant and continuing increase, a trconclude confirmed by Eurostat population statistics. The proportion of older people in the population is growing steadily. Modular construction excels in this context by enabling rapid deployment of sterile, code-compliant units with integrated medical gas and data systems. The UK’s health system is prioritizing the utilize of rapidly deployed, often modular, diagnostic hubs as part of its strategy to reduce waiting lists. These facilities are installed much quicker than traditional construction, accelerating the delivery of essential services. Healthcare planning in Germany, as in other nations, emphasizes robust infection control measures in all facilities, with a focus on structural quality and compliance with established hygiene recommconcludeations from bodies like the Robert Koch Institute. Furthermore, modular isolation wards have become standard in pandemic preparedness plans across Sweden and the Netherlands, ensuring surge capacity without permanent capital lockup. This convergence of demographic urgency, clinical efficacy, and fiscal pragmatism fuels healthcare’s ascent as the highest growth application segment.

COUNTRY ANALYSIS

Germany Modular Construction Market Analysis

Germany led the Europe modular construction market by capturing a 19.2% share in 2024. The supremacy of the German market is propelled by its robust manufacturing base, hoapplying crisis, and policy coherence. Germany currently experiences a significant and widely recognized hoapplying deficit, a situation that is expected to continue to worsen if the pace of new construction does not accelerate. In response, the federal government’s “Bündnis für Wohnen” coalition has hasquick-trackedd zoning reforms that explicitly favor modular developments, including pre-approved designs for up to six-story buildings. Industrial giants like Bosch and Siemens have repurposed automotive assembly lines for modular hoapplying. Regulatory alignment further accelerates adoption. Germany’s updated Baunutzungsverordnung now treats modular and conventional builds identically for mortgage and land utilize purposes, rerelocating historical stigma. Germany’s structural and strategic leadership position is reinforced by its deeply integrated supply chains and consistent public sector demand.

United Kingdom Modular Construction Market Analysis

The UK followed closely in the Europe modular construction market and held a 15.8% share in 2024. The demand for modular construction in the UK is credited to its mature offsite ecosystem and institutional procurement mandates. Following a review that emphasized issues with traditional construction methods, the UK government has integrated modern construction techniques into essential infrastructure initiatives. The justice system incorporates these methods for new facilities, resulting in quicker project completion, and a long-term school building initiative has designated specific funds for off-site construction methods to develop numerous schools. Current building safety regulations require digital modeling for relevant public structures, a necessary met by integrated modern construction processes. Despite Brexit-related supply chain friction, the UK’s early standardization and client readiness sustain its market position.

France Modular Construction Market Analysis

France is also a major player in the Europe modular construction market, with urban densification mandates and climate legislation. Regulatory modifys encourage specific construction methods for new public buildings. Certain building systems meet low-carbon certification standards more easily than conventional on-site construction techniques. A major European city has approved a substantial number of modular hoapplying units as part of its local hoapplying strategy. A specific urban district now features one of the continent’s tallest residential towers built applying modular construction. Projects utilizing modular methods demonstrate reduced emissions compared to traditional construction. These emission reductions are primarily attributed to improved waste management and streamlined material transport. A policy is in place to accelerate permits for modular projects in designated development areas. A growing percentage of new municipal hoapplying projects are now utilizing modular construction methods. The market trconclude is defined by the integration of efficiency, sustainability goals, and social equity objectives in construction practices.

Netherlands Modular Construction Market Analysis

The Netherlands is growing moderately in the Europe modular construction market due to its circular construction mandates and water-adaptive design. New government buildings in the Netherlands are required to meet high standards for material circularity. The government’s hoapplying programs are delivering numerous modular apartments that are designed for full disassembly and reutilize. Infrastructure authorities are applying modular construction for temporary site offices, allowing units to be easily relocated and reutilized across different projects. Dutch firms are leaders in floating construction, utilizing modular designs for floating homes that are engineered to adapt to modifying water levels. Modular construction is a significant portion of new hoapplying starts in urban regions, driven by the necessary to efficiently utilize available land and build resilient homes. The Netherlands’ fusion of climate adaptation and circularity cements its distinct market role.

Sweden Modular Construction Market Analysis

Sweden is predicted to expand in the Europe modular construction market from 2025 to 2033 by leveraging modular construction to uphold its welfare state commitments amid population growth. There is a necessary for a substantial number of new homes, and modular construction methods are being considered to support meet this tarobtain while maintaining quality. A national hoapplying strategy directs that a portion of municipal land reserves be utilized specifically for modular hoapplying developments. One city consistently provides aseveralmodular apartments each year as part of its hoapplying initiatives. The region has strict energy efficiency requirements for public hoapplying, which are being addressed through controlled production environments to achieve efficient insulation and airtightness. Modular construction is seeing increased utilize in elderly care living situations. The consistent indoor environmental quality provided by modular construction is associated with positive effects on resident well-being. So, Sweden exemplifies how social policy and construction innovation converge to drive market expansion.

COMPETITIVE LANDSCAPE

The Europe modular construction market features intense competition characterized by a mix of large multinational construction firms, specialized modular manufacturers, and agile regional players. Competition is not solely price-driven but increasingly hinges on technological sophistication, regulatory compliance, sustainability credentials, and speed of delivery. Major firms differentiate themselves through proprietary factory systems, digital integration capabilities, and strategic alignment with national hoapplying or healthcare policies. Regional players often compete on local code expertise and community relationships, particularly in complex urban retrofit projects. The market lacks a dominant single player, fostering continuous innovation in materials, logistics, and assembly techniques. Consolidation is gradually increasing as companies seek scale to manage rising compliance and capital costs. However, fragmentation persists due to national regulatory differences, limiting pan-European dominance and encouraging collaborative ecosystems over pure market share battles.

KEY MARKET PLAYERS

- Laing O’Rourke,

- Skanska

- Modulaire Group

- KLEUSBERG

- Berkeley Group

- Bouygues Batiment International

- Daiwa Houtilize Modular Europe Ltd.

- Modubuild

- Elements Europe

- Moelven Industrier ASA

Top Players In The Market

- Bouygues Construction is a leading French industrial group with deep expertise in off-site and modular building techniques across Europe. The company has significantly advanced the integration of digital design andfactory-basedd assembly in public infrastructure projects. Recently, Bouygues launched its “Open Source Factory” initiative in France, a dedicated modular production facility focutilized on schools and social hoapplying that combines robotics with sustainable materials. The company has also partnered with academic institutions to develop next-generation timber modular systems compliant with France’s stringent low-carbon building regulations. These actions reinforce its commitment to accelerating delivery while meeting national decarbonization mandates through scalable industrialized construction.

- Skanska is a major Nordic construction and development firm that has embedded modular construction into its core delivery model for healthcare and educational facilities across Sweden, the UK, and Norway. The company operates its own modular manufacturing unit in Wolverhampton, UK, which produces fully fitted volumetric modules for hospitals and student hoapplying. This innovation enhances quality control and lifecycle management, aligning with Sweden’s welfare-driven public procurement standards and strengthening Skansika’s role as a technology-enabled modular solutions provider in Northern Europe.

- Algeco is a pan-European modular space solutions provider with operations in over 20 countries, specializing in both relocatable and permanent modular buildings for public and private sectors. The company has intensified its focus on sustainable modular design by launching its “Green Module” program in 2024, which features recycled steel frames, bio-based insulation, and solar-ready roofs. It also collaborates with local governments on circular economy pilot projects, ensuring modules can be disassembled and repurposed after initial utilize. These initiatives position Algeco as a responsive and environmentally conscious leader in flexible modular infrastructure.

Top Strategies Used By The Key Market Participants

Key players in the Europe modular construction market are prioritizing vertical integration by owning or partnering with dedicated module factories to ensure supply chain control and production consistency. They are investing heavily in digitalization through building information modeling and digital twin technologies to enhance design accuracy and operational efficiency. Strategic public-private partnerships with municipal and national governments enable access to land and quick-tracked permitting. Companies are also standardizing product platforms to achieve economies of scale while maintaining customization for local codes. Additionally, sustainability is central to their strategies, with widespread adoption of low-carbon materials, circular design principles, and energy-efficient manufacturing processes to align with EU regulatory mandates and client expectations.

MARKET SEGMENTATION

This research report on the Europe modular construction market is segmented and sub-segmented into the following categories.

By Type

- Permanent (PMC)

- Relocatable

By Material

By Application

- Commercial

- Healthcare

- Educational & Institution

- Hostility

- Others (Residential, Religious Buildings)

By Counattempt

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Leave a Reply