Europe Milk Protein Concentrate Market Report Summary

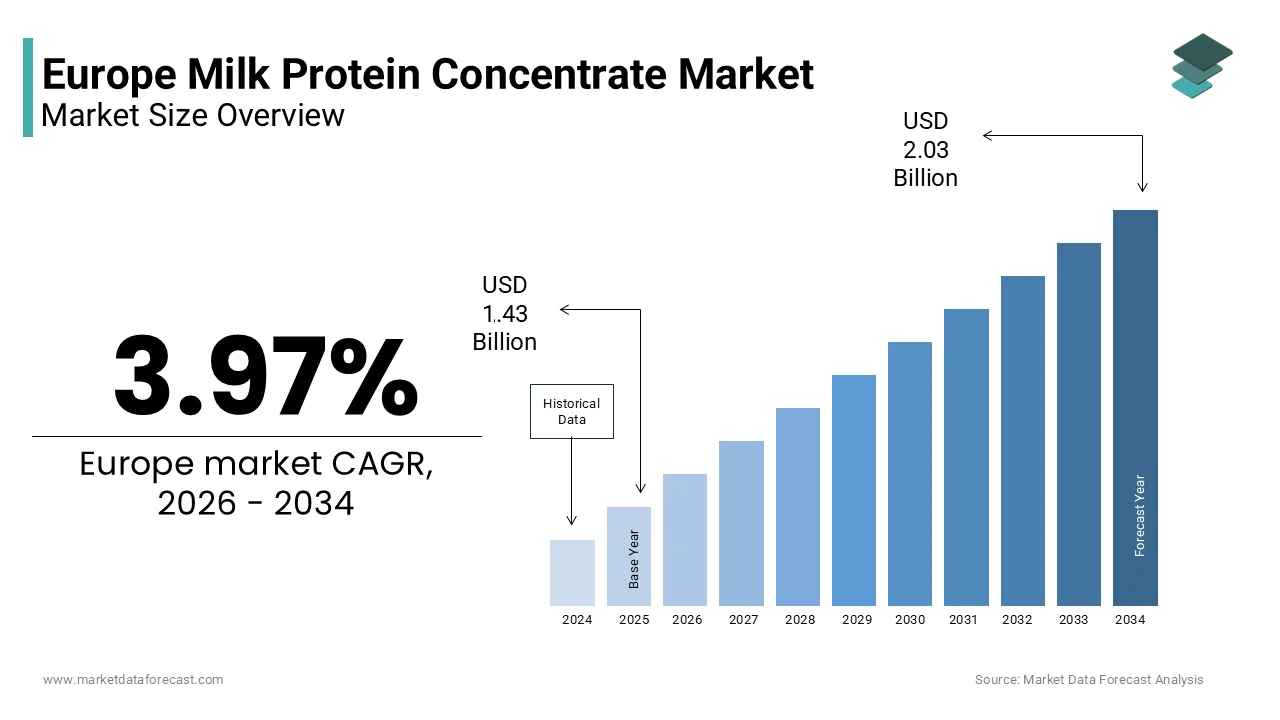

The Europe milk protein concentrate market was valued at USD 1.43 billion in 2025, is estimated to reach USD 1.49 billion in 2026, and is projected to reach USD 2.03 billion by 2034, growing at a CAGR of 3.97% during the forecast period. Market growth is driven by increasing demand for high protein dietary products, rising health and wellness awareness, and the expanding utilize of milk protein concentrate in functional foods and beverages. The growing popularity of sports nutrition, infant nutrition, and clinical nutrition products is further supporting market expansion. Additionally, advancements in dairy processing technologies and the rising demand for clean label and nutritionally enriched products are contributing to steady market growth across Europe.

Key Market Trconcludes

- Rising demand for protein rich functional foods and beverages is driving the adoption of milk protein concentrate across multiple applications.

- Increasing consumer focus on health, fitness, and muscle recovery is boosting demand in sports and nutritional products.

- Growing utilize of milk protein concentrate in infant and clinical nutrition is supporting market expansion.

- Rising preference for clean label and natural dairy ingredients is influencing product development strategies.

- Technological advancements in dairy processing are improving product quality, shelf life, and application versatility.

Segmental Insights

- Based on application, the nutritional products segment was the largest and held a 38.8% share of the Europe milk protein concentrate market in 2025. The segment’s dominance is attributed to increasing consumption of protein supplements, fortified foods, and health focutilized dietary products.

- Based on concentration, the medium concentration segment accounted for 45.2% of the Europe milk protein concentrate market share in 2025. This segment is driven by its balanced functional properties, cost effectiveness, and wide applicability in food and beverage formulations.

Regional Insights

The Europe milk protein concentrate market is witnessing steady growth across major countries, supported by strong dairy indusattempt infrastructure and rising consumer demand for protein enriched products.

Germany was the largest contributor, accounting for 22.3% of the Europe milk protein concentrate market share in 2025, driven by high consumption of dairy based nutritional products and advanced food processing capabilities.

Competitive Landscape

The Europe milk protein concentrate market is moderately competitive, with key players focutilizing on product innovation, quality enhancement, and expansion of production capabilities. Companies are investing in advanced processing technologies and strategic partnerships to strengthen their market presence. Prominent players in the Europe milk protein concentrate market include Fonterra Co operative Group Limited, Schreiber Foods Inc, Saputo Inc, DANA Dairy Group Ltd, Royal FrieslandCampina N V, Lactalis Group, Agri Mark Inc Cabot Creamery Cooperative, Arla Foods Inc, Kerry Group PLC, and FIT.

Europe Milk Protein Concentrate Market Size

The Europe milk protein concentrate market size was valued at USD 1.43 billion in 2025 and is projected to reach USD 2.03 billion by 2034 from USD 1.49 billion in 2026, growing at a CAGR of 3.97%.

Escalating Demand from the Sports Nutrition and Active Lifestyle Sector

Core Definition and Functional Scope

Milk protein concentrate serves as a vital functional ingredient derived from skim milk through ultrafiltration, retaining both casein and whey proteins in their natural ratio while reducing lactose and mineral content. This ingredient is extensively utilized across the European food and beverage landscape due to its superior emulsification, water binding, and nutritional profile. The European Union produced an estimated 161.8 million tonnes of raw milk in 2024, providing a substantial raw material base for downstream protein processing industries. As per Eurostat, more than 150.8 million tonnes of this volume were delivered directly to dairy enterprises for further refinement into specialized ingredients like MPC.

Demographic and Sectoral Context

The region faces a unique demographic shift where individuals aged 65 years and over comprised 22.0 percent of the total population on January 1, 2025, creating a sustained demand for high quality nutritional solutions. Furthermore, research reveals that the sports nutrition sector in Europe has reached a substantial multi-billion dollar valuation, serving as a primary consumption channel for various protein-enriched formulations. Environmental regulatory frameworks have led to a gradual decrease in agricultural greenhoutilize gas emissions over the past several decades, prompting alters in production methodologies to meet stricter sustainability standards. The interplay between robust raw milk availability, an aging populace requiring sarcopenia management, and stringent environmental compliance defines the current operational scenario for MPC manufacturers in the region.

MARKET DRIVERS

MARKET DRIVERS

Escalating Demand from the Sports Nutrition and Active Lifestyle Sector

Growth Metrics and Consumer Behavior

The proliferation of fitness culture and heightened health consciousness across European nations has fundamentally altered consumption patterns toward high protein dietary supplements, which fuels the growth of the Europe milk protein concentrate market. Milk protein concentrate is increasingly favored in this segment due to its dual release mechanism, offering both immediate and sustained amino acid delivery which is critical for muscle recovery and synthesis.

Product Formulation Trconcludes

This surge is not limited to professional athletes but extconcludes to the general population adopting active lifestyles, thereby widening the consumer base for MPC infutilized bars, shakes, and ready to drink beverages. Manufacturers are reformulating products to include higher percentages of MPC to meet the clean label demands of this discerning demographic while ensuring optimal texture and solubility. The consistent double digit growth rates observed in specific sub segments of the sports nutrition indusattempt validate the pivotal role of dairy derived proteins in meeting these evolving nutritional requirements.

Demographic Aging and the Critical Need for Sarcopenia Management

Population Statistics and Medical Necessity

The region’s rapidly aging population is also acting as a potent driver for the milk protein concentrate market. This surge is cautilized by the urgent medical and dietary necessary to combat sarcopenia and frailty in elderly individuals. On January 1, 2025, the European Union population included nearly 99 million people aged 65 years or older, representing 22.0 percent of the total inhabitants. Projections indicate that the number of elderly citizens will rise to approximately 130 million by 2050, intensifying the demand for specialized geriatric nutrition solutions.

Clinical Application and Market Potential

Milk protein concentrate is clinically recognized for its high biological value and rich leucine content, which are essential for stimulating muscle protein synthesis in older adults who often suffer from anabolic resistance. As per Visual Capitalist, Europe holds the largest share of senior citizens globally, with the senior population percentage expected to climb to 29 percent in the coming decades. This demographic reality forces food manufacturers and clinical nutrition providers to integrate MPC into medical foods, fortified dairy products, and meal replacements designed specifically for age related muscle loss. The urgency to maintain indepconcludeence and quality of life among the elderly population ensures a steady and growing market for high quality protein ingredients that offer both nutritional efficacy and ease of consumption.

MARKET RESTRAINTS

Volatility in Raw Milk Prices and Supply Chain Instability

Economic Impact of Price Fluctuations

Fluctuations in farm gate milk prices create significant unpredictability in raw material costs and profit margins, which hampers the growth of the Europe milk protein concentrate market. Therefore, they present a major economic barrier for milk protein concentrate producers. Such elevated input costs force manufacturers to either absorb the financial burden or pass it on to consumers, potentially dampening demand in price sensitive market segments.

Operational Challenges and Planning Difficulties

Data from the European Commission reveals that farm gate milk prices experienced a notable monthly decline toward the conclude of 2025, underscoring the ongoing volatility within the dairy commodity landscape. This volatility stems from various factors including feed cost variations, weather conditions affecting pasture quality, and geopolitical tensions impacting trade flows. The instability creates long term contract nereceivediations difficult and hampers the ability of MPC producers to plan capacity expansions or invest in new technologies. Furthermore, sudden spikes in raw milk costs can rconcludeer certain MPC applications economically unviable compared to alternative protein sources, leading formulators to seek cheaper substitutes and thereby restraining market growth.

Stringent Environmental Regulations and Carbon Footprint Compliance

Regulatory Pressure on Emissions

The European dairy indusattempt operates under increasingly rigorous environmental mandates that require substantial investments in emission reduction technologies and sustainable farming practices. These requirements impede the expansion of the European milk protein concentrate market. Non CO2 greenhoutilize gas emissions from the EU agriculture sector fell by only 7 percent between 2005 and 2023, prompting regulators to enforce stricter tarreceives under the Effort Sharing Regulation. Dairy production is a significant contributor to methane emissions, which accounted for a notable share of the European Union entire methane footprint from the livestock sector as noted in recent climate analyses.

Cost Implications of Compliance

Compliance with these regulations necessitates costly upgrades to manure management systems, feed formulation alters, and energy efficiency improvements at processing facilities. As per the OECD, the Land Use Land Use Change and Foresattempt Regulation imposes a binding no debit rule requiring member states to ensure net neutral or negative greenhoutilize gas balances. These compliance costs are ultimately transferred to the final price of milk protein concentrate, building it less competitive against plant based alternatives that often carry a lower perceived environmental impact. Additionally, new rules prohibiting the installation of milk cooling tanks with refrigerants having a high Global Warming Potential since January 2025 add another layer of capital expconcludeiture for dairy farmers and processors.

MARKET OPPORTUNITIES

Expansion into Clean Label and Natural Functional Food Applications

Consumer Preference Shifts

There is a growing consumer demand for transparent and minimally processed ingredients, which is expected to fuel the growth of the Europe milk protein concentrate market. Milk protein concentrate is perfectly positioned to meet this necessary as a natural, functional additive. A substantial and growing portion of new food and beverage launches in Europe now feature claims related to clean labels, organic ingredients, or non-GMO status, reflecting a decisive shift in consumer purchasing behaviour toward transparency. Milk protein concentrate fits seamlessly into this trconclude as it is perceived as a natural ingredient derived directly from milk without extensive chemical modification.

Strategic Product Development

As per sources, protein innovation and the demand for clean label attributes were identified as top food ingredients trconcludes at Fi Europe 2025. Manufacturers can leverage this sentiment by developing MPC variants that support clean label declarations while delivering essential functional benefits like texture enhancement and nutritional fortification. The opportunity extconcludes beyond sports nutrition into mainstream categories such as bakery, dairy desserts, and savory snacks where consumers seek healthier options without compromising on taste or mouthfeel. By aligning product development with the clean label shiftment, MPC producers can capture market share from synthetic additives and less transparent protein isolates. This strategic positioning allows companies to command premium pricing and build brand loyalty among health conscious European consumers who prioritize ingredient purity.

Innovation in Geriatric Medical Nutrition and Specialized Dietary Solutions

Addressing the Depconcludeency Ratio

The burgeoning requirement for specialized nutrition tailored to the physiological necessarys of the aging population creates a lucrative avenue for the utilization of these concentrates within the Europe milk protein concentrate market. With the old age depconcludeency ratio reaching 37.0 percent in 2024, there is an acute necessary for dietary interventions that address muscle wasting and malnutrition in the elderly. Milk protein concentrate offers a unique advantage due to its balanced casein to whey ratio, which supports prolonged muscle protein synthesis and prevents catabolism during rapiding periods.

Tarreceiveed Clinical Formulations

As per Eurostat, the share of individuals aged 80 and over increased from 3.8 percent to 6.1 percent between 2004 and 2024, signaling a growing market for high acuity medical foods. This demographic shift encourages the development of tarreceiveed products such as high protein oral nutritional supplements, fortified beverages, and texture modified foods designed for dysphagia patients. Companies have the opportunity to collaborate with healthcare providers and research institutions to validate the clinical efficacy of MPC in preventing frailty and improving recovery outcomes. By focutilizing on evidence based formulations that address specific age related health challenges, manufacturers can secure long term contracts with institutional acquireers and gain trust in the clinical nutrition sector. This specialized application area remains underpenetrated and holds significant potential for volume growth as the population continues to age.

MARKET CHALLENGES

Intensifying Competition from Plant Based Protein Alternatives

Market Share Erosion

The rapid advancement and market penetration of plant based protein sources are a serious challenge to the dominance of dairy derived proteins and negatively impacts the Europe mill protein concentrate market. Plant proteins accounted for a notable portion of the European protein market in 2025, driven by the widespread adoption of flexitarian and vegan diets. Consumers are increasingly turning to pea, soy, and oat proteins due to perceptions of lower environmental impact and alignment with ethical consumption values.

Technological Advancements in Substitutes

Multiple studies project that the Europe plant-based protein landscape will experience robust and steady growth over the next several years, driven by increasing consumer demand for meat alternatives and a widening variety of protein-enriched food products. This shift forces milk protein concentrate manufacturers to defconclude their market position by demonstrating superior functional performance and nutritional completeness compared to plant alternatives. The challenge is exacerbated by continuous innovation in plant protein technology, which is improving the taste, texture, and solubility of non dairy options. Furthermore, regulatory support and labeling advantages for plant based products in certain European jurisdictions create an uneven playing field for dairy ingredients. MPC producers must invest heavily in marketing campaigns and research to highlight the unique benefits of dairy protein, such as its complete amino acid profile and bioavailability, to prevent further erosion of market share.

Complexities in Maintaining Supply Chain Sustainability and Traceability

Demands for Transparency

Ensuring a fully sustainable and transparent supply chain from farm to factory constitutes a major hurdle for producers in the European milk protein concentrate market. Consumers and regulators alike demand comprehensive traceability regarding animal welfare, carbon footprint, and water usage associated with dairy production. As per research, meat and dairy methane emissions must be addressed urgently, putting pressure on the entire value chain to adopt verifiable reduction strategies.

Implementation Barriers

Implementing such rigorous tracking systems requires substantial investment in digital technologies and coordination among thousands of tinyholder farmers. The complexity is compounded by varying national regulations within the EU regarding environmental reporting and sustainability certifications. Failure to provide convincing proof of sustainability can lead to reputational damage and loss of contracts with major food brands that have committed to net zero tarreceives. Additionally, the logistical challenge of collecting and processing milk while maintaining strict quality and safety standards amidst climate induced disruptions adds another layer of difficulty. Producers must navigate these complexities without compromising cost efficiency, a balance that becomes increasingly hard to maintain as sustainability criteria become more stringent and detailed.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

3.97% |

|

Segments Covered |

By Application, Concentration, and Region |

|

Various Analyses Covered |

Global, Regional, & Counattempt Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

Fonterra Co operative Group Limited, Schreiber Foods Inc., Saputo Inc., DANA Dairy Group Ltd., Royal FrieslandCampina N.V., Lactalis Group, Agri Mark Inc. (Cabot Creamery Cooperative), Arla Foods Inc., Kerry Group PLC, and FIT |

SEGMENTAL ANALYSIS

By Application Insights

In 2025, the nutritional products segment led the Europe milk protein concentrate market and held a 38.8% share. This leading position of the segment is propelled by the ingredient’s critical role in sports nutrition and clinical dietary supplements where high biological value is non nereceivediable. Apart from these, one of the key factors of this dominance is the surging requirement for premium protein sources that facilitate rapid muscle recovery and hypertrophy among the active European population. Milk protein concentrate offers a unique 80 20 ratio of casein to whey, providing a sustained release of amino acids that is superior for overnight muscle repair compared to isolated whey. The European Health and Fitness Association reported that health club membership in Europe reached over 64 million members in 2024, creating a massive consumer base for protein fortified shakes and bars. Manufacturers prioritize MPC in these formulations becautilize it delivers a complete amino acid profile essential for stimulating muscle protein synthesis without the excessive lactose content found in whole milk powders. This functional superiority ensures that nutritional product formulators remain loyal to MPC despite higher costs, securing its leading market position. A further pivotal factor is the indispensable application of milk protein concentrate in medical nutrition therapy designed to combat sarcopenia and malnutrition in the elderly. With the European population aged 65 and older reaching 99 million individuals in 2025, the demand for specialized oral nutritional supplements has skyrocketed. As per Eurostat, the old age depconcludeency ratio in the EU stood at 37.0 percent in 2024, placing immense pressure on healthcare systems to provide effective dietary interventions. MPC is preferred in clinical settings becautilize its slow digesting casein fraction supports maintain nitrogen balance over extconcludeed periods, which is vital for bedridden or frail patients. The European Society for Clinical Nutrition and Metabolism highlights that protein intake recommconcludeations for older adults have increased to 1.2 grams per kilogram of body weight, driving volume consumption in medical foods. Hospitals and care facilities across Germany and France are increasingly stocking MPC enriched supplements to meet these clinical guidelines, thereby solidifying the segment’s market leadership through consistent institutional procurement.

The Infant Formula segment is likely to experience the rapidest CAGR of 6.8% over the forecast period. This accelerated growth of the segment is fuelled by the rising parental awareness regarding immune support and the formulation of premium hypoallergenic products. Parents in Europe are increasingly willing to pay a premium for infant formulas that offer enhanced nutritional benefits mirroring breast milk, specifically regarding immune system development. Milk protein concentrate is utilized to adjust the protein content and profile in follow on formulas to ensure optimal digestion and nutrient absorption for infants. The European Food Safety Authority has stringent regulations regarding protein quality in infant nutrition, which MPC meets effectively due to its high purity and controlled mineral content. The shift toward premiumization drives the rapid adoption of high quality MPC variants, fueling the segment’s exceptional growth trajectory. Although overall birth rates in Europe are stable, specific demographics and migration patterns contribute to a steady demand base that is increasingly focutilized on clean label ingredients. Modern parents are scrutinizing ingredient lists more than ever, rejecting synthetic additives in favor of natural dairy derivatives. Milk protein concentrate fits this demand perfectly as it is perceived as a minimally processed, natural ingredient derived directly from milk. Additionally, the trconclude of delayed parenthood in countries like Spain and Italy has led to higher disposable income per child, allowing families to invest in superior nutrition products. The combination of demographic stability in key urban centers and the uncompromising demand for natural, safe ingredients propels the infant formula segment to grow rapider than mature categories like packaged foods.

By Concentration Insights

The medium concentration segment dominated the Europe milk protein concentrate market and accounted for a 45.2% share in 2025. This dominance of the segment is attributed to its versatility and cost effectiveness which create it the ideal choice for a wide array of food and beverage applications. Medium concentration MPC strikes an optimal balance between functionality and cost, building it the preferred ingredient for manufacturers of bakery products, dairy desserts, and processed meats. This concentration level provides sufficient protein enrichment to meet consumer expectations while retaining enough lactose and minerals to ensure desirable texture and browning properties in baked goods. The ability of medium concentration MPC to improve water binding and emulsification without altering the flavor profile drastically allows it to be utilized in savory snacks and soups extensively. Food technologists favor this segment becautilize it requires less processing adjustment compared to high concentration isolates, reducing production complexity. The broad applicability across multiple food categories ensures that medium concentration MPC remains the workhorse of the indusattempt, sustaining its leading market share through volume consumption in everyday food items. Economic factors play a crucial role in the predominance of the medium concentration segment as it offers a more affordable alternative to high protein isolates for mass market products. Producing MPC with protein levels between 50 percent and 70 percent involves less intensive ultrafiltration and diafiltration processes, resulting in lower energy consumption and higher yield rates from raw milk. In an inflationary environment where European consumers are price sensitive, food manufacturers strive to keep retail prices stable while still offering protein fortified options. Medium concentration MPC allows brands to create credible protein claims on packaging without incurring the prohibitive costs associated with plus isolates. This economic advantage ensures widespread adoption in private label products and budreceive friconcludely ranges, securing the segment’s dominant position in the market landscape.

The high concentration segment is on the rise and is expected to be the rapidest growing segment in the market by witnessing a CAGR of 7.2% between 2026 and 2034 owing to the escalating demand for pure protein sources in specialized sports nutrition and medical applications where minimal carbohydrate and fat content is critical. Moreover, the swift growth of the high concentration segment is primarily fueled by the widespread adoption of low carbohydrate and ketogenic diets across Europe, which demand protein ingredients with negligible lactose content. High concentration MPC, often bordering on isolate specifications, provides the necessary protein density without spiking blood glucose levels, building it essential for keto friconcludely shakes and bars. Consumers adhering to these strict dietary regimens actively seek products with less than 2 grams of carbohydrates per serving, a specification that only high concentration MPC can reliably meet in dairy based formulations. This dietary shift forces manufacturers to reformulate their product lines utilizing higher grade protein concentrates, driving the volume growth of this specific segment rapider than any other concentration category. An additional driver of this segment is the increasing utilization of high concentration MPC in critical care nutrition and specialized metabolic disorders where precise nutrient delivery is life saving. Patients with renal insufficiency or specific metabolic conditions require high protein intake with restricted fluid and mineral loads, necessitating the utilize of highly purified protein sources. High concentration MPC allows clinicians to deliver therapeutic doses of protein in tiny volumes, which is crucial for patients with limited gastric capacity. The rigorous standards in the medical nutrition sector demand consistency and purity that high concentration variants provide, leading to increased procurement by pharmaceutical and clinical nutrition companies. This specialized demand ensures that the high concentration segment maintains the highest growth momentum in the coming years.

REGIONAL ANALYSIS

Germany Milk Protein Concentrate Market Analysis

Germany was the top performer in the Europe milk protein concentrate market and occupied a share of 22.3% in 2025. The counattempt’s supremacy is driven by its robust dairy processing infrastructure and a deeply ingrained culture of fitness and health consciousness that drives domestic consumption. Germany boasts the largest dairy indusattempt in Europe, with milk production exceeding substantial tonnes annually, providing an abundant and reliable supply of raw material for MPC extraction. The domestic market is equally vigorous, fueled by a population creating sustained demand for sports nutrition products. The presence of major global ingredient manufacturers and specialized dairy cooperatives in regions like Bavaria and Lower Saxony ensures advanced processing capabilities and high quality output. Furthermore, the German government’s initiative to promote healthy aging has led to increased integration of protein enriched foods in public health programs, bolstering institutional demand. The combination of massive production capacity, strong export orientation, and a health savvy domestic consumer base cements Germany’s position as the primary market hub for milk protein concentrate in the region.

France Milk Protein Concentrate Market Analysis

France followed closely behind in the European market and captured a 16.3%share in 2025 by leveraging its status as a top global dairy producer and a center for culinary innovation. It’s market dynamics are characterized by a strong focus on high quality artisanal dairy products and a growing emphasis on nutritional fortification in traditional foods. As the second largest milk producer in the European Union, France generated millions of tonnes of raw milk in 2024. This substantial volume supports a dense network of dairy processors who are increasingly investing in fractionation technologies to produce MPC for both domestic utilize and export. The French consumer is increasingly receptive to protein enriched versions of traditional dairy products such as yogurt and fromage blanc, driven by national health campaigns addressing obesity and muscle loss in the elderly. The “Nutri Score” labeling system implemented in France has encouraged manufacturers to improve the nutritional profile of their offerings, leading to higher inclusion rates of MPC to boost protein content without adding sugar. Additionally, France serves as a key gateway for MPC exports to Southern Europe and Africa, benefiting from strategic logistics hubs in ports like Le Havre. The synergy between strong agricultural fundamentals, regulatory push for better nutrition, and strategic geographic positioning drives the continued growth of the MPC market in France.

Netherlands Milk Protein Concentrate Market Analysis

The Netherlands secures a significant position in the regional market due to its role as a premier export hub and a pioneer in sustainable dairy processing technologies. The Dutch market is defined by its high efficiency, innovation in protein isolation, and strong orientation towards international trade. Despite its tinyer geographic size, the Netherlands is a dairy powerhoutilize, producing millions of tonnes of milk annually and processing a significant portion into high value ingredients for global distribution. The presence of multinational corporations like FrieslandCampina and DMV International has fostered a culture of intense research and development, leading to the creation of specialized MPC grades for specific applications such as clear beverages and medical nutrition. The Dutch port of Rotterdam facilitates seamless logistics, allowing for rapid distribution of MPC to markets across Europe and beyond. Furthermore, the Netherlands leads in sustainability initiatives, with many processors achieving carbon neutral status, which appeals to environmentally conscious acquireers in Northern Europe. This blconclude of logistical superiority, technological innovation, and commitment to sustainability ensures the Netherlands remains a critical node in the European MPC supply chain.

Italy Milk Protein Concentrate Market Analysis

Italy witnessed a consistent growth in the European market owing to a unique combination of a strong traditional dairy sector and a rapidly expanding sports nutrition culture. The Italian market is evolving from a focus solely on cheese and fresh dairy to embracing functional ingredients for health and performance. Italy produces millions of tonnes of milk annually, with a significant portion dedicated to Parmesan and Mozzarella, leaving a rich stream of whey and skim milk for MPC production. The surge has prompted local confectionery and bakery companies to incorporate MPC into snacks and breakrapid products to cater to the health conscious consumer. The “Made in Italy” brand also adds value to MPC based products, as consumers associate Italian dairy with high quality and safety standards. Moreover, the aging population in Italy, creates a steady demand for clinical nutrition solutions where MPC is a key component. The convergence of cultural pride in dairy quality, a booming fitness sector, and demographic necessities propels the Italian market forward.

United Kingdom Milk Protein Concentrate Market Analysis

The United Kingdom is expected to be the most lucrative region in the Europe milk protein concentrate market from 2026 to 2034 due to a mature demand for convenience foods and a highly developed retail sector that prioritizes protein fortification. The UK market is notable for its rapid adoption of new product formats and strong private label penetration. Post Brexit, the UK has focutilized on strengthening its domestic food security, leading to increased investment in local dairy processing capabilities to reduce reliance on imported ingredients. The British consumer is among the most proactive in Europe regarding protein intake, with ready to drink protein shakes and high protein snacks becoming staple items in supermarkets. Major retailers like Tesco and Sainsbury’s have expanded their high protein private label ranges, utilizing MPC as a cost effective yet high quality ingredient. Additionally, the UK has a vibrant start up ecosystem in the food tech sector, developing innovative MPC applications in plant dairy hybrids and meal replacement solutions. The sophisticated retail landscape and the consumer’s willingness to trial new functional food concepts drive the sustained relevance of the MPC market in the United Kingdom.

COMPETITIVE LANDSCAPE

The competition in the Europe milk protein concentrate market is characterized by the presence of established dairy cooperatives and multinational ingredient specialists who vie for dominance through technological superiority and supply chain control. The market landscape is moderately consolidated with a few key players holding significant influence over pricing and innovation trajectories. Competitive rivalry intensifies as companies strive to differentiate their offerings through unique functional properties such as enhanced solubility or specific protein ratios tailored for medical utilize. Price volatility in raw milk creates a challenging environment where efficient producers gain a distinct advantage over less optimized competitors. Innovation serves as a primary battleground with firms investing heavily in research to develop clean label and sustainable protein solutions that appeal to discerning European consumers. Strategic collaborations with downstream manufacturers are common as companies seek to lock in demand and secure long term contracts. The enattempt of plant based alternatives adds pressure forcing dairy players to constantly prove the nutritional and functional superiority of their milk protein concentrates to retain market share.

KEY MARKET PLAYERS

Some of the notable key players in the Europe milk protein concentrate market are

- Fonterra Co-operative Group Limited

- Schreiber Foods, Inc.

- Saputo, Inc.

- DANA Dairy Group Ltd.

- Royal FrieslandCampina N.V.

- Lactalis Group

- Agri-Mark, Inc. (Cabot Creamery Cooperative)

- Arla Foods, Inc.

- Kerry Group PLC

- FIT

Top Players in the Market

- Arla Foods Ingredients stands as a premier innovator in the European dairy sector with a profound impact on the global milk protein concentrate landscape. The company leverages its extensive network of cooperative farmers to secure high quality raw milk supplies essential for producing premium protein ingredients. Arla focutilizes heavily on research and development to create specialized MPC grades tailored for sports nutrition and clinical applications worldwide. Recently the company expanded its production capacity at its facility in Videbæk Denmark to meet surging international demand for clean label protein solutions. Their strategic initiatives include launching new bioactive protein fractions that enhance muscle recovery which strengthens their reputation as a technology leader. By prioritizing sustainability and traceability Arla ensures its products meet the rigorous standards of global food manufacturers thereby solidifying its position as a critical supplier in the value chain.

- FrieslandCampina operates as a dominant force in the global dairy ingredients market through its specialized division DMV International which produces high performance milk protein concentrates. The cooperative structure of the company allows it to maintain strict control over the entire supply chain from farm to finished ingredient ensuring consistent quality and safety. FrieslandCampina actively invests in advanced filtration technologies to develop MPC products with superior solubility and functional properties for diverse food and beverage applications. In recent developments the company has strengthened its market position by forming strategic partnerships with leading sports nutrition brands to co develop innovative protein formulations. They also focus on sustainable manufacturing practices to reduce their carbon footprint which appeals to environmentally conscious global customers. Their commitment to scientific validation and customer collaboration enables them to deliver tailored solutions that address specific nutritional necessarys across various international markets.

- Glanbia plc is a leading global nutrition company with a significant presence in the Europe milk protein concentrate market through its optimized production facilities and extensive distribution networks. The company excels in converting raw milk into high value protein ingredients that serve the sports nutrition medical nutrition and general food sectors worldwide. Glanbia recently undertook major capital investments to upgrade its manufacturing plants in Ireland and the United Kingdom enhancing their ability to produce specialized MPC variants efficiently. Their strategy involves vertical integration which allows them to manage costs effectively while ensuring supply security for global clients. The company also focutilizes on innovation by developing clean label protein solutions that align with current consumer trconcludes for natural ingredients. Through continuous expansion of their technical capabilities and strong relationships with key indusattempt players Glanbia maintains a competitive edge and drives growth in the global protein ingredients sector.

Top Strategies Used by the Key Market Participants

Key players in the Europe milk protein concentrate market primarily employ capacity expansion strategies to meet the rising global demand for dairy proteins. Companies frequently invest in state of the art ultrafiltration technologies to improve yield efficiency and product quality. Strategic acquisitions of tinyer regional processors allow major firms to consolidate their supply chains and secure raw milk access. Product innovation remains a central focus with firms developing specialized MPC grades for niche applications like medical nutrition and clear beverages. Sustainability initiatives are increasingly vital as companies adopt carbon neutral manufacturing processes to comply with strict European environmental regulations. Partnerships with conclude utilizers such as sports nutrition brands support manufacturers co create tailored solutions that foster long term loyalty. Additionally, firms emphasize vertical integration to control costs and ensure consistent supply stability amidst volatile raw material prices.

MARKET SEGMENTATION

This research report on the European milk protein concentrate market has been segmented and sub-segmented based on categories.

By Application

- Packaged Products

- Nutritional Products

- Infant Formula

- Others

By Concentration

By Counattempt

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Leave a Reply