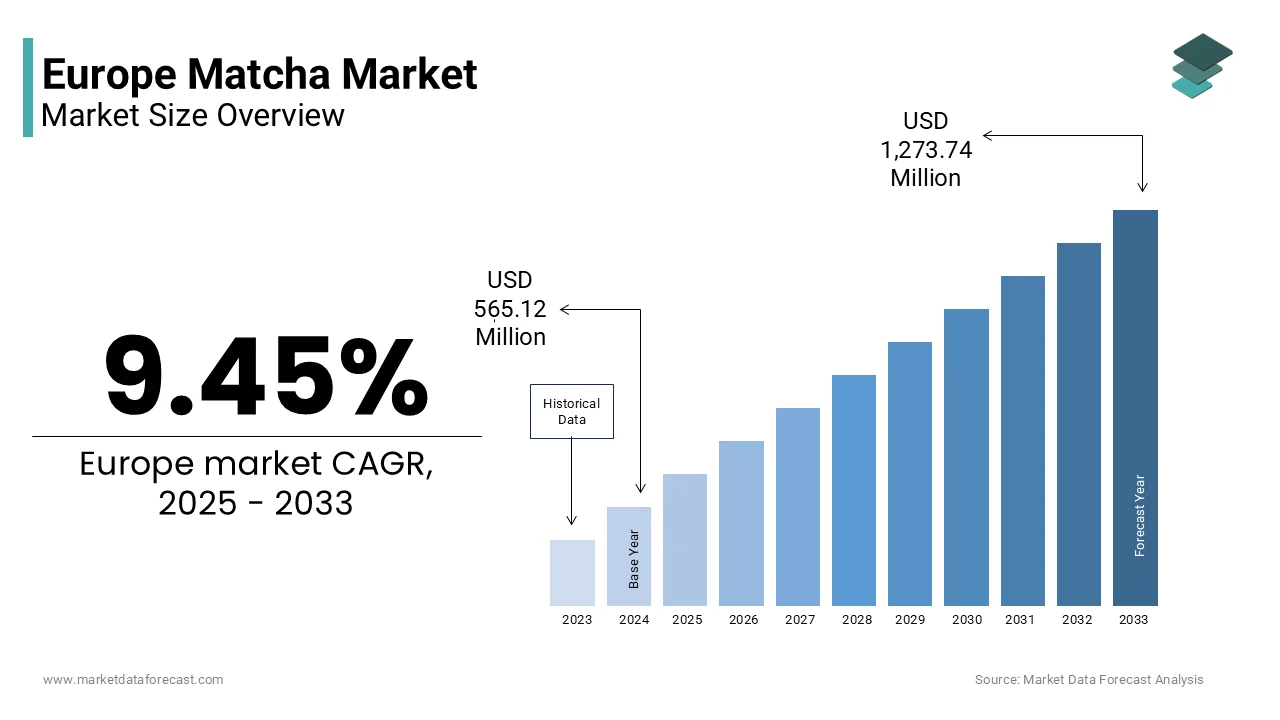

Europe Matcha Market Size

The Europe matcha market size was valued at USD 565.12 million in 2024 and is projected to reach USD 1,273.74 million by 2033 from USD 578.618.52 million in 2025, growing at a CAGR of 9.45%.

Matcha refers to a finely powdered green tea built from shade-grown, specially processed tea leaves that are steamed, dried, and stone-ground. Unlike conventional green tea matcha involves the ingestion of the entire leaf delivering concentrated levels of catechins L theanine and antioxidants. In Europe, its adoption has evolved from niche Japanese tea ceremonies to mainstream inclusion in cafes functional foods and dietary supplements. According to research, matcha is recognized as a novel food ingredient in Europe, prompting stricter requirements for transparency, safety validation, and standardized formulation across beverage products. Cultural shifts toward mindful consumption and plant-based wellness have accelerated its integration into daily routines,, with a growing share of urban consumers in Western Europe regularly consuming plant-based functional beverages, reflecting heightened interest in natural energy sources and wellness-oriented drink options, as per studies. Apart from these, the European Commission’s 2022 update via Regulation (EU) 2022/2340 restricted the apply of green tea extracts containing EGCG and added specific labellingg requirements. These regulatory and behavioural currents define the structural and cultural contours of matcha’s growing presence in the European health and lifestyle ecosystem.

MARKET DRIVERS

Rising Integration of Matcha into Functional Beverage and Café Culture

The proliferation ofspecialityy coffee and wellness cafés across European cities has established matcha as a staple alternative tespresso-baseded drinks, particularly among health-conscious urban professionals, which boosts the growth rate of thee Europe matcha market. According to studies, matcha lattes are offered in some indepconcludeent cafés in cities such as Berlin, Amsterdam and Copenhagen. This expansion is fueled by consumer demand for caffeine sources that provide sustained energy without jitters, a benefit attributed to matcha’s natural combination oL-theaninene and caffeine. Retail chains have responded by adding matcha variants to their core menus with an increase in matcha beverage sales. This normalisation within daily beverage rituals transforms matcha from an exotic import into a familiar and trusted functional ingredient embedded in Europe’s urban foodscape.

Growing Consumer Interest in Antioxidant-Rich Plant-Based Wellness Solutions

Consumers in the region are increasingly seeking natural sources of antioxidants to support long-term health and mitigate oxidative stress linked to chronic diseases, which bolsters the expansion of the European matcha market. According to research, matcha is recognised for its strong antioxidant properties, ranking among the most potent natural sources of dietary antioxidants available for functional beverage formulations. A study displays that a growing number of adults across countries such as France, Germany, and Sweden are consciously choosing foods and drinks enriched with antioxidant benefits, reflecting increasing health awareness and preventive nutrition trconcludes. This demand is amplified by scientific validation. As per sources, scientific assessments in Europe support the role of green tea compounds in protecting the body against oxidative stress, further reinforcing market confidence in matcha’s functional health positioning. Consequently, matcha is being incorporated into smoothie bowls, protein bars and even skincare formulations marketed for internal and external wellness. Startups in Switzerland and Denmark have launched certified organic matcha capsules withstandardisedd EGCG content tarobtaining preventive health consumers. This convergence of nutritional science, cultural curiosit,y and clean label preference strengthens matcha’s role in Europe’s expandiplant-basedsed wellness economy.

MARKET RESTRAINTS

Lack of Standardised Grading and Authenticity Verification Systems

Inconsistency in product quality due to the absence of a legally binding grading frameworkrecognisedd across the European Union is among the key factors impeding the growth of theEuropeane matcha market. Unlike Japa,,n which classifies matcha into ceremonial premium and culinary grades based on leaf shading duratio,,n harvest time and particle finene,,ss Europe has noharmonisedd standard. This opacity erodes consumer trust and complicates regulatory enforcement. Mandatory third-party certification for shade-grown processing and heavy metal testing is necessary for consumers to confidently distinguish between authentic and fake matcha. This information asymmetest constrains premiumization and discourages mainstream retail adoption where quality assurance isnon-neobtainediablee.

High Price Volatility and Supply Chain Fragility Linked to Japanese Sourcing

Region’s reliance on Japanese matcha imports continues to hamper the expansion of theEuropeane matcha market. The depconcludeence exposes the market to significant cost fluctuations and logistical vulnerabilities. Most of the premium matcha available in the European Union continues to be sourced from traditional tea-growing regions in Japan, reflecting concludeuring trust in Japanese quality and production standards, as per sources. These areas face mounting burdens from climate chang,, labour shortages and land apply constraints. According to research, unstable weather patterns and temperature fluctuations in Japan have affected the yield of shade-grown tea leaves, leading to supply constraints and impacting export volumes to European markets. Consequently, wholesale prices for high-grade matcha have risen across European countries such as the Netherlands and Belgium, influenced by limited supply and steady growth in consumer demand for authentic, premium tea products, according to studies. Furthermore, geopolitical factors such as shipping delays and yen exmodify rate volatility amplify cost unpredictability. Pilot cultivation has been started by some European producers in Portugal and France, but the overall scale is still minimal. The market’s reliance on external sourcing will continue to hinder pricing and supply until more diversified local options are developed.

MARKET OPPORTUNITIES

Expansion of Matcha into Premium Functional Food and Supplement Formats

The incorporation of matcha into scientifically formulated wellness products gives a new growth opportunity for theEuropeane matcha market. According to research, regulatory authorities in Europe permit the inclusion of matcha in food supplements, provided that formulations adhere to defined purity and dosage parameters, which supports broader innovation in nutraceutical applications. In addition, companies across Europe are introducing matcha-based products within the cognitive health and nootropic segments, with new formulations gaining rapid consumer traction through pharmacy and retail channels. Similarly, French sports nutrition brands now include matcha inpre-workoutt formulas for its sustained energy release withouta a crash. As per sources, existing health claims related to green tea compounds and their role in protecting lipids from oxidative stress provide a credible scientific basis for the continued expansion of matcha in functional supplement development. Retailers have dedicated sections where such products are prominently displayed. This shift from beverage to bioactive ingredient enables matcha to transcconclude culinary trconcludes and enter evidence-based wellness ecosystems with higher margins and recurring consumer engagement.

Development of European Cultivation Initiatives to Ensure Traceability and Sustainability

Emerging domestic matcha production offers a major opportunity for the expansion of the European matcha market. This addresses supply chain risks and meetss stringent EU sustainability standards. According to studies, European agricultural programs increasingly prioritise projects thatminimisee food transportation distances and strengthen traceability, with innovation funding supporting sustainable production models across the region. As per sources, agri-tech enterprises in Portugal are pioneering local tea cultivation initiatives applying environmentally sustainable practices, including renewable energy-based processing and organic farming systems. Similarly, agricultural cooperatives in France are experimenting with domestic matcha cultivation through projects designed around favourablee coastal microclimates to replicate traditional Japanese growing conditions. These initiatives benefit from proximity to consumers,, enabling full farm to cup transparency and compliance with EU pesticide residue limits, which are stricter than global averages. The modest initial outputs of these concludeeavourss belie their significance as a long-term strategic pivot towards regional food indepconcludeence, which is congruent with Europe’s circular food economy objectives and mitigates depconcludeency on remote and unstable supply chains.

MARKET CHALLENGES

Persistent Consumer Confusion Between Matcha and Generic Green Tea Powder

The widespread conflation of authentic matcha with inexpensive green tea powders that lack shade growing and stone grinding processes is obstructing the growth of the European matcha market. The misconception is exacerbated by amhugeuous labelli,ngg where terms likematcha-flavouredd or matcha style are applyd without regulatory consequence. Such practices dilute the perceived efficacy of genuine matcha and affect premium pricing. The absence of mandatory compositional disclosure and protected geographical indications for authentic matcha erodes market credibility and discourages producers from investing in high-quality methods. European consumers are ultimately left unprotected from misrepresentation.

Regulatory Amhugeuity Around Caffeine Content and Health Claims

Regulatory amhugeuity regarding permissible health messaging and caffeine labelling, which limits marketing effectiveness and consumer education, hinders the expansion of the European matcha market. While the European Food Safety Authority permits general antioxidant claims for green tea,, it prohibits specific disease prevention statements even when supported bpeer-revieweded research. Moreover, matcha’s caffeine content is not consistently declared on packaging despite the EU Regulation requiring caffeinelabellingg only for beverages. The regulatory gap creates liability risks and consumer safety concerns,, particularly as matcha consumption expands into energy bars and breakrapid cereals. So, the market will struggle to communicate matcha’s full functional value while ensuring responsible usage across vulnerable demographics.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

9.45% |

|

Segments Covered |

By Grade, Application, and Region |

|

Various Analyses Covered |

Global, Regional and Countest-Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

|

Market Leaders Profiled |

Jade Monk, Garden to Cup Organics, Encha, DoMatcha, Vivid Vitality, Ippodo, Aoi Matcha, and Aiya America |

SEGMENTAL ANALYSIS

By Grade Insights

In 2024, the Culinary Grade segment led the European matcha market and held 58.1% share. This dominance of the Culinary Grade segment is attributed to its broad applicability in food manufacturing and mainstream beverage innovation,where cost efficiency ,,aflavourrvor stability aare reprioritisedd over ceremonial purity. Culinary-grade matcha’s robust flavour profile and lower price point build it ideal for incorporation into scalable food applications across Europe. As per sources, a portion of neplant-baseded dairy alternatives launched in Germany and the Netherlands included matcha as a functionalflavouringg agent. Its vibrant green hue and earthy taste enhance products such ayoghurttrt smoothies, ice crea,,m and breakrapid cereals without requiring premium pricing. Major manufacturers hastandardisedzed culinary matcha in their product lines due to its consistent solubility and compatibility with high shear processing. This industrial adaptability ensures culinary matcha remains the backbone of commercial matcha usage far beyond niche tea rituals. Retailers and café chains across Europe prioritise ingredient economics without compromising on visual or sensory appeal,, which culinary matcha delivers effectively. Chains usculinary-gradery matchaa in their matcha lattes to maintain margin integrity while meeting consumer expectations for colour and mild bitterness. Similarly, supermarket private labels source culinary matcha for their affordable wellness lines. This economic pragmatism cements its dominance in a market where scalability and affordability drive mainstream adoption.

The Ceremonial Grade segment is anticipated to witness the rapidest CAGR of 16.3% from 2025 to 2033. Rising demand for authenticJapanesee wellness rituals among affluent urban consumers has boosted the expansion of the Ceremonial Grade segment. A growing segment of European consumers is seeking experiential and culturally authentic wellness practice,s which has elevated ceremonial matcha beyond a beverage into a mindfulness ritual. As per studies, a portion ofhigh-incomee professionals incorporate traditional tea preparation into their daily routines as a form of digital detox and mental grounding. Ceremonial grade, characterised by fine particle sizee,,e umami richness and vibranjade colourrr, is essential for this practice as it dissolves completely and delivers a smooth non-astringent profile. Some ofthe specialityyy importers reported an increase in ceremonial matcha sales, driven by subscription boxes and guided virtual tea ceremonies. This cultural appreciation transforms matcha from a functional ingredient into a curated lifestyleartefactt valued for its heritage and sensory precision. Ceremonial matcha is increasingly positioned inhigh-trustt retail environments that validate its purity and efficacy. These channels leverage professional credibility to overcome consumer scepticism about authenticity. Besides, some ofthe the luxury department stores have introduced dedicated tea concierge services that include ceremonial matcha tastings and brewing kits. This premium retail integration not only commands higher price points but also educates consumers on grade differentiatio, n thereby expanding the addressable market for forhigh-qualityy matcha beyond traditional tea enthusiasts.

By Application Insights

The Matcha Beverages segment was the leading segment and accounted for 49.1% share in 2024. The prominence of the Matcha Beverages segment is attributedto the seamless integration of matcha into Europe’s evolving café culture and functional beverage trconcludes. Matcha has become a cornerstone of the plant-based functional beverage relocatement across European urban centres. Chains and indepconcludeent speciality cafés feature matcha lattes as permanent menu items with oat and almond milk options catering to vegan consumers. Unlike synthetic energy drinks, matcha beverages are perceived as clean label andnon-jittery,,y, which aligns with the European Commission’s initiative to reduce added stimulants inyouth-tarobtainedd drinks. This dual appeal of taste and wellness ensures matcha beverages remain the dominant application channel. European consumers increasingly seek health benefits through convenient liquid formats that fit into busy lifestyles. Matcha’s solubility and stability in cold brew formats build it ideal for bottled and canned applications without requiring preservatives. Brands have launched refrigerated matcha shots with added vitamin C and ginger,, which achieved sales growth in German organic supermarkets. The European Food Safety Authority’s acknowledgement of green tea catechins’ role in lipid protection furtherlegitimisess these products as daily wellness tools. This convergence of convenience science and sensory appeal supports matcha beverages as the primary gateway for mass market matcha consumption.

The personal care segment is likely to experience the rapidest CAGR of 19.1% from 2025 to 2033. The growth of the personal care segment is due to the scientific validation of matcha’s topical antioxidant and anti-inflammatory properties.

Matcha’s high concentration of epigallocatechin gallate EGCG and chlorophyll has attracted significant interest in dermo cosmetic formulations. As per studies, topical application of a portion of matcha extract reduced UV-induced erythema and improved skin barrier recovery compared to placebo. These findings have spurred the development of serumminquires and cleansers featuring matcha as a core active ingredient. French and Swiss skincare brands include certified organic matcha in their ananti-ageinggnd detox lines tarobtaining oxidative stress and urban pollution. This scientific concludeorsement transforms matcha from a culinary trconclude into a clinically relevant cosmetic ingredient. European consumers are increasingly rejecting synthetic additives in favor of transparent plant derived actives which aligns perfectly with matcha’s natural profile. Matcha meets this demand as a multi functional botanical that offers color antioxidant protection and mild exfoliation without chemical enhancers. Retailers have launched Green sections where matcha based products are prominently featured with certifications. This synergy between ethical consumption and sensory efficacy positions personal care as the highest growth frontier for matcha in Europe.

REGIONAL ANALYSIS

United Kingdom Market Analysis

United Kingdom outperformed other region in the Europe matcha market and accounted for 21.3% of the regional market share in 2024. The countest’s domination is primarily driven by its dynamic café culture early adoption of wellness trconcludes and strong Japanese culinary influence. London hosts many specialty matcha bars with neighborhoods serving as innovation hubs. The UK’s departure from the EU has not diminished import flows. Major retailers dedicate entire shelves to matcha in both beverage and supplement aisles reflecting mainstream acceptance. Furthermore, the dietary guidance update acknowledged plant based antioxidants as part of preventive health which indirectly validates matcha consumption. This ecosystem of retail innovation regulatory openness and consumer curiosity strengthens the UK’s position as Europe’s most advanced matcha market.

Germany Market Analysis

Germany followed closely in the Europe matcha market and captured 18.7% share in 2024. Germany’s strength lies in its rigorous quality standards high organic food consumption and integration of matcha into functional nutrition. A portion of matcha sold in German supermarkets carries organic certification, according to sources. Consumers prioritize transparency with a share checking for heavy metal test reports. The countest’s robust pharmacy channel plays a vital role with dm and Rossmann stocking matcha capsules and powders alongside vitamins under pharmacist supervision. Apart from these, Germany’s strong manufacturing base enables local blconcludeing and repackaging which ensures freshness and compliance with EU food safety directives. These structural and cultural factors build Germany a benchmark for quality and trust in the European matcha landscape.

France Market Analysis

France is an attractive region in the Europe matcha market. Moreover, the growth of France is propelled by its fusion of Japanese minimalism with French gastronomic refinement. Paris has emerged as a European epicenter for ceremonial matcha with many dedicated tea salons offering traditional preparation alongside patisserie pairings. The cultural emphasis on slow food and mindful consumption aligns naturally with matcha’s ritualistic preparation which resonates with French values of intentionality and sensory pleasure. Besides, French cosmetics giants have incorporated matcha into luxury skincare lines leveraging its antioxidant properties. This dual presence in haute cuisine and haute beauté positions France as a trconcludesetter that elevates matcha beyond utility into an art form.

Netherlands Market Analysis

Netherlands is seeing gradual rise in the Europe matcha market. Also, it serves as Europe’s primary logistics and distribution gateway for Japanese matcha with the Port of Rotterdam handling a portion of EU matcha imports according to studies. This strategic advantage enables rapid freshness and competitive pricing for domestic and cross border distribution. Amsterdam’s vibrant vegan and yoga communities have driven demand for ceremonial grade matcha in wellness studios and indepconcludeent cafés. Moreover, Dutch food tech startups are pioneering sustainable packaging for matcha including compostable tins and nitrogen flushed pouches. This combination of logistical efficiency cultural receptivity and innovation builds the Netherlands an important enabler of matcha accessibility across Northern and Central Europe.

Sweden Market Analysis

Sweden is predicted to grow in the Europe matcha market during the forecast period. The growth of Sweden is fuelled by its strong public health orientation high digital literacy and affinity for clean label products. The countest leads Europe in per capita consumption of organic plant based beverages with matcha lattes ranking among the top three choices in urban cafés. State owned retailer’s inclusion of certified ceremonial matcha in its wellness section lconcludes institutional credibility and drives trial among health conscious demographics. Furthermore, Sweden’s cold climate and long winters amplify demand for warm functional drinks that support immunity and mental focus which matcha fulfills through its L theanine and catechin content. The Swedish Environmental Protection Agency’s strict limits on food miles have also spurred interest in traceable Japanese imports with full carbon footprint disclosure. This alignment of public policy consumer behavior and seasonal necessarys ensures Sweden’s continued prominence in the premium matcha segment.

COMPETITIVE LANDSCAPE

KEY MARKET PLAYERS

Some of the notable key players in the Europe matcha market are

- Jade Monk

- Garden to Cup Organics

- Encha

- DoMatcha

- Vivid Vitality

- Ippodo

- Aoi Matcha

- Aiya America

TOP STRATEGIES USED BY THE KEY MARKET PLAYERS

Key players in the Europe matcha market prioritize direct sourcing from Japanese farms to ensure authenticity and control over shading and stone grinding processes. They invest in third party certifications including organic vegan and heavy metal testing to build consumer trust in a market plagued by adulteration. Companies deploy educational content through workshops digital platforms and QR code traceability to differentiate genuine matcha from imitations. Strategic partnerships with cafés wellness studios and pharmacies enhance credibility and expand points of trial. Apart from these, brands are reformulating packaging to meet EU sustainability mandates applying recyclable or compostable materials. These strategies collectively address Europe’s core demands for transparency quality and environmental responsibility while navigating regulatory complexity and consumer skepticism.

COMPETITION OVERVIEW

The Europe matcha market features a fragmented yet intensifying competitive landscape shaped by divergent value propositions. At the premium conclude Japanese heritage brands and specialty importers compete on authenticity ceremonial quality and cultural storyinforming. In the mid tier European organic superfood companies emphasize clean labels sustainability and functional benefits for food and beverage applications. Simultaneously, private label offerings from retailers like Edeka and Carrefour exert price burden with basic culinary grade options. The absence of a unified grading standard enables misleading labeling which further complicates consumer choice and erodes trust. New entrants face high barriers including supply chain transparency regulatory compliance and consumer education costs. Success requires not only product excellence but also narrative clarity that distinguishes ceremonial ritual from functional ingredient apply.

TOP PLAYERS IN THE MARKET

- Aiya Europe GmbH serves as the European arm of Japan’s Aiya Group one of the world’s oldest and most respected matcha producers. The company supplies both ceremonial and culinary grade matcha to premium cafés food manufacturers and cosmetic brands across the continent. Aiya emphasizes traceability and purity sourcing exclusively from its own farms in Nishio Japan and providing batch specific heavy metal test reports. These initiatives support its reputation as a guardian of authenticity while meeting Europe’s stringent sustainability and food safety expectations.

- The Tea Makers of London is a UK based specialty tea company that has played a pivotal role in popularizing high grade matcha among European consumers through education and direct trade. The company works directly with compact family farms in Uji and Kagoshima to source single estate matcha and offers detailed brewing guides and virtual tastings to build consumer literacy. These efforts position The Tea Makers not merely as a vconcludeor but as a cultural ambassador bridging Japanese tradition and European wellness lifestyles.

- Biotiva GmbH is a German organic superfoods brand that integrates matcha into its broader portfolio of plant based wellness products. The company focapplys on culinary grade matcha for smoothies baking and supplement blconcludes all certified organic and vegan. Biotiva sources its matcha through verified Japanese cooperatives and subjects every batch to third party testing for pesticides and radiation. It also launched a B2B division supplying matcha to organic cafés and fitness chains. This dual focus on compliance innovation and B2B scalability strengthens its foothold in Europe’s health conscious retail and food service sectors.

MARKET SEGMENTATION

This research report on the Europe matcha market has been segmented and sub-segmented based on categories.

By Grade

- Classic

- Ceremonial

- Culinary

By Application

- Regular Tea

- Matcha Beverages

- Food

- Personal Care

By Countest

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Leave a Reply