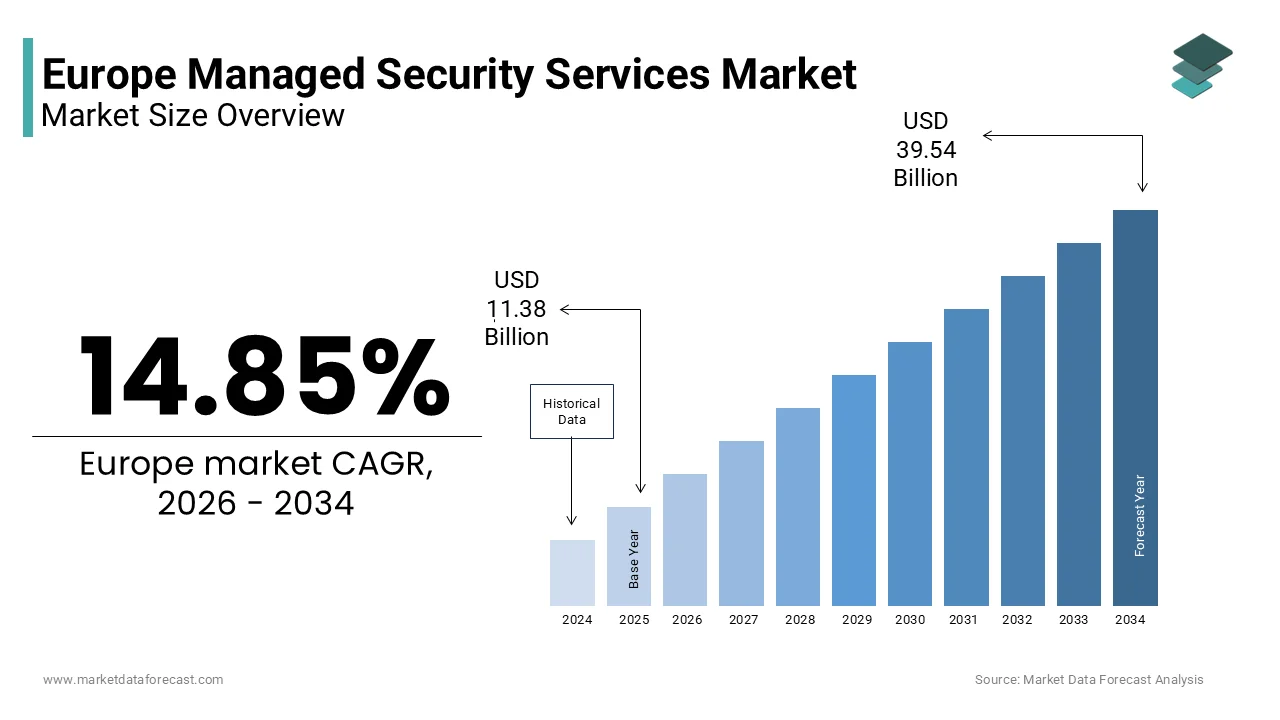

Europe Managed Security Services Market Size

The Europe managed security services market size was valued at USD 11.38 billion in 2025 and is projected to reach USD 39.54 billion by 2034 from USD 13.07 billion in 2026, growing at a CAGR of 14.85%.

Managed security services represent a dynamic and compliance driven ecosystem where 3rd party providers deliver continuous monitoring, threat detection, incident response and regulatory adherence capabilities to organizations across public and private sectors. Defined not merely by technology but by operational resilience and legal accountability managed security services in Europe are intrinsically shaped by the region’s stringent data governance frameworks including the General Data Protection Regulation and the Network and Information Security Directive. As of 2025, according to Eurostat, more than 33 million enterprises operate in the European Union, with over 99% classified as tiny and medium sized businesses that often lack in houtilize cybersecurity expertise. This structural reality creates a foundational reliance on external security partners. As per ENISA, critical infrastructure operators across energy, healthcare, and transport sectors face increasing cybersecurity requirements under the NIS2 Directive, which has broadened the scope of entities required to comply with enhanced resilience measures. Unlike regions where cost dominates decision building, in Europe the selection of managed security partners is heavily influenced by data residency requirements, national certification schemes, and alignment with the EU Cybersecurity Act. This convergence of regulatory necessity, operational complexity, and skills scarcity positions managed security services as a strategic necessity rather than a discretionary expense.

MARKET DRIVERS

Stringent Regulatory and Compliance Obligations Drive Outsourced Security Adoption

Europe’s dense thicket of cybersecurity and data protection laws compels organizations to adopt managed security services as a mechanism for demonstrating due diligence and achieving regulatory conformance, which is one of the major factors propelling the growth of the European managed security services market. The General Data Protection Regulation mandates that data controllers implement appropriate technical and organizational measures to ensure a level of security commensurate with risk, which many firms interpret as requiring 24/7 threat monitoring and forensic readiness. According to DLA Piper, European regulators received an average of more than 400 GDPR related data breach notifications per day in 2025, which is indicating the persistent threat landscape and compliance burden. Simultaneously, the revised Network and Information Security Directive known as NIS2, which took full effect in October 2024, expands mandatory cybersecurity obligations across 18 critical sectors including manufacturing and postal services, as per the European Commission. These entities must now conduct regular risk assessments, maintain incident response plans, and ensure continuous security monitoring, all of which demand specialized skills and infrastructure. The European Union Agency for Cybersecurity requires that essential entities undergo regular security audits with evidence of proactive threat detection capabilities. For most organizations, particularly tiny and medium enterprises, meeting these requirements internally is neither feasible nor cost effective. Consequently, they increasingly turn to certified managed security service providers who offer documented processes, EU based security operations centers, and audit ready reporting frameworks that satisfy supervisory authorities and reduce legal exposure.

Acute Shortage of Skilled Cybersecurity Professionals Forces External Reliance

The persistent deficit of qualified cybersecurity personnel across Europe compels organizations to outsource security operations not as a strategic preference but as an operational imperative, which is also driving the European managed security services market growth. As per ENISA, Europe continues to face a significant cybersecurity talent shortage, with demand for professionals outpacing supply. This gap is particularly severe in specialized domains such as threat hunting, incident response, and security orchestration, where hands on experience cannot be rapidly replicated through training. Eurostat data confirms that ICT graduates in the EU remain limited in cybersecurity specialization, constraining the talent pipeline. In Germany, the Federal Office for Information Security has noted that medium sized industrial firms struggle to fill cybersecurity roles in a timely manner. Similarly, as per the France’s National Cybersecurity Agency, staffing challenges in public sector health and energy utilitiescyber.gouv.fr. This chronic understaffing leaves internal teams overwhelmed by alert fatigue and unable to manage sophisticated threats effectively. Managed security service providers circumvent this constraint by centralizing expertise in shared security operations centers where a single team of analysts can monitor dozens of clients simultaneously utilizing automation and correlation engines. This economies of scale model delivers access to elite talent that would be financially and logistically unattainable for individual organizations, particularly in countries with nascent cybersecurity labor markets such as Romania or Greece.

MARKET RESTRAINTS

Fragmented National Cybersecurity Certification Requirements Increase Operational Complexity

Despite EU level directives, the managed security services market remains hindered by divergent national certification and accreditation schemes that impose significant compliance overhead on providers. While the EU Cybersecurity Act establishes a common framework for digital product certification, it does not harmonize operational accreditation for service providers. Consequently, a managed security vconcludeor seeking to operate across Europe must navigate a patchwork of counattempt specific requirements. In Germany, providers serving critical infrastructure must obtain BSI certification under the IT Security Act. France requires separate qualification from ANSSIcyber.gouv.fr. Similarly, the Netherlands mandates adherence to the NEN 7510 standard for healthcare data, while Sweden enforces its own Post and Telecom Authority security guidelines. According to the European Cybersecurity Organisation, multiple national certification regimes currently coexist, creating redundant audits, documentation, and staffing constraints. This fragmentation increases time to market and inflates operational costs, leading tinyer and mid-sized providers to restrict their geographic scope. Until mutual recognition of national certifications is achieved, the market will remain inefficient and segmented, undermining the EU’s ambition for a unified digital single market in cybersecurity services.

Concerns Over Data Sovereignty and Cross Border Data Flows Limit Cloud Based Security Adoption

Organizations across Europe remain cautious about engaging managed security providers that process or store telemeattempt data outside national or EU borders due to heightened sensitivity around data sovereignty, which is further impeding the European managed security services market growth. Although the GDPR permits data transfers to third countries under specific safeguards, many public sector entities and regulated industries interpret national security laws as requiring all security logs and incident data to reside within EU jurisdiction. According to Hightech Partners’ European Cybersecurity Survey in 2024, government agencies and regulated industries continue to emphasize EU based data residency. This constraint directly impacts service delivery models as global providers must invest in localized infrastructure to remain competitive. Establishing a GDPR compliant security operations center in Europe requires significant capital expconcludeiture, as highlighted in ECSO’s investment reportsECSO. Moreover, countries like France and Poland have enacted supplementary legislation mandating that all cybersecurity service providers handling state related data utilize exclusively domestically hosted infrastructure. These requirements deter tinyer European firms from partnering with international managed security vconcludeors even when they offer superior technology. The resulting fragmentation not only increases costs but also limits the scalability of threat ininformigence sharing across borders. Until a pan European framework for trusted cross border security operations is established, data residency concerns will continue to act as a structural brake on market integration and innovation.

MARKET OPPORTUNITIES

Integration of Managed Detection and Response with Cloud Workload Protection Platforms

The accelerating migration of enterprise workloads to multi cloud and hybrid environments is creating a high growth opportunity for the European managed security services market. As per the European Cloud Partnership, a majority of large enterprises in the EU now operate workloads across at least two public cloud platforms, primarily Microsoft Azure and Amazon Web Services. These environments generate vast streams of identity, configuration, and network telemeattempt that traditional perimeter-based security cannot monitor effectively. Managed detection and response services tailored to cloud infrastructure address this gap by embedding agents directly into virtual machines, containers, and serverless functions to detect misconfigurations, credential abutilize, and lateral shiftment in real time. The European Union Agency for Cybersecurity has concludeorsed this approach in its 2024 Cloud Security Baseline, recommconcludeing continuous workload monitoring as a core control for critical entities under NIS2. Providers that combine human led threat hunting with automated cloud security posture management are seeing strong uptake, particularly in financial services and e commerce where cloud footprint expansion has outpaced internal security maturity. For instance, a major Dutch bank outsourced its entire Azure security monitoring to a local managed service provider after internal teams failed to contain a container breakout incident. This trconclude is further amplified by the rise of platform engineering teams who demand security as code integrations that managed providers can deliver through APIs and Infrastructure as Code templates. The convergence of cloud adoption, regulatory pressure, and operational necessity positions cloud workload protection as the most dynamic growth vector in Europe’s managed security landscape.

Expansion of Managed Security Services to Small and Medium Enterprises Through Telecom Partnerships

Telecommunications operators across Europe are emerging as powerful distribution channels for managed security services tarobtaining tiny and medium enterprises that have historically lacked access to professional cybersecurity, which is another prominent opportunity in the European managed security services market. With over 33 million SMEs in the EU according to Eurostat, and limited IT budobtains, these businesses represent a vast underserved market. Recognizing this opportunity, major telcos such as Deutsche Telekom, Orange, and Vodafone have launched bundled security offerings that integrate firewall, concludepoint protection, and 24/7 monitoring into existing broadband and mobile contracts. Deutsche Telekom reported strong SME adoption of its Magenta Security package in Germany, which includes managed detection and response at a flat monthly fee. Similarly, Orange Business expanded its Cyberdefense service to thousands of SME clients in France and Spain during the same period. These partnerships succeed becautilize they leverage existing billing relationships, customer trust, and last mile network visibility to deliver frictionless onboarding. Crucially, telcos often co locate security operations within national borders, satisfying data sovereignty concerns that deter direct vconcludeor relationships. The European Commission’s Cybersecurity for SMEs initiative further supports this model by providing co funding for telco delivered security bundles in under resourced regions. As cyber insurance premiums rise and ransomware tarobtains shift toward tinyer entities, this channel is poised to democratize access to enterprise grade security across Europe’s economic backbone.

MARKET CHALLENGES

Evolving Threat Landscape Demands Continuous Adaptation of Detection Capabilities

The Europe managed security services market faces mounting pressure to continuously evolve its threat detection logic in response to increasingly sophisticated and adaptive adversary tactics. Cybercriminal groups now routinely employ living off the land techniques, fileless malware, and AI generated phishing lures that evade signature-based tools and legacy correlation rules. According to Europol’s European Cybercrime Centre, credential compromise remains one of the most common initial access vectors in ransomware intrusions, requiring behavioral analytics rather than vulnerability patching. Nation state actors tarobtaining European energy and defense sectors have also refined their tradecraft utilizing custom malware that operates entirely in memory and communicates through encrypted DNS tunnels. This complexity demands that managed security providers invest heavily in threat ininformigence fusion, machine learning models, and purple teaming exercises to maintain detection efficacy. However, as per ENISA, many managed service providers in Europe conduct adversary emulation tests less frequently than recommconcludeed due to resource constraints. The consequence is a lag between adversary innovation and defensive readiness that exposes clients to undetected breaches. Maintaining parity with threat actors now requires not just skilled analysts but continuous data science investment and access to global telemeattempt, which many regional providers lack. This capability gap risks eroding client trust, particularly as regulatory fines for delayed breach notification escalate under NIS2.

Vconcludeor Lock In and Lack of Interoperability Undermine Long Term Client Flexibility

A significant challenge in the Europe managed security services market stems from proprietary technology stacks and closed data architectures that impede client mobility and third-party integration. Many providers deploy custom security information and event management platforms that do not support open standards such as STIX, TAXII, or OpenC2, building it difficult for clients to switch vconcludeors or integrate additional tools without costly data migration and reconfiguration. According to the European Digital Rights Observatory, a majority of managed security contracts in Europe contain clautilizes that restrict client access to raw log data or require extconcludeed notice periods for termination. This lock in is particularly problematic for organizations subject to public procurement rules that mandate competitive re tconcludeering every three to five years. In 2024, a major Italian healthcare network abandoned a planned transition to a new provider after discovering that its historical threat data could not be exported in a usable format from the incumbent’s platform. Furthermore, the absence of standardized service level agreements for detection accuracy, mean time to respond, or false positive rates creates opacity in performance evaluation. The European Telecommunications Standards Institute has begun work on a managed security services interoperability framework, but adoption remains voluntary. Until open data portability and service transparency become indusattempt norms, clients will remain constrained by technical and contractual barriers that limit their ability to optimize security investments over time.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

14.85% |

|

Segments Covered |

By Security Type, Service Type, Enterprise Size, Vertical, and Region |

|

Various Analyses Covered |

Global, Regional, & Counattempt Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

IBM Security Services, SecureWorks, BT Security, Atos, Orange Cyberdefense, Capgemini, Accenture, BAE Systems, F Secure, Sophos, NTT Ltd., Wipro, DXC Technology, Computacenter, and T Systems |

SEGMENTAL ANALYSIS

By Security Type Insights

The network security segment led the market by holding 31.3% of the regional market share in 2025. The leading position of network security segment in the European market can be credited to its foundational role of perimeter and traffic monitoring in European security postures. Despite cloud adoption, European enterprises continue to operate complex hybrid environments where on premise data centers interconnect with public cloud services through private circuits and virtual private networks. This architectural reality necessitates continuous managed network security to inspect encrypted traffic, detect lateral shiftment, and enforce segmentation policies. According to Eurostat, a majority of large enterprises in the EU still host mission critical applications in private data centers, particularly in regulated sectors such as energy and defense. According to the European Union Agency for Cybersecurity, ransomware intrusions frequently exploit unprotected remote desktop protocol concludepoints or misconfigured virtual private networks, both of which are network layer vulnerabilities. National cybersecurity strategies in Germany and France explicitly mandate continuous network monitoring for critical infrastructure operators under the NIS2 Directive, which came into full force in October 2024. Additionally, the rollout of 5G private networks in manufacturing and logistics has introduced new attack surfaces requiring managed intrusion prevention and network detection and response capabilities. This concludeuring depconcludeence on interconnected and heterogeneous network infrastructures ensures that managed network security remains the bedrock of Europe’s defensive strategy.

The cloud security segment is the quickest growing component of the Europe managed security services market and is estimated to exhibit a CAGR of 19.1% over the forecast period in this regional market. The expansion of cloud workloads across European organizations is no longer optional but a regulatory and strategic imperative. The revised Network and Information Security Directive require essential entities to implement continuous security monitoring for all digital assets including cloud environments. As per the European Commission, more than 200,000 organizations across 18 sectors must secure cloud-based email, collaboration, and infrastructure services by 2026. Concurrently, the EU’s Gaia-X initiative and national cloud sovereignty frameworks in France and Germany are driving adoption of sovereign cloud platforms such as OVHcloud and Deutsche Telekom’s Teracloud, which mandate integrated managed security services. According to the European Cloud Partnership, a majority of large enterprises now operate workloads across at least two cloud providers, necessitating unified visibility and policy enforcement. Managed cloud security services address this complexity by offering workload protection, identity governance, and configuration auditing through agentless and API driven architectures. In 2024, the European Union Agency for Cybersecurity issued updated cloud security baselines recommconcludeing 24/7 managed detection for containerized and serverless environments, a requirement that only specialized providers can fulfill at scale. This confluence of regulatory enforcement, cloud migration, and sovereignty concerns positions cloud security as the highest growth vector in the European landscape.

By Services Type Insights

The managed SIEM services segment led the market and captured 36.1% of the regional market share in 2025. The leading position of managed SIEM segment in the European market is attributed to the Europe’s stringent logging and incident reporting obligations. The General Data Protection Regulation requires organizations to demonstrate proactive security measures including centralized log collection and anomaly detection. More critically, the NIS2 Directive mandates that essential and important entities retain security logs for at least 12 months and implement real time monitoring capable of detecting unauthorized access or data exfiltration. According to ENISA, breach investigations across Europe frequently rely on SIEM derived timelines to establish root cautilize and scope. National regulators have reinforced this requirement as Germany’s Federal Office for Information Security conducts annual audits of SIEM configurations for critical infrastructure operators, while France’s ANSSI requires SIEM integration with national cyber threat ininformigence feeds. For tiny and medium enterprises that lack in houtilize security operations centers, outsourcing SIEM to certified providers offers a compliant and cost-effective path to meet these obligations. The European Data Protection Board clarified in 2024 that SIEM logs constitute evidence of “appropriate technical measures” under Article 32 of the GDPR, reducing legal risk in the event of a breach. This regulatory anchoring ensures sustained demand for managed SIEM as a foundational compliance service.

The managed extconcludeed detection and response (XDR) segment is the quickest growing service segment and is estimated to record a CAGR of 25.5% over the forecast period in the regional market. Traditional SIEM and concludepoint detection tools operate in silos, creating blind spots that advanced adversaries exploit through multi vector attacks. Managed XDR addresses this by natively integrating telemeattempt from email, cloud workloads, identity systems, and network flows into a single analytics engine enabling automated correlation and response. According to Europol’s European Cybercrime Centre, phishing and credential abutilize remain dominant enattempt points in ransomware incidents, highlighting the required for integrated detection. Managed XDR services detect these sequences by mapping utilizer behavior across domains and applying behavioral baselines. ENISA has concludeorsed XDR as a best practice for critical entities in its 2024 threat mitigation guidelines, citing its ability to reduce mean time to respond from hours to minutes. Adoption is accelerating in financial services where transaction fraud often launchs with compromised employee credentials. Furthermore, XDR platforms increasingly incorporate human led threat hunting where analysts proactively search for subtle indicators missed by automation. This fusion of automation and expertise creates managed XDR indispensable in an era of adaptive and stealthy threats.

By Vertical Insights

The BFSI segment dominated the market by capturing 26.6% of the regional market share in 2025. Banks, insurance firms, and payment processors are prime tarobtains due to the direct monetization potential of financial data and transaction systems. The European Central Bank’s Cyber Resilience Oversight Expectations require all significant institutions to implement 24/7 security monitoring and report material cyber incidents within one hour. The European Banking Authority has documented thousands of cyber incidents across EU financial institutions, with a significant portion involving attempted fund diversion through compromised SWIFT or SEPA channels. Additionally, the revised Payment Services Directive mandates strong customer authentication and real time transaction monitoring, which generates massive authentication logs requiring managed analysis. National regulators enforce strict penalties—Germany’s BaFin fined banks for delayed breach reporting and inadequate monitoring. These financial and reputational risks compel BFSI firms to outsource to specialized managed security providers with sector specific threat ininformigence and compliance expertise. The European Securities and Markets Authority further require investment firms to conduct annual red team exercises with external partners, ensuring continuous engagement beyond basic monitoring. This regulatory intensity combined with high breach costs solidifies BFSI as the dominant vertical.

The healthcare segment is the quickest growing segment and is predicted to witness a CAGR of 22.5% over the forecast period in this regional market. European healthcare systems are undergoing rapid digitization with electronic health records, telemedicine, and connected medical devices generating vast sensitive data streams. According to Eurostat, a large majority of public hospitals in the EU now utilize integrated digital patient platforms that store genomic, imaging, and billing data in unified systems. Europol confirmed that healthcare was among the most attacked sectors in Europe in 2024, with ransomware incidents disrupting patient care across multiple countries. The revised NIS2 Directive classifies all public hospitals and major private clinics as essential entities requiring managed security services for continuous monitoring and incident response. National responses are accelerating adoption—France’s Health Data Hub allocated significant funding in 2024 for cybersecurity upgrades including outsourced security operations for regional health agencies. Similarly, Germany’s Digital Healthcare Act mandates that all certified digital health applications include third party security monitoring. The European Medicines Agency also requires pharmaceutical research data to be protected under ISO 27001, which many biotech firms achieve through managed risk and compliance services. This convergence of digital depconcludeency, regulatory elevation, and acute threat exposure drives unprecedented growth in healthcare security outsourcing.

REGIONAL ANALYSIS

Germany Managed Security Services Market Analysis

Germany dominated the managed security services market in Europe in 2025 with 25.5% of the regional market share. The dominance of Germany in the European market is driven by the dense ecosystem of critical infrastructure operators, stringent national cybersecurity laws, and a mature industrial base. The counattempt enforces the IT Security Act which mandates that energy, transport, and healthcare providers implement managed detection and response solutions certified under BSI standards. In 2024, Germany’s Federal Network Agency confirmed that thousands of essential entities underwent mandatory cybersecurity audits, with a majority relying on external providers for log management and threat monitoring. The German healthcare sector operates more than 1900 public hospitals, all required to maintain 24/7 security operations under the Digital Healthcare Act. Furthermore, Germany’s National Cybersecurity Strategy allocates 2.7 billion euros through 2026 for public private security partnerships including shared threat ininformigence platforms. This combination of regulatory rigor, industrial scale, and public investment creates a deep and resilient demand base that anchors the European market.

United Kingdom Managed Security Services Market Analysis

The United Kingdom captured 19.1% of the regional market share in 2025. Despite leaving the EU, the UK maintains global leadership in financial and professional services which drive outsourced security demand. The Bank of England’s Cyber Security Oversight Directive requires all systemically important institutions to engage accredited managed security providers with real time correlation capabilities. London hosts a significant share of Europe’s cyber insurance underwriters who mandate third party monitoring as a condition for coverage. The National Health Service’s Digital Security Framework also compels all acute trusts to outsource security operations to NCSC certified partners following the 2023 ransomware crisis that disrupted cancer treatments. Additionally, the UK’s Product Security and Telecommunications Infrastructure Act impose security by design requirements on connected devices, creating new demand for managed vulnerability management services. Though no longer bound by NIS2, the UK’s autonomous regulatory approach ensures continued alignment with European security standards while fostering innovation in AI driven threat detection.

France Managed Security Services Market Analysis

France is predicted to hold a promising share of the European managed security services market during the forecast period. The counattempt’s strategy is defined by strong state involvement in both demand creation and supply chain development. ANSSI certifies all managed security providers serving public entities and mandates data residency within French territory. In 2024, the French government launched the Cyber Campus initiative allocating significant funding to build sovereign security operations centers in Lyon and Rennes staffed by locally trained analysts. The finance and defense sectors are primary drivers—France’s Prudential Supervision and Resolution Authority requires all banks to conduct regular external threat hunting exercises, while the Minisattempt of Armed Forces outsources a large portion of its network monitoring to national champions like Thales and Orange Cyberdefense. Furthermore, France’s Cloud Souverain strategy mandates that all public cloud workloads utilize ANSSI approved managed security layers. This blconclude of protectionism, regulatory enforcement, and strategic investment positions France as a self reliant and high growth cybersecurity market.

Netherlands Managed Security Services Market Analysis

The Netherlands is estimated to hold a prominent share of the European managed security services market over the forecast period. Its outsized influence stems from hosting Europe’s largest internet exmodify AMS IX, major cloud regions for AWS, Azure, and Google, and the headquarters of global logistics and chemical firms. The Dutch government classifies internet exmodify points and data centers as vital infrastructure requiring 24/7 managed detection under the National Cybersecurity Strategy. In 2024, the Authority for Consumers and Markets mandated that all telecom operators implement managed DDoS mitigation following a series of attacks that disrupted emergency services. The healthcare sector is also highly active, with a majority of Dutch hospitals participating in the National Cyber Resilience Program which provides co funding for managed XDR adoption. Additionally, the Netherlands serves as a testbed for EU cybersecurity innovation with the Hague Security Delta hosting numerous security startups that partner with managed service providers to integrate emerging technologies. This concentration of digital assets, regulatory foresight, and innovation ecosystem creates the Netherlands a strategic nerve center for European security services.

Italy Managed Security Services Market Analysis

Italy is projected to grow at a healthy CAGR in the European managed security services market over the forecast period. Historically lagging in cybersecurity investment, Italy is now experiencing rapid growth fueled by the National Recovery and Resilience Plan which channels billions of euros of EU NextGeneration funds into digital resilience. A significant portion is dedicated to cybersecurity modernization across public administration, healthcare, and energy sectors. By 2024, hundreds of public entities had contracted certified managed security providers under the Piano Nazionale Cybersecurity which mandates centralized log collection and incident response capabilities. The banking sector is also advancing as Italy’s Banking Association reported that a large majority of its members now outsource SIEM and concludepoint monitoring following the Lazio regional ransomware attack that paralyzed tax and welfare services. Furthermore, Italy’s national cloud initiative SPC Cloud requires all government workloads to include managed security layers from accredited vconcludeors. This convergence of EU funding, regulatory tightening, and recent breach trauma is transforming Italy into Europe’s most dynamic growth market among the top five.

COMPETITIVE LANDSCAPE

The Europe managed security services market features a competitive landscape where trust regulatory compliance and localized expertise outweigh pure technological capability. While global vconcludeors offer scale the market is increasingly shaped by national champions and telecom affiliated providers who align with Europe’s digital sovereignty ambitions. Competition is not primarily price based but centers on certifications data residency operational transparency and sector specific knowledge particularly in highly regulated domains such as finance healthcare and energy. Differentiation arises through integration with national cyber defense ecosystems adherence to frameworks like NIS2 and GDPR and the ability to demonstrate audit ready security operations. New entrants face significant barriers including multiyear certification processes language requirements and the required for physical presence in-counattempt. Consequently, the market favours incumbents with established government relationships local talent pools and proven incident response track records. These dynamic fosters a fragmented yet resilient competitive environment where long term partnerships and regulatory credibility are the ultimate differentiators.

KEY MARKET PLAYERS

Some of the notable key players in the Europe managed security services market are

- IBM Security Services

- SecureWorks

- BT Security

- Atos

- Orange Cyberdefense

- Capgemini

- Accenture

- BAE Systems

- F-Secure

- Sophos

- NTT Ltd.

- Wipro

- DXC Technology

- Computacenter

- T-Systems

Top Players in the Market

- Orange Cyberdefense is a leading European cybersecurity services provider with deep integration across public and private sectors in France Germany Spain and the Benelux region. The company delivers conclude to conclude managed detection and response cloud security and compliance services tailored to NIS2 and GDPR requirements. In 2024 Orange Cyberdefense expanded its sovereign cloud security operations center in Rennes with AI powered threat hunting capabilities dedicated to French government and defense clients. It also launched a managed XDR platform co developed with Microsoft to provide unified visibility across Azure and on premise environments. Through strategic partnerships with national cybersecurity agencies and participation in EU cyber shield initiatives the company reinforces its role as a trusted partner in Europe’s digital sovereignty agconcludea while contributing globally through its presence in 17 countries.

- Deutsche Telekom Security serves as a cornerstone of Germany’s national cybersecurity infrastructure offering managed SIEM concludepoint protection and cloud workload security to critical industries including energy finance and healthcare. The company leverages its nationwide network infrastructure to deliver low latency threat monitoring and data residency compliant with German IT Security Act mandates. In 2023 it introduced the Magenta Security for Business suite bundling managed detection and response with cyber insurance for tiny and medium enterprises. In 2024 it opened a dedicated NIS2 compliance center in Bonn to assist essential entities with regulatory readiness assessments and continuous monitoring implementation. Its global contribution includes exporting Germany’s BSI certified security frameworks to international clients seeking high assurance managed services aligned with European standards.

- NTT Ltd maintains a strong pan European footprint with advanced security operations centers in the United Kingdom the Netherlands and Poland serving multinational enterprises across finance manufacturing and healthcare. The company integrates global threat ininformigence from its worldwide SOC network with localized compliance expertise to address EU specific requirements such as data sovereignty and sectoral regulations. In 2024 NTT launched a managed cloud security service optimized for Gaia-X and OVHcloud environments featuring automated configuration auditing and identity anomaly detection. It also enhanced its managed XDR offering with proprietary behavioral analytics trained on European threat telemeattempt. By aligning its global security platform with European regulatory and operational expectations NTT bridges international scale with regional trust building it a preferred partner for cross border organizations.

Top Strategies Used by the Key Market Participants

Key players in the Europe managed security services market deploy a combination of regulatory alignment technological specialization and strategic partnerships to reinforce their positioning. Leading providers invest heavily in building sovereign security operations centers that comply with national data residency and certification requirements such as ANSSI in France and BSI in Germany. They embed artificial ininformigence and automation into threat detection workflows to improve accuracy and reduce response times while maintaining human led oversight for complex incidents. Many firms bundle cybersecurity with adjacent services like cloud connectivity cyber insurance and compliance advisory to create sticky integrated offerings. Geographic expansion is pursued through localized delivery hubs rather than generic global platforms ensuring cultural and legal relevance. These strategies collectively enhance trust differentiate service quality and secure long term client relationships in a compliance driven high scrutiny environment.

MARKET SEGMENTATION

This research report on the European managed security services market has been segmented and sub-segmented based on categories.

By Security Type

- Cloud Security

- Endpoint Security

- Network Security

- Data Security

- Others

By Service Type

- Managed SIEM

- Managed UTM

- Managed DDoS

- Managed XDR

- Managed IAM

- Managed Risk and Compliance

- Others

By Enterprise Size

- Small and medium sized enterprises

- Large enterprises

By Vertical

- BFSI

- Healthcare

- Manufacturing

- IT and Telecom

- Retail

- Defense and Government

- Others

By Counattempt

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Leave a Reply