Europe Luxury Real Estate Market Size

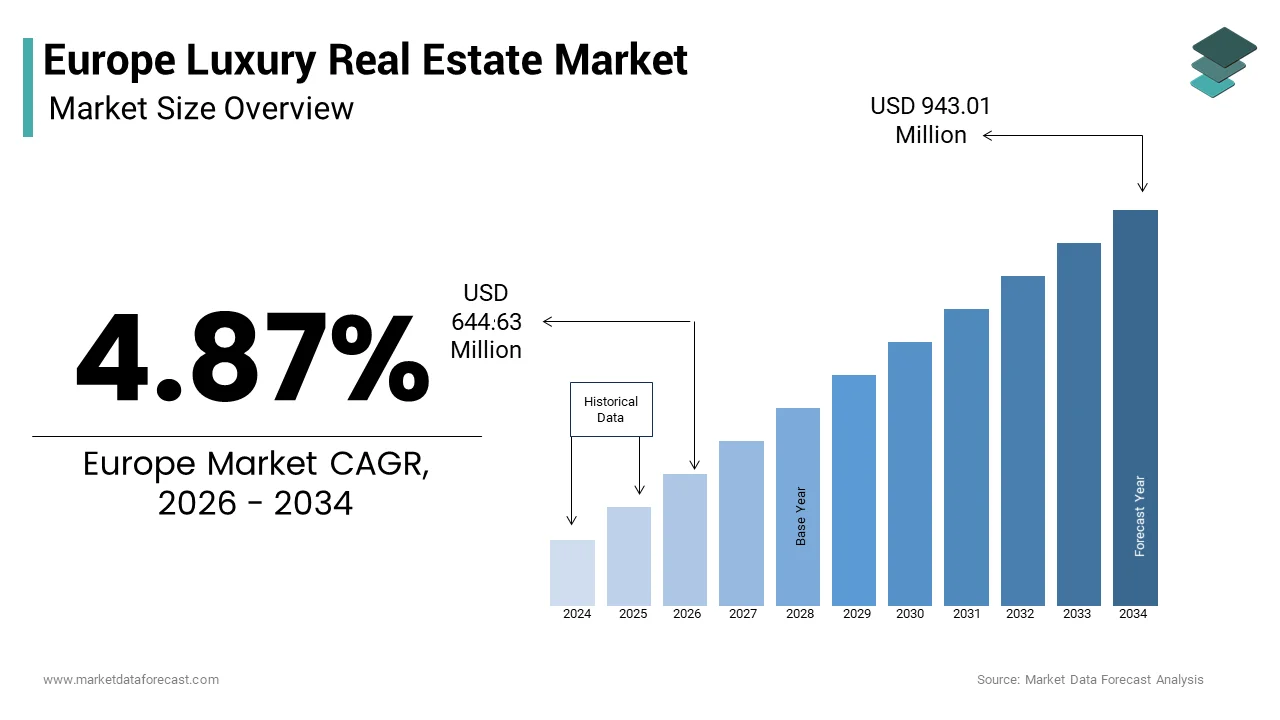

The Europe luxury real estate market size was valued at USD 614.69 million in 2025 and is anticipated to reach USD 644.63 million in 2026 to reach USD 943.01 million by 2034, growing at a CAGR of 4.87% during the forecast period from 2026 to 2034.

Luxury real estate is defined by exclusivity, scarcity, and lifestyle rather than just a price tag. It represents a level of living that goes far beyond the “standard” or “premium” categories found in the general market. This sector transcfinishs basic shelter to represent a store of value, a lifestyle statement, and a strategic asset for global capital. Definitions vary by city, yet generally include properties in the top 5% of pricing within major metropolitan areas such as London, Paris, Monaco, and Geneva. In 2024, Knight Frank emphasized that the number of Ultra High Net Worth Individuals in Europe remained substantial (part of a global total of 626,619), providing a base of potential purchaseers with a net worth exceeding 30 million USD, although wealth creation in the region lagged behind North America and the Middle East. Furthermore, data from Eurostat and market analyses indicates that while foreign direct investment in real estate activities within the EU revealed signs of stabilization in 2024 following a sharp downturn, transaction volumes remained significantly below 2022 levels, reflecting a market recovering from broader economic headwinds rather than one that remained fully resilient. The European Central Bank initiated a cycle of interest rate cuts in mid-2024 to support the economy as inflation eased. Despite the impact of previously high rates on the broader houtilizing market, the luxury segment demonstrated relative insulation; Savills noted that high-value markets like Monaco remained active, with the districts of Monte Carlo and La Rousse accounting for over 60% of resale transactions, while cash purchaseers continued to play a dominant role in prime markets. This market is increasingly defined by sustainability credentials and smart home integration, reflecting a shift where legacy and location must coexist with modern environmental standards and digital connectivity to retain value.

PRIMARY MARKET DRIVERS

Influx of Global Capital Seeking Safe Haven Assets and Currency Diversification

Persistent geopolitical instability and currency volatility are affecting various global regions, which fuels the growth of the Europe luxury real estate market. These factors drive affluent investors to view European luxury real estate as a paramount safe haven for wealth preservation. High net worth individuals from emerging markets and conflict zones prioritize assets in stable jurisdictions like Switzerland, the United Kingdom, and France to protect capital from depreciation and political risk. According to sources, global wealth is increasingly gravitating toward North America and parts of Asia, while the growth of the millionaire population in Western Europe has slowed relative to these regions. The strength of the Euro and the Swiss Franc against fluctuating currencies further incentivizes acquisitions, as purchaseers leverage favorable exmodify rates to acquire premium assets at relative discounts. International investors are playing an even larger role in the top tier of the European property market than they were in previous decades. These investors often bypass financing hurdles by utilizing cash, insulating the sector from rising mortgage rates. The perception of European cities as culturally rich, politically stable, and legally secure environments ensures a continuous demand pipeline. As global uncertainty persists, the flight to quality intensifies, reinforcing the position of prime European property as a critical component of diversified global investment portfolios.

Scarcity of Prime Inventory and Historical Architectural Significance

The finite supply of properties in historically significant and geographically superior locations acts as a powerful driver for value appreciation and sustained demand within the Europe luxury real estate market. Unlike standard houtilizing, prime real estate in cities like Rome, Vienna, and Edinburgh cannot be replicated due to strict heritage conservation laws and physical geographic constraints. UNESCO reported in 2024 that Europe hosts over 40% of the world’s World Heritage Sites, many of which are located within city centers where development is heavily restricted or entirely prohibited. This regulatory environment creates an artificial scarcity that drives competition among purchaseers seeking unique assets with provenance. The most expensive properties are becoming harder to find in traditional European safe havens as purchaseers compete for a very compact number of high-quality available homes. The inability to construct new buildings in these coveted zones means that existing stock becomes increasingly valuable over time. Buyers are motivated by the exclusivity of owning a piece of history, whether it is a palazzo in Venice or a townhoapply in Mayfair. This scarcity value ensures that prices remain robust even during broader economic downturns, as the unique nature of these assets decouples them from the cyclical dynamics of the mass market.

CRITICAL MARKET RESTRAINTS

Stringent Regulatory Frameworks and Enhanced Taxation Policies

Aggressive government measures aimed at cooling houtilizing landscapes and increasing tax revenues from high value properties serve as significant restraints on transaction volumes, investor appetite, and the growth of the Europe luxury real estate market. European nations have increasingly implemented higher stamp duties, annual property taxes, and restrictions on foreign ownership to address affordability crises and generate public funds. The UK is increasing upfront costs for foreign property investors to discourage speculative purchaseing and prioritise domestic homeownership. Similarly, France and Spain have tightened regulations on short term rentals, a key revenue stream for luxury investment properties, thereby impacting the total return on investment calculations. The European Commission has also pushed for greater transparency in beneficial ownership, forcing many anonymous purchaseers to disclose identities, which deters those seeking privacy. As borrowing and tax costs rise, properties in major world cities are spfinishing more time on the market before a deal is closed. The complexity of navigating diverse legal systems and tax regimes across the continent adds administrative burdens and costs that discourage speculative activity. Governments continue to view luxury real estate as a source of fiscal relief. Consequently, the increasing tax burden acts as a persistent drag on market liquidity and dampens the enthusiasm of marginal purchaseers.

Rising Operational Costs and Energy Compliance Mandates

The escalating costs associated with maintaining historic luxury properties alongside stringent new energy efficiency mandates pose a formidable barrier to ownership and renovation, and thereby hinder the expansion of the Europe luxury real estate market. The European Union’s Green Deal and subsequent Energy Performance of Buildings Directive require all buildings to meet specific energy ratings, necessitating costly retrofits for older, listed properties that often face preservation restrictions. The high price of building old, historic homes energy-efficient is cautilizing many wealthy purchaseers to reconsider their investments in protected buildings. Furthermore, soaring energy prices across Europe have dramatically increased the running costs of large estates, particularly those with extensive heating requirements for stone structures or large floor plates. Insurance premiums for luxury properties have also surged due to increased climate related risks such as flooding in Venice and wildfires in the Mediterranean, with some insurers withdrawing coverage entirely from high risk zones. These compounding operational expenses erode the attractiveness of holding luxury assets, leading some owners to delay sales or reduce inquireing prices. The tension between preserving architectural integrity and meeting modern environmental standards creates a complex landscape that restrains market fluidity and complicates the valuation process.

EMERGING MARKET OPPORTUNITIES

Integration of Sustainable Technologies and Green Certification Premiums

The growing emphasis on environmental sustainability presents a lucrative opportunity for developers and owners within the Europe luxury real estate market. This is especially true for those who successfully integrate green technologies and achieve high energy performance certifications in luxury properties. Affluent purchaseers are increasingly prioritizing eco frifinishly features, viewing them as essential for future proofing assets and aligning with personal values. Opportunities abound for retrofitting historic buildings with discreet solar solutions, geothermal heating, and advanced insulation materials that respect architectural heritage while maximizing efficiency. Smart home systems that optimize energy consumption and monitor air quality are becoming standard expectations rather than optional extras. Developers who can navigate the complexities of upgrading listed buildings to meet these standards without compromising their character will capture a discerning segment of the market. As regulatory pressure mounts, properties that already possess high sustainability ratings will become scarce commodities, driving further value appreciation. This shift transforms sustainability from a compliance issue into a core value driver, opening new avenues for innovation in materials and design within the luxury sector.

Expansion of Lifestyle Centric Developments and Wellness Amenities

There is a burgeoning opportunity to redefine luxury real estate by integrating comprehensive wellness facilities and lifestyle services directly into residential developments, which provides potential prospects for the Europe luxury real estate market. This shift caters to the holistic health priorities of modern ultra-high-net-worth individuals. The post pandemic era has shifted purchaseer preferences towards homes that function as private sanctuaries offering spa facilities, medical suites, fitness centers, and biophilic design elements. Developers are seizing this trfinish by creating branded residences that offer concierge health services, organic dining options, and private parks within secure compounds. Locations in the Swiss Alps and the French Riviera are seeing a surge in projects that combine skiing or beach access with world class medical and wellness infrastructure. This evolution allows sellers to differentiate their offerings in a crowded market by selling a complete lifestyle ecosystem rather than just square footage. The ability to provide seamless access to health and leisure amenities within the home environment appeals strongly to purchaseers seeking convenience and exclusivity. As the definition of luxury expands to encompass physical and mental well being, properties that deliver these integrated experiences will command significant premiums and attract a new generation of health conscious investors.

SIGNIFICANT MARKET CHALLENGES

Geopolitical Instability and Sanctions Impacting Buyer Demographics

Ongoing geopolitical tensions and the imposition of international sanctions have drastically altered the demographic landscape of purchaseers, which inhibits the growth of the Europe luxury real estate market. This shift is creating uncertainty and reducing liquidity from traditional source markets. The conflict in Eastern Europe and subsequent sanctions regimes have led to the freezing of assets and restrictions on property purchases for nationals from specific countries, rerelocating a significant cohort of active participants from the market. EU sanctions have led to the freezing of billions of euros in assets, complicating real estate transactions for sanctioned individuals, but the specific property count is not a centralized EEAS metric. This scrutiny has forced many legitimate purchaseers to withdraw due to fears of heightened regulatory examination and reputational risk. The shift has compelled markets like London and Monaco to pivot towards purchaseers from North America and the Middle East, but this transition takes time and does not fully offset the loss of previous volume. The unpredictability of international relations builds long term planning difficult for developers and investors who rely on stable cross border capital flows. Governments are tightening rules on money laundering and source of funds verification. Consequently, the due diligence process is becoming more arduous and lengthy, slowing market velocity and challenging the traditional model of rapid, high-value transactions.

Labor Shortages and Supply Chain Disruptions in High End Construction

A chronic shortage of skilled artisans and persistent supply chain disruptions are creating major hurdles for the Europe luxury real estate market. These issues are actively delaying project completion and driving up construction costs. High finish properties require specialized craftsmanship in areas such as bespoke joinery, stone masonry, and intricate restoration, skills that are becoming increasingly rare in the European workforce. The construction sector across Europe is struggling to find enough qualified tradespeople, with specific national reports in Germany and France indicating shortfalls in the hundreds of thousands. Simultaneously, the reliance on imported luxury materials such as rare marbles, exotic woods, and custom repairtures has led to prolonged lead times and volatile pricing due to global logistics bottlenecks. These factors result in significant project delays, with some super prime developments in London and Paris experiencing timeline extensions of 18 to 24 months. The rising costs of labor and materials erode profit margins and force developers to increase selling prices, potentially pricing out marginal purchaseers. The inability to guarantee timely delivery of finished products undermines purchaseer confidence and complicates the marketing of off plan luxury units. The workforce pipeline must be replenished and supply chains stabilized. Until then, the delivery of new luxury inventory will remain constrained, limiting market growth.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

4.87% |

|

Segments Covered |

By Business Model, Property, Mode of Sale and Countest |

|

Various Analyses Covered |

Global, Regional, and Countest Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities. |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe |

|

Market Leaders Profiled |

Sotheby’s International Realty Affiliates LLC, Knight Frank LLP, Savills plc, Engel & Völkers AG, Barnes International Realty, Proprietes Le Figaro, Mansion Global, John Taylor, Luxury Places SA, Christie’s International Real Estate, Coldwell Banker Global Luxury, Quintessentially Estates, Fine & Countest, Strutt & Parker, Foxtons Prime Services, Keller Williams Luxury International, Cain International, Battersea Power Station Development Co., Lodha UK, Emaar Europe Ltd |

SEGMENTAL ANALYSIS

By Business Model Insights

The sales segment was the largest segment in the Europe luxury real estate market and captured a substantial share in 2025. The prominence of the segment is supported by the fundamental perception of luxury real estate in Europe as a primary vehicle for capital preservation and long-term wealth accumulation rather than a source of recurring rental income. High net worth individuals prioritize the acquisition of prime European assets primarily for their ability to retain and grow value over time, often outperforming traditional financial instruments during periods of volatility. The scarcity of land in historic city centers like London, Paris, and Monaco ensures that supply constraints drive consistent price appreciation, building ownership more attractive than leasing. High interest rates and tax uncertainty have caapplyd property values in London’s most expensive districts to drift downward, underperforming compared to other global luxury hubs. Ultra high net worth investors view these transactions as strategic allocations to hard assets that offer a hedge against currency devaluation and stock market fluctuations. The psychological security of owning tangible heritage assets in politically stable jurisdictions further reinforces this preference. Wealthy purchaseers are increasingly paying upfront to avoid high mortgage rates. This focus on balance sheet strength rather than income generation solidifies the sales segment as the dominant force, as the primary motivation remains the secure storage of capital in appreciating physical forms. The acquisition of luxury property serves as a definitive status symbol and a critical component of legacy planning for affluent families, driving a robust culture of ownership over tenancy. Owning a prestigious address in cities like Geneva or Vienna confers social capital and access to exclusive networks that renting cannot replicate. Families often purchase properties to establish a permanent foothold in Europe for education, business, or retirement, viewing the asset as a multi generational home rather than a temporary residence. The emotional connection to specific architectural styles and historical provenance motivates purchaseers to invest heavily in customization and restoration, actions that are typically restricted in rental agreements. Furthermore, ownership provides complete control over privacy and security, which are paramount concerns for this demographic. The desire to leave a lasting physical legacy in a renowned location ensures that the decision to purchase outweighs the flexibility of renting, sustaining the overwhelming market share of the sales sector.

The rental segment is predicted to witness the highest CAGR of 9.4% from 2026 to 2034. The swift acceleration of the segment is fueled by shifting lifestyle preferences towards flexibility, the rise of the “nomadic” ultra wealthy, and increasing regulatory barriers to ownership in certain jurisdictions. A significant shift in the behavior of the global elite towards a more mobile lifestyle has spurred demand for high finish short term and medium term rentals, allowing them to relocate seamlessly between global hubs without the commitment of ownership. Modern ultra high net worth individuals increasingly prefer the freedom to relocate based on business opportunities, climate, or political stability without being tethered to a single asset. The “portfolio living” approach necessitates a reliable supply of fully serviced, turnkey luxury rentals that offer hotel-like amenities with the privacy of a home. The rise of digital nomadism among younger millionaires further accelerates this trfinish, as they seek immersive experiences in different European cultures for months at a time. The ability to test different neighborhoods before committing to a purchase also drives trial-through-rent strategies. As the definition of home becomes more fluid, the rental market expands to accommodate this dynamic, high value. Increasingly stringent regulations and punitive tax measures on foreign ownership and second homes in key European markets are pushing investors towards the rental sector as a viable alternative. Governments in cities like Barcelona, Amsterdam, and parts of London have introduced higher stamp duties, annual vacancy taxes, and restrictions on non resident purchases to cool local houtilizing markets. Consequently, many potential purchaseers are opting to rent luxury properties to avoid these fiscal burdens and administrative complexities while still enjoying access to prime locations. Landlords, often institutional investors or local entities, are stepping in to fill the gap, purchasing assets to lease to those priced out or discouraged by regulation. This regulatory push factor creates a structural tailwind for the rental segment, transforming it from a secondary option into a preferred strategy for accessing luxury living in Europe’s most coveted cities.

By Property Insights

The apartments and condominiums segment led the Europe luxury real estate market and occupied a 58.5% share in 2025. The leading position of the segment is attributed to the urban-centric nature of luxury demand, where proximity to cultural institutions, financial districts, and exclusive services in dense city centers dictates value. The overwhelming preference of luxury purchaseers for locations within walking distance of world class dining, shopping, arts, and business hubs drives the dominance of high finish apartments in major European capitals. Cities like Paris, London, and Milan define luxury through their historic urban fabric, where landed hoapplys are exceptionally rare and often converted into multiple units or institutional buildings. The lifestyle of the ultra wealthy often revolves around immediate access to private members’ clubs, Michelin starred restaurants, and flagship boutiques, which are predominantly located in dense urban cores. High rise and historic mansion block apartments offer security, concierge services, and vertical views that are highly prized. The efficiency of urban living allows owners to minimize commute times and maximize social engagement. Furthermore, the maintenance of a large landed hoapply in a city center is often impractical due to space constraints and noise, building locked up and leave apartments more suitable for international purchaseers who travel frequently. This geographic reality ensures that apartments remain the default and most liquid asset class in the European luxury market. The superior security protocols and comprehensive managed services available in luxury apartment complexes build them the preferred choice for high profile individuals concerned with privacy and safety. Gated communities and prestigious condo buildings offer 24 hour concierge, CCTV monitoring, controlled access, and on site security personnel, features that are difficult and costly to replicate in standalone villas within urban environments. These developments often include shared amenities such as private gyms, spas, screening rooms, and business centers, providing a hotel-like experience without the necessary for individual staffing. For international purchaseers who may only occupy the property for part of the year, the ability to leave the residence securely managed is crucial. The collective maintenance of exteriors and common areas also reduces the administrative burden on owners. This combination of fortified privacy and effortless living appeals strongly to celebrities, politicians, and business leaders, cementing the apartment segment as the market leader.

The villas and landed hoapplys segment is estimated to register the rapidest CAGR of 11.2% during the forecast period due to the post pandemic desire for space, privacy, and self-sufficiency, particularly in scenic rural and coastal regions away from dense urban centers. The global pandemic fundamentally altered luxury purchaseer priorities, creating a sustained surge in demand for detached properties that offer expansive indoor and outdoor space, private gardens, and isolation from neighbors. Affluent individuals who previously prioritized city center convenience now seek retreats where they can work, live, and exercise safely within their own grounds. Buyers are willing to trade urban proximity for acreage, swimming pools, and home offices, viewing these properties as sanctuaries from public health risks and urban congestion. The ability to host private gatherings without restriction has become a key selling point. This trfinish is reinforced by the normalization of remote work, which allows executives to manage global businesses from secluded locations. The psychological value of owning a substantial plot of land has never been higher, driving prices and transaction volumes for landed properties at a rate that outpaces urban apartments. As the desire for a “home as a resort” mentality persists, the villa segment continues to capture significant market momentum. The growing tfinishency for ultra high net worth individuals to acquire secondary or tertiary homes in idyllic leisure destinations is fueling the growth of the villa and landed hoapply segment. Europe boasts some of the world’s most desirable holiday regions, from the ski slopes of the Swiss Alps to the beaches of Sardinia and the Algarve, where detached villas are the standard form of luxury accommodation. Research indicates that sales of second homes in prime leisure locations grew, driven by purchaseers seeking personal vacation havens rather than investment yields. These properties often serve as family gathering spots for generations, embedding emotional value into the purchase. The development of high speed internet in rural areas has built these locations viable for extfinished stays, blurring the line between holiday home and primary residence. Investors are also drawn to the potential for high yield short term lets in these tourist hotspots when the property is not in personal apply. The limited supply of beachfront or ski-in ski-out land creates intense competition, pushing values higher. As the concept of the “multi home lifestyle” gains traction, the demand for standalone villas in Europe’s premier leisure corridors accelerates rapidly.

By Mode of Sale Insights

The secondary segment held the majority share of the Europe luxury real estate market in 2025. The supremacy of the segment is attributed to the mature nature of European cities where developable land is scarce, and the most prestigious addresses are already occupied by historic structures that rarely come to market. The physical limitation of available land in Europe’s most coveted city centers forces the majority of luxury transactions into the resale market, as new construction is often impossible or severely restricted. Cities like Rome, Vienna, and Edinburgh are protected by strict conservation laws that prevent demolition or significant alteration of historic facades, meaning the stock of luxury homes is essentially repaired. Zone 1 is densely built-up, so new development relies almost entirely on recycling existing “brownfield” sites and repurposing commercial buildings rather than utilizing open land. Wealthy purchaseers in London are increasingly prioritizing “turnkey” properties, modernized homes they can relocate into immediately, over historic repair-up projects, even in prestigious streets. Consequently, purchaseers seeking addresses in Mayfair, Kensington, or the Golden Triangle of Paris must compete for existing properties. The allure of owning a piece of history, such as a 19th century townhoapply or a renovated palace, draws purchaseers to the secondary market where provenance adds significant value. The inability to create new supply in these locations creates a closed loop where existing inventory modifys hands repeatedly, maintaining the secondary segment’s overwhelming dominance in terms of volume and value. Luxury purchaseers exhibit a strong preference for established neighborhoods with proven track records of stability, prestige, and community character, which are exclusively found in the existing home market. New developments, even in regenerating areas, lack the decades or centuries of social capital and neighborhood maturity that define prime locations. The certainty of location value in established districts reduces investment risk, as these areas have weathered economic cycles successfully. Furthermore, existing homes often feature mature gardens, mature trees, and a specific architectural charm that new builds struggle to replicate authentically. The immediate availability of infrastructure, schools, and social networks in these long standing communities builds them more attractive than waiting for new projects to mature. The emotional appeal of relocating into a home with a story and a place in the social fabric of the city drives the vast majority of transactions. This deep seated preference for the tested and tested ensures that the resale market remains the primary arena for luxury real estate activity.

The primary segment is anticipated to witness the rapidest CAGR of 8.7% over the forecast period owing to the demand for modern sustainability standards, smart home integration, and customization options that older stock cannot easily provide. Stricter environmental regulations and the growing eco consciousness of wealthy purchaseers are driving a surge in demand for new build luxury properties that inherently meet high energy performance standards. Older European buildings often struggle to achieve the required Energy Performance Certificate (EPC) ratings without prohibitive renovation costs, building new constructions with built in green technology highly attractive. Buyers are increasingly unwilling to undertake the complexity of retrofitting listed buildings for solar power, heat pumps, and advanced insulation. New builds offer turnkey sustainability, lower running costs, and future proofing against impfinishing carbon taxes. The ability to market a property as “green luxury” appeals to the values of younger ultra high net worth individuals, creating a distinct premium for primary stock. As regulatory pressure mounts, the comparative advantage of new builds in terms of compliance and efficiency will continue to accelerate their market share growth. The desire for bespoke living spaces equipped with the latest integrated smart home ecosystems is a powerful driver for the primary market, as existing homes often lack the infrastructure to support cutting edge technology seamlessly. New developments allow purchaseers to customize layouts, finishes, and technical systems from the ground up, ensuring the home perfectly aligns with their lifestyle and aesthetic preferences. Retrofitting historic properties with such technology can be invasive, expensive, and sometimes prohibited by preservation orders. Developers are responding by offering “white box” solutions where purchaseers can dictate the interior specification before completion. The promise of a brand new property with no wear and tear, full warranties, and state of the art connectivity offers a compelling value proposition. As technology evolves rapidly, the obsolescence of older systems builds new builds increasingly desirable for tech savvy elites, fueling the growth of the primary sales channel.

COUNTRY LEVEL ANALYSIS

United Kingdom Luxury Real Estate Market Analysis

The United Kingdom dominated the Europe luxury real estate market and captured a 26.6% share in 2025. The nation’s position is supported by London’s status as a global financial capital and a magnet for international capital, supported by a deep pool of ultra high net worth individuals and a stable legal framework. Despite recent tax modifys, markets in Mayfair, Knightsbridge, and Chelsea continue to attract significant inbound investment from the Middle East and Asia, drawn by the prestige of British addresses and the English language common law system. The weakness of the pound sterling at various points has also provided entest opportunities for dollar denominated purchaseers. The market is characterized by a mix of historic townhoapplys and modern high rise developments, offering diverse options for different purchaseer profiles. Strong demand from the finance and technology sectors supports rental yields and capital values. Although regulatory headwinds exist, the sheer depth of liquidity and the global brand equity of “London Luxury” ensure the UK retains its leadership position, acting as the benchmark for pricing and trfinishs across the continent.

France Luxury Real Estate Market Analysis

France was the next prominent countest in the Europe luxury real estate market and accounted for a 22.7% in 2025 becaapply of the finishuring allure of Paris as a cultural capital and the prestige of the French Riviera. The French market benefits from a unique dual engine of urban sophistication and coastal leisure, appealing to a broad spectrum of luxury purchaseers. Moreover, the Côte d’Azur remains a global hotspot for villa acquisitions, with towns like Saint Tropez and Antibes seeing record transaction volumes among the ultra wealthy seeking summer residences. France’s rich culinary scene, fashion heritage, and lifestyle offerings act as powerful non financial drivers for investment. The government’s efforts to streamline visa processes for investors and the stability of the Euro zone further enhance attractiveness. While tax regimes can be complex, the emotional and lifestyle value of owning in France often outweighs fiscal considerations. The market is also buoyed by a strong domestic wealthy class that reinvests in regional chateaux and city apartments. This combination of global icon status and diverse geographical offerings sustains France’s position as a cornerstone of the European luxury landscape.

Italy Luxury Real Estate Market Analysis

Italy continues to be a major player in the Europe luxury real estate market due to its unparalleled heritage assets and the global fascination with the “Dolce Vita” lifestyle. The Italian market is uniquely driven by the availability of historic properties such as Renaissance villas, palazzos, and restored farmhoapplys that offer a level of architectural grandeur unmatched elsewhere. Italy’s favorable tax regime for new residents, including the flat tax on foreign income, has become a significant catalyst, attracting high net worth individuals to relocate and purchase primary residences. The countest’s reputation for design, art, and gastronomy adds intangible value to real estate holdings. Cities like Milan serve as fashion and finance hubs, driving urban luxury demand, while rural areas offer retreats for leisure. The restoration of historic properties is viewed not just as a purchase but as a custodial duty, appealing to purchaseers with a passion for preservation. Despite bureaucratic challenges, the unique inventory and lifestyle incentives keep Italy as a top tier destination for luxury capital.

Switzerland Luxury Real Estate Market Analysis

Switzerland expanded steadily in the Europe luxury real estate market owing to extreme stability, privacy, and its status as a safe haven for global wealth. The Swiss market is known for its exclusivity, with strict regulations on foreign ownership in certain cantons adding to the scarcity and desirability of available stock. High net worth individuals are drawn to Switzerland for its banking secrecy traditions, low crime rates, and exceptional quality of life. The Alpine resort towns command some of the highest price per square meter globally, attracting a clientele seeking privacy and winter sports access. The market is less volatile than its neighbors, serving as a defensive asset class during times of global uncertainty. The presence of international organizations and multinational headquarters in cities like Geneva and Zurich ensures a steady stream of corporate relocations and executive houtilizing demand. This blfinish of financial security, natural beauty, and regulatory protection cements Switzerland’s role as a premium niche within the broader European market.

Spain Luxury Real Estate Market Analysis

Spain is predicted to grow in the Europe luxury real estate market during the forecast period due to its extensive coastline, favorable climate, and growing appeal as a year round residence for Northern Europeans. The Spanish luxury market has evolved from a purely seasonal holiday destination to a hub for permanent relocation, particularly in areas like Marbella, Ibiza, and Barcelona. The “Golden Visa” program, despite recent modifications, has historically facilitated inflows, and the lifestyle offering of sun, sea, and golf remains a potent draw. Barcelona has emerged as a tech and cultural hub, attracting a younger demographic of wealthy entrepreneurs. The renovation of historic properties in Andalusia and the Balearic Islands caters to purchaseers seeking authentic character combined with modern luxury. Competitive pricing relative to London or Paris also offers perceived value. The development of high finish marina facilities and exclusive beach clubs enhances the ecosystem for luxury living. As remote work enables longer stays, the demand for high specification homes in Spain continues to grow, solidifying its position as a key player in the European luxury sector.

COMPETITIVE LANDSCAPE

The competition within the Europe luxury real estate market is characterized by an intense rivalry between global powerhoapply brokerages and highly specialized local boutique firms that possess deep neighborhood knowledge. Global brands leverage their international networks and marketing muscle to attract cross border capital, while local experts compete by offering unparalleled access to off market listings and personalized service rooted in community trust. The battle for dominance often centers on the ability to secure exclusive mandates for trophy assets, leading to aggressive bidding for talent among top producing agents. Differentiation increasingly relies on the integration of luxury lifestyle services, where firms offer concierge support ranging from yacht chartering to art advisory to create a holistic client experience. Data analytics and predictive modeling have become critical tools for gaining a competitive edge in pricing and market timing. The rise of digital platforms has lowered barriers for new entrants, yet the high stakes nature of super prime transactions ensures that reputation and discretion remain the ultimate currencies. Regulatory compliance and sustainability expertise are emerging as new frontiers for competition as purchaseers demand future proof assets. This dynamic environment forces all participants to continuously innovate their service offerings and marketing strategies to capture the attention of the discerning global elite.

KEY MARKET PLAYERS

A few of the dominating players that are dominating the Europe luxury real estate market are

- Sotheby’s International Realty Affiliates LLC

- Knight Frank LLP

- Savills plc

- Engel & Völkers AG

- Barnes International Realty

- Proprietes Le Figaro

- Mansion Global

- John Taylor

- Luxury Places SA

- Christie’s International Real Estate

- Coldwell Banker Global Luxury

- Quintessentially Estates

- Fine & Countest

- Strutt & Parker

- Foxtons Prime Services

- Keller Williams Luxury International

- Cain International

- Battersea Power Station Development Co.

- Lodha UK

- Emaar Europe Ltd.

Top Players In The Market

- Knight Frank stands as a preeminent global property consultancy with a profound influence on the Europe luxury real estate market through its specialized prime residential division. The firm contributes to the global sector by setting benchmark standards for valuation, market research, and the marketing of super prime assets across major capitals. In Europe, Knight Frank recently strengthened its position by expanding its private office services tailored specifically for ultra high net worth families seeking discreet acquisition and portfolio management. They have launched innovative digital platforms that utilize virtual reality to revealcase historic estates to international purchaseers without physical travel. Their strategic focus on sustainability reporting for luxury buildings aligns with evolving European regulations and purchaseer preferences. By fostering exclusive partnerships with family offices and private banks, Knight Frank ensures a steady pipeline of qualified purchaseers. Their commitment to data driven insights and bespoke client service solidifies their reputation as a trusted advisor for the world’s wealthiest individuals navigating the complex European property landscape.

- Savills operates as a leading global real estate service provider with a dominant presence in the Europe luxury market, particularly renowned for its expertise in countest estates and prime city residences. The company contributes globally by facilitating cross border investments and offering comprehensive advisory services that span from acquisition to asset management. In Europe, Savills has recently enhanced its market standing by acquiring boutique agencies in key locations like the French Riviera and the Swiss Alps to deepen local market knowledge. They have introduced specialized divisions focapplyd on the sale of heritage listed buildings and eco frifinishly luxury developments. Their proactive approach involves hosting exclusive international property exhibitions that connect European sellers with high net worth investors from Asia and the Middle East. Savills also leverages advanced analytics to predict market trfinishs and advise clients on optimal timing for transactions. Savills maintains a robust network of local experts and delivers personalized strategies. This allows the firm to drive significant transaction volumes and remain a premier partner for luxury real estate in Europe.

- Sotheby’s International Realty affilates leverage the prestigious global brand of the auction hoapply to dominate the Europe luxury real estate market with a focus on exceptional properties and art centric marketing. The network contributes to the global market by integrating real estate sales with the broader luxury lifestyle ecosystem, appealing to collectors and connoisseurs. In Europe, affiliates have recently strengthened their position by launching tarobtained marketing campaigns that highlight the artistic and historical provenance of properties to attract culturally motivated purchaseers. They have expanded their footprint in emerging luxury hubs like Lisbon and Athens through strategic affiliations with top local brokerages. The brand utilizes its access to high net worth art collectors to cross promote real estate listings at global auctions and events. Their emphasis on cinematic property videos and high quality print media ensures maximum visibility for exclusive listings. Sotheby’s International Realty creates a unique value proposition by combining the allure of the art world with real estate expertise. This approach resonates deeply with the elite demographic, driving sustained growth and brand loyalty across the European continent.

Top Strategies Used By Key Market Participants

Key players in the Europe luxury real estate market predominantly employ niche specialization strategies by focutilizing exclusively on super prime segments and heritage properties to differentiate their services from generalist competitors. Companies frequently invest in advanced digital technologies such as virtual reality tours and artificial ininformigence driven valuation tools to enhance the remote purchaseing experience for international clients. Another vital strategy involves forming strategic alliances with private banks, family offices, and wealth management firms to gain direct access to ultra high net worth individuals seeking investment opportunities. Market leaders also prioritize brand building through exclusive events, art sponsorships, and high profile marketing campaigns that reinforce their status as purveyors of the finest lifestyles. Furthermore, participants expand their geographic reach by acquiring or affiliating with local boutique agencies in emerging luxury destinations to secure off market inventory. Providing bespoke concierge services that extfinish beyond the transaction to include interior design and property management assists retain clients and generate recurring revenue. Finally, firms actively adapt to regulatory modifys by developing expertise in sustainability compliance to guide clients through evolving environmental mandates.

MARKET SEGMENTATION

This research report on the Europe luxury real estate market is segmented and sub-segmented into the following categories.

By Business Model

By Property Type

- Apartments & Condominiums

- Villas & Landed Hoapplys

By Mode of Sale

- Primary (New-Build)

- Secondary (Existing-Home Resale)

By Countest

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Leave a Reply