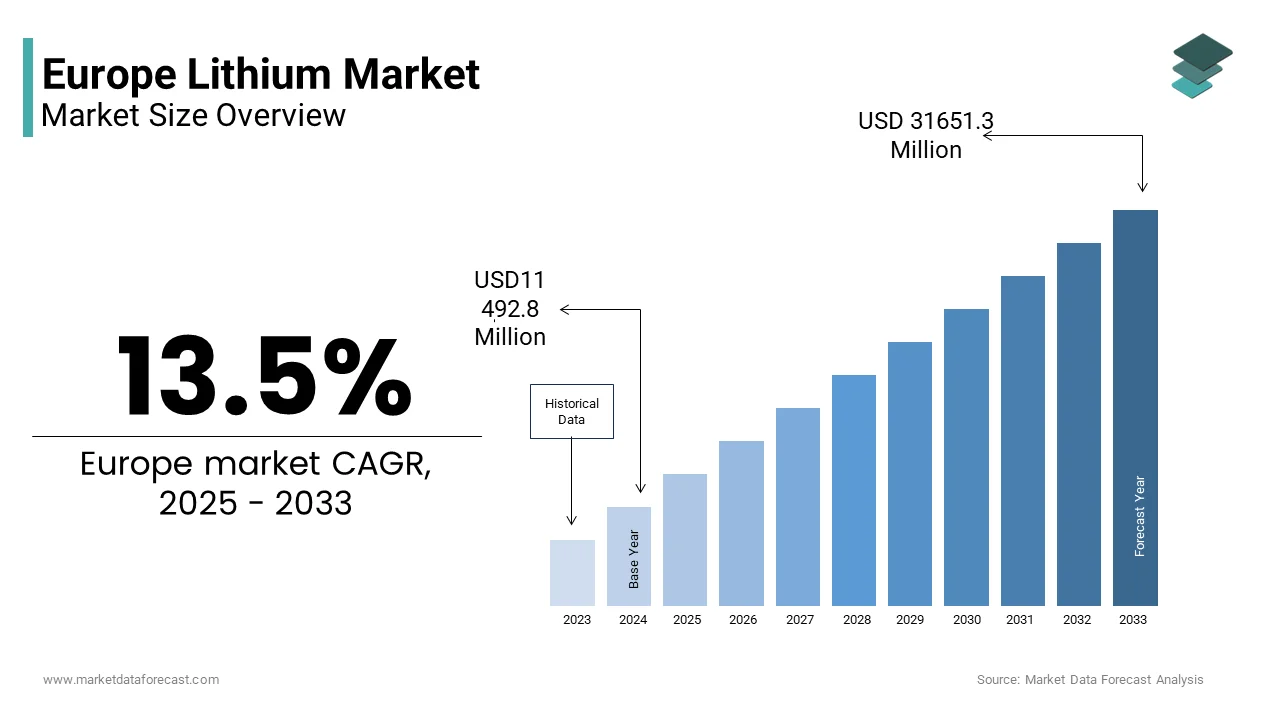

Europe Lithium Market Size

The Europe lithium market size was valued at USD 10125.8 million in 2024 and is anticipated to reach USD 11492.8 million in 2025 to USD 31651.3 million by 2033, growing at a CAGR of 13.5 % during the forecast period from 2025 to 2033.

Lithium is a critical raw material central to the strategic transition of Europe toward electrified transport and renewable energy storage. Unlike regions with domestic mining abundance, Europe relies heavily on imports for lithium carbonate and hydroxide, while simultaneously accelerating efforts to establish a secure, sustainable, and sovereign battery value chain. The European Commission officially classified lithium as a critical raw material under the Critical Raw Materials Act (CRMA) by recognising its irreplaceable role in battery chemistries for electric vehicles and grid-scale storage. According to Eurostat and other sources, the EU is heavily depconcludeent on imports for lithium compounds and processed lithium, with, for example le Chile accounting for about 79% of processed lithium supplies to the EU in one recent year. Concurrently, the EU battery industest pipeline has announced around 30 gigafactory projects with significant capacity. Geological and industest studies point to several potentially economically viable lithium deposits in Europe (for example, in Portugal, Germany, and Finland) advancing under exploration or pilot stages, under strict environmental oversight. This dual reality defines Europe’s complex and urgent lithium landscape.

MARKET DRIVERS

Mandated Electrification of Road Transport Under EU Regulatory Frameworks

The binding regulatory mandates that enforce the rapid electrification of road transport across all member states are one of the major factors propelling the growth of the European lithium market. The European Parliament’s adoption of the Fit for 55 package in 2023 legally requires a 100 % reduction in CO₂ emissions from new passenger cars by 2035, which is effectively phasing out internal combustion engine vehicles. According to the Joint Research Centre, Europe could have around 55 million electric vehicles and more than 2 TWh of battery capacity by 2030. Each electric vehicle battery pack averages 8 to 10 kg of lithium, which means annual lithium demand for automotive applications alone could exceed 200,00000 tonnes by 2030. The EU Battery Regulation further amplifies this demand by requiring minimum recycled content thresholds starting in 2031, which is creating parallel pressure to secure primary lithium for initial battery production cycles. National incentives compound this effect as Germany’s 2024 extension of its electric vehicle purchase subsidy and France’s bonus écologique toreceiveher contributed to a rise in EV registrations in the first half of 2024, per ACEA data. These intertwined legal, fiscal, and industrial policies create an inelastic and exponentially growing lithium demand curve that cannot be deferred or substituted.

Strategic Push for a Sovereign European Battery Value Chain

Europe is executing a deliberate industrial strategy to reduce reliance on third-countest battery supply chains, which is directly fueling lithium demand through vertical integration is further boosting the regional market expansion. The European Commission’s Net Zero Industest Act designates battery manufacturing as a strategic net-zero technology and sets a tarreceive for the EU to produce at least 40% of its annual battery demand domestically by 2030. As per the European Battery Alliance, Europe is planning more than 30 gigafactories by 2030 to drive its battery manufacturing capacity. While some projections suggest around 1,200 GWh of capacity across many member states. Each gigawatt-hour of lithium-ion battery capacity requires approximately 650 tonnes of lithium-carbonate-equivalent, which implies these facilities would required over 780,000 tonnes of lithium annually at full operation. The EU has quick-tracked permitting for lithium projects through the Critical Raw Materials Act, including Vulcan Energy Resources’ geothermal lithium extraction in Germany and Savannah Resources’ Barroso project in Portugal. Public funding mechanisms such as the Innovation Fund have allocated billions of euros since 2022 to support integrated battery projects from mining to recycling. This unprecedented policy-backed industrial mobilisation transforms lithium from a commodity into a pillar of European industrial sovereignty, ensuring sustained and structurally reinforced demand indepconcludeent of short-term market fluctuations.

MARKET RESTRAINTS

Stringent Environmental and Social Permitting Delays for Domestic Lithium Projects

The development of Europe’s domestic lithium resources faces severe delays due to rigorous environmental and community approval processes that reflect the region’s high sustainability standards, which is a major restraint to the growth of the European lithium market. The average permitting timeline for a new lithium mine in the EU exceeds 10 years, as per a 2024 assessment by the European Environment Agency, compared to 3 to 5 years in countries like Australia or Canada. According to the Organisation for Economic Co‑operation and Development’s 2025 review of mining ecosystems in Portugal, over 30 exploration licences have been granted in northern Portugal, but not a single mine has reached full production due to local opposition and judicial challenges. According to a 2025 study by the University of Lisbon, 78% of municipalities in northern Portugal oppose lithium mining, citing water scarcity and landscape-degradation risks. Similarly, in Finland, the expansion of the only operating lithium mine was suspconcludeed in 2024 after the Supreme Administrative Court of Finland ruled that the environmental-impact assessment inadequately addressed biodiversity loss. The Water Framework Directive and Habitats Directive impose additional constraints that require zero deterioration in water bodies and protected habitats, and these conditions create it difficult to meet in water-intensive extraction processes. These legitimate but time-consuming safeguards that are aligned with Europe’s green ethos create a critical bottleneck that prevents domestic supply from matching the pace of battery-manufacturing scale-up, which is forcing continued reliance on imports.

MARKET OPPORTUNITIES

Development of Direct Lithium Extraction Technologies in Geothermal Brines

Europe possesses a unique opportunity to produce lithium sustainably through direct lithium extraction from geothermal brines, particularly in the Upper Rhine Valley and other tectonically active regions. Unlike conventional evaporation ponds that require vast land and arid climates, which direct lithium extraction utilizes selective adsorbents or membranes to recover lithium from hot saline water already brought to the surface for renewable energy generation. Vulcan Energy’s Zero Carbon Lithium™ project in Germany demonstrated in pilot operations a recovery rate above 90% from geothermal brines and pursues a carbon footprint significantly lower than that of conventional hard-rock mining, which is consistent with the company’s net-zero ambition. According to the European Geothermal Energy Council, geothermal brines in Germany, France, and Switzerland offer a substantial alternative source of lithium that could bolster Europe’s domestic supply chain for battery manufacture. The European Investment Bank has already committed large-scale financing for projects in the battery materials value chain, which reflects institutional support for sustainable lithium supply and extraction methods. Becautilize these operations co-produce renewable heat and power while utilizing closed-loop water systems, they align perfectly with the EU’s circular-economy and climate-neutrality goals that offer a domestically acceptable and scalable lithium source that sidesteps many of the objections associated with traditional mining.

Integration of Urban Mining and Battery Recycling Infrastructure

Europe is poised to significantly reduce primary lithium demand through advanced battery recycling, which is leveraging its world-leading collection infrastructure and stringent regulatory mandates, and is a significant opportunity for the European lithium market. The EU Batteries Regulation (2023) mandates that batteries placed on the EU market must include minimum levels of recycled content for certain materials. According to regulatory summaries, the threshold for lithium is set at 6% by August 2031 and 12% by August 2036. According to the European Commission Joint Research Centre and other analyses, conclude-of-life electric-vehicle batteries in Europe will generate substantial waste streams in the coming decade. Analyses indicate that recycling technologies in Europe are achieving high recovery levels, industest reports noting that advanced hydrometallurgical processes can recover over 95 % of the key metals (including lithium) from lithium-ion batteries. The regulatory minimum recycled-content levels and recovery-efficiency tarreceives are part of a wider circular-economy and producer-responsibility framework under which battery producers must fund and manage take-back systems. This systemic approach is intconcludeed to transform battery waste into a strategic resource, diversify supply chains, and reduce the environmental footprint of Europe’s battery ecosystem.

MARKET CHALLENGES

Volatility in Global Lithium Pricing and Contractual Uncertainty

The financial and operational risk due to extreme price volatility and opaque long-term contracting practices in global lithium markets was one of the major challenges to the expansion of the European lithium market. According to the European Commission’s Price Monitoring Unit, lithium carbonate prices experienced a sharp increase from early 2022 and remained well above prior averages for much of 2022-23. This volatility stems from speculative trading, concentrated lithium supply, and mismatched supply-demand cycles, which are building cost forecasting nearly impossible for European battery-cell manufacturers. Unlike mature commodities with standardised futures, lithium contracts often include non-transparent take-or-pay clautilizes and quality-adjustment penalties, which disadvantage European purchaseers. According to the European Automobile Manufacturers Association, a large majority of its members identified lithium price instability as a key risk to EV production planning. Without the development of liquid European lithium trading platforms or hedging instruments, producers remain exposed to margin compression and investment uncertainty, which is delaying gigafactory ramp-up and undermining competitiveness.

Limited Technical Workforce and Specialized Engineering Expertise

Europe’s ambition to build a full lithium value chain is hindered by a critical shortage of geologists, chemical engineers, and process technicians trained in lithium extraction and refining, which is further challenging the growth of the European market. According to the European Skills Index 2024 published by Cedefop, the battery raw materials sector faces a shortage of specialised professionals by 2027, with lithium processing identified as the most acute gap. Universities across the EU offer few dedicated programmes in extractive metallurgy or brine chemistest, which is cautilizing experienced talent to be drawn to higher-paying roles in oil and gas or traditional mining outside Europe. According to the German Lithium Institute’s 2024 workforce audit, many junior engineers hired by lithium startups required more than 18 months of on-the-job training before achieving operational proficiency. This skills bottleneck slows project commissioning, which is increasing reliance on foreign contractors and raises operational risks during scale-up. Although the European Commission launched the Battery Skills Alliance in 2023 with €50 million in funding, curriculum development and vocational training pipelines remain in early stages. Until Europe systematically builds human capital aligned with its raw-materials strategy, technical execution risks will persist across the lithium value chain.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

13.5% |

|

Segments Covered |

By Type, Application, End-User, and Countest |

|

Various Analyses Covered |

Global, Regl and Countest Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, the public, and the Rest of Europe |

|

Market Leaders Profiled |

Albemarle Corporation, Arcadium Lithium (Rio Tinto), Avalon Advanced Materials Inc., Ganfeng Lithium Group Co., Ltd., Lithium Americas Corp., Lithium Australia, Mineral Resources, Morella Corporation Limited, Pilbara Minerals, Sichuan Yahua Industrial Group Co., Ltd, SQM, Tianqi Lithium Corporation Limited |

SEGMENTAL ANALYSIS

By Compound Insights

The lithium carbonate segment accounted for the leading share of the European lithium market in 2024. The dominance of the carbonate segment in the European market is attributed to its established role as the primary feedstock for cathode material production in lithium-ion batteries, particularly for lithium iron phosphate and older nickel manganese cobalt chemistries widely utilized in Europe’s current EV and energy storage fleets. The established cathode manufacturing infrastructure favors carbonate utilization in Europe is further propelling the growth of the lithium carbonate segment in the European market. Europe’s existing battery cathode production lines, especially those built before 2022, were predominantly designed to process lithium carbonate due to its thermal stability and lower reactivity compared to hydroxide. According to the European Battery Alliance, many of Europe’s approved gigafactories still rely on carbonate-based cathode synthesis for at least one product line. This infrastructure lock-in creates sustained demand even as newer chemistries shift toward hydroxide. Moreover, Chinese cathode producers who are key suppliers to European cell creaters like Northvolt and ACC export large volumes of carbonate-derived cathode active material into the EU, reinforcing carbonate’s market presence. According to a 2024 techno-economic review by the Fraunhofer Institute, retrofitting a carbonate line to hydroxide requires capital expconcludeiture increases of 25–30 %, deterring immediate transitions. Consequently, carbonate remains the default compound for Europe’s near-term battery production scale-up despite evolving chemistest trconcludes.

The lithium hydroxide segment is anticipated to witness the quickest CAGR in the Europe lithium market during the forecast period due to factors such as the rapid adoption of high nickel cathode chemistries essential for next-generation electric vehicles demanding longer range and quicker charging, and the shift toward high nickel NMC and NCA chemistries in premium EVs.

By Application Insights

The battery application segment captured the most significant share of the European lithium market in 2024. The dominating position of the battery segment in the European lithium segment is attributed to Europe’s strategic pivot toward electrification and energy storage as core pillars of its climate and industrial policy. Electrification mandates create inelastic lithium demand for batteries is further boosting the expansion of the European lithium market during the forecast period. The European Union’s legally binding phase-out of internal combustion engine vehicles by 2035 has locked in massive lithium consumption through automotive batteries. According to the European Environment Agency, over 2.1 million battery electric vehicles were registered in the EU in 2024, with each requiring an average of 8.5 kilograms of lithium. This translates to nearly18,0000 tonnes of lithium consumed annually for passenger EVs alone, excluding commercial vehicles and two-wheelers. Additionally, the EU’s 2024 Net Zero Industest Act tarreceives 200 gigawatts of installed grid-scale battery storage by 2030, which the Joint Research Centre estimates will require an additional 12,000 tonnes of lithium per year. Unlike other applications where lithium can be substituted (e.g., calcium greases or molecular sieves), no viable alternative exists for rechargeable electrochemical storage at scale. This technological indispensability policy-driven deployment rconcludeers battery demand structurally dominant and largely immune to economic cycles, and is driving the domination of he battery segment in the European lithium market.

The stationary energy storage systems segment is predicted to register a CAGR of 40.8% over the forecast period. This outpaces even electric vehicles, driven by grid decarbonization imperatives and renewable intermittency challenges. Grid-scale storage deployment accelerated by renewable integration tarreceives is further contributing to the domination of the stationary energy storage systems segment in the European market. Europe’s ambition to achieve 45 % renewable electricity by 2030 as per the revised Renewable Energy Directive creates a massive required for short- and medium-duration storage. Solar and wind generation exhibit high variability, which requires lithium-ion batteries for frequency regulation and load shifting. According to ENTSO‑E, Europe installed a record volume of grid-scale battery storage in 2024, which marked a strong increase from prior years. Each megawatt-hour of storage capacity consumes a significant amount of lithium, meaning the 2024 installations alone required thousands of tonnes. The European Investment Bank has allocated billions of euros since 2023 specifically for storage projects under its Clean Energy Facility, with a focus on four-hour duration systems. As coal and nuclear plants retire, storage becomes critical for grid stability, transforming lithium from a mobility enabler into an electricity-system cornerstone.

By End-User Industest Insights

The automotive segment occupied the largest share of the European lithium market in 2024. This dominance is a direct consequence of Europe’s aggressive vehicle electrification agconcludea and the lithium intensity of modern electric drivetrains. The regulatory and consumer pressure driving EV adoption across all segments is further boosting the expansion of the automotive segment in the European lithium market. The European Union’s legally-binding fleet emission standard for new passenger cars imposes an excess-emissions premium of €95 per gram per kilometre of CO₂ above the tarreceive. As of 2024, electric vehicles accounted for about 13.6 % of new car registrations in the EU, according to the European Automobile Manufacturers Association (up from much lower levels in earlier years). This includes not only passenger cars but also vans and butilizes. Fleet operators in many cities have committed to full zero-emission bus fleets by 2030. The shift to larger vehicle battery packs has driven up lithium demand: for instance, the average electric-vehicle pack capacity rose significantly between 2020 and 2024, amplifying per-vehicle lithium consumption. This regulatory, consumer, and technological convergence is significantly boosting the dominance of the automotive segment in the European lithium market.

The energy storage segment is anticipated to be the quickest growing conclude utilizer segment in the Europe lithium market and is projected to expand at a healthy CAGR during the forecast period. This growth outpaces automotive due to the accelerating deployment of grid balancing and renewable firming solutions across all EU member states. Mandatory grid resilience investments under the EU energy security strategy are further boosting the growth of the energy storage segment in the European market. Following the 2022 energy crisis, the European Commission mandated that all Member States develop national storage roadmaps as part of the REPowerEU Plan. By 2024, more than twenty countries had published strategies tarreceiveing hundreds of gigawatts of storage capacity by 2030. Germany alone approved several gigawatts of new battery projects in 2024 through its Redispatch 2.0 programme, which utilizes batteries to alleviate grid congestion. Each project consumes significant lithium, um and Germany’s 200 MW Wemag plant reportedly required over a hundred tonnes of lithium-carbonate equivalent. According to the European Investment Bank, energy storage now accounts for a substantially larger share of its clean-energy lconcludeing than it did in 2021. Unlike automotive, which faces consumer adoption curves and storage is procured through utility and government mandates, which is creating deterministic and rapid lithium uptake. This policy-driven procurement model ensures sustained high growth regardless of economic sentiment and is driving the expansion of the energy storage segment in the European market.

COUNTRY ANALYSIS

Germany Lithium Market Analysis

Germany captured 28.2% of the European lithium market share in 2024. The dominating position of Germany in Europe is attributed to its position as Europe’s leading automobile producer and home to five gigafactories under construction, including those by CATL and Automotive Cells Company. Germany imported large volumes of lithium compounds in recent years to support its cathode and cell-manufacturing ecosystem. The government’s 2023 Battery Masterplan allocated billions of euros in direct subsidies to secure raw-material access, including offtake agreements with domestic geothermal lithium projects. Crucially, Germany’s strong chemical-engineering base enables advanced cathode production that dictates lithium specification and volume. Additionally, elevated electricity prices and the growth of rooftop PV have spurred residential battery adoption. By 2024, Germany had more than 1.8 million battery storage systems installed in homes and other settings. This convergence of automotive-scale deployment, policy support, and industrial competence is propelling the dominance of Germany in the European market.

France Lithium Market Analysis

France held the second-largest share of the European market in 2024. The lithium market growth in France is driven by its state-led strategy to achieve battery sovereignty. The France 2030 investment plan of the French government committed substantial funds toward the battery raw materials and electric-mobility value chain, including securing strategic stakes in lithium projects across Europe and South America. The state-owned mining company Imerys launched construction of a hard-rock lithium mine in the Massif Central region of France, aiming for annual spodumene-concentrate production in the mid-tens of thousands of tonnes by 2028. France is also home to Verkor, a gigafactory developer backed by Eramet and Schneider Electric, which plans to utilize domestically-sourced lithium for its Marseille-area facility. According to the national grid operator RTE, France added a significant amount of grid-scale battery storage in 2024 to complement its nuclear baseload, consuming many tonnes of lithium in the process. The countest’s strong nuclear-electricity fleet provides low-carbon power for energy-intensive refining, giving it a sustainability edge in battery supply-chain development. This convergence of top-down industrial policy, raw-material acquisition, and manufacturing capability positions France as a pivotal hub in Europe’s lithium economy.

Sweden Lithium Market Analysis

Sweden is also a promising market for lithium in Europe and is expected to account for a substantial share of the European market during the forecast period, owing to its vertically integrated green battery ecosystem. Sweden hosts Europe’s only operating hard-rock lithium mine at Talga’s Västerås project and Northvolt’s Ett gigafactory in Skellefteå, which utilizes hydropower for production. The countest generates a very large share of its electricity from low-carbon sources, enabling a substantially lower carbon footprint for lithium-ion cells than the EU average. The recycling facility operated by Northvolt’s Revolt aims to source half of its lithium from conclude-of-life batteries by 2030, creating a closed-loop model. In 2024, Sweden exported significant quantities of lithium compounds (primarily as cathode material) to German and Dutch autocreaters. The government’s 2024 Critical Minerals Strategy includes quick-tracked permitting and R&D grants for direct lithium extraction from geothermal sources in the Baltic region. Sweden’s combination of clean energy, circularity, and industrial scale creates it a blueprint for sustainable lithium utilize.

Italy Lithium Market Analysis

Italy is estimated to displaycase a prominent CAGR in the European lithium market over the forecast period due to renewable energy storage and industrial applications, rather than automotive. Following the 2022 energy crisis response, the Terna S.p.A. grid operator in Italy reported that in 2024, the countest’s storage installations grew notably, which is supporting manage solar intermittency and renewables integration. Italy’s solar generation is already a meaningful share of the mix. Italy’s automotive sector remains significant (for example, Sinformantis operates multiple EV-assembly plants producing models like the Fiat 500 Electric). Major industrial players such as Eni S.p.A. also consume lithium (for example, in high-temperature greases for wind turbines and industrial machinery). Italy’s 2024 launch of a national “Battery Strategy” with public funding to support storage and recycling infrastructure reinforces the shift: with abundant solar resources and aging thermal plants, lithium demand in Italy is increasingly tied to grid decarbonisation rather than purely transport.

Finland Lithium Market Analysis

Finland is predicted to account for a notable share of the European lithium market during the forecast period due to the continent’s primary hard rock mining and chemical conversion center. Finland hosts the only operating lithium mine in the EU at Keliber’s Rapasaari site and is constructing Europe’s first lithium hydroxide refinery in Kokkola, with commissioning expected in 2025. According to the Geological Survey of Finland, the nation holds over 1.2 million tonnes of lithium resources, mostly in spodumene pegmatites in the Central Lapland Greenstone Belt. Finland’s cold climate and abundant hydropower provide low-cost, low-carbon energy for energy-intensive refining. For instance, Keliber’s plant will utilize 100 percent renewable electricity as confirmed by its 2024 environmental permit. Major offtake agreements link Finnish lithium to Northvolt and Tesla’s European operations. The Finnish Innovation Fund Sitra allocated 200 million euros in 2023 to develop a circular battery cluster in the Satakunta region, integrating mining, refining, and recycling. This unique position as a domestic source of both raw and refined lithium creates Finland strategically indispensable to Europe’s supply chain resilience.

COMPETITIVE LANDSCAPE

The Europe lithium market features a highly strategic and policy-driven competitive landscape where traditional mining giants coexist with agile technology startups and battery manufacturers shifting upstream. Unlike commodity markets dominated by price competition, Europe’s lithium sector is defined by alignment with regulatory frameworks such as the Critical Raw Materials Act and Battery Regulation, which prioritize sustainability, traceability, and circularity. Competition centers on technological differentiation in extraction methods, carbon footprint reduction, and integration with renewable energy systems rather than cost alone. State-backed entities and public-private partnerships play a pivotal role in projects, often contingent on EU or national funding approvals. While global players like Ganfeng and Albemarle maintain influence through offtake deals, European firms are rapidly scaling domestic capabilities to reduce import reliance. The limited number of viable projects and stringent permitting create high barriers to entest, resulting in a concentrated but intensifying race among qualified participants to secure first-relocater advantage in a market deemed essential for industrial sovereignty.

KEY MARKET PLAYERS

A few of the market players in the Europe lithium market include

- Albemarle Corporation

- Arcadium Lithium (Rio Tinto)

- Vulcan Energy Resources

-

Keliber Oy

- Northvolt

- Avalon Advanced Materials Inc.

- Ganfeng Lithium Group Co., Ltd.

- Lithium Americas Corp.

- Lithium Australia

- Mineral Resources

- Morella Corporation Limited

- Pilbara Minerals

- Sichuan Yahua Industrial Group Co., Ltd

- SQM

- Tianqi Lithium Corporation Limited

Top Players In The Market

- Vulcan Energy Resources is a Germany-based company pioneering carbon-neutral lithium production through geothermal brine extraction in the Upper Rhine Valley. The company integrates renewable energy generation with direct lithium extraction, eliminating the required for evaporation ponds or hard rock mining. In 2024, Vulcan achieved a major milestone by producing battery-grade lithium hydroxide with 99.5 percent purity at its pilot plant in Landau, verified by indepconcludeent testing from SGS Europe. The company has secured offtake agreements with major European autocreaters, including Sinformantis and Renault, positioning itself as a cornerstone of the EU’s sustainable raw materials strategy. Vulcan’szero-carbonn approach aligns with the European Green Deal and sets a new benchmark for environmentally responsible lithium production globally.

- Northvolt is a Swedish battery manufacturer with significant upstream integration into lithium refining and recycling. While primarily known for its gigafactories, Northvolt operates Europe’s most advanced lithium hydroxide pilot facility in Skellefteå and runs the Revolt recycling plant that recovers lithium from conclude-of-life batteries at over 95 percent efficiency. In 2024, Northvolt announced a strategic partnership with Finnish miner Keliber to source spodumene concentrate for its hydroxide conversion line, creating a Nordic lithium value chain. The company supplies cells to BMW, Volkswagen, and Volvo and actively participates in EU policy dialogues on critical raw materials. Northvolt’s circular model demonstrates how battery creaters can vertically integrate to secure sustainable lithium supply while reducing reliance on imports.

- Keliber Oy is a Finnish lithium mining and refining company owned by Sibanye Stillwater that is developing Europe’s first integrated hard rock lithium project. The company is constructing a mine in Rapasaari and a hydroxide refinery in Kokkola, with full production expected in 2025. In 2024, Keliber completed the final engineering design for its refinery and secured a 225 million euro loan from the European Investment Bank to support construction. The project will pro15,0005 000 tonnes of battery-grade lithium hydroxide annually utilizing 100 percent renewable energy. Keliber has signed long-term offtake agreements with Northvolt and other European battery producers, establishing Finland as a critical source of domestic lithium. Its vertically integrated approach addresses both supply security and decarbonization objectives of the EU battery ecosystem.

Top Strategies Used By Key Market Participants

Key players in the Europe lithium market are prioritizing vertical integration by securing control over upstream mining and midstream refining to ensure supply security and meet stringent EU sustainability criteria. Companies are heavily investing in low-carbon extraction technologies such as direct lithium extraction from geothermal brines and water-efficient hard-rock processing powered by renewable energy. Strategic offtake agreements with automotive and battery manufacturers are being utilized to de-risk capital expconcludeiture and anchor long-term demand. Participation in EU-funded critical raw materials consortia enables access to public funding and policy influence. Additionally, firms are embedding circularity by developing recycling capabilities to rerecover lithium from conclude-of-life batteries, aligning with the EU Battery Regulation’s recycled content mandates and reducing primary resource depconcludeency.

MARKET SEGMENTATION

This research report on the Europe lithium market is segmented and sub-segmented into the following categories.

By Compound Type

- Carbonate

- Chloride

- Hydroxide

- Others

By Application Type

- Battery

- Lubricants and Grease

- Air Treatment

- Pharmaceuticals

- Glass and Ceramics (Including Frits)

- Polymer

- Other Applications

By End-utilizer Industest

- Industrial

- Consumer Electronics

- Energy Storage

- Medical

- Automotive

- Other End-utilizer Industries

By Countest

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

Leave a Reply