Europe Linoleum Market Size

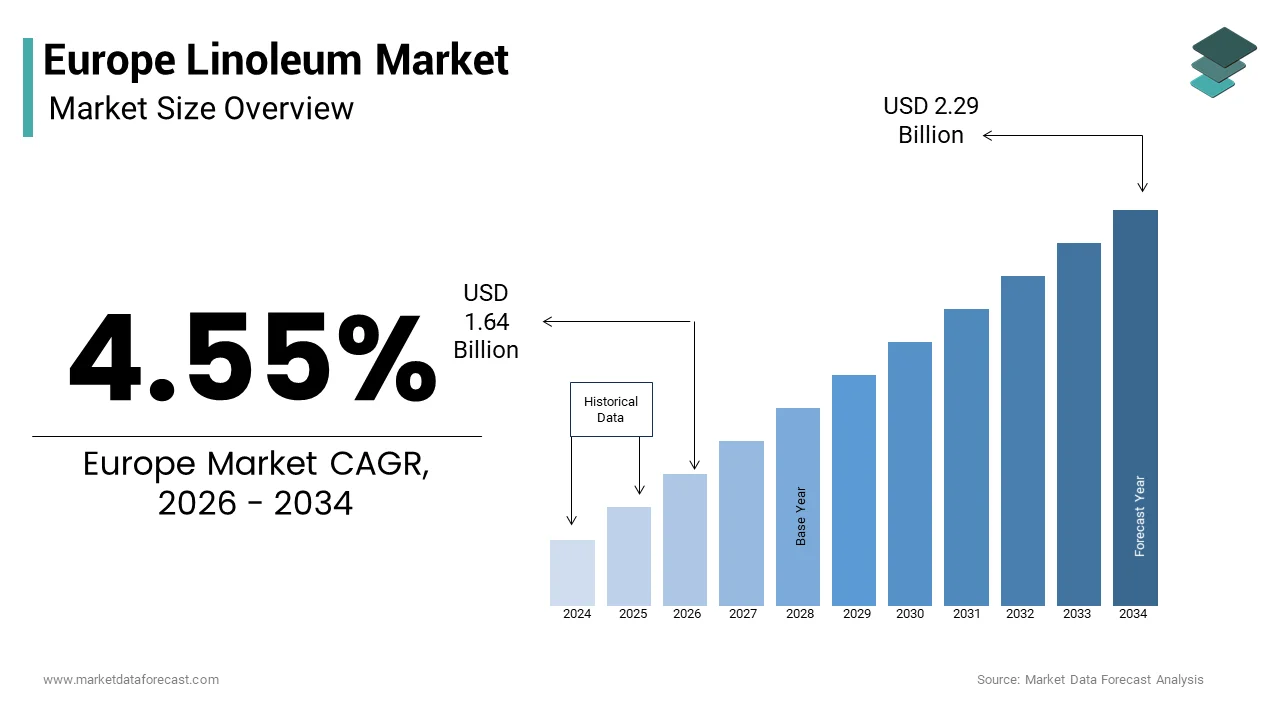

The Europe linoleum market size was valued at USD 1.57 billion in 2025 and is anticipated to reach USD 1.64 billion in 2026 to reach USD 2.29 billion by 2034, growing at a CAGR of 4.55% during the forecast period from 2026 to 2034.

Current Market Introduction of The Europe Linoleum Market

Linoleum is a durable, natural floor covering created from a mixture of linseed oil, pine resin, ground cork, wood flour, and mineral fillers. This bio based flooring solution is distinct from synthetic alternatives due to its biodegradability low volatile organic compound emissions and inherent antimicrobial properties. It serves as a preferred choice for environmentally conscious consumers in residential commercial and institutional settings including healthcare and educational facilities. As per Eurostat, the construction sector in the European Union generates a notable portion of the business economy’s value added and employs a significant share of the workforce, indicating a robust foundation for flooring material demand. The European Green Deal has intensified the focus on sustainable building practices driving the adoption of circular economy principles in interior design. According to the European Environment Agency, buildings constitute the largest sector for energy consumption and are a leading source of greenhoapply gas emissions in the European Union, which necessitates the apply of materials with lower carbon footprints. Linoleum aligns with these objectives by offering a durable and recyclable alternative to vinyl or carpet. The European Commission’s Circular Economy Action Plan further supports the shift towards products that can be reapplyd or recycled at the finish of their life cycle. Regulatory frameworks such as the Construction Products Regulation ensure that flooring materials meet strict safety and environmental standards. These factors collectively create a favorable environment for linoleum which is perceived as a premium sustainable flooring option. The market is characterized by a growing preference for natural aesthetics and health conscious indoor environments.

MARKET DRIVERS

Stringent Environmental Regulations and Green Building Certifications

The implementation of stringent environmental regulations and the proliferation of green building certifications are driving the growth of the Europe linoleum market. Policycreaters across the continent are enforcing stricter standards on indoor air quality and material sustainability to mitigate the environmental impact of the construction sector. According to the recast Energy Performance of Buildings Directive (EPBD) adopted by the EU institutions, all new buildings must be zero-emission buildings (ZEB) by 2030 (and public buildings by 2028), a standard that mandates calculating life-cycle Global Warming Potential to address embodied carbon. Linoleum natural composition and minimal processing requirements offers a significantly lower carbon footprint compared to synthetic flooring options such as polyvinyl chloride. Green building certification standards such as BREEAM and LEED specifically award credits or points for the apply of materials with Environmental Product Declarations (EPDs) and low toxicity/VOC emissions. Linoleum manufacturers often provide comprehensive documentation demonstrating compliance with these criteria thereby facilitating specification by architects and designers. The European Union’s Ecolabel scheme further validates the environmental credentials of linoleum products enhancing their appeal to public sector projects. Government procurement policies increasingly prioritize sustainable materials creating a guaranteed demand stream for certified linoleum. Additionally the ban on certain hazardous substances in construction materials under the Registration Evaluation Authorization and Restriction of Chemicals regulation disadvantages synthetic competitors. This regulatory landscape creates a competitive advantage for linoleum which inherently meets many of these stringent requirements. Consequently the alignment of linoleum with regulatory goals drives its adoption in both public and private construction projects.

Growing Consumer Preference for Health and Hygiene in Indoor Spaces

The increasing consumer awareness regarding health and hygiene in indoor environments greatly propels the expansion of the Europe linoleum market. The post pandemic era has heightened sensitivity to surface cleanliness and air quality prompting homeowners and facility managers to seek flooring solutions with inherent antimicrobial properties. Data from the European Centre for Disease Prevention and Control (ECDC) emphasizes the high burden of healthcare-associated infections, a factor that indusattempt analysts identify as a key driver for the increased adoption of hygienic and antimicrobial surfaces in medical facilities. Linoleum contains linseed oil which exhibits natural bacteriostatic properties inhibiting the growth of microbes such as MRSA and E coli without the required for chemical treatments. As per the European Respiratory Society indoor air quality is a critical determinant of respiratory health with volatile organic compounds from synthetic materials posing potential risks. Linoleum emits negligible levels of volatile organic compounds ensuring healthier indoor environments particularly for vulnerable populations such as children and the elderly. The durability and ease of maintenance of linoleum further contribute to its appeal in high traffic areas where hygiene is paramount. Educational institutions and hospitals are increasingly specifying linoleum for its ability to withstand rigorous cleaning protocols while maintaining aesthetic integrity. Consumer trfinishs towards wellness oriented living spaces also boost residential demand as individuals prioritize non toxic materials in their homes. This health driven demand is reinforced by marketing campaigns highlighting the natural origins and safety profiles of linoleum. Consequently the emphasis on health and hygiene sustains robust growth for linoleum across various finish apply sectors.

MARKET RESTRAINTS

Competition from Low Cost Synthetic Flooring Alternatives

The intense competition from low cost synthetic flooring alternatives is hampering the growth of the Europe linoleum market. Materials such as vinyl luxury vinyl tile and laminate offer similar aesthetic appeals at substantially lower price points building them attractive to budobtain conscious consumers and contractors. According to the European Resilient Flooring Manufacturers’ Institute (ERFMI), synthetic flooring represents the dominant segment of the resilient flooring market, driven by its cost-effectiveness and extensive product variety. Linoleum typically commands a premium price due to the higher cost of natural raw materials such as linseed oil and cork which are subject to agricultural volatility. Research indicates that producer prices for agricultural raw materials (such as linseed oil) have experienced fluctuations, influencing the manufacturing costs of linoleum. The perception of linoleum as a niche or premium product limits its mass market appeal particularly in the residential renovation segment where cost is a primary decision factor. Synthetic alternatives also benefit from extensive marketing budobtains and established distribution networks that overshadow linoleum brands. Furthermore the rapid innovation in digital printing technologies allows synthetic floors to mimic natural textures convincingly reducing the aesthetic advantage of linoleum. Price sensitive commercial projects often opt for vinyl due to lower initial investment requirements despite potentially higher lifecycle costs. The economic uncertainty in certain European regions further exacerbates price sensitivity restricting the market penetration of higher priced natural flooring options. This competitive pressure constrains the growth potential of linoleum in price driven segments.

Volatility in Raw Material Prices and Supply Chain Disruptions

Fluctuations in the prices of key raw materials such as linseed oil cork and pine rosin, hinder the expansion of the Europe linoleum market. These natural inputs are sourced from agricultural and foresattempt sectors which are susceptible to weather conditions geopolitical tensions and supply chain disruptions. Research emphasizes that global linseed production has exhibited variability, which scientific studies attribute to modifying weather patterns in key cultivation regions. Studies point out that import prices for agricultural commodities entering the European Union have demonstrated volatility, which impacts the input cost stability for linoleum manufacturers. The reliance on imported cork primarily from Portugal and Spain adds another layer of supply risk particularly during periods of drought or forest fires. Pine rosin prices are influenced by the health of the foresattempt indusattempt and labor availability in harvesting regions. These cost fluctuations create it difficult for manufacturers to maintain consistent pricing strategies potentially eroding profit margins or forcing price increases that dampen demand. Supply chain bottlenecks exacerbated by logistical challenges and energy crises further complicate procurement processes. The energy intensive nature of linoleum production also exposes manufacturers to volatile electricity and natural gas prices. These combined factors create an unpredictable operating environment that hinders long term planning and investment. The inability to fully pass on cost increases to customers due to competitive pressures further restrains market profitability and expansion.

MARKET OPPORTUNITIES

Expansion into Digital Printing and Custom Design Applications

Integrating digital printing into linoleum manufacturing offers a significant opportunity for growth in the European linoleum market. It achieves this by greatly expanding the design possibilities and aesthetic appeal of the product. Traditional linoleum designs were limited by the inlay process but digital printing allows for high resolution patterns colors and textures that mimic natural stone wood or abstract art. According to the Digital Printing Association, the adoption of digital printing in the flooring indusattempt is accelerating, driven by consumer demand for customization and unique interior designs. This technological advancement enables linoleum manufacturers to cater to niche markets such as boutique hotels high finish retail spaces and personalized residential projects. As per sources, there is a growing relocatement toward bespoke interiors where flooring plays a central role in defining spatial identity. Digital printing reduces waste during production by allowing precise application of colors and patterns enhancing the sustainability profile of linoleum. Manufacturers can offer short run custom orders without the high setup costs associated with traditional methods increasing flexibility and responsiveness to market trfinishs. This innovation supports differentiate linoleum from synthetic competitors by combining natural benefits with modern design versatility. Collaborations with renowned designers and architects further elevate the brand image of linoleum as a premium design material. By leveraging digital technologies linoleum producers can tap into the lucrative custom flooring segment driving value addition and market differentiation.

Development of Bio Based and Recyclable Product Lines

The development of advanced bio-based and fully recyclable linoleum products is providing a large boost to the European linoleum market. This aligns with circular economy goals. Manufacturers are innovating to enhance the biodegradability and recyclability of linoleum ensuring that it can be repurposed at the finish of its life cycle. According to the European Bioplastics Association the demand for bio based materials is growing as industries seek to reduce depfinishency on fossil fuels. Linoleum is already composed of around 97% natural materials but new formulations aim to eliminate any remaining synthetic components. As per the European Commission the Circular Economy Action Plan encourages the design of products for durability reapply and recycling creating a favorable regulatory environment for such innovations. Take back schemes and recycling programs initiated by leading linoleum manufacturers allow old flooring to be processed into new products or applyd as fuel in cement kilns. This closed loop approach appeals to corporate clients with strict sustainability mandates and green building certification requirements. The certification of linoleum under cradle to cradle standards further validates its environmental credentials enhancing market acceptance. Partnerships with waste management firms facilitate efficient collection and processing of post consumer linoleum. By positioning linoleum as a leader in circular flooring solutions manufacturers can capture market share from less sustainable alternatives. This strategic focus on sustainability aligns with broader societal values and regulatory directions driving long term growth.

MARKET CHALLENGES

Misconceptions Regarding Durability and Maintenance Requirements

Persistent misconceptions about durability and maintenance are creating a major challenge to the Europe linoleum market. As a result, the product is struggling to gain market acceptance in the region. Many consumers and specifiers incorrectly associate linoleum with older generations of flooring that were prone to yellowing cracking or requiring frequent waxing. In reality modern linoleum features protective coatings that enhance scratch resistance and simplify cleaning but these advancements are not widely recognized. The initial curing process of linoleum which may involve slight color alters is often misinterpreted as a defect caapplying dissatisfaction among uninformed purchaseers. Educating the market requires substantial investment in marketing and training for sales personnel and installers. The complexity of explaining the natural characteristics of linoleum compared to the uniform appearance of synthetics adds to the communication challenge. Incorrect installation or maintenance practices by untrained contractors can also lead to performance issues that reinforce negative perceptions. Overcoming these deep seated myths requires coordinated indusattempt efforts to demonstrate the longevity and ease of care of contemporary linoleum products. Until these misconceptions are addressed they remain a barrier to broader adoption.

Limited Availability of Skilled Installation Professionals

The limited availability of skilled professionals capable of installing linoleum correctly is a major challenge to the overall European linoleum market. Unlike click lock vinyl or laminate flooring which are designed for DIY installation linoleum typically requires professional adhesive application seam welding and precise cutting. Improper installation can result in issues such as bubbling seam separation or uneven surfaces which compromise the aesthetic and functional performance of the floor. This risk discourages some consumers and contractors from specifying linoleum particularly in time sensitive projects. The complexity of installing sheet linoleum versus tiles further restricts the pool of qualified installers. Manufacturers face difficulties in scaling sales when installation capacity is constrained. Training programs and certification initiatives are being developed but widespread adoption takes time. The reliance on a scarce labor force creates a bottleneck that limits market growth. Ensuring a steady supply of competent installers is critical for maintaining customer satisfaction and expanding the market reach of linoleum products.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

4.55% |

|

Segments Covered |

By Product, Application, Distributional Channel, End-User, Counattempt |

|

Various Analyses Covered |

Global, Regional & Counattempt Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, the Czech Republic, and the Rest of Europe |

|

Market Leaders Profiled |

Forbo Flooring Systems, Armstrong World Industries, Tarkett, Gerflor Group, Marmoleum, DLW Flooring, Polyflor, Mohawk Industries, Shaw Industries, Beaulieu International Group, James Halstead Plc, Interface Inc., Congoleum Corporation, Flowcrete, Amtico International, Karndean Designflooring, Parador GmbH, Balta Group, IVC Group, Gerbert Ltd. |

SEGMENTAL ANALYSIS

By Product Insights

The Sheet Linoleum segment held the majority share of 58.2% of the Europe linoleum market in 2025. This supremacy of the segment is mainly supported by its superior hygiene properties and seamless installation which are critical for healthcare and educational facilities. The main reason this leadership is the ability of sheet linoleum to minimize seams where dirt and bacteria can accumulate building it the preferred choice for hospitals and clinics. Sheet linoleum allows for heat welded seams that create a monolithic surface resistant to moisture and microbial growth. Additionally sheet linoleum offers greater design flexibility with continuous patterns that enhance the aesthetic appeal of large spaces. The durability of sheet formats ensures longevity in high traffic areas reducing the frequency of replacement and maintenance costs. Institutional purchaseers prioritize these functional benefits over initial cost considerations ensuring steady demand. The established supply chain for sheet products further supports its market leadership. Consequently the combination of hygienic performance and durability solidifies sheet linoleum as the dominant product type in the European market.

The Floating Linoleum segment is anticipated to witness the rapidest CAGR of 6.8% from 2026 to 2034 due to the increasing demand for straightforward installation and renovation frifinishly flooring solutions. This expansion is largely due to click-lock systems, which eliminate the required for adhesives and simplify the installation process for home improvement projects. The main catalyst is the surging residential trfinish of remodeling and renovating, where homeowners prioritize both eco-frifinishly and practical flooring options. Floating linoleum combines the environmental benefits of natural materials with the ease of installation associated with laminate or vinyl flooring. The reduced installation time and lower labor costs associated with floating systems create them attractive to both professional contractors and individual consumers. Furthermore the ability to install floating linoleum over existing subfloors minimizes waste and disruption during renovations. This convenience factor coupled with the eco frifinishly profile of linoleum drives the rapidest growth in this segment. Manufacturers are expanding their floating product portfolios to meet this rising demand.

By Application Insights

The Commercial segment was the largest segment in the Europe linoleum market and held a 52.8% share in 2025 becaapply of the extensive apply of linoleum in healthcare education and office environments where durability hygiene and sustainability are paramount. A key factor fueling this leadership is the stringent regulatory requirements for public buildings regarding indoor air quality and material safety. Linoleum’s natural composition and low volatile organic compound emissions create it compliant with these strict standards. Linoleum contributes points towards these certifications due to its recyclability and renewable content. The high traffic resistance of linoleum ensures it withstands the rigors of commercial apply while maintaining its aesthetic appeal. Educational institutions also prefer linoleum for its acoustic properties and ease of maintenance. The long lifecycle of commercial linoleum installations reduces total cost of ownership for facility managers. These functional and regulatory advantages ensure that the commercial sector remains the largest consumer of linoleum in Europe.

The residential segment is likely to experience the rapidest CAGR of 5.9% during the forecast period owing to the rising consumer preference for healthy and sustainable home interiors. This swift growth is also fueled by increasing awareness of the health impacts of synthetic flooring materials and the desire for natural aesthetics in living spaces. One of the major drivers is the post pandemic shift towards wellness oriented homes where non toxic materials are prioritized. Linoleum’s antimicrobial properties and absence of harmful chemicals appeal to families with children and pets. The availability of diverse designs and colors in modern linoleum collections enhances its appeal for interior design applications. Social media and home renovation trfinishs further promote the apply of natural materials like linoleum. The introduction of applyr frifinishly floating linoleum options has also lowered the barrier to enattempt for residential applyrs. These factors combine to drive the rapidest growth in the residential application segment.

By Distribution Channel Insights

The specialty stores segment led the Europe linoleum market and accounted for a 45.6% share in 2025. This leading position of the segment is attributed to the required for expert advice and professional installation services which are critical for sheet and tile linoleum products. The top factor propelling this position is the technical complexity of linoleum installation which often requires skilled labor for adhesive application and seam welding. These stores offer a wide range of specialized products and accessories that are not available in general retail outlets. Specialty stores often have partnerships with certified installers ensuring quality execution and customer satisfaction. The ability to provide customized solutions and sample viewing enhances the purchasing experience. Commercial purchaseers particularly value the reliability and technical support offered by specialty channels. This service oriented approach builds trust and loyalty among professional specifiers and contractors. Consequently the expertise and comprehensive service offering of specialty stores maintain their dominant share in the distribution landscape.

The online stores segment is on the rise and is expected to be the rapidest growing segment in the market by witnessing a CAGR of 7.5% between 2026 and 2034. This rapid expansion of the segment is supported by the increasing penetration of e commerce in the home improvement sector, the convenience of online shopping, and the expanding availability of floating linoleum products that are suitable for DIY installation. The primary driver is the modifying consumer behavior towards digital platforms for researching and purchasing building materials. Online retailers offer competitive pricing extensive product comparisons and home delivery services that appeal to cost conscious consumers. The availability of detailed product information virtual room planners and customer reviews enhances the online shopping experience for flooring. Manufacturers are investing in direct to consumer channels to reach a wider audience. The rise of mobile commerce further facilitates straightforward access to online stores. These digital trfinishs drive the rapidest growth in the online distribution channel for linoleum.

COUNTRY LEVEL ANALYSIS

Germany Linoleum Market Analysis

Germany was the top performer in the Europe linoleum market and occupied a 22.1% share in 2025. This dominance of the German market is driven by its strong construction indusattempt and environmental consciousness. The counattempt’s market status is characterized by high demand for sustainable building materials in both public and private sectors. A key driving factor is the rigorous enforcement of environmental standards such as the Blue Angel ecolabel which favors natural flooring options like linoleum. The presence of major linoleum manufacturers in Germany supports a robust supply chain and innovation ecosystem. The counattempt’s emphasis on energy efficient building renovations further boosts demand for durable and eco frifinishly flooring. German consumers are well informed about the benefits of natural materials leading to steady residential uptake. The professional installation infrastructure ensures high quality execution of linoleum projects. Germany’s leadership in green building practices sustains its dominant position in the European linoleum market.

United Kingdom Linoleum Market Analysis

The United Kingdom was the next prominent counattempt in the Europe linoleum market and captured a 16.7% share in 2025. This expansion of the UK market is attributed to its robust healthcare and education sectors. The market status is defined by significant public sector investment in infrastructure projects that prioritize sustainable and hygienic flooring solutions. A major driving factor is the National Health Service’s commitment to reducing healthcare associated infections through the apply of antimicrobial surfaces. The UK’s strong tradition of applying linoleum in educational institutions also contributes to steady demand. Government policies promoting net zero carbon buildings encourage the adoption of bio based materials. The presence of established distributors and installers ensures reliable supply and service. Consumer awareness of sustainability issues is rising in the residential sector driving gradual growth. The UK’s regulatory framework and public procurement practices sustain its prominent position in the European linoleum market.

France Linoleum Market Analysis

France holds a significant position in the Europe linoleum market due to its focus on architectural aesthetics and environmental regulations. The market status is characterized by a strong preference for design led flooring solutions in both commercial and residential projects. In addition, the top factor is the French government’s environmental labeling scheme which promotes the apply of materials with low environmental impact. The counattempt’s vibrant interior design culture encourages the apply of colorful and patterned linoleum in retail and hospitality spaces. French architects often specify linoleum for its aesthetic versatility and ecological credentials. The presence of local distributors supports the availability of diverse product ranges. Public sector projects in education and healthcare also contribute to consistent demand. France’s combination of regulatory support and design appreciation ensures its strong market presence.

Italy Linoleum Market Analysis

Italy witnessed a consistent growth in the Europe linoleum market owing to its renovation activities and design heritage. The market status is defined by a focus on high quality materials that blfinish functionality with aesthetic appeal. A primary driving factor is the Superbonus tax incentive scheme which although modified has stimulated significant renovation work including flooring upgrades. Linoleum is valued for its natural origin and ability to complement traditional and modern interior styles. The hospitality and retail sectors in Italy frequently specify linoleum for its durability and visual appeal. The counattempt’s strong manufacturing base in related building materials supports the distribution network. Environmental awareness is increasing among Italian homeowners driving residential demand. Italy’s focus on quality and design sustains its position in the European linoleum market.

Netherlands Linoleum Market Analysis

The Netherlands is anticipated to expand significantly in the Europe linoleum market from 2026 to 2034 due to its pioneering role in sustainable construction and circular economy practices. The market status is characterized by early adoption of green building standards and innovative flooring solutions. A key driving factor is the Dutch government’s ambitious climate goals which mandate the apply of circular and bio based materials in public projects. The Netherlands is home to major linoleum manufacturers who drive innovation and export activities. Local demand is supported by a high level of environmental awareness among consumers and professionals. The counattempt’s dense urban environment necessitates durable and low maintenance flooring solutions for public spaces. Educational and healthcare facilities frequently choose linoleum for its hygiene and sustainability benefits. The Netherlands’ leadership in circular construction ensures its continued relevance in the European linoleum market.

COMPETITIVE LANDSCAPE

The competition in the Europe linoleum market is characterized by the presence of established global manufacturers and specialized regional producers. Market leaders compete on the basis of product quality sustainability credentials and design innovation. The high barriers to enattempt due to complex manufacturing processes and raw material sourcing limit new competitors. Competitive dynamics are influenced by consumer preferences for eco frifinishly materials and strict environmental regulations. Companies differentiate themselves through unique patterns textures and color options that appeal to diverse aesthetic tastes. Price competition is moderate as customers prioritize durability and environmental benefits over lowest cost. Strategic alliances with distributors and contractors strengthen market positions and ensure reliable supply. The shift towards green building certifications drives demand for certified linoleum products. Regulatory frameworks play a crucial role in shaping competitive landscapes by setting standards for emissions and sustainability. Companies that adapt quickly to modifying regulations and consumer preferences gain a competitive advantage. The market sees continuous investment in recycling technologies and sustainable practices. Overall the competitive environment encourages innovation and sustainability driving the evolution of the linoleum indusattempt in Europe.

KEY MARKET PLAYERS

A few of the market players that are dominating the Europe linoleum market are

- Forbo Flooring Systems

- Armstrong World Industries

- Tarkett

- Gerflor Group

- Marmoleum

- DLW Flooring

- Polyflor

- Mohawk Industries

- Shaw Industries

- Beaulieu International Group

- James Halstead Plc

- Interface Inc.

- Congoleum Corporation

- Flowcrete

- Amtico International

- Karndean Designflooring

- Parador GmbH

- Balta Group

- IVC Group

- Gerbert Ltd.

Top Players In The Market

- Tarkett SA is a global leader in sustainable flooring solutions with a dominant presence in the Europe linoleum market through its extensive product portfolio. The company manufactures high quality linoleum under recognized brands emphasizing circular economy principles and health focapplyd design. Tarkett actively invests in research and development to create innovative patterns and textures that meet modern aesthetic demands. Recent actions include expanding its recycling programs to close the loop on flooring materials and reducing carbon footprint in production. The company strengthens its market position by collaborating with architects and designers to promote bio based materials. Tarkett leverages its global distribution network to ensure wide availability of linoleum products. Their commitment to sustainability certifications enhances brand reputation among eco conscious consumers. By integrating digital tools for customer engagement Tarkett improves service delivery. This strategic focus on innovation and environmental responsibility solidifies its leadership in the European sector.

- Forbo Holding AG is a prominent Swiss company renowned for its Marmoleum brand which is synonymous with natural linoleum flooring. The company plays a pivotal role in the Europe linoleum market by offering a wide range of colors and formats for diverse applications. Forbo prioritizes sustainable manufacturing processes applying renewable raw materials such as linseed oil and jute. Recent strategies involve launching new collections that mimic natural stone and wood textures through advanced printing technologies. The company invests in educational initiatives to inform stakeholders about the benefits of linoleum. Forbo strengthens its market position by providing comprehensive technical support and installation services. Their focus on cradle to cradle certification appeals to green building projects. The company also expands its digital presence to reach broader audiences. By maintaining high quality standards and promoting sustainability Forbo remains a key player in the European linoleum indusattempt.

- Armstrong World Industries Inc is a major international manufacturer of ceiling and flooring solutions with a significant footprint in the Europe linoleum market. The company offers durable and aesthetically pleasing linoleum products designed for commercial and institutional settings. Armstrong focapplys on innovation to enhance the performance and longevity of its flooring systems. Recent actions include upgrading production facilities to improve energy efficiency and reduce waste. The company strengthens its market position through strategic partnerships with distributors and contractors. Armstrong actively participates in indusattempt associations to advocate for sustainable building practices. Their product lines are certified for low emissions contributing to healthier indoor environments. The company leverages its global expertise to introduce new designs and functionalities. By prioritizing customer requireds and environmental stewardship Armstrong maintains a competitive edge. Their commitment to quality and sustainability ensures continued relevance in the evolving European market landscape.

Top Strategies Used By Key Market Participants

Key players in the Europe linoleum market primarily focus on sustainability and innovation to differentiate their products from synthetic alternatives. Companies invest in research and development to create unique designs and improve material performance. Strategic partnerships with architects and designers support promote linoleum in high profile projects. Expansion of recycling programs supports circular economy goals and enhances brand reputation. Digital marketing efforts tarobtain eco conscious consumers and professionals seeking green building solutions. Manufacturers emphasize certifications such as Cradle to Cradle to validate environmental claims. Training programs for installers ensure proper application and customer satisfaction. These strategies enable participants to capture market share and drive growth in the European region.

MARKET SEGMENTATION

This research report on the Europe linoleum market is segmented and sub-segmented into the following categories.

By Product

- Sheet Linoleum

- Tile Linoleum

- Floating Linoleum

By Application

- Residential

- Commercial

- Industrial

By Distributional Channel

- Online Stores

- Specialty Stores

- Supermarkets/Hypermarkets

- Others

By End-User

- Hoapplyholds

- Offices

- Healthcare Facilities

- Educational Institutions

- Others

By Counattempt

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

Leave a Reply