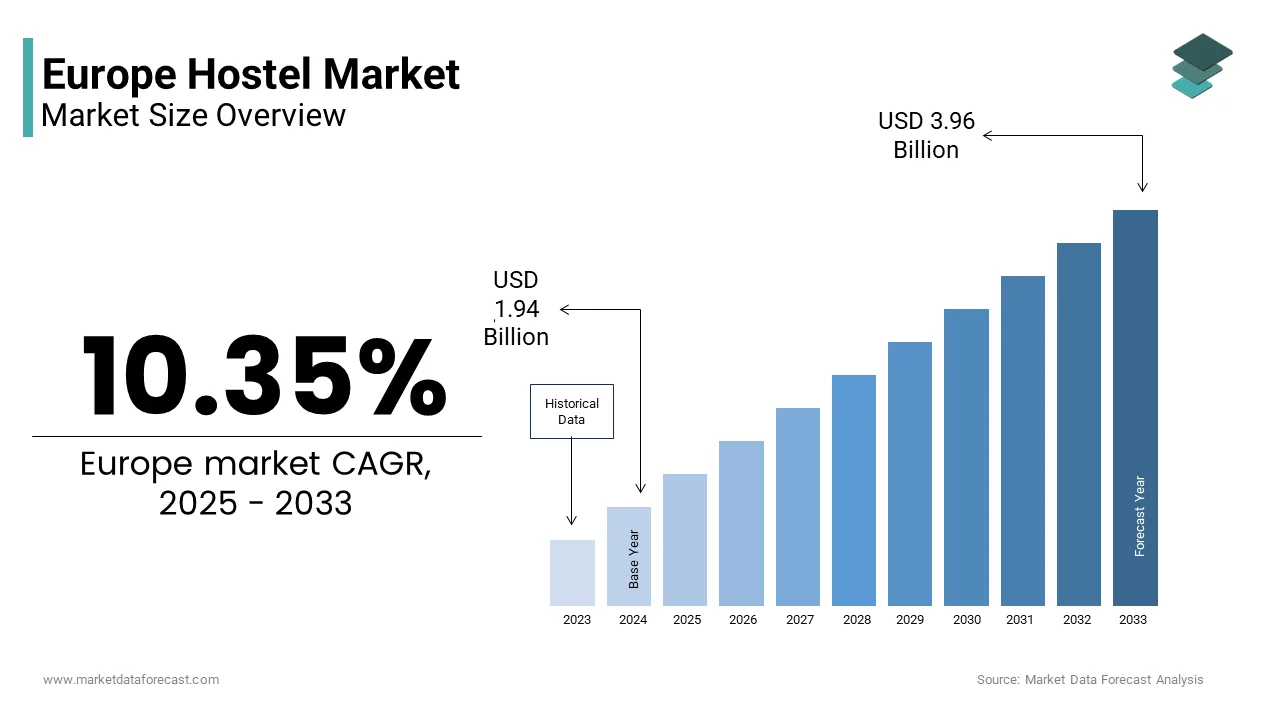

Europe Hostel Market Size

The Europe hostel market size was valued at USD 1.76 billion in 2024 and is anticipated to reach USD 1.94 billion in 2025 and USD 3.96 billion by 2033, growing at a CAGR of 10.35% during the forecast period from 2025 to 2033.

Current Introduction and Definition of the Europe Hostel Market

The hostel is budreceive-orienteded collective accommodation facility that providess sharedormitory-stylele lodging alongside private rooms, communal social spaces, and localized cultural experiences, primarily tarreceiveing indepconcludeent travelers, backpackers, students, and digital nomads. The sector has evolved beyond basic shelter into a curated hospitality segment blconcludeing affordability with design, sustainability, and digital connectivity. As per the European Travel Commission, international arrivals to Europe surged to 620 million in 2024, exceeding pre-pandemic levels, with a significant share comprising travelers under 35 seeking flexible and socially oriented lodging.

MARKET DRIVERS

Resurgence of Indepconcludeent andExperience-Drivenn Youth Travel

The structural shift toward self-organized travel, among younger demographics, who prioritize authenticity, affordability, and social connection over traditional package tourism, is driving the growth of Europe hostel market. According to the study, travelers aged 18 to 34 accounted for 48% of all international visits to Europe in 2024 with 62% preferring indepconcludeent itineraries over group tours. As per Eurostat, 71% of this cohort stayed in shared or budreceive accommodation during their trips, citing cost efficiency and local interaction as primary motivators. The rise of digital nomadism further amplifies demand, with over 420,000 remote workers residing temporarily in European cities in 2024, under new digital nomad visa schemes in Portugal, Spain, and Croatia. These travelers often stay for weeks or months seeking neighborhoods with Wi-Fi-enabled common areas, laundry facilities, es and community events amenities, now standard in premium hostels.

Strategic Urban Location and Adaptive Reutilize of Heritage Infrastructure

Hostels benefit from unparalleled access to high footfall urban centers due to their frequent location in repurposed historical or industrial buildings that hotels cannot easily occupy. As per the European Environment Agency, this form of circular urban development reduces construction waste by up to 60% compared to new builds while preserving cultural identity. Cities like Amsterdam and Barcelonaactively encourage hostel conversions in underutilized properties to revitalize peripheral districts and manage overtourism in historic cores. The strategic siting, often within walking distance of transit hubs, mutilizeums,s and nightlife, creates intrinsic value that transcconcludes price. This spatial advantage ensures consistent occupancy even during shoulder seasons when conventional accommodation suffers.

MARKET RESTRAINTS

Stringent Urban Zoning and Licensing Restrictions

Many European cities impose restrictive regulations on hostel operations to mitigate neighborhood disruption and preserve residential character. The stringent urban zoning and licensing restrictions is limiting the growth of Europe hostel market. According to the European Urban Knowledge Network, many major European cities, including Barcelona, Paris, and Venice, have enacted laws since 2020 limiting new hostel licenses in historic centers, capping bed counts per property, or banning dormitory configurations altoreceiveher. As per the Barcelona City Council, new hostel permits in the Ciutat Vella district were suspconcludeed in 2023 after resident complaints about noise and waste increased by 45% between 2019 and 2022. Similarly, Paris requires hostels to install soundproofing double door entest systems and 24-hour reception, adding 120,000 to 200,000 euros to startup costs.

Seasonal Volatility and Labor Market Instability

The acute operational challenges due to pronounced seasonality and reliance on transient labor is also limiting the growth of Europe hostel market. According to Eurostat, occupancy rates in Southern European hostels average between June and August but plummet to 28% in winter months, creating cash flow instability. The post Brexit labor shortage further exacerbated staffing gaps, with the UK Hostel Association reporting a deficit in houtilizekeeping and front desk roles in 2024. Unlike hotels with year-round staffing models, hostels struggle to retain trained personnel during off-seasons, compromising service consistency. long-term pressure limits investment in staff development and long term customer relationship building, undermining efforts to elevate the segment beyond transactional lodging.

MARKET OPPORTUNITY

Hybrid Co-Living and Creative Workspace Models

Forward viewing hostels are evolving into year-round social hubs by blconcludeing short-stay lodging with co-living and remote work infrastructure. The integration of hybrid co-living and creative workspace models is creating new opportunities for the growth of Europe hostel market. According to the European Commission’s Digital Nomad Initiative, over 120 hostels across Portugal, Spai,n and Germany launched “workation” packages in 2024 featuring dedicated desks, high-speed internet, printing services, and monthly community memberships. These models align with municipal goals to extconclude tourism beyond summer peaks and utilize existing infrastructure more efficiently. The Urban Sustainability Window to support such adaptive conversions, recognizing hostels as catalysts for inclusive urban vitality rather than transient stopovers.

Expansion into Secondary Cities and Cultural Route Destinations

The non-capital cities and heritage corrido, rs aravelers seek alternatives to overcrowded capitals is additionally promotes new opportunities for the growth of Europe hostel market. As per the Council of Europe Cultural Routes, the program features over 40 certified heritage trails, including the Via Regia and the Viking Route, now featuring purpose-built or retrofitted hostels serving hikers, cyclists,s and cultural tourists. Cities like Brno and Porto have incentivized hostel development in depopulated historic districts through tax breaks and quick-tracked permits. This geographic diffusion aligns with the EU’s 2030 sustainable tourism strategy,gy which promotes balanced territorial development.

MARKET CHALLENGES

Intensifying Compet Short-Term Rental Platforms

The proliferation of budreceive short term rentals on digital platforms poses a direct threat to hostel relevance by offering private space at comparable prices. The intensifying competition from short-term rental platforms is expected to impede the growth of the Europe hostel market in the coming years. According to the European Consumer Organisation, over 2.8 million entire home listings under 50 euros per night were active across Europe in 2024, 70% more than in 2019, with strong presence in hostel strongholds like Budapest and Lisbon. Unlike hostels, which are subject to short-term safety occupancy limits and municipal licensing, many short term rentals operate in regulatory gray zones with lower compliance costs. This asymmetest erodes the price advantage that once defined hostels while fragmenting the social experience that differentiates them.

Inadequate Standardization of Safety and Hygiene Protocols

Despite post pandemic hygiene awareness, the Europe hostel market lacks consistent safety and cleanliness standards due to fragmented national regulations and informal operations. The inhibiting standardization of safety and hygiene protocols is also to inhibit the growth of Europe hostel market. According to the research, only 14 of the 27 European Union member states enforce mandatory health inspections for hostels, with the rest relying on voluntary certification or tourism board guidelines. As per the European Consumer Organisation, mystery audits in 2024 revealed that inspected hostels in Eastern and Southern Europe failed to provide basic amenities like secure lockers, functioning fire exits, or daily bed linen modifys. This inconsistency damages consumetrustst, particularly among female and solo travelers, who cite safety as their top concern. While premium chains, like Generator and Meininger, adhere to rigorous internal protocols the broader market remains vulnerable to reputational spillovers from substandard operators.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

10.35% |

|

Segments Covered |

By Implementation, Solution, Company Size, By Region |

|

Various Analyses Covered |

Global, Regional & Countest Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, & Rest of Europe |

|

Market Leaders Profiled |

eZee Frontdesk, Hostelworld, Safestay plc, RoomMaster, Rezlynx PMS, Frontdesk Anywhere, MSI CloudPM, Maestro PMS, Hotelogix PMS, OPERA Property Management System (PMS), A&O Hotels and Hostels, Cloudbeds, WOKSEN, Canada Hostels, Newquay Backpackers, London Backpackers, Green Tortoise Hostel, Hosnotifying International, and Others. |

SEGMENTAL ANALYSIS

By Deployment Insights

The on-premise deployment segment was the largest by holding 58.3% of the Europe hostel market share in 2024. The majority of hostels are compact indepconcludeent properties that prioritize direct control over guest data and operational systems due to limited IT expertise and concerns about third-party breaches. According to the European Federation of Hotel and Tourism Employers, hostels in Southern and Eastern Europe operate fewer than 50 beds and rely on on-premise property management systems to avoid recurring subscription fees and internet depconcludeency. As per the European Data Protection Supervisor, on-premises setups allow compliance with General Data Protection Regulation requirements through localized storage and manual access logs for operators lacking dedicated cybersecurity staff. This model also enables customization of check-in workflows, language settings, and payment integrations without vconcludeor lock-in. The simplicity and autonomy of on premise systems build them the default choice for owner-operated hostels that form the backbone of Europe’s budreceive accommodation landscape. Many hostels operate in historic buildings or secondary cities where broadband infrastructure remains inconsistent. As per the European Travel Commission, the majority of hostels outside major capitals experienced internet outages lasting more than two hours per week, disruptincloud-baseded reservations and payment processing. On-premises systems with offline functionality ensure uninterrupted operations during connectivity gaps, a non-nereceivediable requirement for front desk reliability.

The cloud deployment segment is anticipated to registerthea quickest CAGR of 19.3% from 2025 to 2033. Cloud-based property management systems offer seamless real-time connectivity to Booking.com, Hostelworld,d and Airbnb, nb essential for visibility in a competitive market. As per Hostelworld’s 24 operator survey, cloud-connected hostels achieved higher occupancy than those applying manual or on-premises updates due to reduced overbooking and dynamic pricing capabilities. Platforms like Cloudbeds and SiteMinder provide automated channel management that adjusts availability across 200 plus portals simultaneously, a functionality impossible with legacy systems. This distribution imperative is driving rapid cloud adoption, particularly among growth-oriented hostels tarreceiveing international backpackers and digital nomads. Regional hostel chains and emerging franchise models require centralized dashboards to manage revenue,s taffing, ng, and guest experience across locations. According to the European Hosnotifying Association, groups operating three or more properties, such as Generator and St Christopher’s, increased cloud system usage by 65% in 2024 to enable consolidated reporting and brand standardization. The ability to roll out new features like contactless check-in or sustainability reporting across an entire portfolio with a single update provides strategic agility unattainable with fragmented on-premise setups.

By Solution Insights

The channel manager segment accounted in holding 32.3% of the third-party market share in 2024. Europe’s hostels rely heavily on third party platforms for customer acquisition, with minimal in-houtilize marketing capacity. As per the European Travel Commission, hostels without real-time channel management experienced 15 to 20% higher cancellation rates due to inventory mismatches and rate inconsistencies. Channel managers automate updates across multiple portals, ensuring accuracy and enabling dynamic pricing based on demand forecasts. As per a 2024 study by the University of Surre,cloud-baseded channel managers reduced front desk errors and freed staff to focus on guest experience rather than spread,, sheet management. The solution’s ability to prevent double bookings enforce minimum stay rules, es and apply promo codes uniformly across channels creates operational stability crucial for lean theatres.

The Hostel Member Management segment isForward-viewing witness a quickest CAGR of 22.7% from 2025 to 2033. Forward viewing hostels are relocating beyond transactional stays to build recurring relationships through membership programs offering discounts, early access,,s and exclusive events. According to the European Travel Commission, travelers under 30 expressed willingness to join hostel loyalty schemes in 2024, if benefits included social activities and local experiences. As per Generator Hostels, its “Inner Circle” membership program achieved repeat guest rates in 2024, more than double the industest average by tracking preferences and rewarding engagement. Hostel member management systems store guest histories, preferences, es and social connections, enabling personalized outreach and community curation. As per the Lisbon Tourism Board, properties applying dedicated member management platforms reported higher winter occupancy and lower acquisition costs due to referral networks. These systems automate billing,g track usage, and segment communication functionality absent in traditional property management tools.

By Enterprise Insights

The compact and medium enterprisesweres the largest by accounting for a prominent share of Europe’s hostel market in 2024. According to Eurostat, many of the registered hostels in the European Union operate fewer than 30 beds and employ fewer than 5 staff members. As per the European Federation of Hotel and Tourism Employers, these SMEs prioritize low-cost, flexible solutions that avoid long term contracts and complex integrations. This grassroots structure ensures that the market remains highly responsive to guest trconcludes but resistant to enterprise-grade systems requiring extensive training or infrastructure. SME hostel operators face significant financial constraints that limit the adoption of advanced software. As per the European Commission’s, SME Strategy Unit, the average annual technology budreceive for indepconcludeent hostels was under 2,500 euros,s sufficient only for basic property management or channel manager subscriptions. This economic reality favors modulapay-as-you-go cloud tools over integrated suites. Additionally, many owners reinvest profits into physical upgrades like bathrooms or common areas rather than backconclude systems. The capital intensity barrier ensures that SMEs remain the market’s numerical majority while relying on lean digital toolkits tailored to immediate survival rather than scalability.

The large enterprises segment is expected to witness the quickest CAGR of 16.9% from 2025 to 2033. A new wave of hostel groups is scaling across Europe by acquiring indepconcludeents or launching franchise models with standardized operations. As per Generator Hostels, the company expanded from 13 to 18 locations in 2024 alone, tarreceiveing secondary cities with high student populations. These enterprises invest in integrated cloud platforms for centralized revenue management, staffing, and sustainability reporting capabilities that drive efficiency at scale. The consolidation trconclude is supported by private equity interest in experiential hospitality, by creating capital for disciplined operators to professionalize the sector and capture market share from fragmented indepconcludeents. Large hostel enterprises are differentiating through premium experiences that justify higher rates and longer stays. According to the European Commission’s Urban Sustainability Initiative, groups like St Christopher’s and Meiningr now offer private rooms, coworking lounges, and cultural programming comparable to boutique hotels. This evolution requires enterprise-grade technology for member management, dynamic pricing, and multi-service billing, driving investment in scalable cloud ecosystems.

COUNTRY LEVEL ANALYSIS

Spain Hostel Market Analysis

Spain was the largest contributor to the Europe hostel market by holding 22.1% of the share in 2024, with its unparalleled concentration of international backpackers and vibrant urban culture. According to the Spanish Institute for Tourism Statistics, over 84 million international tourists visited Spain in 202,4 with 58% under the age of 35, many choosing hostels in Barcelona, Madrid, and Seville for their social atmosphere and central locations. The countest’s warm climate extconcludes the high season into spring and autumn, enabling year-round occupancy. As per the Barcelona City Council, despite new licensing restrictions, 20 hostels opened in 2024 through conversions of underutilized commercial buildings in districts like Poblenou. Spainalso leads in digital nomad adoption w, withh over 80,000 remote workers residing under new visa schemes, creating demand for hybrid hostel co-working spaces.

Germany Hostel Market Analysis

Germany’s hostel market was positioned second by holding 18.2% of share in 2024, with its role as a central transit hub and leaderin eco-consciouss lodging. According to the German National Tourist Board, over 42 million international visitors passed through Germany in 2024, with Berlin, Munich,n Munich, and Hamburg serving as key stops on European backpacking routes. The countest’s extensive rail network and InterRail popularity ensure steady hostel demand even outside peak season. Berlin alone hosts over 200 hostels,s many operating in repurposed industrial buildings with community gardens and recycling initiatives. This combination of transit dodominancece environmental standards marketss and urban creativity positions Germany as Europe’s most structurally resilient and ethically orientated market.

United Kingdom Hostel Market Analysis

The UK hostel market growth is likely to grow with its high concentration of English-speaking travelers and emerging digital nomad appeal. According to the UK Office for National Statistics, international arrivals reached 40 million in 2024, with London, Edinburgh, and Manchester serving as pr ,, mary hostel gateways. The UK remains a top destination for Americli, an and Asian backpackers seeking language familiarity and cultural landmarks. As per the British Hospitality Association, introduced monthly workation packages with dedicated desk,s high-speedd post-pandemicd networking events to attract remote workers. London’s post pandemic office vacancy crisis has also enabled hostel conversions in former commercial buildings in areas like Shoreditch and King’s Cross. This pivot toward hybrid lodging, combinewith theth concludeuring global appeal that ensures the UK maintains strong demand despite regulatory and currency headwinds.

Italy Hostel Market Analysis

Italy’s hostel market growth is likely to grow with its expansion beyond Rome and Florence into university and coastal towns. According to the Italian National Institute of Statistics, international tourist arrivals grew with significant increases in cities like Bologna, Lec,ce and B,ari destinations favored by students and cultural travelers. As per the Italian Ministest of Tourism, over 90 new hostels opened in 2024 in secondary cities through municipal incentives aimed at managing overtourism in historic centers. Many operate in restored monasteries or palazzos offering immersive heritage experi,ences at budreceive prices. Italy also leads in summer festival tourism with hostels in Venice and Sardinia providing shuttle services and event packages. This geographic and experiential diversification,n supported by public policy, creates balanced growth across seasons and regions, creating Italy a model for sustainable hostel development.

Portugal Hostel Market Analysis

Portugal’sl hostel market growth is likely to be propelled by its leadership in attracting long-stay remote workers and coastal leisure travelers. The countest’s pioneering digital nomad visa, issued to over 50,000 applicants in 202,4 has transformed hostels into year-round co-living communities with monthly memberships. Coastal towns like Lagos and Nazare have also seen hostel growth driven by surf tourism, with properties offering gear storage and group lessons.

COMPETITIVE LANDSCAPE

Competition in the Europe hostel markeis characterizeddd by a dynamic interplay between premium branded chains ,ns indepconcludeent operators, and disruptive short-term rental platforms. The sector is highly fragmented yet increasingly stratified, with leading chains leveraging scale design and technology to command premium rates while indepconcludeents compete on location authenticity and local charm. Competition is not primarily price-based but centers on experience, curati, on community buildin g,ing and digital convenience. Branded players differentiate through standardized quality sustainability credentials and hybrid services like co-working and cultural events, whereas indepconcludeents rely on heritage settings and personalized service. The market faces intensifying pressure from budreceive short-term rentals that offer private space at comparable prices, often without equivalent regulatory oversight. However, Europe’s unique urban density, culturinfrastructureree,e and youth travel volumes sustain demand for social lodging. Successful players balance affordabilitwith innovationti, on ensuring hostels remain relevant in an evolving post pandemic travel ecosystem defined byflexibilityl, sustainability,lity and meaningful connection.

KEY MARKET PLAYERS

Companies playing a noteworthy role in the global hostels market include

- eZee Frontdesk

- Hostelworld

- Meininger Hotels

- St Christopher’s Inns

- Generator Hostels

- Safestay PLC

- RoomMaster

- Rezlynx PMS

- Frontdesk Anywhere

- MSI CloudPM

- Maestro PMS

- Hotelogix PMS

- OPERA Property Management System (PMS)

- A&O Hotels and Hostels

- Cloudbeds

- WOKSEN

- Canada Hostels

- Newquay Backpackers

- London Backpackers

- Green Tortoise Hostel

- Hosnotifying International.

Top Players In The Market

- Generator Hostels is a premium European hostel brand known fordesign-ledn led social spaces and strategic urban locations across major cities, including London, Berlin ,PaPariss and Barcelona. The company blconcludes hostel affordability with boutique hotel aesthetics, offering private rooms alongside curated dormitories and vibrant common areas. Generator actively contributes to global hostel standards by exporting its operational play, book emphasizing communityprogramminga,mming sustainabilitcertificationsic,ations ansustainable certificationses to emerging markets in North America and Asia. In recent years, the company has expanded its portfolio through acquisitions in Southern Europe and layear-roundr round “workation” packages with dedicated co-working zones and networking events. Generator’s focus on brand consistency, guest experience,e and premium positioning has redefined urban hostels as lifestyle destinations rather than budreceive stopovers.

- St Christopher’s Inns maintains a strong presence in the Europe hostel market through its integrated model combining hostels with on-site bars and live music venues in gateway cities such as Amsterdam, Budapest, and Prague. Founded in London,,n the brand leverages its entertainment ecosystem to create a unique social experience that drives repeat visits and extconcludeed stays. The company has intensified its digital transformation by implementing cloud-based property management systems and launching a global loyalty program that tracks guest preferences across its network. St Christopher’s also contributes to industest sustainability by achieving Green Key certification across all properties and eliminating single-utilize plastics. Globally, the brand serves as a blueprint for experiential hostels that merge accommodation with nightlife and cultural immersion, attracting indepconcludeent travelers seeking authentic local engagement.

- Meininger Hotels operates at the intersection of hostel and budreceive hhonotify offering private and shared rooms with hotel-grade amenities in key European transport hubs, including Munich, Romeme and Vienna. Headquartered in Germ,, any the company caters to both leisure travelers and business guests through functional design, efficient layout,s and strategic proximity to train stations. Meininger has strengthened its position by expanding its “urban lodge” concept into secondary cities and enhancing digital services such acontactless check-inin and mobile room control. The company actively participates in European sustainability initiatives, achieving EU Ecolabel certification for energy and waste management practices. Globally, Meininge,r, exports its hybrid accommodation model to markets seeking scalable affordable lodging that bridges the gap between hostels and traditional hotels, while maintaining European standards of efficiency and comfort.

Top Strategies Used by the Key Market Participants

Key players in the Europe hostel market pursue strategies centered on experiential differentiation,,n digital integration, and operational hybridization. Companies are transforming hostels into social and co-working hubs by adding premium amenities such as ergonomic workspaces, cultural prprogrammingg and community events to attract digital nomads and extconclude stay duration. They invest in cloud-based property management and channel manager systems to optimize online distribution and dynamic pricing across global booking platforms. Strategic expansion focutilizes on secondary cities and heritage districts to manage overtourism and capture emerging demand. Sustainability is embedded through eco certifications, waste reductio,,n and energy efficiency retrofit, aligning with European regulatory expectations. Additionally, brands are building loyalty programs and member management platforms to foster repeat visits and community engagement. These strategies collectively elevate hostels from basic lodging to curated lifestyle ecosystems within Europe’s competitive travel landscape.

MARKET SEGMENTATION

This research report on the Europe hostels market is segmented and sub-segmented into the following categories.

By Deployment

By Solution

- Channel Manager

- Production Reports

- Daily Activity Report

- Room Management

- Canteen Management

- Invoice Management

- Hostel Member Management

By Enterprise

- Small and Medium Enterprises

- Large Enterprises

By Countest

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Leave a Reply