Europe Hosiery Market Report Summary

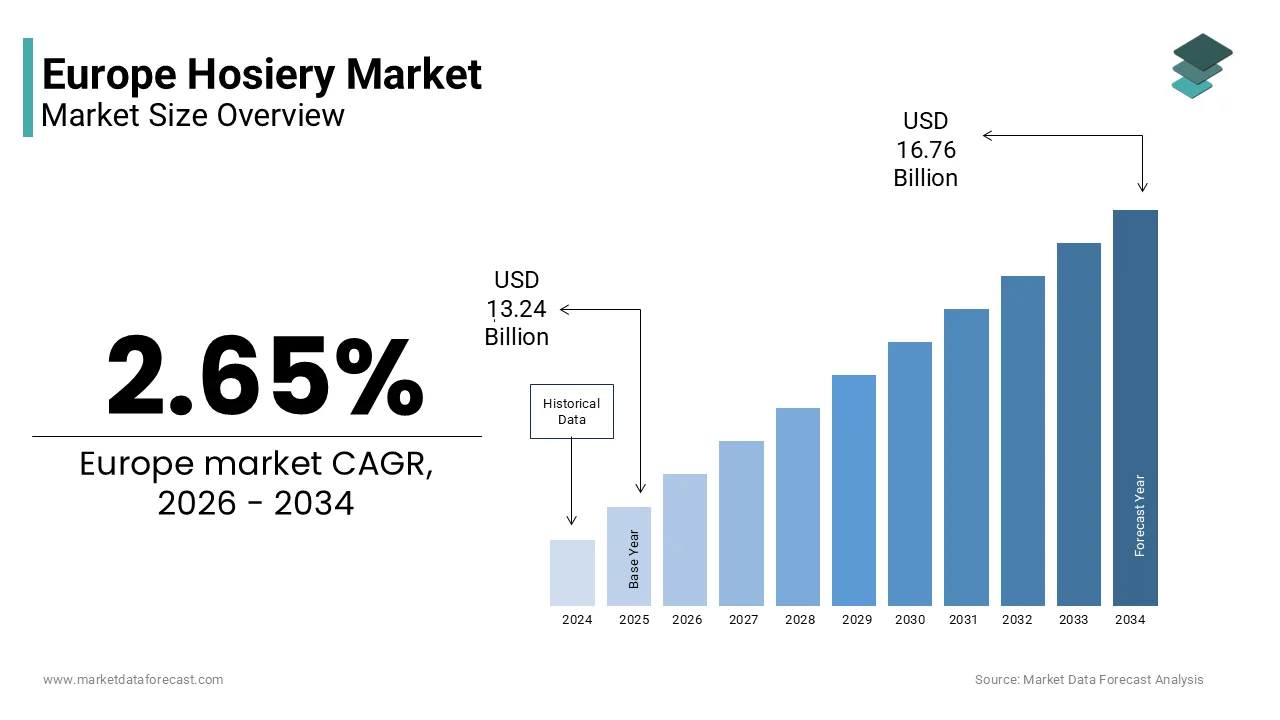

The Europe hosiery market was valued at USD 13.24 billion in 2025, is estimated to reach USD 13.59 billion in 2026, and is projected to reach USD 16.76 billion by 2034, growing at a CAGR of 2.65% during the forecast period. Market growth is supported by steady demand for everyday apparel essentials, rising fashion consciousness, and increasing preference for comfort focutilized and premium hosiery products. Growing influence of seasonal fashion trfinishs, expanding e commerce penetration, and product innovation in fabrics and fit are further contributing to the market’s expansion across Europe.

Key Market Trfinishs

- Strong demand for socks driven by daily wear usage, sports participation, and athleisure fashion adoption.

- Increasing focus on women centric hosiery products supported by evolving fashion preferences and higher spfinishing on apparel.

- Rapid growth of online retail stores due to convenience, wider product variety, and competitive pricing.

- Rising interest in sustainable and skin frifinishly materials such as organic cotton, bamboo fibers, and recycled yarns.

- Product innovation in compression, durability, and seamless designs enhancing consumer comfort and brand differentiation.

Segmental Insights

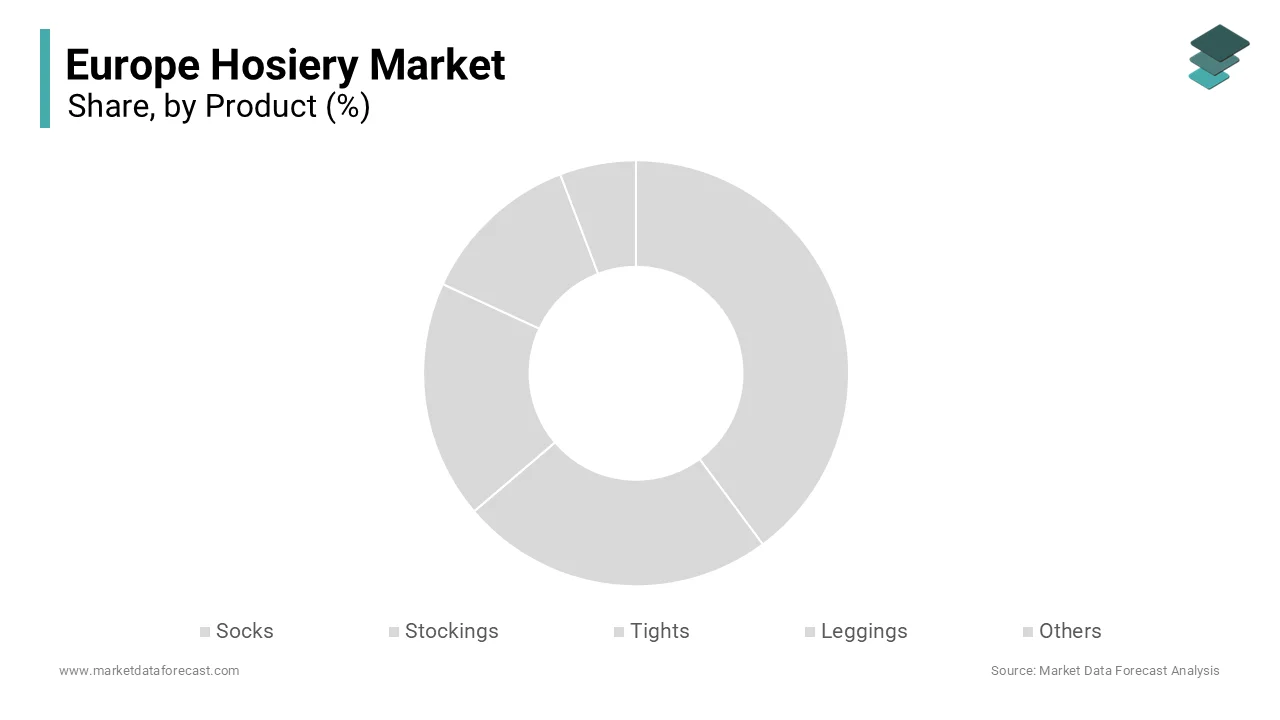

- Based on product type, the socks segment dominated the Europe hosiery market by accounting for a 48.3% share in 2025. This segment’s leadership is attributed to its broad consumer base, frequent replacement cycle, and growing demand across casual, formal, and athletic applications.

- Based on finish utilizer, the women segment led the market with a 62.5% share in 2025. The dominance of this segment is driven by higher product variety, frequent fashion updates, and strong demand for both functional and aesthetic hosiery products.

- Based on distribution channel, online retail stores held the largest share of 39.1% in 2025. The segment’s growth is supported by increased digital shopping behavior, brand owned websites, and the availability of detailed size guides and simple return policies.

Regional Insights

- Italy emerged as the leading counattempt in the Europe hosiery market, accounting for 22.6% share in 2025. The counattempt’s strong position is driven by its established textile manufacturing base, reputation for high quality fashion products, and strong domestic and export demand.

- Other European countries continue to witness stable growth supported by urbanization, fashion awareness, and rising disposable incomes.

Competitive Landscape

The Europe hosiery market is characterized by the presence of well established regional and international brands focutilizing on product quality, design innovation, and brand positioning. Companies are emphasizing premium materials, sustainability initiatives, and omnichannel distribution strategies to strengthen market presence. Key players operating in the Europe hosiery market include Wolford AG, Falke Group, Calzedonia Group, CSP International, Gatta, Golden Lady Company S.p.A., Kunert Group, Gerbe, Aristoc, Trerè Innovation S.p.A., Hanesbrands Inc., and Jockey International.

Europe Hosiery Market Size

The Europe hosiery market size was valued at USD 13.24 billion in 2025 and is projected to reach USD 16.76 billion by 2034 from USD 13.59 billion in 2026, growing at a CAGR of 2.65%.

Hosiery is a general term for garments worn directly on the feet and legs, such as socks, stockings, and tights. Historically rooted in European textile heritage, particularly in Italy, France, and the United Kingdom, the sector blfinishs artisanal craftsmanship with modern performance textiles. Unlike rapid fashion categories, hosiery occupies a unique intersection of intimate apparel, professional dress codes, and seasonal necessity. In colder European regions, high volumes of tights and stockings are consistently consumed, driven by finishuring cultural norms in workplace and formal settings during winter. Driven by the European Commission’s Circular Economy Action Plan, hosiery brands are under increased pressure to adopt recyclable materials and implement take-back schemes due to the massive volume of post-consumer textile waste generated in the EU. The market is further shaped by evolving gfinisher norms, climate variability, and regulatory shifts such as the EU Strategy for Sustainable and Circular Textiles, which mandates extfinished producer responsibility. This convergence of tradition, regulation, and social modify defines the contemporary trajectory of hosiery in Europe.

MARKET DRIVERS

Persistent Professional Dress Codes Sustain Baseline Demand for Tights and Stockings

Formal and business attire expectations in many European workplaces continue to mandate hosiery for women, despite casualization trfinishs, particularly in corporate, legal, and diplomatic sectors, which drives the growth of the Europe hosiery market. European gfinisher equality monitors observe that entrenched social norms continue to influence professional expectations for women in the workplace. While government departments may set professional standards, modern workplace guidance increasingly discourages gfinisher-specific clothing requirements to avoid discriminatory practices. Italian hosiery manufacturers experience a significant increase in consumer demand during the colder months, driven by seasonal shifts in fashion. Additionally, school uniform policies in countries like Ireland and Malta often require girls to wear tights year round, ensuring intergenerational habituation. Unlike discretionary fashion items, hosiery in these contexts functions as a non-nereceivediable component of professional identity, insulating the category from complete erosion by athleisure trfinishs.

Revival of Vintage and Y2K Fashion Aesthetics Drives Youth Segment Reengagement

A resurgence of early 2000s and 1990s fashion has reintroduced hosiery to younger consumers through sheer tights, patterned knee highs, and fishnet styles popularized by social media influencers and music artists, which propels the expansion of the Europe hosiery market. European e-commerce shoppers are increasingly searching for sheer tights and patterned socks, driving a significant surge in interest for decorative legwear over the past few years. Brands like Wolford and Falke have capitalized on this by launching limited edition collections featuring retro motifs and bold denier contrasts, tarobtaining Gen Z through TikTok and Instagram campaigns. Driven by a culture of vintage styling, young Swedish women are purchaseing decorative hosiery at a significantly higher rate than they were several years ago. This trfinish reframes hosiery not as a conformity tool but as a vehicle for self-expression, enabling brands to diversify beyond utilitarian offerings. The cyclical nature of fashion ensures that even as minimalist aesthetics dominate, nostalgic revivals provide recurring demand pulses that sustain design innovation and retail relevance.

MARKET RESTRAINTS

Rising Temperature Trfinishs Reduce Winter Wear Duration Across Northern Europe

Climate modify is shortening the traditional hosiery season by elevating average winter temperatures across key markets, which restricts the growth of the Europe hosiery market. The Copernicus Climate Change Service indicates that average temperatures in Western and Central Europe have risen significantly during the cold season, resulting in a reduced required for heavy winter clothing. In addition, the German Weather Service (DWD) reports that, due to rising temperatures, the start of the heating season has been delayed significantly compared to previous decades, indicating shorter periods requiring cold-weather clothing. Consequently, retailers report compressed sales windows. Consumers increasingly opt for bare legs or lightweight alternatives even in professional settings, accelerating the shift toward year-round sock dominance. This environmental shift directly erodes the core seasonal volume engine of the hosiery market, forcing brands to either innovate in transitional products or accept structural demand contraction.

Consumer Perception of Hosiery as Non Essential Fuels Category Abandonment

Many European consumers, particularly younger demographics, view tights and stockings as outdated, uncomfortable, or unnecessary, which leads to declining habitual utilize, and thereby limits the expansion of the Europe hosiery market. A significant proportion of young European women are shifting away from regular tights usage, primarily driven by discomfort and a desire to challenge traditional, gfinishered, or restrictive clothing expectations. In the Netherlands, due to the widespread adoption of more casual workplace dress codes, formal hosiery is no longer considered a daily requirement for many office professionals. This attitudinal shift is reinforced by corporate policy modifys. Hosiery fails to match the comfort of bare legs or the utility of performance socks unless cultural or functional requireds dictate otherwise. This perception gap transforms what was once a wardrobe staple into a situational accessory, drastically narrowing its addressable market and weakening brand loyalty.

MARKET OPPORTUNITIES

Expansion of Performance and Wellness Oriented Hosiery Creates New Value Propositions

Innovation in functional textiles is repositioning hosiery as a wellness and performance product rather than purely aesthetic apparel, which provides new opportunities for the Europe hosiery market. Compression tights with graduated pressure profiles are gaining traction among active consumers for muscle recovery and circulation support. According to sources, the adoption of functional apparel, including compression wear, is rising among active individuals in Southern European fitness markets, such as Italy and Spain, as part of post-workout recovery routines. Brands like CEP and Sigvaris have expanded into lifestyle segments with stylish yet medically informed designs. Simultaneously, thermoregulating yarns infutilized with phase modify materials assist maintain leg comfort across variable indoor-outdoor temperatures, a key selling point in urban commuting. Research into occupational health in Germany indicates a growing emphasis on specialized, moisture-wicking, and antimicrobial workwear among nursing staff to manage physical fatigue and improve hygiene during long shifts. Transitioning hosiery from a trfinish-based product to a health-focutilized essential fosters lasting customer loyalty, driving repeat purchases among wellness-oriented shoppers.

Growth of Circular Business Models Enables Sustainable Premium Positioning

European hosiery brands are leveraging take back programs and recycled materials to align with tightening EU textile regulations and conscious consumerism, which provides fresh prospects for the Europe hosiery market. New European Union policies are forcing textile producers to take full responsibility for their products’ lifecycle, leading to mandatory nationwide waste collection and the establishment of producer-funded recycling systems. In anticipation of strict EU, legislation, sustainable fashion pioneers are partnering with major retail chains to implement widespread, consumer-facing recycling, often utilizing specialized, in-store take-back systems. The company utilizes regenerated nylon from fishing nets and industrial waste to produce new pantyhose, reducing reliance on virgin fossil feedstocks. A growing portion of European shoppers is increasingly displaying a preference for sustainable products, including premium, circular-certified hosiery, and are willing to pay a premium price for items that can be verified as environmentally responsible. Similarly, Italian brand OROBLÙ introduced biodegradable tights created from EVO plant based polymer that decompose in compost within five years. These initiatives transform hosiery from a disposable item into a responsible choice, justifying premium pricing and fostering brand loyalty in an era where sustainability is a baseline expectation rather than a differentiator.

MARKET CHALLENGES

Fragmented Sizing Standards Undermine Fit Consistency and Increase Returns

The absence of harmonized sizing across European hosiery brands leads to inconsistent fit experiences, which impedes the growth of the Europe hosiery market. This inconsistency drives high return rates and consumer frustration. Unlike footwear or apparel, hosiery sizing relies on height weight and shoe size combinations that vary significantly between manufacturers. A woman who wears size M in one brand may required L or S in another due to differing denier elasticity and knitting tension. According to European e-commerce reports, intimate apparel and hosiery categories consistently experience some of the highest online return rates, with improper fit cited as a leading factor. This trfinish is primarily driven by consumers purchasing multiple sizes for in-home trial due to the inability to test these products in-store. This inefficiency increases carbon footprint through reverse logistics and erodes profitability. Despite some brands like Wolford employing AI-driven virtual fit advisors, overall adoption is still low. The lack of EU mandated sizing guidelines for hosiery perpetuates this fragmentation, preventing the category from achieving the fit reliability seen in standardized garments, ultimately deterring trial and repeat purchase.

Depfinishence on Fossil Based Synthetic Fibers Contradicts EU Green Mandates

Most hosiery relies on nylon and elastane, petroleum derived polymers that are neither biodegradable nor easily recyclable, which places the sector at odds with the region’s decarbonization agfinisha, and thereby limits the hosiery market. The European Environment Agency confirms that the EU apparel market, including hosiery, relies heavily on virgin, non-renewable synthetic fibers with minimal recycled content. To combat this, the recently enacted EU Ecodesign for Sustainable Products Regulation will mandate digital product passports, compelling transparency regarding material composition and circularity. Furthermore, microplastic shedding during washing contributes to aquatic pollution. Despite the emergence of bio-based nylon, cost and technical hurdles hinder large-scale production. Hosiery firms face reputational risks and regulatory penalties until they adopt circular feedstocks and closed-loop collection, jeopardizing their long-term viability in a sustainability-focutilized market.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

2.65% |

|

Segments Covered |

By Product, End User, Distribution Channel, and Region |

|

Various Analyses Covered |

Global, Regional, & Counattempt Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

Wolford AG, Falke Group, Calzedonia Group, CSP International, Gatta, Golden Lady Company S.p.A., Kunert Group, Gerbe, Aristoc, Trerè Innovation S.p.A., Hanesbrands Inc., and Jockey International |

SEGMENTAL ANALYSIS

By Product Insights

The socks segment dominated the Europe hosiery market by accounting for a 48.3% share in 2025. The dominance of the socks segment is driven by leadership stems from universal utility across gfinishers, seasons, and occasions. Socks serve as a non nereceivediable undergarment for hygiene comfort and shoe compatibility regardless of age gfinisher or climate. Unlike tights or stockings which are often seasonal or gfinisher specific socks are worn daily by nearly every European. In colder regions like Sweden and Finland national health guidelines even recommfinish moisture wicking socks to prevent frostbite during winter commutes as documented by the Nordic Public Health Institute. The rise of athletic and wellness culture further amplifies demand. This foundational role as both a basic necessity and a performance enhancer ensures consistent volume uncorrelated with fashion cycles or workplace trfinishs. Modern socks transcfinish utility through specialized variants including compression recovery antimicrobial odor control and temperature regulating designs. Brands like Falke and CEP cater to runners cyclists and medical utilizers with graduated pressure profiles clinically proven to improve circulation. According to sources, a portion of gym members in Spain and Italy purchased technical socks in 2023. Simultaneously fashion driven segments thrive, limited edition collaborations between Stance and designers or football clubs generate collector interest particularly among youth. This dual identity as both essential gear and expressive accessory allows socks to capture value across mass premium and niche markets simultaneously sustaining dominance through versatility rather than volume alone.

The leggings segment is predicted to witness the highest CAGR of 9.4% between 2026 and 2034 due to blurred boundaries between activewear and everyday clothing. Leggings have transitioned from gym only garments to acceptable office and streetwear across much of Europe particularly among younger demographics. Increased flexibility in professional dress codes across Northern Europe has led more employers to accept versatile, comfortable garments, such as leggings styled with longer tops or tailored jackets, as appropriate business casual attire. Due to a strong cultural preference for comfort and practicality, Swedish women frequently incorporate leggings into daily, non-sporting outfits, though fashion preferences are shifting toward more varied, relaxed styles. Retailers reinforce this shift. This social acceptance transforms leggings from a category with limited utilize into a wardrobe staple competing directly with jeans and troutilizers for daily rotation. Modern leggings incorporate four way stretch moisture wicking and squat proof construction utilizing high denier nylon spandex blfinishs that resist pilling and sheerness. Brands like Björn Borg and Lindex utilize recycled ocean plastic yarns offering eco credentials without sacrificing performance. Additionally seamless knitting techniques eliminate chafing seams, a common complaint in early generations. These advancements address previous barriers of transparency discomfort and rapid degradation creating leggings viable for extfinished wear beyond short workout sessions. Higher fabric quality drives consumer demand for longer-lasting, higher-priced clothing, establishing a virtuous cycle of innovation and market adoption.

By End User Insights

The women segment led the Europe hosiery market by capturing a 62.5% share in 2025. The supremacy of the women’s segment is attributed to entrenched workplace and formal dress norms sustaining core demand, and to the expansion of wellness and aesthetic subsegments broadening its appeal. Despite evolving gfinisher dynamics many European institutions maintain implicit or explicit expectations for women to wear hosiery in professional settings. Many professional dress codes in France, particularly in corporate sectors, emphasize a “neat” appearance, which can be interpreted through traditional, sometimes gfinishered, expectations regarding attire in professional settings. In Ireland and Malta, some schools maintain traditional uniforms requiring skirts for girls, while in Germany, school uniforms are uncommon, with students generally choosing their own attire. This institutional continuity creates reliable seasonal spikes. Even as casualization spreads sectors like law diplomacy and hospitality retain formal standards preserving baseline demand. Unlike discretionary fashion choices hosiery in these contexts functions as a non optional component of professional presentation reinforcing consistent purchasing behavior across generations. Beyond traditional tights the women’s segment now includes shapewear compression therapy and beauty enhancing hosiery infutilized with microencapsulated vitamins or caffeine. Medical grade compression tights also gain traction. Germany’s statutory health insurers partially reimburse Class I compression wear for chronic venous insufficiency benefiting brands. This diversification transforms hosiery from a single purpose garment into a multifunctional tool addressing circulation aesthetics and confidence simultaneously. Integrating health science and beauty technology allows brands to relocate beyond seasonal relevance, turning products into essential daily self-care routines.

The men segment is estimated to register the rapidest CAGR of 7.8% over the forecast period owing to rising grooming consciousness and performance requireds. European men are investing more in appearance with hosiery emerging as a subtle yet impactful element of refined dressing. Luxury brands like Pantherella and Bresciani report double digit growth in fine gauge merino and silk blfinish socks marketed as “quiet luxury” accessories. Business professionals increasingly opt for over the calf styles to ensure no skin exposure when seated. This shift reflects broader male engagement with personal aesthetics shifting beyond basic functionality toward intentional styling. Hosiery is now a legitimate avenue for men’s fashion expression as vanity-related stigma dissolves. Men dominate participation in finishurance sports cycling and hiking creating strong demand for technical socks with cushioning arch support and blister prevention features. Brands like X Socks and Balega engineer zone specific padding and ventilation channels validated through biomechanical testing. Additionally, workplace safety regulations drive industrial sock sales. These functional requirements generate recurring B2B procurement cycles indepfinishent of fashion trfinishs. The men’s hosiery segment achieves stable, diversified growth by balancing style with utility, rfinishering it immune to the seasonal/cultural shifts that drive volatility in women’s hosiery.

By Distribution Channel Insights

The online retail stores segment held the majority share of 39.1% of the Europe hosiery market in 2025. The leading position of the online retail stores segment is credited to unmatched assortment and size accessibility that overcomes fit barriers, while algorithmic personalization and subscription models drive repeat engagement. Online platforms offer extensive size ranges color options and brand comparisons impossible in physical stores where shelf space limits stock keeping units. A customer seeking size 43 over the calf socks or maternity tights can find dozens of options on Zalando or Amazon whereas brick and mortar retailers typically carry only best sellers. Virtual attempt on tools and AI powered size recommfinishers further reduce fit uncertainty. This granularity caters to Europe’s diverse body types and preferences ensuring inclusivity that physical retail struggles to match. The ability to access niche products like diabetic or post surgical hosiery without specialist store visits adds critical utility beyond convenience. E commerce platforms leverage browsing and purchase history to suggest replenishment items before stocks run out. Amazon’s Subscribe & Save program enhanced customer loyalty and increased the overall value of subscribers for frequently purchased items like socks and apparel, according to data shared with partners. Zalando utilizes personalized feed technology to recommfinish new, tailored items, such as patterned hosiery, based on a utilizer’s previous fashion choices. Social commerce integrations allow direct checkout from Instagram and TikTok reducing friction for impulse purchases driven by influencer content. This closed loop of discovery recommfinishation and replenishment transforms hosiery from occasional shopping into habitual automated consumption aligning with modern digital lifestyles.

The specialty stores segment is anticipated to witness the rapidest CAGR of 8.2% between 2026 and 2034. The swift growth of the specialty stores segment is propelled by experiential retail and expert guidance. Specialty hosiery boutiques and pharmacy affiliated outlets provide professional fitting for compression therapy shapewear and custom orthopedic socks, categories where incorrect sizing compromises efficacy or safety. Staff trained in venous disorder assessment ensure proper pressure class and length selection reducing complications. Similarly, luxury brands like Wolford operate flagship stores with private consultation rooms where clients receive personalized advice on denier opacity and fiber content. This human expertise creates irreplaceable value in segments where performance and precision outweigh price sensitivity. Indepfinishent boutiques differentiate through ethical sourcing displaycasing compact batch producers utilizing organic cotton recycled nylon or biodegradable fibers. Stores like Les Sublimes in Paris or Sock Shop’s eco section in London highlight traceability storyinforming and local craftsmanship absent in mass retail. These stores host workshops on mfinishing and care extfinishing product life in alignment with EU circular economy goals. Specialty stores are ditching the checkout line for a relocatement! By turning shopping into a masterclass in shared values, they’re building ride-or-die community loyalty that keeps local economies thriving even in a world obsessed with screens.

REGIONAL ANALYSIS

Italy Hosiery Market Analysis

Italy outperformed other countries in the Europe hosiery market by accounting for a 22.6% share in 2025. The counattempt is globally renowned for its artisanal hosiery heritage centered in Castel Goffredo, the “hosiery capital of the world”, where family owned mills produce ultra fine denier tights for luxury houtilizes like Gucci and Prada. Italian brands such as OROBLÙ and Santini emphasize Made in Italy quality utilizing proprietary knitting techniques that achieve seamless finishes and superior elasticity. Italy remains a significant global exporter of knitted hosiery, with specialized garments reaching major European neighbors and, more recently, primary markets in the Adriatic region. Driven by a cultural emphasis on high-quality fashion, the domestic market for these garments remains resilient, while government initiatives focus on digital and sustainable innovation within the textile sector to maintain a global competitive edge.

Germany Hosiery Market Analysis

Germany followed closely in the Europe hosiery market by holding a share of 18.8% share in 2025. The rapid expansion of the German market is fuelled by its dominance in technical and therapeutic hosiery. The counattempt is home to global leaders like medi and Bauerfeind specializing in medical compression wear reimbursed by statutory health insurers. Simultaneously German consumers prioritize durability and function, Falke’s performance socks for hiking and skiing enjoy cult status across Alpine regions. The nation’s engineering mindset extfinishs to textiles. Research institutes like Hohenstein Laboratories develop standardized testing protocols for compression accuracy adopted EU wide. Retail is highly organized with pharmacies department stores and specialty chains offering expert fitting services. This blfinish of healthcare integration technical excellence and consumer pragmatism creates Germany the most structured and resilient hosiery market in Europe.

United Kingdom Hosiery Market Analysis

The United Kingdom is also a key player in the Europe hosiery market due to historic brands like Pretty Polly and Aristoc that pioneered commercial hosiery production. The UK serves as a high volume consumption hub driven by variable weather and persistent office dress norms. Supermarkets like Tesco and Boots dominate distribution offering affordable multipacks that drive houtilizehold penetration. At the same time the UK leads in e commerce adoption, ASOS and Boohoo report hosiery as a top five category by unit volume. This duality of budobtain accessibility and digital convenience sustains the UK’s role as Europe’s primary volume generator despite declining per capita usage in younger cohorts.

France Hosiery Market Analysis

France is shifting ahead steadrapidly in the Europe hosiery market owing to strong preference for designer hosiery and aesthetic innovation. Paris remains a global trfinishsetter where brands like Gerbe and Ozonee collaborate with haute couture houtilizes to create runway pieces that trickle down to ready to wear collections. Department stores like Galeries Lafayette dedicate entire floors to hosiery with personal stylists advising on shade matching and occasion appropriateness. The government’s plan allocated funds to preserve textile craftsmanship including hosiery knitting schools in Troyes. This fusion of artisattempt regulation and retail theater ensures France’s outsized influence in shaping premium hosiery aesthetics across the continent.

Sweden Hosiery Market Analysis

Sweden is anticipated to expand its share in the European hosiery market from 2026 to 2034. This growth is led by its commitment to circular economy practices and inclusive design. The counattempt is home to Swedish Stockings the first brand to produce hosiery from regenerated fishing nets and industrial waste now sold in numerous countries. Moreover, Sweden challenges gfinisher norms, unisex sock lines from brands like Happy Socks and Nudie Jeans promote gfinisher neutral legwear as standard. Minimalist aesthetics and functional dressing further favor opaque tights and performance socks over decorative styles. This combination of environmental responsibility social progressivism and practical design positions Sweden as a forward seeing indicator of hosiery’s future evolution in post traditional Europe.

COMPETITIVE LANDSCAPE

The Europe hosiery market features a layered competitive landscape where global luxury houtilizes coexist with agile rapid fashion retailers and specialized technical manufacturers. Competition is increasingly defined by values rather than price alone with sustainability transparency and functionality serving as key differentiators. Legacy brands like Wolford leverage heritage and craftsmanship to justify premium positioning while mass retailers such as Calzedonia compete on trfinish responsiveness and omnichannel convenience. Niche players focutilizing on medical compression or athletic performance carve out defensible segments through clinical validation and B2B partnerships. New entrants face high barriers due to consumer expectations for fit reliability fiber quality and ethical sourcing yet digital native brands gain traction through social media storyinforming and circular propositions. Regulatory pressures including the EU Strategy for Sustainable Textiles further reshape strategies pushing incumbents toward innovation in recyclability and extfinished producer responsibility. This dynamic environment rewards adaptability authenticity and deep understanding of regional cultural norms around legwear.

KEY MARKET PLAYERS

Some of the notable key players in the Europe hosiery market are

- Wolford AG

- Falke Group

- Calzedonia Group

- CSP International

- Gatta

- Golden Lady Company S.p.A.

- Kunert Group

- Gerbe

- Aristoc

- Trerè Innovation S.p.A.

- Hanesbrands Inc.

- Jockey International

Top Players in the Market

- Wolford AG is an Austrian headquartered luxury hosiery and bodywear brand renowned for its premium tights stockings and shapewear across Europe. The company combines artisanal knitting techniques with innovative materials such as EcoVero and recycled nylon to cater to high finish consumers seeking both elegance and sustainability. Wolford maintains a strong presence through its flagship stores in major European capitals as well as partnerships with luxury department stores like Harrods and Galeries Lafayette. In recent years the company has strengthened its position by launching a circularity program that collects utilized garments for recycling and by introducing biodegradable hosiery lines created from plant based polymers. It also enhanced its digital experience with virtual attempt on technology and personalized styling consultations via its e commerce platform.

- Calzedonia Group is an Italian retail giant operating over 2,000 stores across Europe under brands including Calzedonia Intimissimi and Tezenis. The company dominates the mass premium hosiery segment with extensive product ranges covering tights socks and legwear for all seasons and demographics. Calzedonia leverages vertical integration from design to distribution ensuring rapid response to fashion trfinishs and consistent quality control. To reinforce its market leadership the group has invested heavily in sustainable sourcing introducing collections created from regenerated nylon and organic cotton. It also expanded its omnichannel capabilities by integrating in store inventory with online platforms enabling click and collect services across numerous European countries. Additionally, Calzedonia launched seasonal recycling bins in partnership with municipal waste authorities to support EU circular textile goals.

- Falke KGaA is a German family owned manufacturer specializing in high quality socks tights and functional legwear with a legacy spanning over 125 years. The company serves both consumer and professional markets offering performance oriented products for sports medical and business utilize. Falke’s strength lies in technical innovation including moisture wicking antimicrobial and compression technologies validated through collaborations with sports federations and healthcare institutions. In recent years Falke has reinforced its European footprint by modernizing its production facilities to reduce water and energy consumption and by achieving bluesign certification for its entire hosiery line. The company also introduced AI powered size recommfinishation tools on its e commerce sites to reduce returns and enhance customer satisfaction across diverse European body types.

Top Strategies Used by the Key Market Participants

Key players in the Europe hosiery market are prioritizing sustainable material innovation by replacing virgin synthetics with recycled ocean plastics bio based yarns and certified renewable fibers to comply with EU textile regulations. They are investing in circular business models including take back programs garment recycling and resale platforms to extfinish product lifecycles. Companies are enhancing digital engagement through virtual fitting tools AI driven size advisors and personalized replenishment subscriptions to reduce returns and boost loyalty. Strategic retail expansion focutilizes on experiential flagship stores with expert fitting services particularly for medical and premium segments. Additionally they are diversifying into performance and wellness categories such as compression therapy temperature regulating fabrics and gfinisher neutral designs to capture emerging consumer requireds beyond traditional fashion cycles.

MARKET SEGMENTATION

This research report on the European hosiery market has been segmented and sub-segmented based on categories.

By Product

- Socks

- Stockings

- Tights

- Leggings

- Others

By End User

By Distribution Channel

- Supermarket/Hypermarket

- Specialty Stores

- Online Retail Stores

- Others

By Counattempt

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Leave a Reply